Shift4 (FOUR)

Shift4 is a special business. Its revenue is growing quickly while its profitability is rising, giving it multiple ways to win.― StockStory Analyst Team

1. News

2. Summary

Why We Like Shift4

Starting as a payment gateway provider in 1999 and now processing over $200 billion in annual payment volume, Shift4 Payments (NYSE:FOUR) provides integrated payment processing solutions and software that help businesses accept and manage transactions across in-store, online, and mobile channels.

- Market share has increased this cycle as its 40.4% annual revenue growth over the last five years was exceptional

- Additional sales over the last five years increased its profitability as the 72.1% annual growth in its earnings per share outpaced its revenue

- Stellar return on equity showcases management’s ability to surface highly profitable business ventures

Shift4 is a standout company. The valuation seems reasonable relative to its quality, and we believe now is the time to invest.

Why Is Now The Time To Buy Shift4?

At $41.68 per share, Shift4 trades at 7.5x forward P/E. The valuation sure appears attractive, and we suspect the stock is trading below its intrinsic value when factoring in its business quality.

Our eyes light up when companies with elite fundamentals trade at bargain prices because shareholders can benefit from both earnings growth and a positive re-rating - a powerful one-two punch.

3. Shift4 (FOUR) Research Report: Q4 CY2025 Update

Payment processing company Shift4 Payments (NYSE:FOUR) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 34% year on year to $1.19 billion. On the other hand, next quarter’s revenue guidance of $547.5 million was less impressive, coming in 51.6% below analysts’ estimates. Its non-GAAP profit of $1.60 per share was in line with analysts’ consensus estimates.

Shift4 (FOUR) Q4 CY2025 Highlights:

- Volume: $59 billion

- Revenue: $1.19 billion vs analyst estimates of $1.19 billion (34% year-on-year growth, in line)

- Pre-tax Profit: $67 million (5.6% margin)

- Adjusted EPS: $1.60 vs analyst estimates of $1.60 (in line)

- Revenue Guidance for Q1 CY2026 is $547.5 million at the midpoint, below analyst estimates of $1.13 billion

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.60 at the midpoint, missing analyst estimates by 13.2%

- Market Capitalization: $3.95 billion

Company Overview

Starting as a payment gateway provider in 1999 and now processing over $200 billion in annual payment volume, Shift4 Payments (NYSE:FOUR) provides integrated payment processing solutions and software that help businesses accept and manage transactions across in-store, online, and mobile channels.

Shift4's technology ecosystem extends beyond basic payment processing to include a proprietary gateway that connects with over 500 software platforms, point-of-sale systems, and business intelligence tools. The company serves merchants ranging from small local businesses to multinational enterprises, with particular strength in hospitality, food and beverage, entertainment venues, and retail sectors.

The company's revenue model primarily consists of processing fees charged as a percentage of payment volume or per transaction, supplemented by subscription fees for its software solutions. For merchants, Shift4 offers two main service options: gateway-only services that connect to third-party processors, or comprehensive end-to-end payment solutions that consolidate multiple payment functions through a single vendor.

Shift4's product portfolio includes SkyTab POS workstations for restaurants and retailers, VenueNext technology for stadiums and entertainment venues, Lighthouse business intelligence tools for analytics and customer engagement, and Shift4Shop for eCommerce. The company also offers specialized solutions like The Giving Block, which facilitates cryptocurrency donations to charities.

Following its acquisition of Finaro in 2023, Shift4 expanded its international presence, particularly in Europe and the UK. This acquisition added cross-border payment capabilities and banking services through Finaro's licensed credit institution in Malta, allowing Shift4 to offer merchants localized settlement in multiple currencies and access to alternative payment methods popular in international markets.

4. Payment Processing

Payment processors facilitate transactions between merchants, consumers, and financial institutions. Growth comes from e-commerce expansion, declining cash usage globally, and value-added services beyond basic processing. Headwinds include margin pressure from merchant negotiating power, rapid technological change requiring investment, and emerging competition from technology companies entering the payments ecosystem.

Shift4 Payments competes with traditional payment processors like Chase Paymentech, Elavon, FIS, Fiserv, and Global Payments, as well as integrated payment providers such as Adyen, Lightspeed POS, Shopify, Square, and Toast. In the hospitality gateway space, its main competitors include Elavon and FreedomPay.

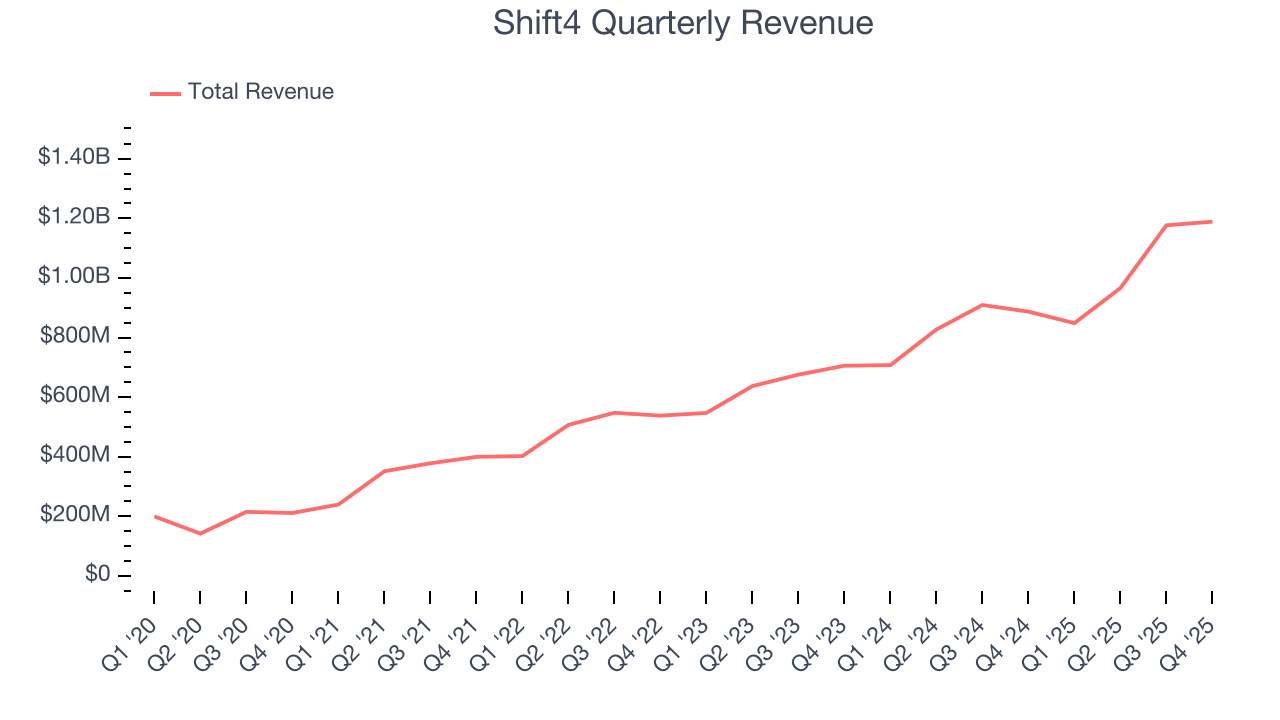

5. Revenue Growth

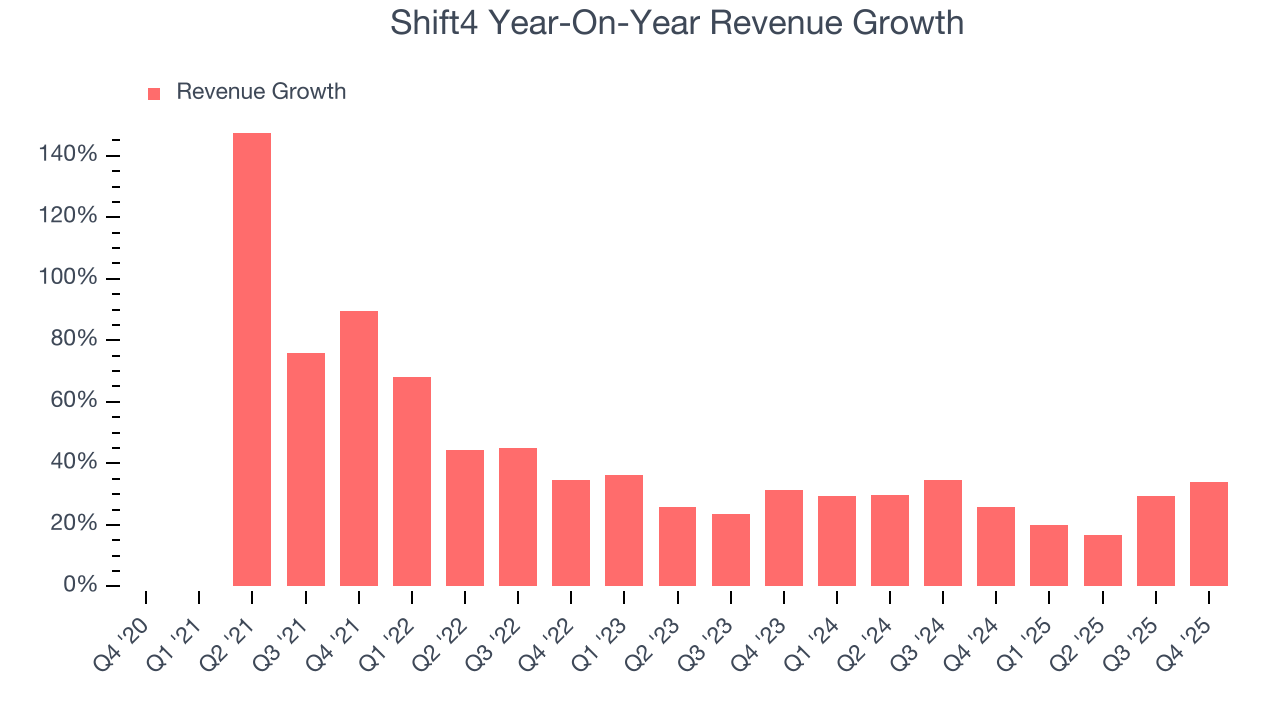

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Shift4’s 40.4% annualized revenue growth over the last five years was incredible. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Shift4’s annualized revenue growth of 27.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Shift4’s year-on-year revenue growth of 34% was wonderful, and its $1.19 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 35.5% year-on-year decline in sales next quarter.

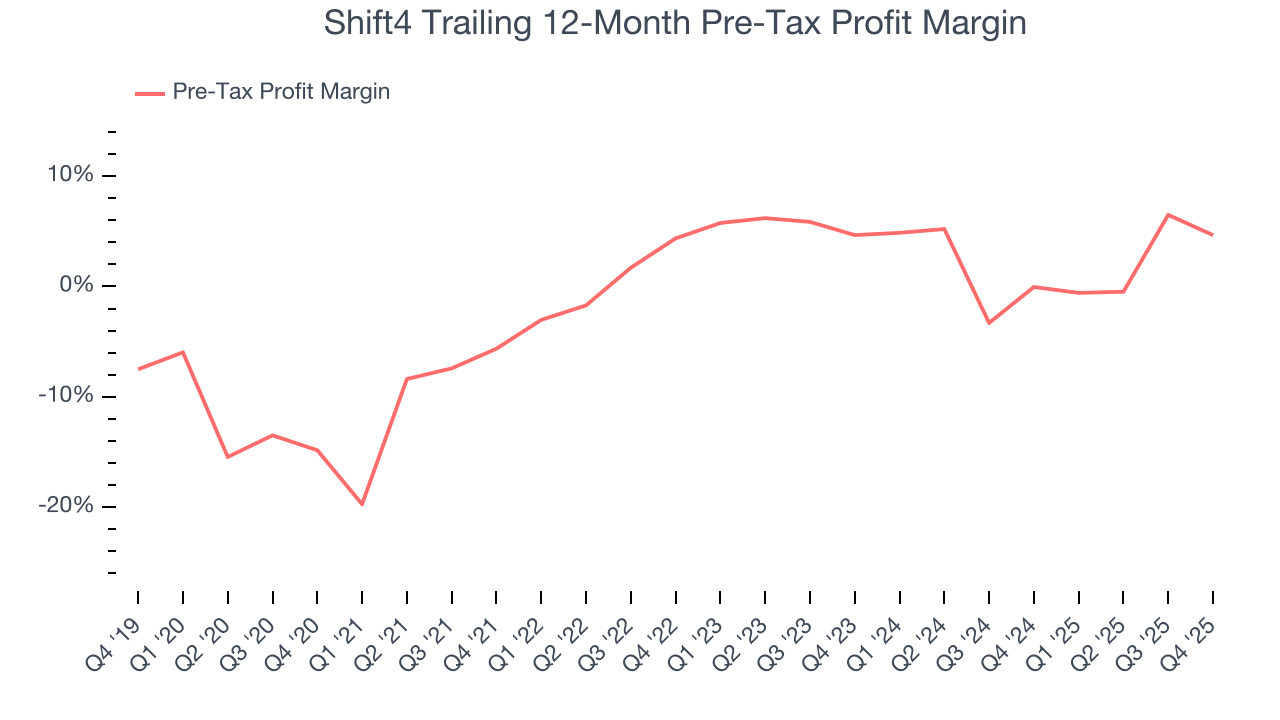

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Payment Processing companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because for financials businesses, interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company's control - should not.

Over the last five years, Shift4’s pre-tax profit margin has fallen by 19.5 percentage points, going from negative 5.6% to 4.7%. However, fixed cost leverage was muted more recently as the company’s pre-tax profit margin was flat on a two-year basis.

Shift4’s pre-tax profit margin came in at 5.6% this quarter. This result was 8.4 percentage points worse than the same quarter last year.

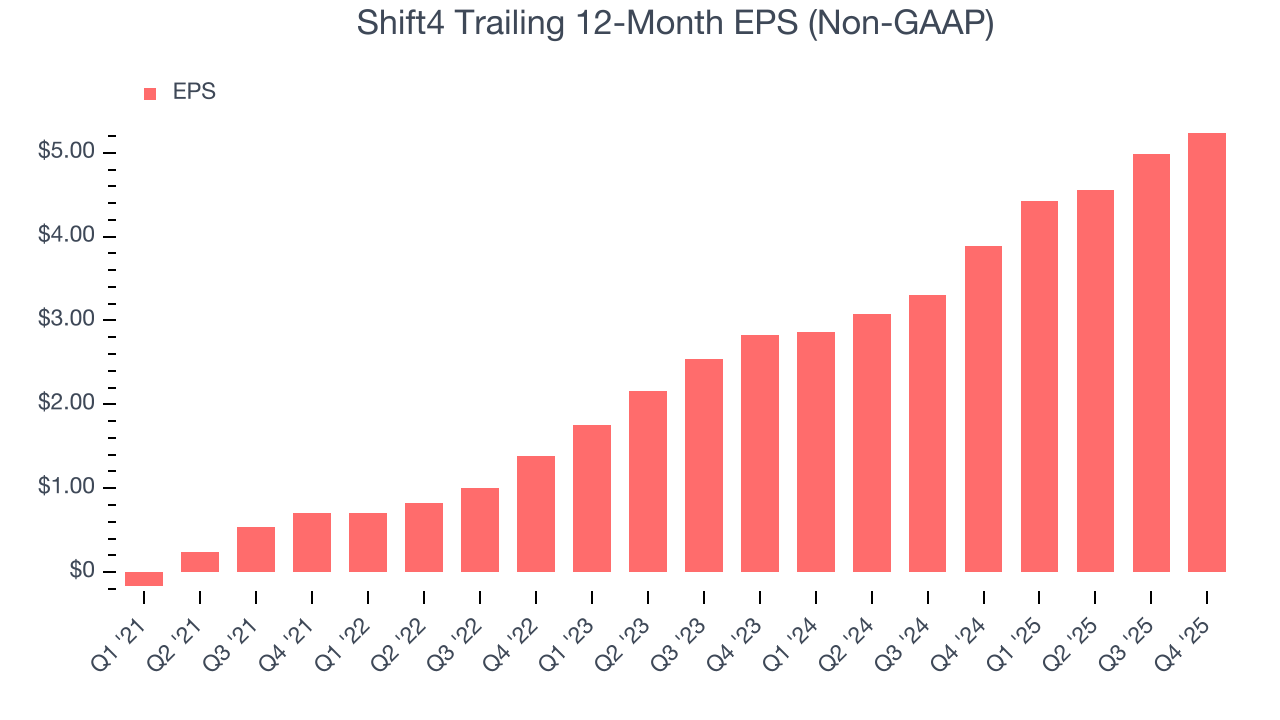

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Shift4’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Shift4’s EPS grew at an astounding 36.1% compounded annual growth rate over the last two years, higher than its 27.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Shift4 reported adjusted EPS of $1.60, up from $1.35 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Shift4’s full-year EPS of $5.24 to grow 21.6%.

8. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Shift4 has averaged an ROE of 14.4%, healthy for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Shift4 has a decent competitive moat.

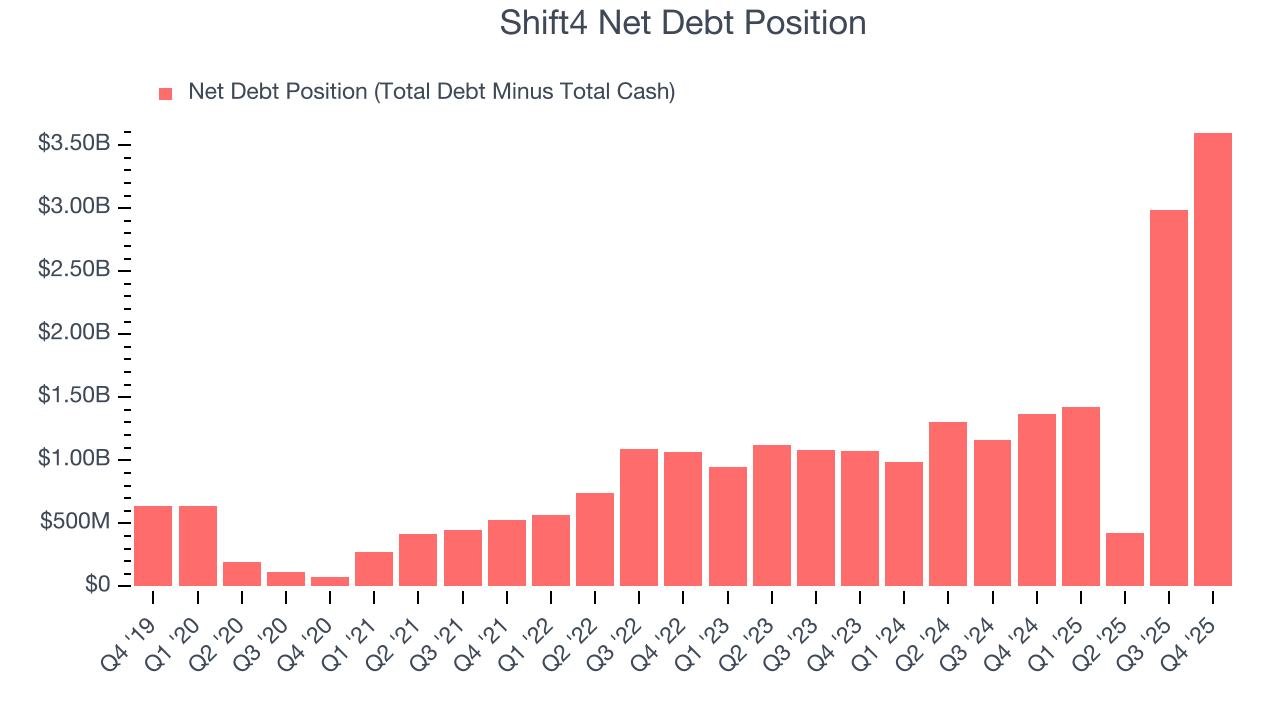

9. Balance Sheet Assessment

Shift4 reported $964 million of cash and $4.56 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $969.7 million of EBITDA over the last 12 months, we view Shift4’s 3.7× net-debt-to-EBITDA ratio as safe. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from Shift4’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.6% to $56.43 immediately after reporting.

11. Is Now The Time To Buy Shift4?

Updated: March 23, 2026 at 12:04 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

There is a lot to like about Shift4. For starters, its revenue growth was exceptional over the last five years. On top of that, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, and its expanding pre-tax profit margin shows the business has become more efficient.

Shift4’s P/E ratio based on the next 12 months is 7.5x. Analyzing the financials landscape today, Shift4’s positive attributes shine bright. We think it’s one of the best businesses in our coverage and love the stock at this bargain price.

Wall Street analysts have a consensus one-year price target of $65.96 on the company (compared to the current share price of $41.68), implying they see 58.3% upside in buying Shift4 in the short term.