Western Union (WU)

Western Union keeps us up at night. Its sales and profitability have plummeted, suggesting it struggled to scale down its costs as demand faded.― StockStory Analyst Team

1. News

2. Summary

Why We Think Western Union Will Underperform

With a history dating back to 1851 when it began as a telegraph company, Western Union (NYSE:WU) is a global money transfer service that enables consumers and businesses to send funds across borders and currencies, typically within minutes.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 2.9% annually over the last five years

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- A bright spot is that its industry-leading 168% return on equity demonstrates management’s skill in finding high-return investments

Western Union’s quality doesn’t meet our bar. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Western Union

At $9.56 per share, Western Union trades at 5.4x forward P/E. Western Union’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Western Union (WU) Research Report: Q4 CY2025 Update

Money transfer company Western Union (NYSE:WU) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 3.1% year on year to $1.01 billion. Its non-GAAP profit of $0.45 per share was 4% above analysts’ consensus estimates.

Western Union (WU) Q4 CY2025 Highlights:

- Revenue: $1.01 billion vs analyst estimates of $1.04 billion (3.1% year-on-year decline, 3.3% miss)

- Pre-tax Profit: $151.1 million (15% margin)

- Adjusted EPS: $0.45 vs analyst estimates of $0.43 (4% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.80 at the midpoint, beating analyst estimates by 0.5%

- Market Capitalization: $3 billion

Company Overview

With a history dating back to 1851 when it began as a telegraph company, Western Union (NYSE:WU) is a global money transfer service that enables consumers and businesses to send funds across borders and currencies, typically within minutes.

Western Union operates through a vast network of approximately 400,000 agent locations spanning more than 200 countries and territories. These agents include post offices, banks, retailers, and independent businesses that serve as the physical touchpoints where customers can initiate or collect money transfers. The company also offers digital services through its website and mobile applications, allowing customers to send money online using credit cards, debit cards, or bank accounts.

The company's core business revolves around cross-border remittances, where individuals send money to family members or friends in different countries. For example, a migrant worker in the United States might use Western Union to send part of their paycheck to support relatives in Mexico, with the recipient collecting cash at a local agent location by presenting identification and a transaction code.

Western Union generates revenue primarily through transaction fees and foreign exchange spreads—the difference between the exchange rate offered to customers and wholesale market rates. The company's business model relies on the global mobility of people and the resulting need to move money across borders. Beyond consumer money transfers, which account for about 90% of its revenue, Western Union offers bill payment services, money orders, and digital wallet capabilities in select markets.

The company maintains long-standing relationships with its top agents, many of whom have partnered with Western Union for over two decades. These established partnerships, combined with Western Union's brand recognition and compliance infrastructure, create a resilient global network for moving money.

4. Diversified Financial Services

Diversified financial services encompass specialized offerings outside traditional categories. These firms benefit from identifying niche market opportunities, developing tailored financial products, and often facing less direct competition. Challenges include scale limitations, regulatory classification uncertainties, and the need to continuously innovate to maintain market differentiation against larger competitors expanding their offerings.

Western Union's primary competitors include MoneyGram International, Wise (formerly TransferWise), PayPal (NASDAQ:PYPL), and Remitly (NASDAQ:RELY), along with regional players and traditional banks offering international wire transfers. The company also faces growing competition from fintech startups and digital payment platforms.

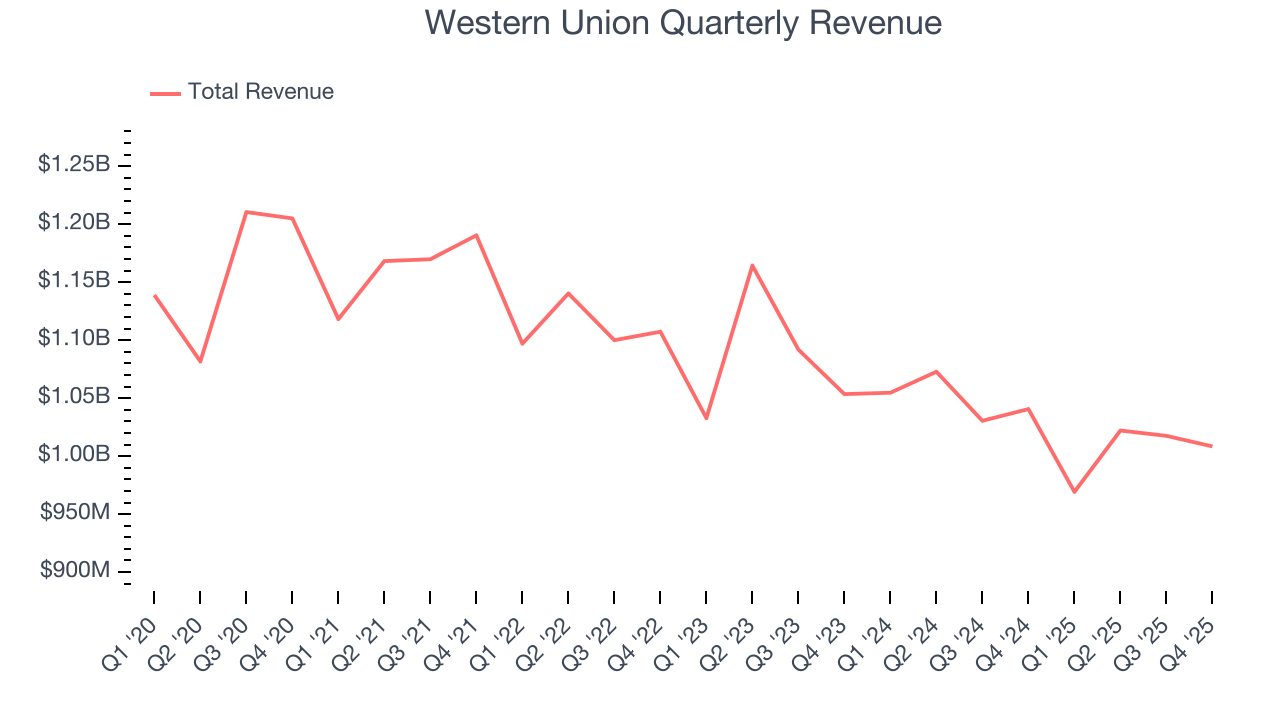

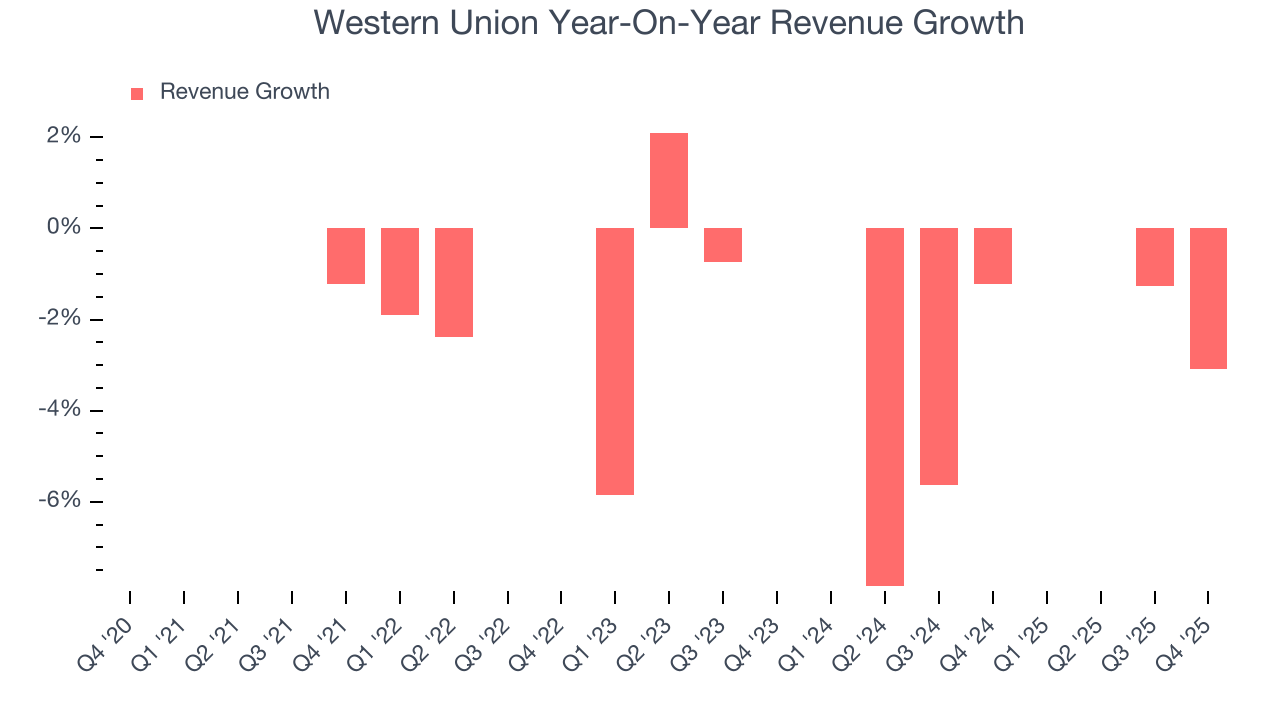

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Western Union’s demand was weak and its revenue declined by 2.8% per year. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Western Union’s annualized revenue declines of 3.8% over the last two years align with its five-year trend, suggesting its demand has consistently shrunk.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Western Union missed Wall Street’s estimates and reported a rather uninspiring 3.1% year-on-year revenue decline, generating $1.01 billion of revenue.

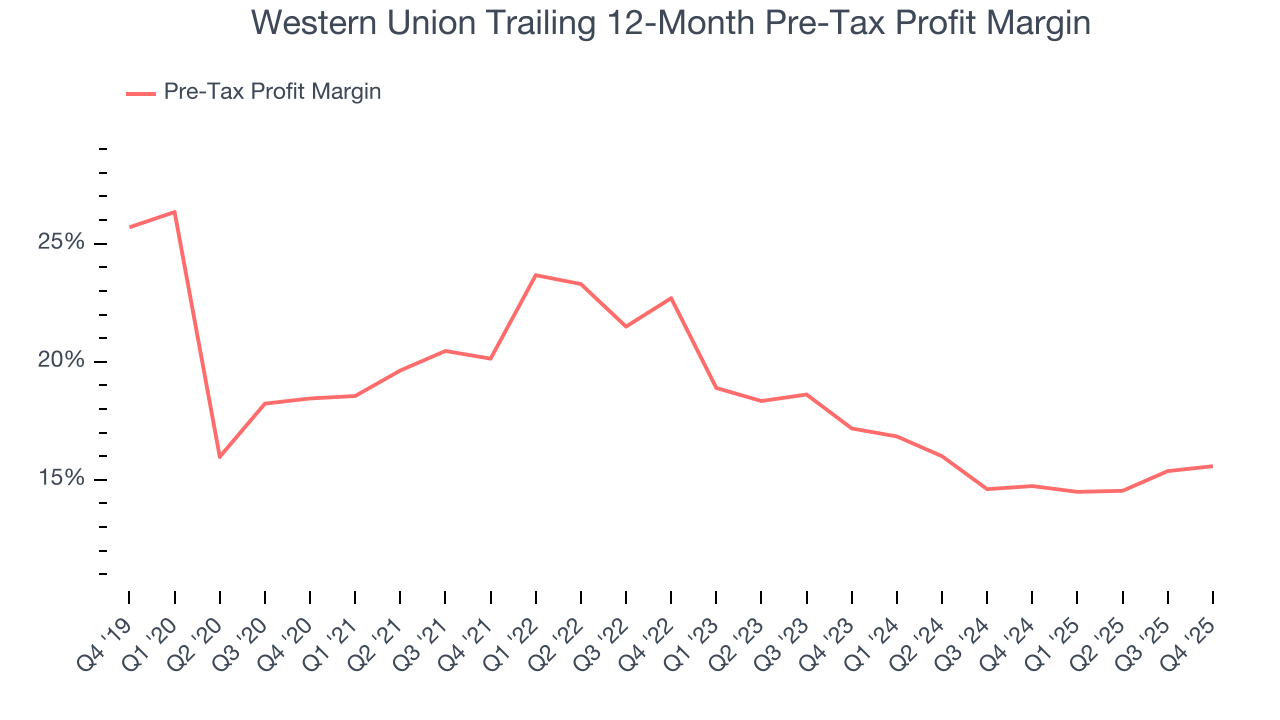

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Diversified Financial Services companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last five years, Western Union’s pre-tax profit margin has risen by 2.9 percentage points, going from 20.1% to 15.6%. It has also declined by 1.6 percentage points on a two-year basis, showing its expenses have consistently increased at a faster rate than revenue. This usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

Western Union’s pre-tax profit margin came in at 15% this quarter. This result was in line with the same quarter last year.

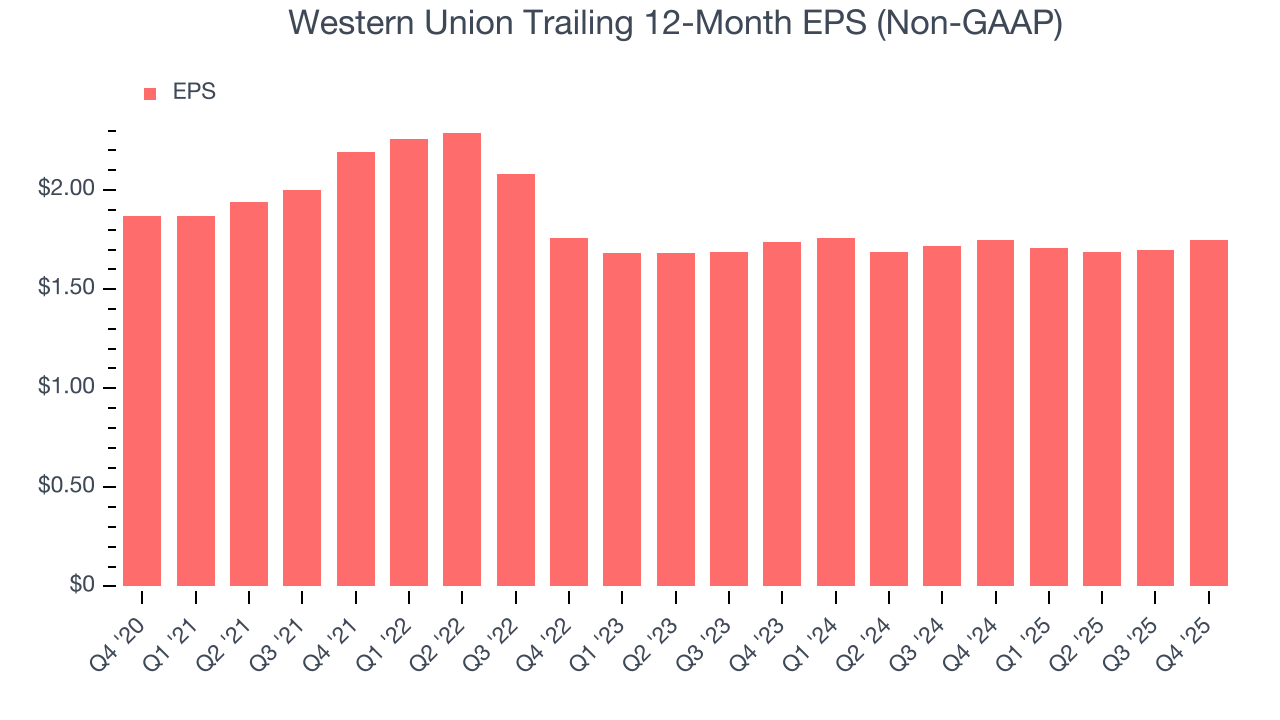

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Western Union, its EPS and revenue declined by 1.3% and 2.8% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Western Union’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Although it wasn’t great, Western Union’s flat two-year EPS topped its two-year revenue performance.

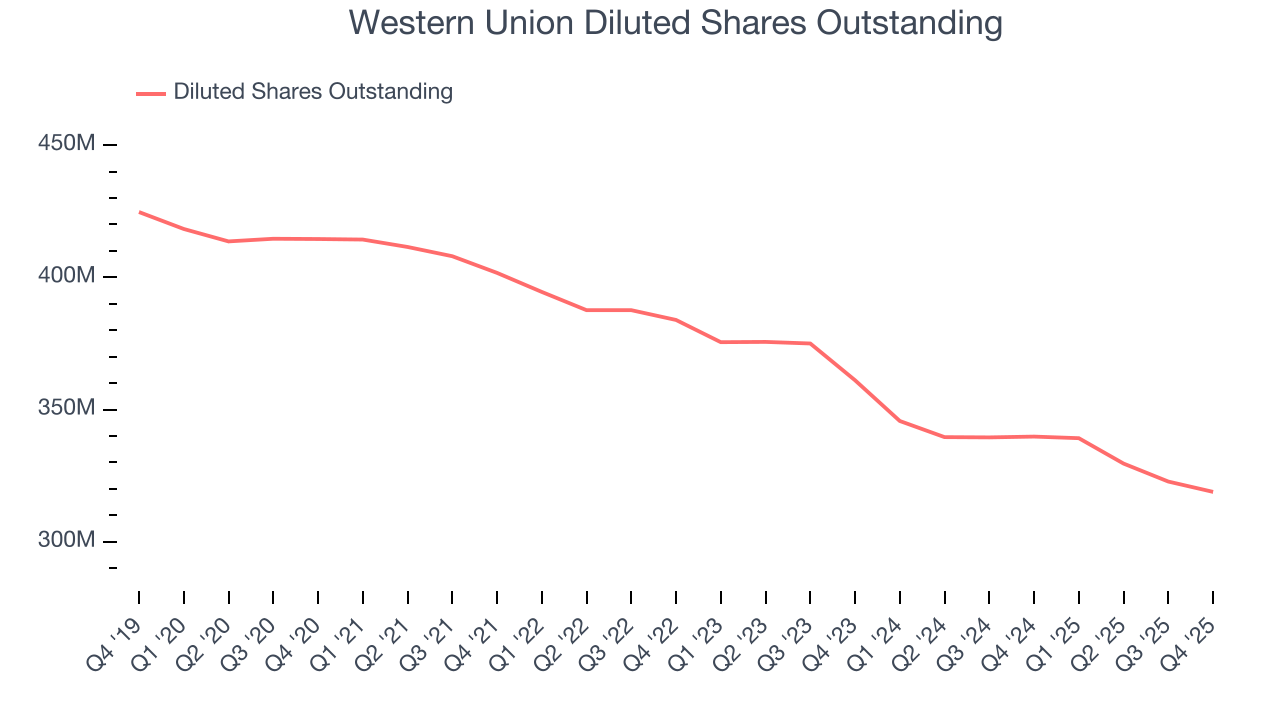

Diving into the nuances of Western Union’s earnings can give us a better understanding of its performance. A two-year view shows that Western Union has repurchased its stock, shrinking its share count by 11.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Western Union reported adjusted EPS of $0.45, up from $0.40 in the same quarter last year. This print beat analysts’ estimates by 4%. Over the next 12 months, Wall Street expects Western Union’s full-year EPS of $1.75 to grow 2.5%.

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Western Union has averaged an ROE of 174%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for Western Union.

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

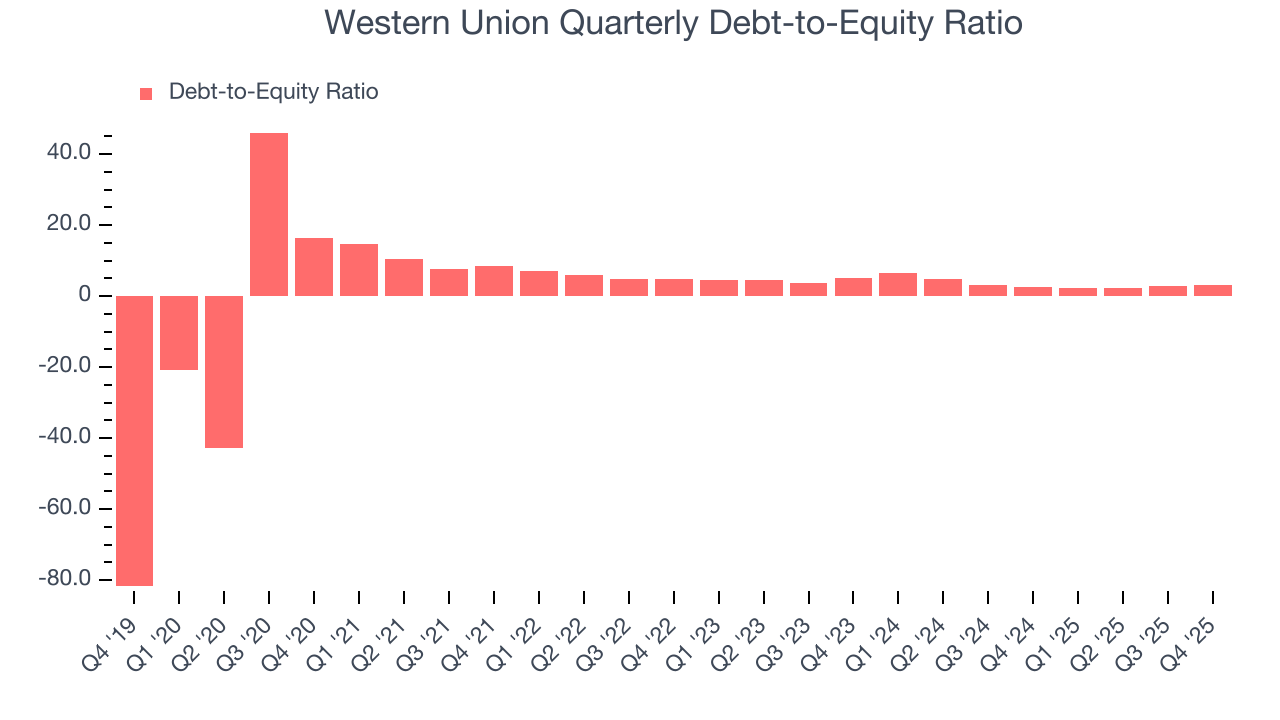

Western Union currently has $2.88 billion of debt and $957.8 million of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 2.6×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from Western Union’s Q4 Results

It was good to see Western Union beat analysts’ EPS expectations this quarter. We were also glad its full-year EPS guidance slightly exceeded Wall Street’s estimates. On the other hand, its revenue missed. Overall, this was a mixed quarter. The stock traded down 2.6% to $9.20 immediately following the results.

11. Is Now The Time To Buy Western Union?

Updated: March 14, 2026 at 12:27 AM EDT

When considering an investment in Western Union, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Western Union doesn’t pass our quality test. To begin with, its revenue has declined over the last five years. While its stellar ROE suggests it has been a well-run company historically, the downside is its declining pre-tax profit margin shows the business has become less efficient. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Western Union’s P/E ratio based on the next 12 months is 5.4x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $9.62 on the company (compared to the current share price of $9.56).