Globe Life (GL)

We’re skeptical of Globe Life. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Globe Life Is Not Exciting

With roots dating back to 1900 and a rebranding from Torchmark Corporation in 2019, Globe Life (NYSE:GL) is an insurance holding company that offers life insurance, supplemental health insurance, and annuity products through various distribution channels.

- Policy losses and capital returns have eroded its book value per share this cycle as its book value per share declined by 2.2% annually over the last five years

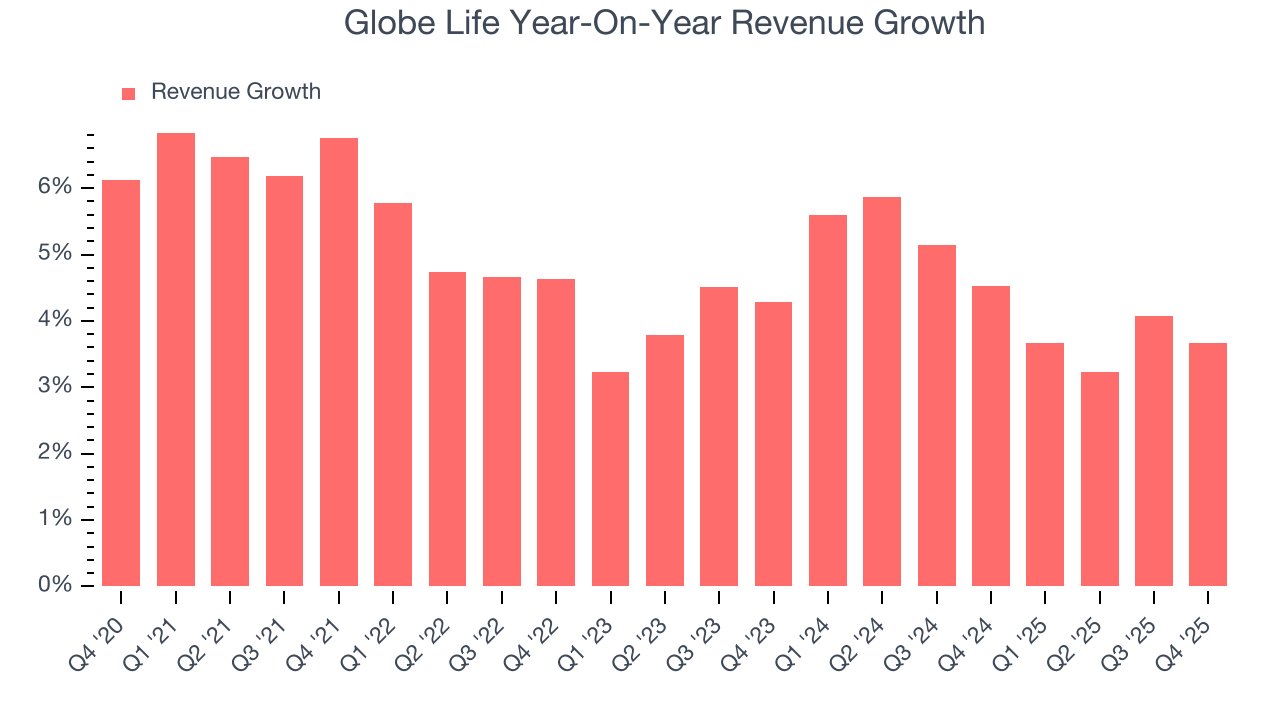

- 4.9% annual revenue growth over the last five years was slower than its insurance peers

- On the bright side, its exciting book value per share outlook for the upcoming 12 months calls for 43.7% growth, an acceleration from its two-year trend

Globe Life’s quality is not up to our standards. There are more promising alternatives.

Why There Are Better Opportunities Than Globe Life

Globe Life’s stock price of $138.48 implies a valuation ratio of 1.6x forward P/B. While valuation is appropriate for the quality you get, we’re still not buyers.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Globe Life (GL) Research Report: Q4 CY2025 Update

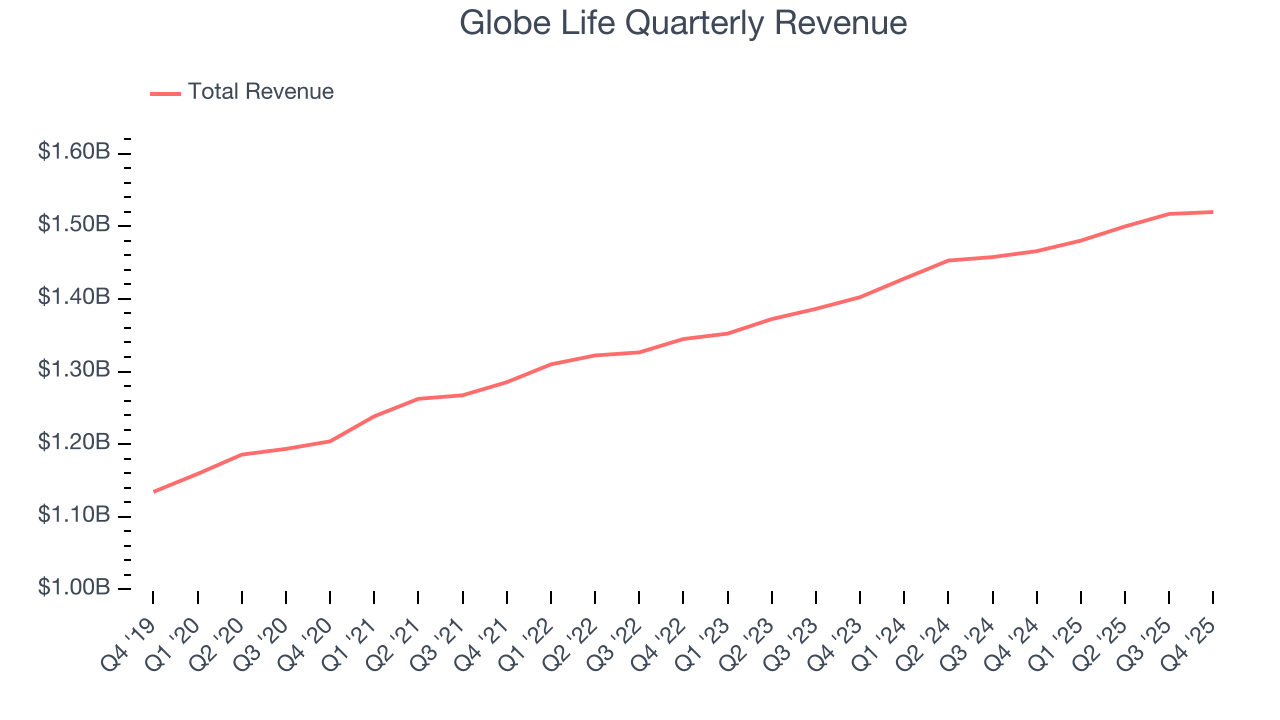

Insurance holding company Globe Life (NYSE:GL) fell short of the market’s revenue expectations in Q4 CY2025 as sales rose 3.7% year on year to $1.52 billion. Its GAAP profit of $3.29 per share was 3.2% below analysts’ consensus estimates.

Globe Life (GL) Q4 CY2025 Highlights:

- Net Premiums Earned: $1.24 billion vs analyst estimates of $1.24 billion (5.1% year-on-year growth, in line)

- Revenue: $1.52 billion vs analyst estimates of $1.54 billion (3.7% year-on-year growth, 1.3% miss)

- Pre-tax Profit: $329.5 million (21.7% margin)

- EPS (GAAP): $3.29 vs analyst expectations of $3.40 (3.2% miss)

- Book Value per Share: $74.17 vs analyst estimates of $97.30 (17.4% year-on-year growth, 23.8% miss)

- Market Capitalization: $11.44 billion

Company Overview

With roots dating back to 1900 and a rebranding from Torchmark Corporation in 2019, Globe Life (NYSE:GL) is an insurance holding company that offers life insurance, supplemental health insurance, and annuity products through various distribution channels.

Globe Life operates through several primary subsidiaries including Globe Life and Accident Insurance Company, American Income Life Insurance Company, Liberty National Life Insurance Company, Family Heritage Life Insurance Company of America, and United American Insurance Company. These subsidiaries collectively provide a range of insurance products tailored to different market segments.

The company's business is organized into four main segments. The life insurance segment offers traditional whole life and term life policies, marketed through multiple distribution channels including direct-to-consumer and agent networks. The supplemental health insurance segment provides Medicare Supplement plans and limited-benefit products covering specific conditions like cancer and critical illness, designed to complement existing health coverage. While Globe Life does have an annuities segment, it represents less than 1% of premium income and the company doesn't actively market stand-alone annuity products.

A typical customer might be a middle-income family purchasing a whole life policy through an American Income Life agent to provide financial protection for their loved ones, or a Medicare enrollee buying a Medicare Supplement plan through United American to cover costs not paid by traditional Medicare.

Globe Life generates revenue primarily through premium payments on insurance policies. Its investment segment manages the company's capital resources, with approximately 91% of invested assets allocated to fixed-maturity securities, reflecting the conservative investment approach typical of insurance companies. This segment plays a crucial role in maintaining the financial stability needed to meet future policy obligations.

4. Life Insurance

Life insurance companies collect premiums from policyholders in exchange for providing a future death benefit or retirement income stream. Interest rates matter for the sector (and make it cyclical), with higher rates allowing insurers to reinvest their fixed-income portfolios at more attractive yields and vice versa. Additionally, favorable demographic shifts, such as an aging population, are driving strong demand for retirement products while AI and data analytics offer significant opportunities to improve underwriting accuracy and operational efficiency. Conversely, the industry faces headwinds from persistent competition from agile insurtechs that threaten traditional distribution models.

Globe Life competes with other insurance providers such as Aflac (NYSE:AFL), MetLife (NYSE:MET), Prudential Financial (NYSE:PRU), and Lincoln National (NYSE:LNC) in the life and supplemental health insurance markets.

5. Revenue Growth

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services. Unfortunately, Globe Life’s 4.9% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the insurance sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Globe Life’s annualized revenue growth of 4.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Globe Life’s revenue grew by 3.7% year on year to $1.52 billion, falling short of Wall Street’s estimates.

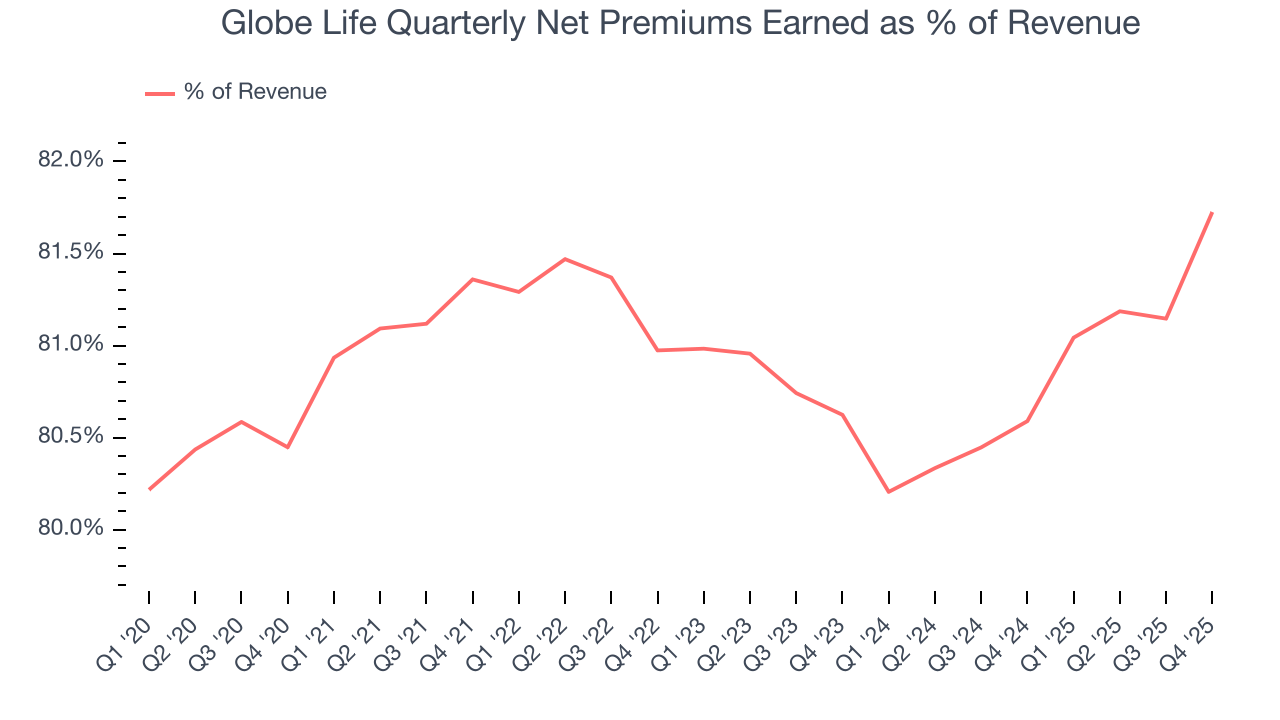

Net premiums earned made up 81% of the company’s total revenue during the last five years, meaning Globe Life barely relies on non-insurance activities to drive its overall growth.

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

6. Net Premiums Earned

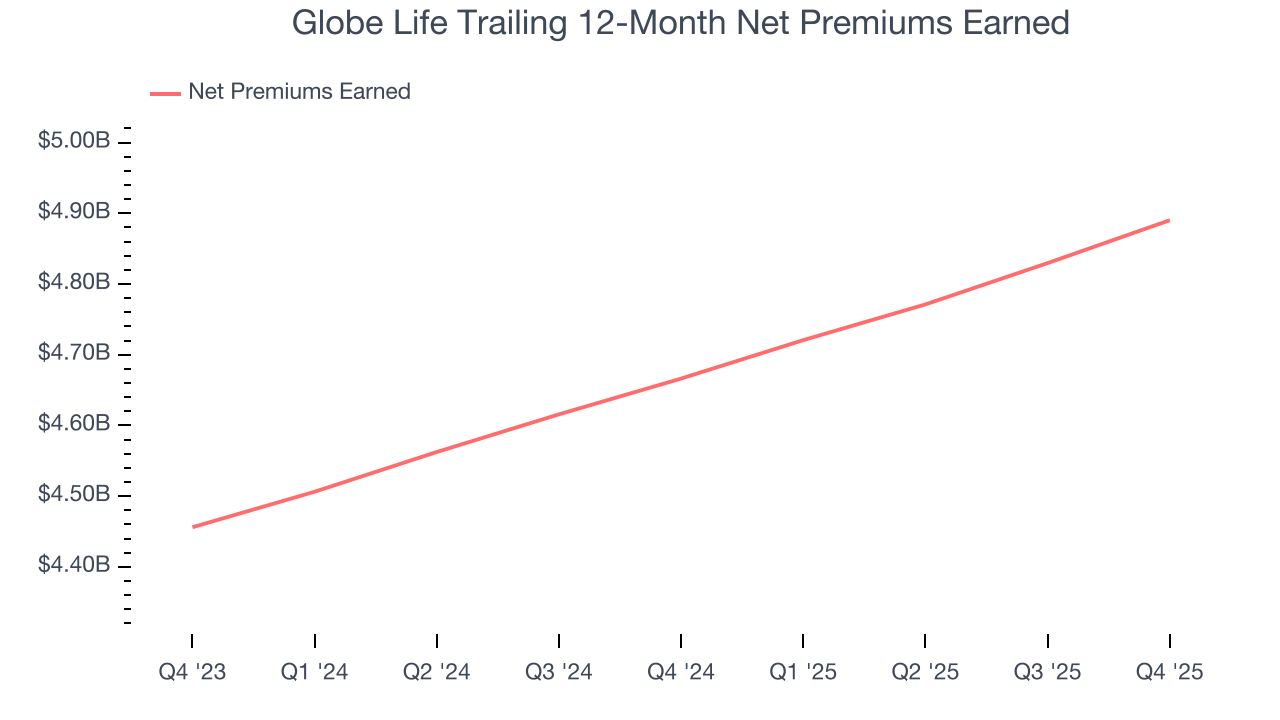

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

Globe Life’s net premiums earned has grown at a 5.1% annualized rate over the last five years, worse than the broader insurance industry and in line with its total revenue.

When analyzing Globe Life’s net premiums earned over the last two years, we can paint a similar picture as it recorded an annual growth rate of 4.8%. This performance was similar to its total revenue.

In Q4, Globe Life produced $1.24 billion of net premiums earned, up 5.1% year on year and in line with Wall Street Consensus estimates.

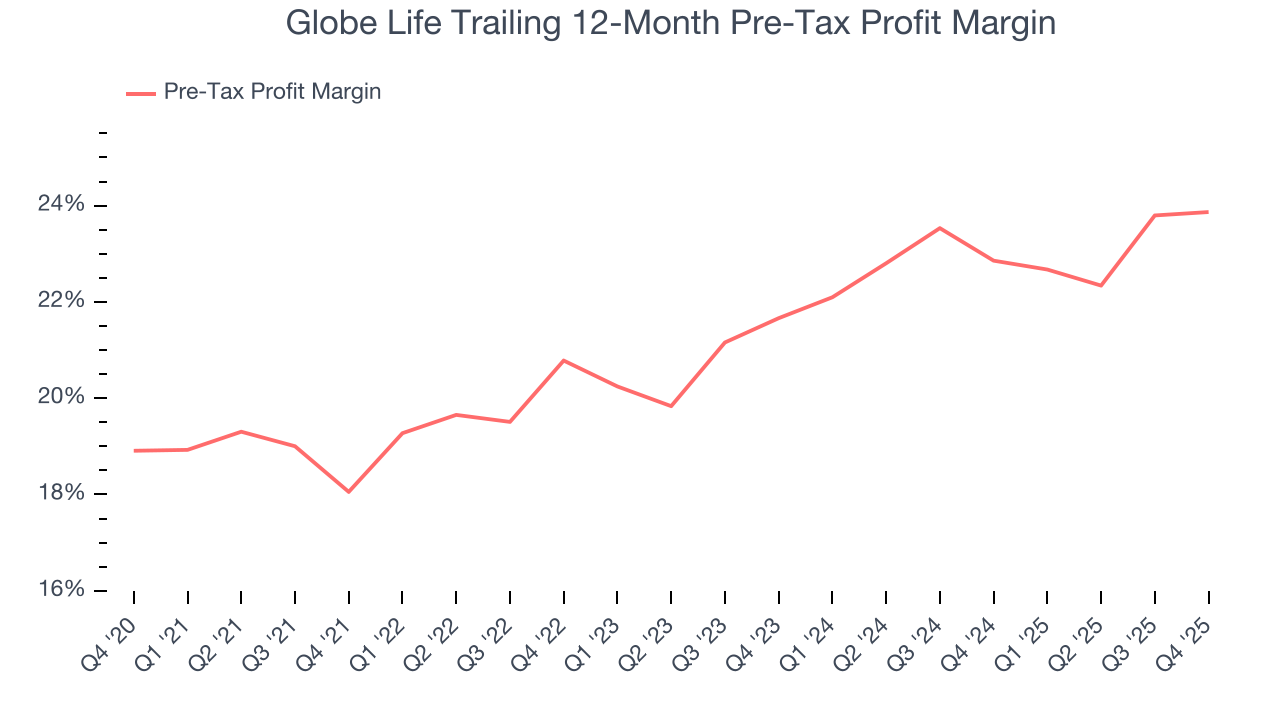

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The economics of insurers are driven by their balance sheets, where assets (investing the float + premiums receivable) and liabilities (claims to pay) define the fundamentals. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last five years, Globe Life’s pre-tax profit margin has fallen by 5 percentage points, going from 18.1% to 23.9%. It has also expanded by 2.2 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

In Q4, Globe Life’s pre-tax profit margin was 21.7%. This result was in line with the same quarter last year.

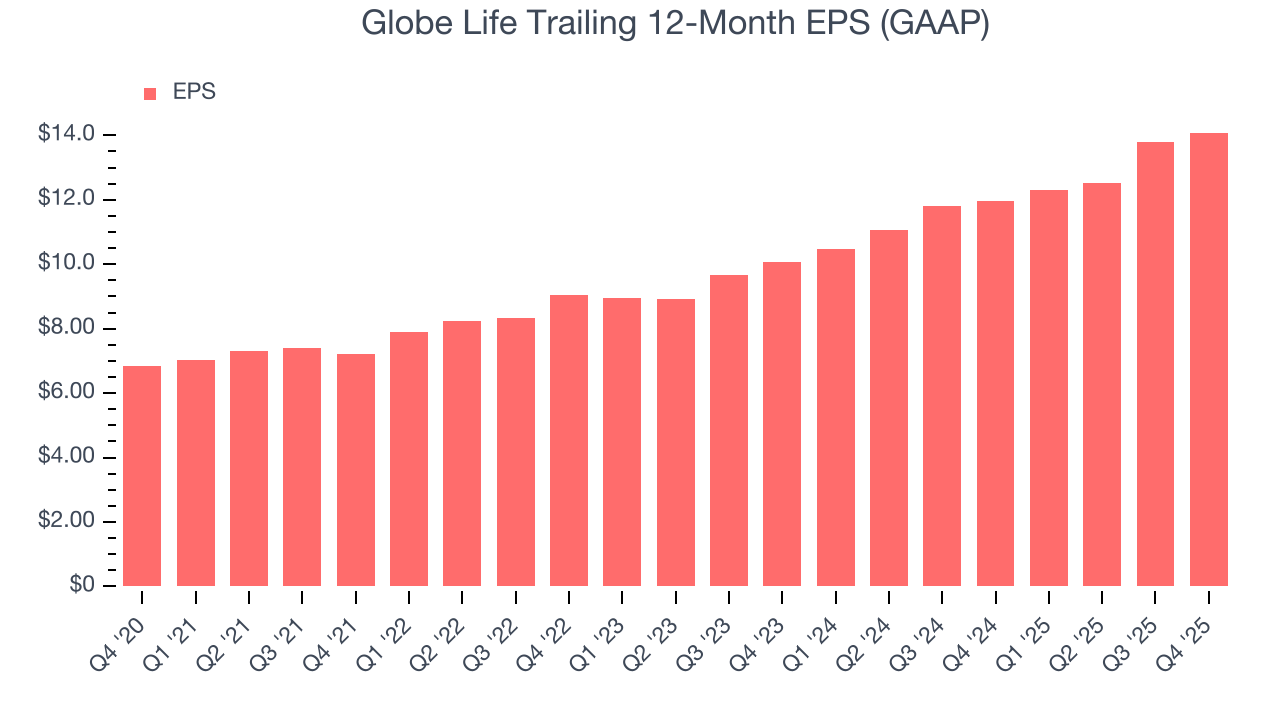

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Globe Life’s EPS grew at a solid 15.6% compounded annual growth rate over the last five years, higher than its 4.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Globe Life, its two-year annual EPS growth of 18.2% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Globe Life reported EPS of $3.29, up from $3.01 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Globe Life’s full-year EPS of $14.08 to grow 5.9%.

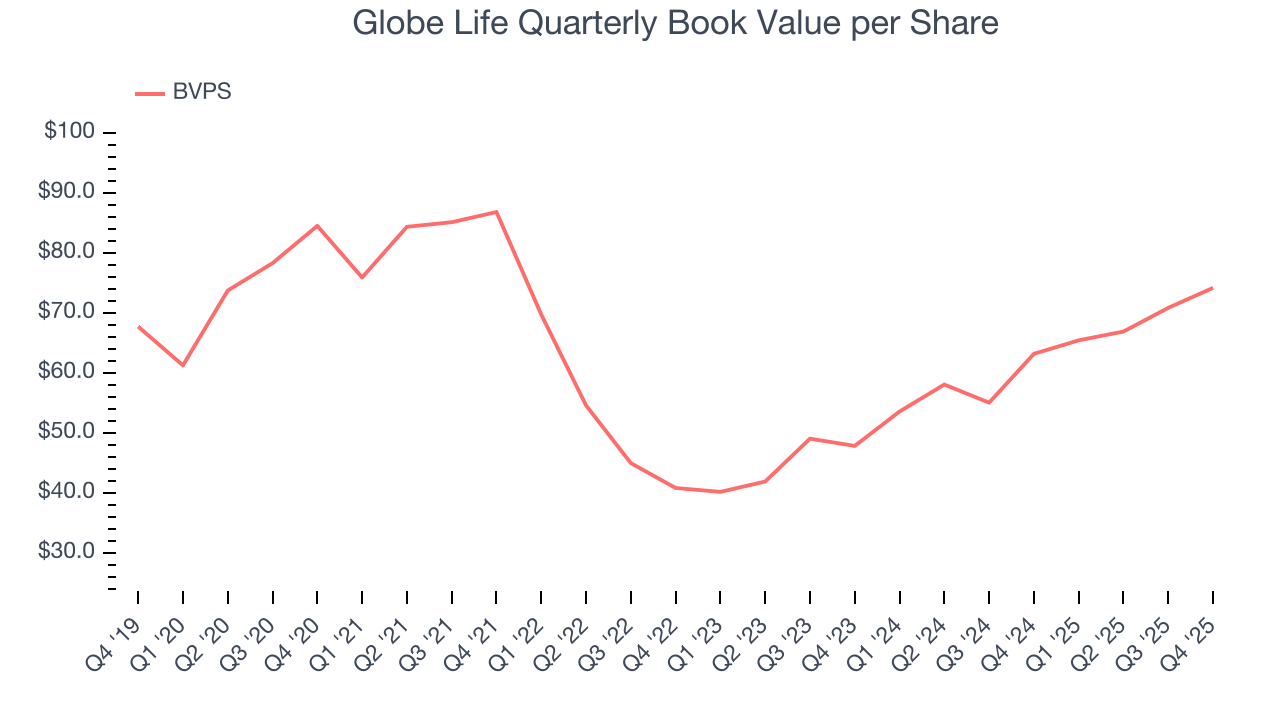

9. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

Globe Life’s BVPS declined at a 2.6% annual clip over the last five years. However, BVPS growth has accelerated recently, growing by 24.5% annually over the last two years from $47.84 to $74.17 per share.

Over the next 12 months, Consensus estimates call for Globe Life’s BVPS to grow by 46.1% to $97.30, elite growth rate.

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Globe Life has no debt, so leverage is not an issue here.

11. Return on Equity

Return on equity (ROE) serves as a comprehensive measure of an insurer's performance, showing how efficiently it converts shareholder capital into profits. Strong ROE performance typically translates to better returns for investors through a combination of earnings retention, share repurchases, and dividend distributions.

Over the last five years, Globe Life has averaged an ROE of 18.2%, excellent for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This is a bright spot for Globe Life.

12. Key Takeaways from Globe Life’s Q4 Results

We struggled to find many positives in these results. Its book value per share missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.1% to $140.34 immediately after reporting.

13. Is Now The Time To Buy Globe Life?

Updated: March 15, 2026 at 12:23 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Globe Life.

Globe Life isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue growth was uninspiring over the last five years. While its estimated BVPS growth for the next 12 months is great, the downside is its BVPS has declined over the last five years. On top of that, its projected EPS for the next year is lacking.

Globe Life’s P/B ratio based on the next 12 months is 1.6x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $172.10 on the company (compared to the current share price of $138.48).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.