NCR Atleos (NATL)

NCR Atleos is interesting. Its annual EPS growth of 16.4% over the last three years has topped its peer group.― StockStory Analyst Team

1. News

2. Summary

Why NCR Atleos Is Interesting

Spun off from NCR Voyix in 2023 to focus exclusively on self-service banking technology, NCR Atleos (NYSE:NATL) provides self-directed banking solutions including ATM and interactive teller machine technology, software, services, and a surcharge-free ATM network for financial institutions and retailers.

- Earnings per share grew by 16.4% annually over the last three years and easily exceeded the peer group average

- On the flip side, its flat sales over the last three years suggest it must find different ways to grow during this cycle

NCR Atleos shows some potential. If you’ve been itching to buy the stock, the valuation seems reasonable.

3. NCR Atleos (NATL) Research Report: Q4 CY2025 Update

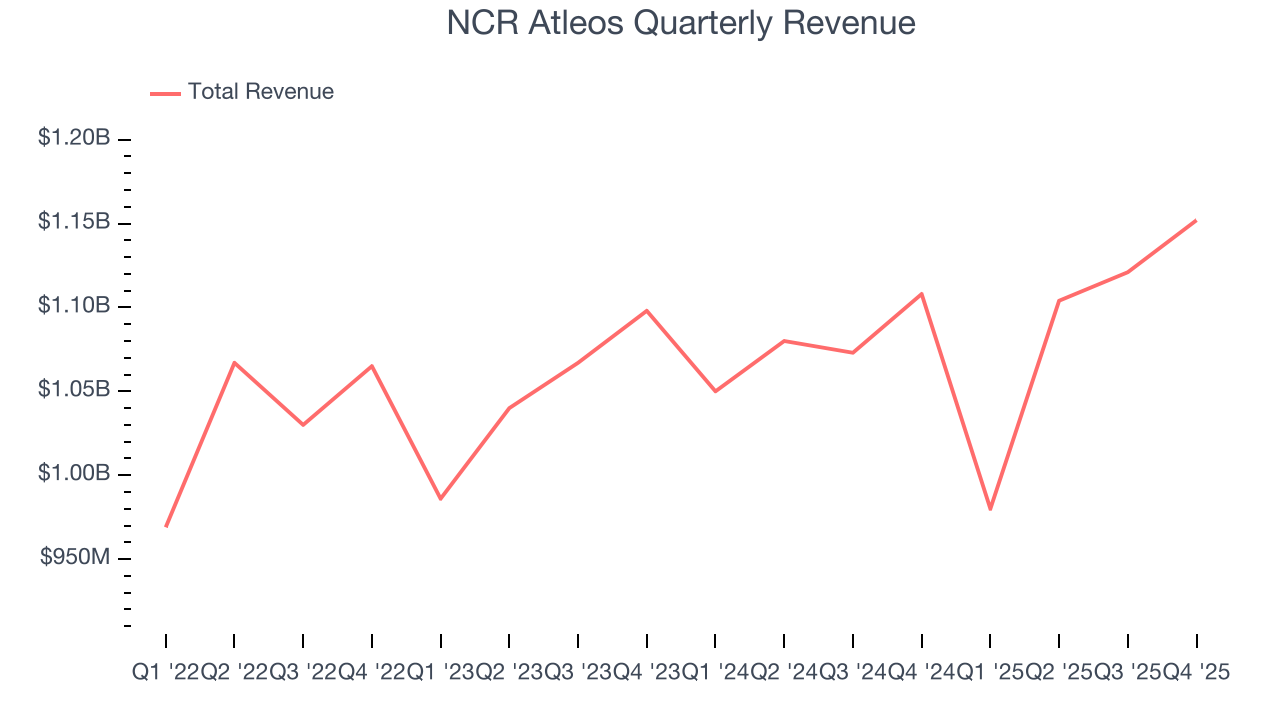

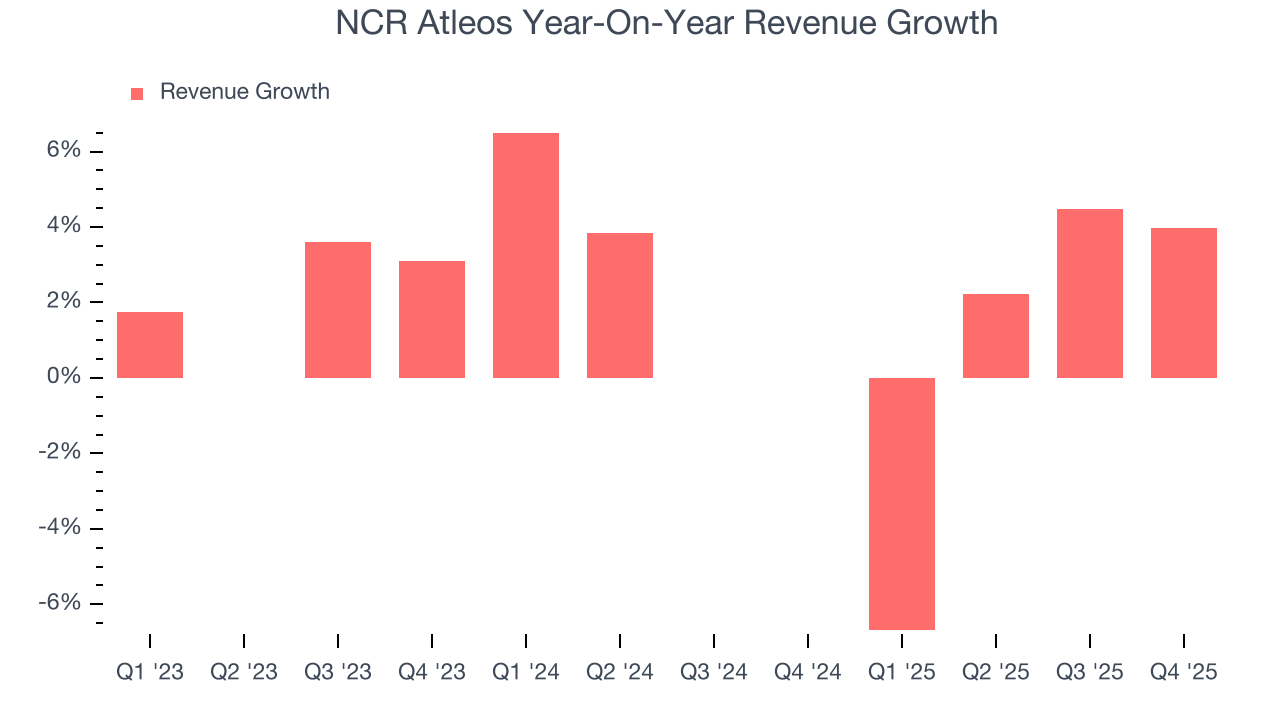

Financial technology company NCR Atleos (NYSE:NATL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 4% year on year to $1.15 billion. Its GAAP profit of $1.09 per share was 11.2% above analysts’ consensus estimates.

NCR Atleos (NATL) Q4 CY2025 Highlights:

- Revenue: $1.15 billion vs analyst estimates of $1.15 billion (4% year-on-year growth, in line)

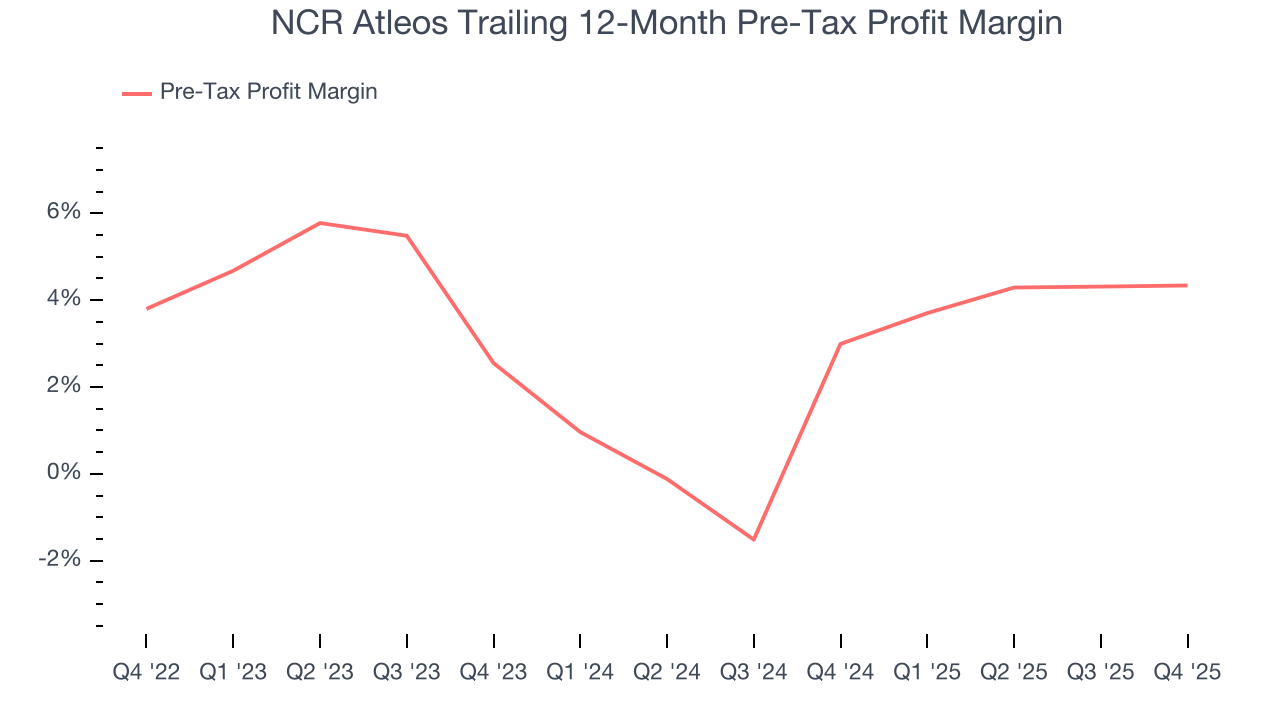

- Pre-tax Profit: $77 million (6.7% margin)

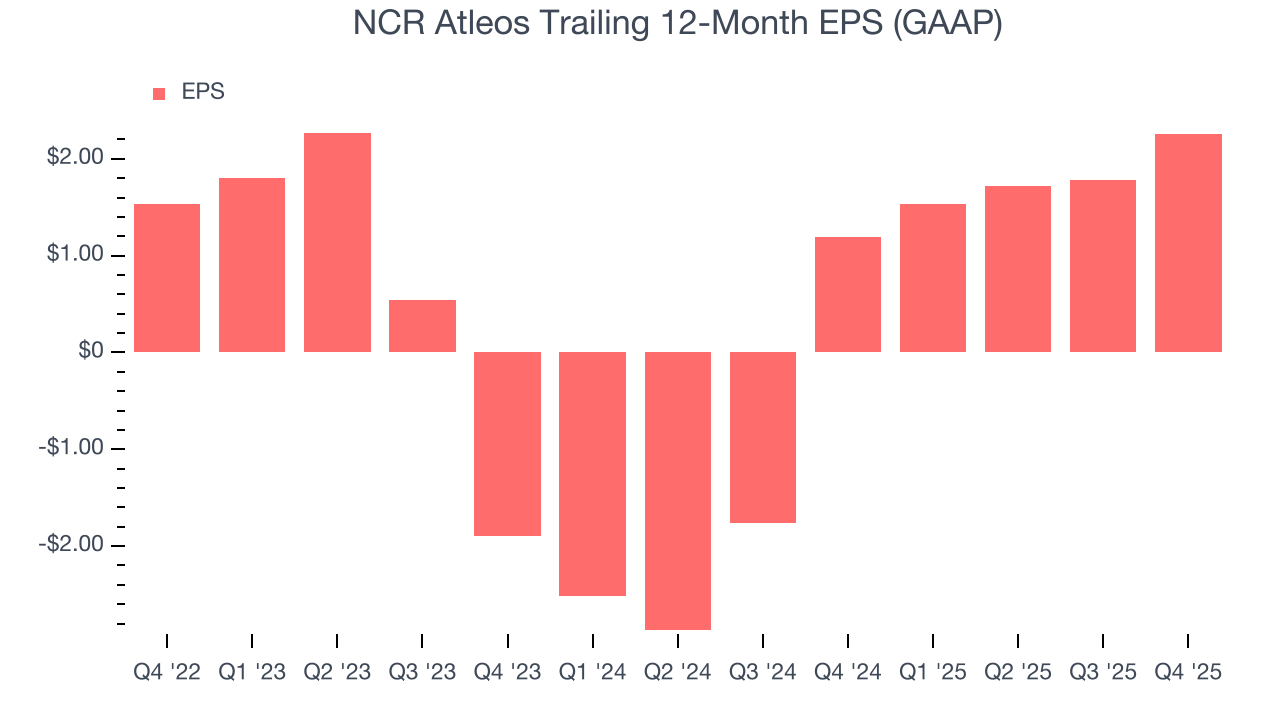

- EPS (GAAP): $1.09 vs analyst estimates of $0.98 (11.2% beat)

- Market Capitalization: $3 billion

Company Overview

Spun off from NCR Voyix in 2023 to focus exclusively on self-service banking technology, NCR Atleos (NYSE:NATL) provides self-directed banking solutions including ATM and interactive teller machine technology, software, services, and a surcharge-free ATM network for financial institutions and retailers.

NCR Atleos operates at the intersection of banking and technology, enabling financial institutions to transform traditional branch models into more efficient self-service experiences. The company's comprehensive platform includes hardware (ATMs and ITMs), software, managed services, and access to its Allpoint network—the largest retail surcharge-free ATM network in the United States with approximately 83,000 locations.

The company serves two primary customer groups. For financial institutions, NCR Atleos provides the technology and services to offer their customers convenient banking without requiring full-service branches. Its interactive teller machines (ITMs) allow remote bank employees to assist customers via video with complex transactions like account opening and loan applications. For retailers, the company's solutions create in-store banking destinations that drive foot traffic and reduce labor costs associated with financial service desks.

NCR Atleos generates revenue through multiple streams: selling hardware, licensing software on subscription models, providing managed services (including its comprehensive "ATM as a Service" offering), collecting transaction fees, and through branding arrangements where financial institutions pay to place their logos on company-owned ATMs. This diversified revenue model includes significant recurring components through long-term contracts.

The company's strategy focuses on increasing transaction volumes at existing locations while expanding its footprint globally. It's also transitioning toward more software-led solutions, with its Digital First ATM software platform enabling modern user experiences across both proprietary and third-party hardware. This cloud-based platform includes microservices and APIs that integrate with customers' systems, allowing NCR Atleos to earn a greater proportion of recurring revenues.

4. Diversified Financial Services

Diversified financial services encompass specialized offerings outside traditional categories. These firms benefit from identifying niche market opportunities, developing tailored financial products, and often facing less direct competition. Challenges include scale limitations, regulatory classification uncertainties, and the need to continuously innovate to maintain market differentiation against larger competitors expanding their offerings.

NCR Atleos competes with global ATM software, services, and hardware providers including Fiserv (NASDAQ:FISV), Euronet Worldwide (NASDAQ:EEFT), Diebold Nixdorf (OTC:DDBDF), as well as Cord Financial, Brinks (NYSE:BCO), and Hyosung.

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, NCR Atleos struggled to consistently increase demand as its $4.36 billion of revenue for the trailing 12 months was close to its revenue three years ago. This wasn’t a great result, but there are still things to like about NCR Atleos.

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. NCR Atleos’s annualized revenue growth of 2% over the last two years is above its three-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, NCR Atleos grew its revenue by 4% year on year, and its $1.15 billion of revenue was in line with Wall Street’s estimates.

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Diversified Financial Services companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Financials companies manage interest-bearing assets and liabilities, making the interest income and expenses included in pre-tax profit essential to their profit calculation. Taxes, being external factors beyond management control, are appropriately excluded from this alternative margin measure.

Over the last two years, NCR Atleos’s pre-tax profit margin has fallen by 1.8 percentage points, going from 2.6% to 4.3%. Said differently, the company’s expenses have grown at a slower rate than revenue, which typically signals prudent management.

In Q4, NCR Atleos’s pre-tax profit margin was 6.7%. This result was in line with the same quarter last year.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

NCR Atleos’s EPS grew at a remarkable 16.4% compounded annual growth rate over the last three years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

In Q4, NCR Atleos reported EPS of $1.09, up from $0.61 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects NCR Atleos’s full-year EPS of $2.26 to grow 48.3%.

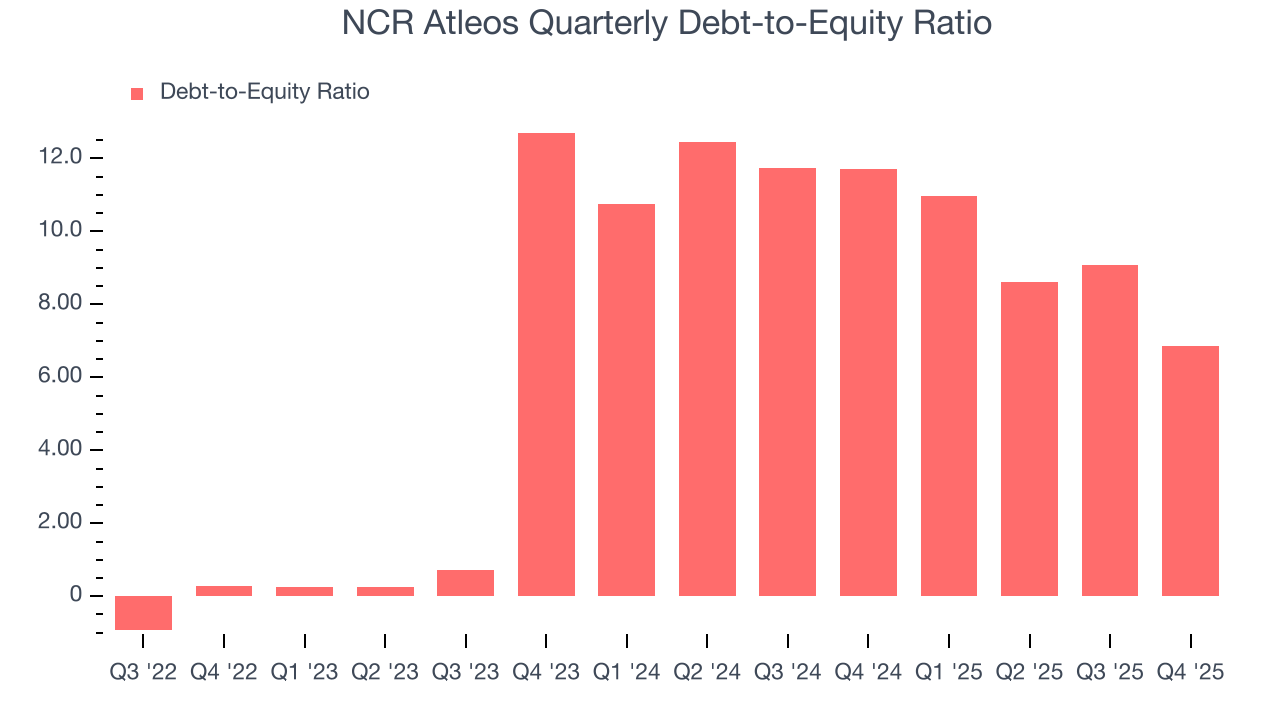

8. Balance Sheet Risk

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

NCR Atleos currently has $2.76 billion of debt and $402 million of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 8.9×. We think this is dangerous - for a financials business, anything above 3.5× raises red flags.

9. Key Takeaways from NCR Atleos’s Q4 Results

It was good to see NCR Atleos beat analysts’ EPS expectations this quarter. Overall, this print had some key positives. The stock traded up 9.2% to $45.74 immediately after reporting.

10. Is Now The Time To Buy NCR Atleos?

Updated: March 14, 2026 at 12:37 AM EDT

Before investing in or passing on NCR Atleos, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are things to like about NCR Atleos. Although its revenue growth was weak over the last three years, its growth over the next 12 months is expected to be higher. On top of that, NCR Atleos’s remarkable EPS growth over the last three years shows its profits are trickling down to shareholders, and the company’s expanding pre-tax profit margin shows the business has become more efficient.

NCR Atleos’s P/E ratio based on the next 12 months is 9.1x. Looking at the financials space right now, NCR Atleos trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $50.27 on the company (compared to the current share price of $44.12), implying they see 13.9% upside in buying NCR Atleos in the short term.