Payoneer (PAYO)

We love companies like Payoneer. Its superb revenue growth indicates its market share is increasing.― StockStory Analyst Team

1. News

2. Summary

Why We Like Payoneer

Founded during the early days of global e-commerce in 2005 to solve international payment challenges, Payoneer (NASDAQ:PAYO) provides financial technology services that enable small and medium-sized businesses to send and receive payments globally across borders.

- Market share has increased this cycle as its 26.3% annual revenue growth over the last five years was exceptional

- Incremental sales significantly boosted profitability as its annual earnings per share growth of 24.6% over the last two years outstripped its revenue performance

- The stock is slightly expensive, but we’d argue it’s often wise to hold onto high-quality businesses for the long term

We see a bright future for Payoneer. This is a fantastic business you don’t see often.

Is Now The Time To Buy Payoneer?

Payoneer is trading at $4.54 per share, or 18.2x forward P/E. There are high expectations given this pricey multiple; we can’t deny that.

Do you like the business model and believe in the company’s future? If so, you can own a smaller position, as our work shows that high-quality companies outperform the market over a multi-year period regardless of valuation at entry.

3. Payoneer (PAYO) Research Report: Q4 CY2025 Update

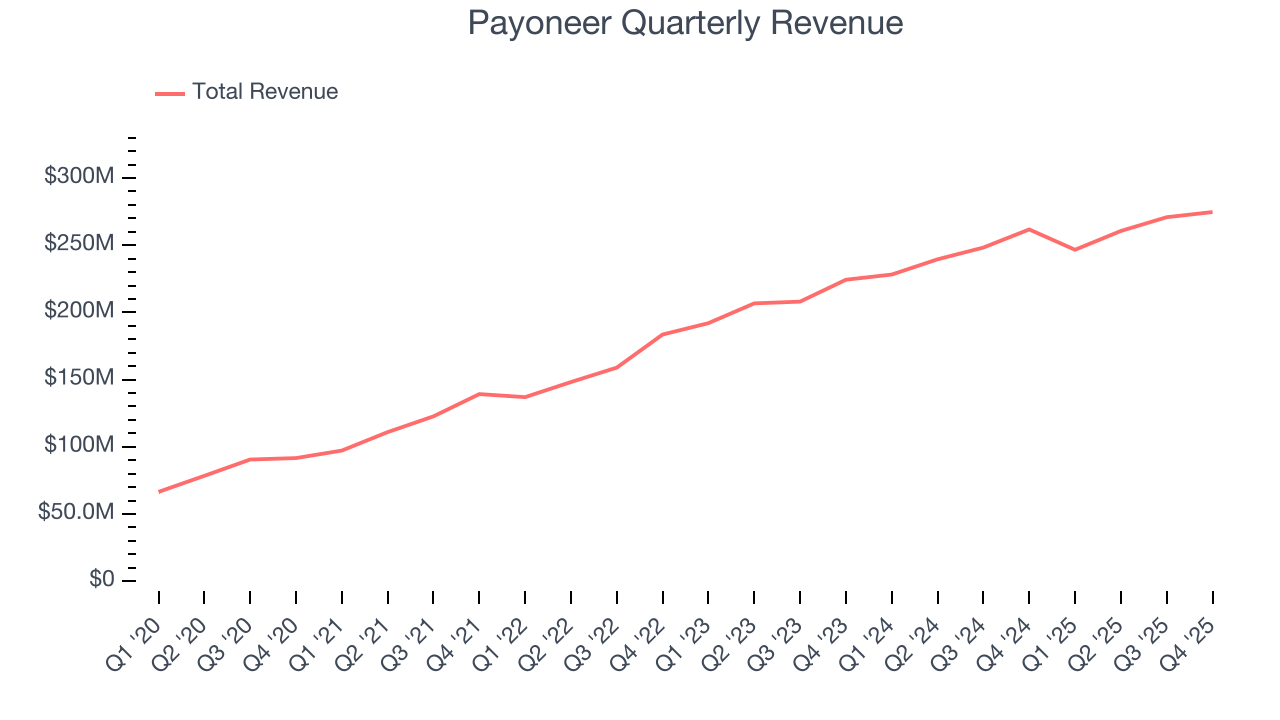

Cross-border payment platform Payoneer (NASDAQ:PAYO) fell short of the market’s revenue expectations in Q4 CY2025 as sales rose 4.9% year on year to $274.7 million. The company’s full-year revenue guidance of $1.11 billion at the midpoint came in 1.7% below analysts’ estimates. Its GAAP profit of $0.05 per share was in line with analysts’ consensus estimates.

Payoneer (PAYO) Q4 CY2025 Highlights:

- Revenue: $274.7 million vs analyst estimates of $281.6 million (4.9% year-on-year growth, 2.5% miss)

- Pre-tax Profit: $27.46 million (10% margin)

- EPS (GAAP): $0.05 vs analyst estimates of $0.06 (in line)

- Market Capitalization: $1.87 billion

Company Overview

Founded during the early days of global e-commerce in 2005 to solve international payment challenges, Payoneer (NASDAQ:PAYO) provides financial technology services that enable small and medium-sized businesses to send and receive payments globally across borders.

At the heart of Payoneer's offering is its multi-currency account, which functions as a comprehensive financial stack for cross-border commerce. This account allows businesses to receive payments from international marketplaces, direct business clients, and consumers, while also managing outgoing payments to suppliers and vendors worldwide. Users can hold balances in multiple currencies, convert funds at competitive rates, and access their money through local bank withdrawals or Payoneer-issued physical and virtual cards.

The company serves diverse customer segments, including e-commerce sellers on global marketplaces, business-to-business service providers, freelancers, and direct-to-consumer merchants. For example, a handcraft producer in India might use Payoneer to receive payments from customers in Europe and the United States, then use those funds to pay for raw materials from suppliers in China—all without the complexity and high fees typically associated with traditional international banking.

Payoneer generates revenue through transaction fees, currency conversion spreads, and interest on customer balances. It also offers additional services like working capital loans to qualified merchants, invoice management tools, and mass payout solutions for enterprises that need to pay multiple recipients globally. The company's platform connects to approximately 100 banking and payment service providers worldwide, enabling transactions across over 7,000 trade corridors with same-day settlement capabilities in more than 150 countries.

Operating in a highly regulated industry, Payoneer maintains licenses in multiple jurisdictions, including money transmitter licenses in U.S. states and payment service authorizations in regions like the European Economic Area, the United Kingdom, Australia, and Japan.

4. Diversified Financial Services

Diversified financial services encompass specialized offerings outside traditional categories. These firms benefit from identifying niche market opportunities, developing tailored financial products, and often facing less direct competition. Challenges include scale limitations, regulatory classification uncertainties, and the need to continuously innovate to maintain market differentiation against larger competitors expanding their offerings.

Payoneer competes with other cross-border payment providers like Wise (LSE:WISE), PayPal (NASDAQ:PYPL), and Stripe (private), as well as traditional banks offering international wire transfers and specialized B2B payment platforms such as Flywire (NASDAQ:FLYW) and Adyen (AMS:ADYEN).

5. Revenue Growth

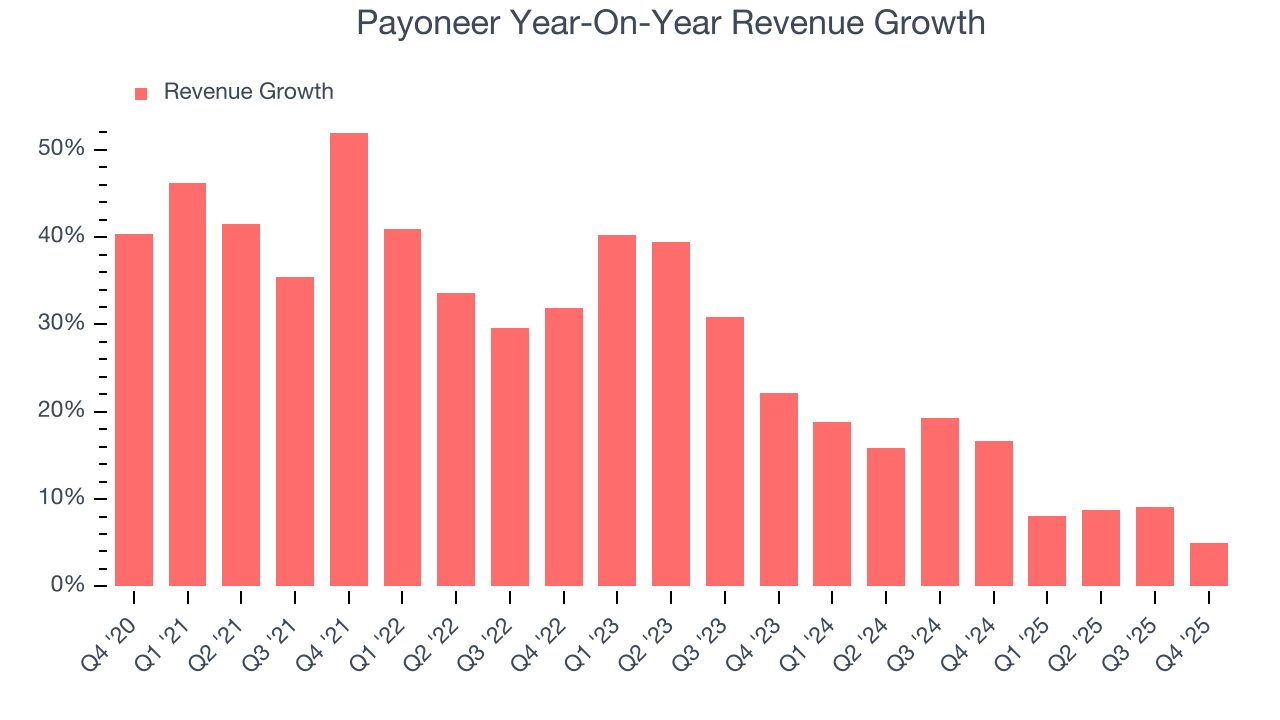

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Payoneer grew its revenue at an incredible 26.3% compounded annual growth rate. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Payoneer’s annualized revenue growth of 12.5% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Payoneer’s revenue grew by 4.9% year on year to $274.7 million, falling short of Wall Street’s estimates.

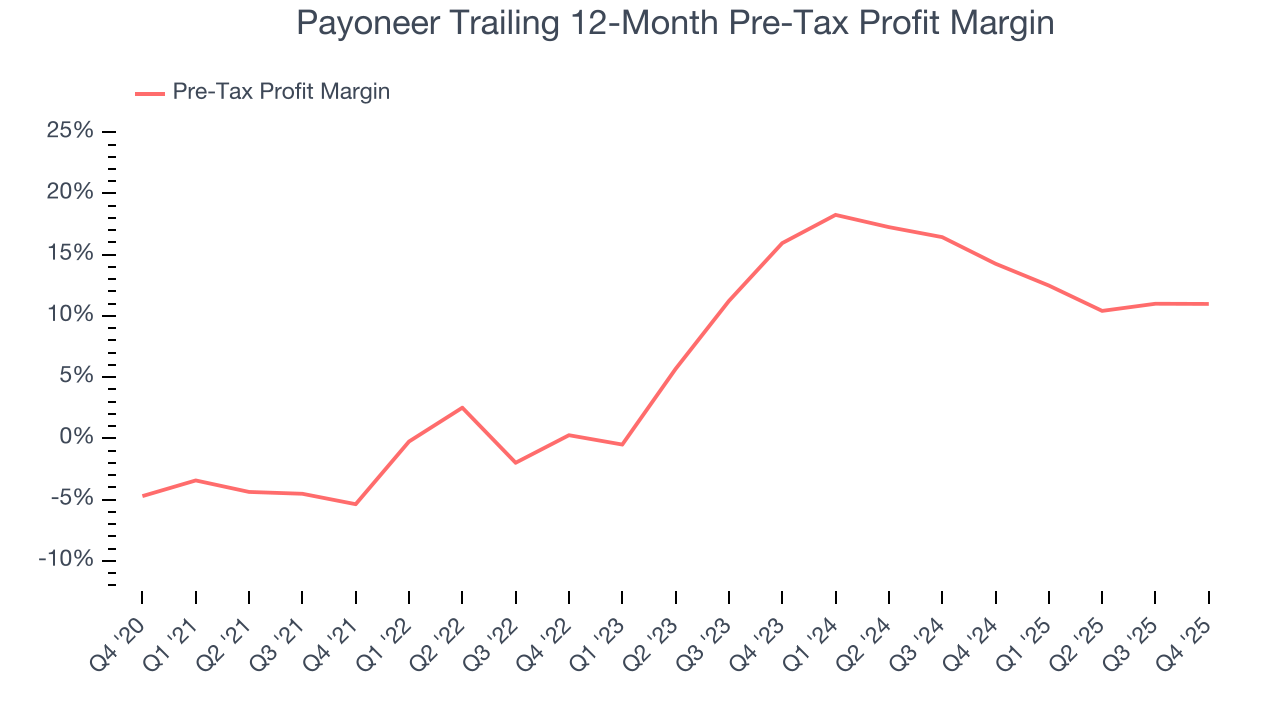

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Diversified Financial Services companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Interest income and expenses play a big role in financial institutions' profitability, so they should be factored into the definition of profit. Taxes, however, should not as they are largely out of a company's control. This is pre-tax profit by definition.

Over the last five years, Payoneer’s pre-tax profit margin has fallen by 15.7 percentage points, going from negative 5.4% to 11%. However, the company gave back some of its expense savings as its pre-tax profit margin declined by 5 percentage points on a two-year basis.

Payoneer’s pre-tax profit margin came in at 10% this quarter. This result was in line with the same quarter last year.

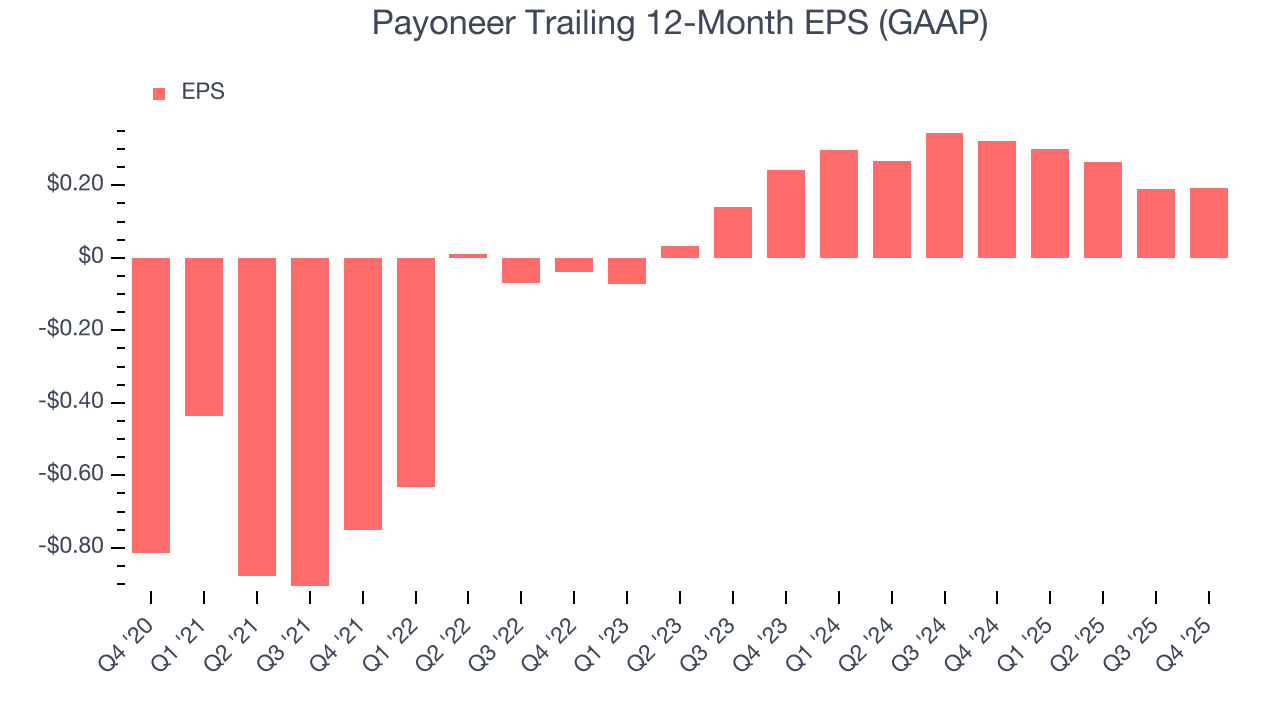

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Payoneer’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Payoneer, its EPS declined by 11% annually over the last two years while its revenue grew by 12.5%. This tells us the company became less profitable on a per-share basis as it expanded.

Diving into the nuances of Payoneer’s earnings can give us a better understanding of its performance. While we mentioned earlier that Payoneer’s pre-tax profit margin was flat this quarter, a two-year view shows its margin has declined. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Payoneer reported EPS of $0.05, in line with the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Payoneer’s full-year EPS of $0.19 to grow 50%.

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Payoneer has averaged an ROE of 6.1%, uninspiring for a company operating in a sector where the average shakes out around 10%. We’re optimistic Payoneer can turn the ship around given its success in other measures of financial health.

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Payoneer has no debt, so leverage is not an issue here.

10. Key Takeaways from Payoneer’s Q4 Results

We struggled to find many positives in these results. Its EPS was in line and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9.4% to $4.75 immediately after reporting.

11. Is Now The Time To Buy Payoneer?

Updated: March 14, 2026 at 12:35 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Payoneer.

Payoneer is an amazing business ranking highly on our list. For starters, its revenue growth was exceptional over the last five years. And while its mediocre ROE lags the market and is a headwind for its stock price, its expanding pre-tax profit margin shows the business has become more efficient. Additionally, Payoneer’s spectacular EPS growth over the last four years shows its profits are trickling down to shareholders.

Payoneer’s P/E ratio based on the next 12 months is 18.2x. This multiple isn’t necessarily cheap, but we’ll happily own Payoneer as its fundamentals shine bright. Investments like this should be held patiently for at least three to five years as they benefit from the power of long-term compounding, which more than makes up for any short-term price volatility that comes with relatively high valuations.

Wall Street analysts have a consensus one-year price target of $7.71 on the company (compared to the current share price of $4.54).