Granite Ridge Resources (GRNT)

We’re not sold on Granite Ridge Resources. It not only barely produces cash but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why Granite Ridge Resources Is Not Exciting

Operating without drilling rigs or field crews of its own, Granite Ridge Resources (NYSE:GRNT) owns interests in oil and natural gas wells across six major US shale basins.

- Revenue base of $450.3 million puts it at a disadvantage compared to larger competitors exhibiting economies of scale

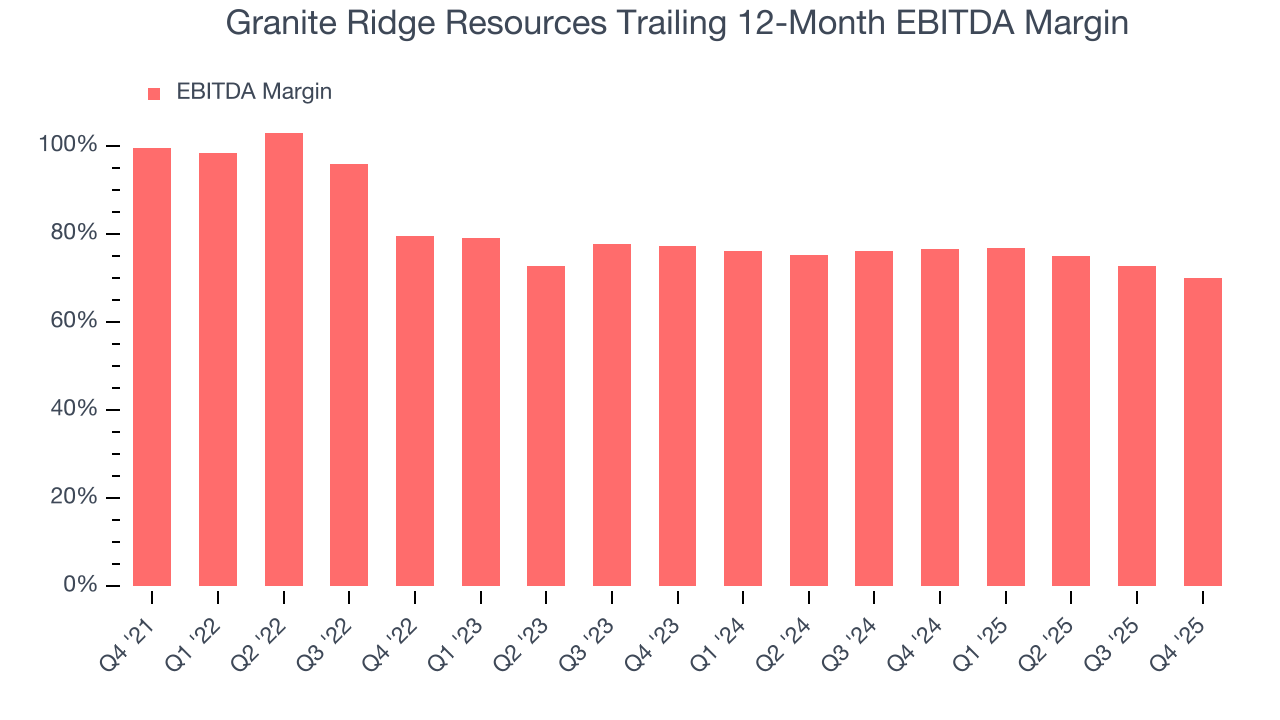

- Efficiency has decreased over the last five years as its EBITDA margin fell by 29.6 percentage points

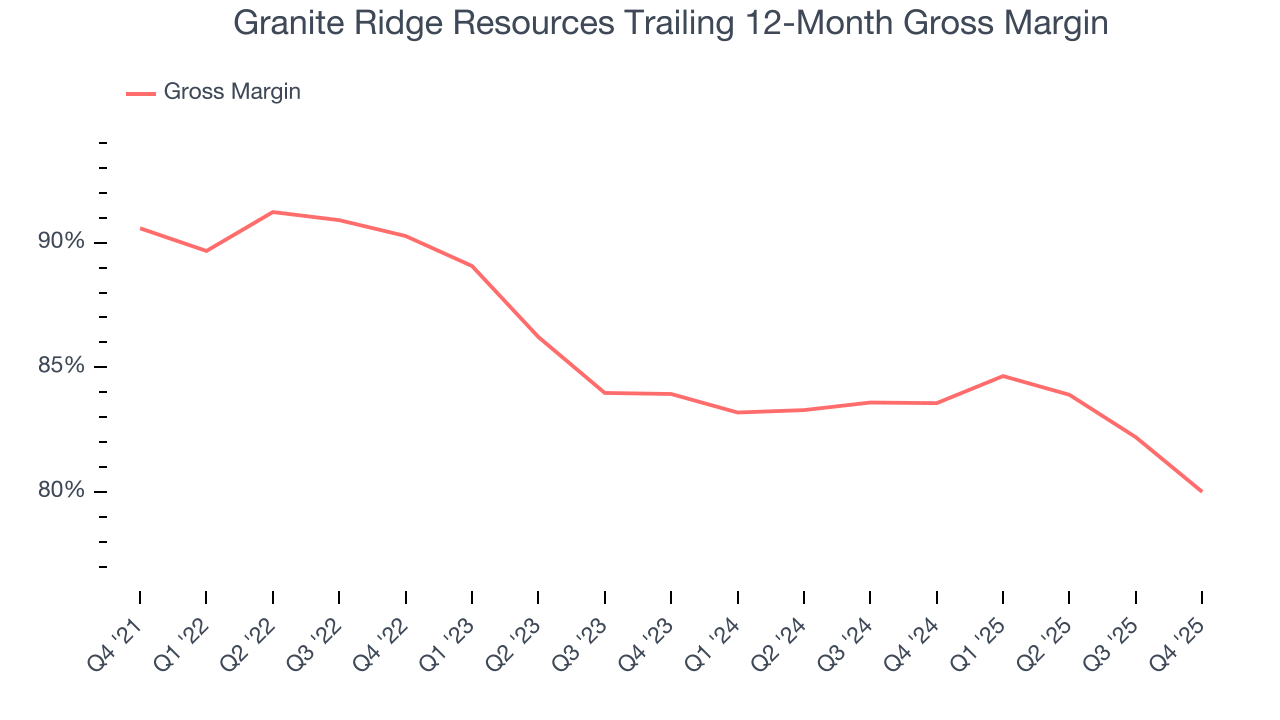

- One positive is that its attractive asset base leads to wonderful unit economics and a best-in-class gross margin of 85.5%

Granite Ridge Resources doesn’t fulfill our quality requirements. There are more promising prospects in the market.

Why There Are Better Opportunities Than Granite Ridge Resources

At $5.32 per share, Granite Ridge Resources trades at 13.5x forward P/E. This multiple is cheaper than most energy upstream and integrated energy peers, but we think this is justified.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Granite Ridge Resources (GRNT) Research Report: Q4 CY2025 Update

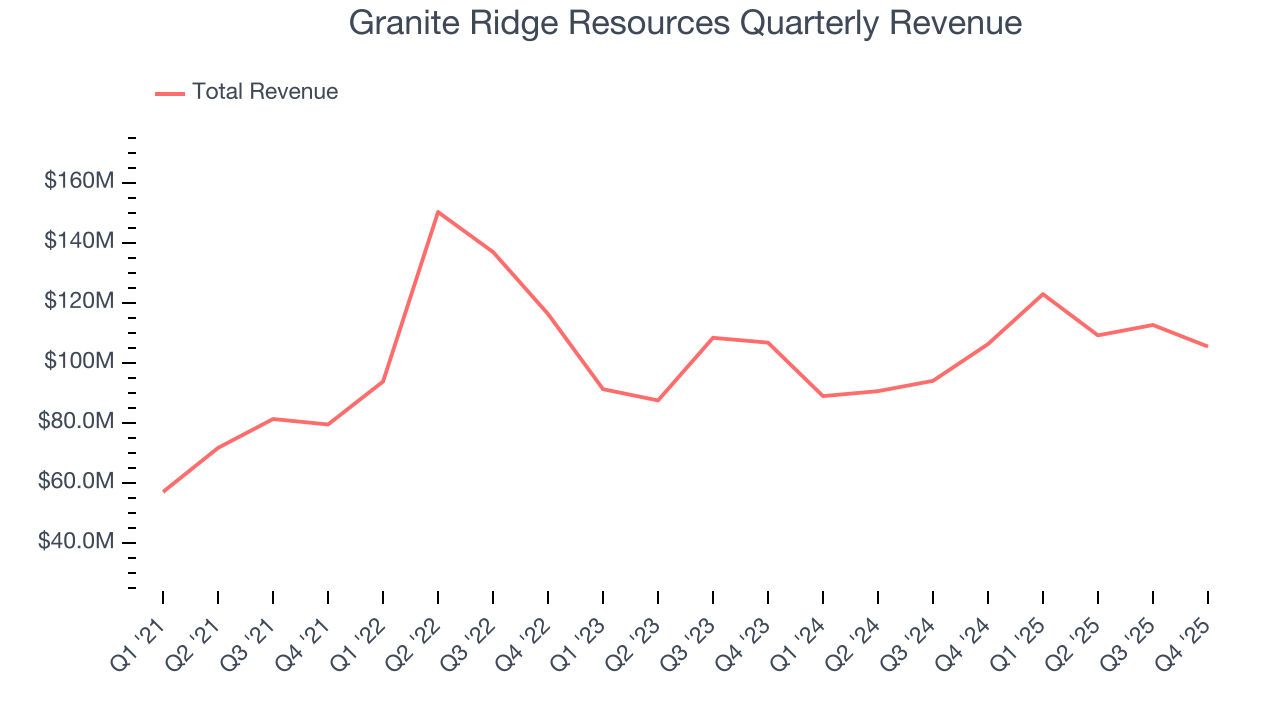

Oil and gas company Granite Ridge Resources (NYSE:GRNT) missed Wall Street’s revenue expectations in Q4 CY2025, with sales flat year on year at $105.5 million. Its non-GAAP profit of $0.01 per share was 90% below analysts’ consensus estimates.

Granite Ridge Resources (GRNT) Q4 CY2025 Highlights:

- Revenue: $105.5 million vs analyst estimates of $121.5 million (flat year on year, 13.2% miss)

- Adjusted EPS: $0.01 vs analyst expectations of $0.10 (90% miss)

- Adjusted EBITDA: $69.5 million vs analyst estimates of $83.76 million (65.9% margin, 17% miss)

- Operating Margin: -34.5%, down from -6.5% in the same quarter last year

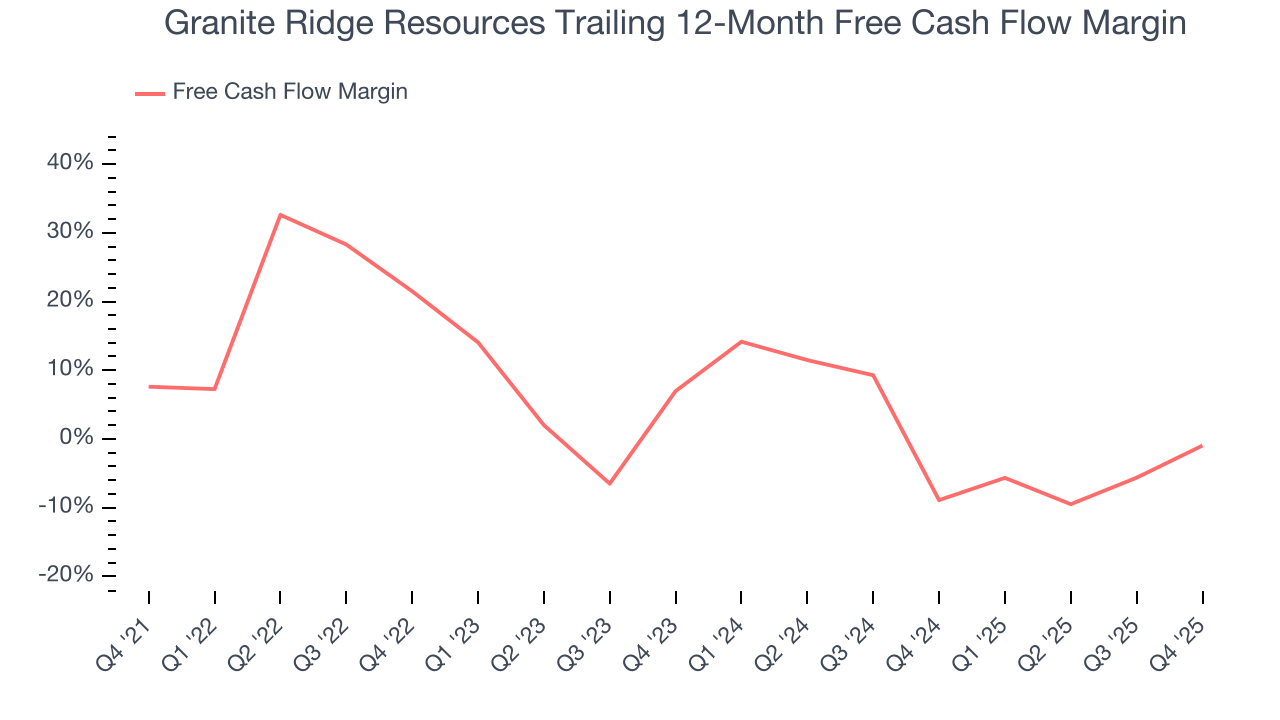

- Free Cash Flow was -$3.13 million compared to -$24.22 million in the same quarter last year

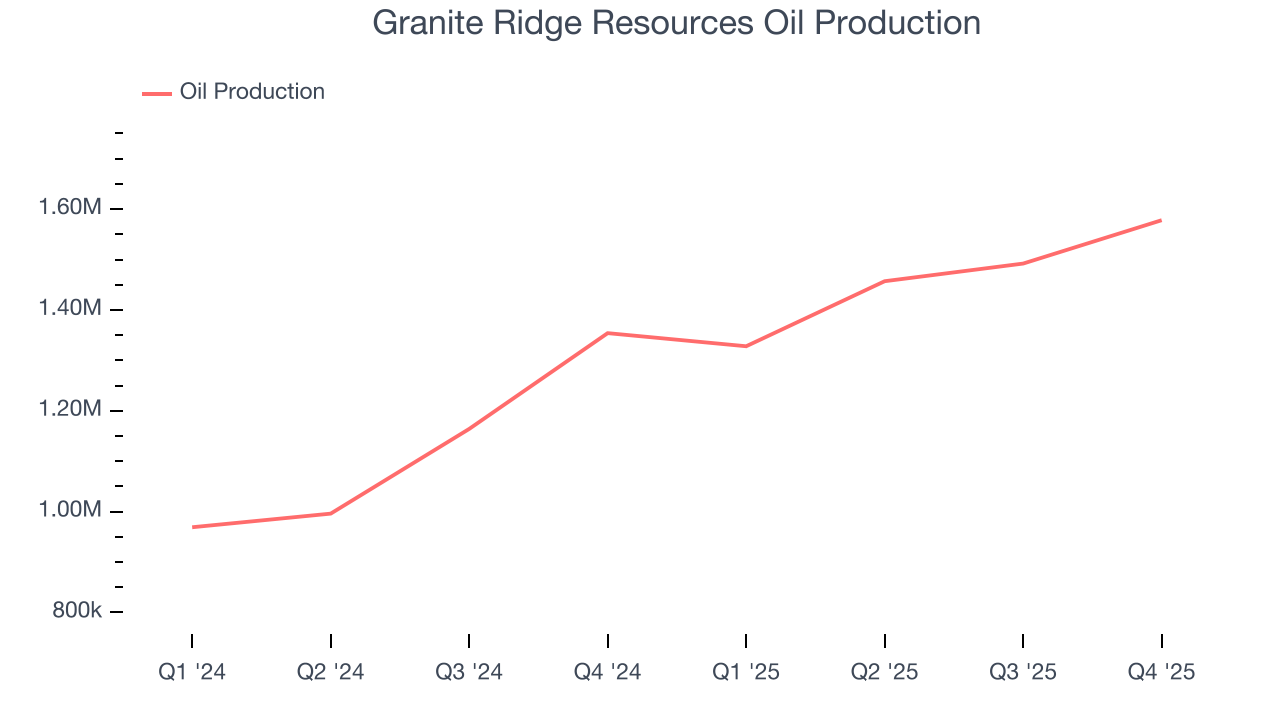

- Oil production: 1.58 million, up 224,000 year on year

- Market Capitalization: $694.1 million

Company Overview

Operating without drilling rigs or field crews of its own, Granite Ridge Resources (NYSE:GRNT) owns interests in oil and natural gas wells across six major US shale basins.

The company owns working interests in wells spread across the Permian Basin in west Texas and New Mexico, the Eagle Ford in south Texas, the Bakken in North Dakota, the Haynesville in Louisiana and east Texas, the Denver-Julesburg Basin in Colorado, and the Appalachian Basin's Utica Shale in Ohio. Rather than operating wells itself, Granite Ridge participates alongside third-party operators who handle the day-to-day drilling, completion, and production activities. When a well is drilled on acreage where Granite Ridge holds mineral rights, it receives a proportionate share of the oil and natural gas produced, minus its share of operating costs.

The company employs two primary strategies to build its portfolio. First, it acquires mineral and leasehold interests in specific geographic areas, which entitle it to participate in future wells drilled on that acreage. Second, it purchases wellbore-only working interests—direct stakes in individual wells—from third parties who choose not to participate in particular drilling projects. For example, if an independent operator plans to drill a well but a landowner or small mineral rights holder decides not to fund their proportionate share of drilling costs, Granite Ridge can step in to acquire that interest.

This asset-light model means Granite Ridge doesn't employ geologists to select drill sites or field engineers to oversee operations. Instead, it relies on its operating partners—ranging from large publicly traded exploration companies to smaller private operators—to propose wells, obtain permits, and manage production. The company's revenue comes from its proportionate share of oil and natural gas sales, with pricing typically tied to spot market rates for oil and monthly or daily index prices for natural gas.

4. Mixed or Offshore Upstream E&P

This category includes smaller or niche E&P companies operating in specialized basins, geographies, or resource types outside major classifications. These firms may target unconventional resources, frontier regions, or specific commodity niches. Tailwinds include potential for outsized returns from successful exploration, acquisition opportunities during industry downturns, and specialized expertise commanding premium valuations. Headwinds include higher operational and geological risks, limited scale reducing negotiating power and cost efficiencies, and constrained capital market access during challenging commodity environments. Regulatory risks and ESG concerns may disproportionately affect smaller operators with fewer resources for compliance.

Granite Ridge Resources competes with other non-operated oil and gas companies including Sitio Royalties (NYSE:STR), Permianville Royalty Trust (NYSE:PVL), and Viper Energy (NASDAQ:VNOM), along with numerous private mineral and royalty aggregators.

5. Revenue Scale

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program. Granite Ridge Resources’s $450.3 million of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night.

6. Revenue Growth

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Luckily, Granite Ridge Resources’s sales grew at a decent 11.6% compounded annual growth rate over the last four years. Its growth was slightly above the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Revenue provides useful context, but it is heavily influenced by commodity prices and acquisitions. Production volumes, by contrast, reveal whether the underlying asset base is actually growing. Over the last two years, Granite Ridge Resources’s oil production averaged 32% year-on-year growth while its natural gas production averaged 25% year-on-year growth.

This quarter, Granite Ridge Resources missed Wall Street’s estimates and reported a rather uninspiring 0.8% year-on-year revenue decline, generating $105.5 million of revenue. This quarter, Granite Ridge Resources reported year-on-year Oil production growth of 16.5%.

7. Gross Margin

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

Granite Ridge Resources, which averaged 85.5% gross margin over the last five years, exhibits impressive unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an excellent starting point for ultimate operating profits and free cash flow generation.

In Q4, Granite Ridge Resources produced a 75.3% gross profit margin, down 9.3 percentage points year on year.

8. Adjusted EBITDA Margin

Granite Ridge Resources has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 79.3%.

Looking at the trend in its profitability, Granite Ridge Resources’s EBITDA margin decreased by 29.6 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Granite Ridge Resources become more profitable in the future.

In Q4, Granite Ridge Resources generated an EBITDA margin profit margin of 65.9%, down 11.8 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

Granite Ridge Resources has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5.9%, below what we’d expect for an upstream and integrated energy business.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Granite Ridge Resources’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 27.9 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Granite Ridge Resources? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Granite Ridge Resources burned through $3.13 million of cash in Q4, equivalent to a negative 3% margin. The company’s cash burn slowed from $24.22 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

10. Balance Sheet Assessment

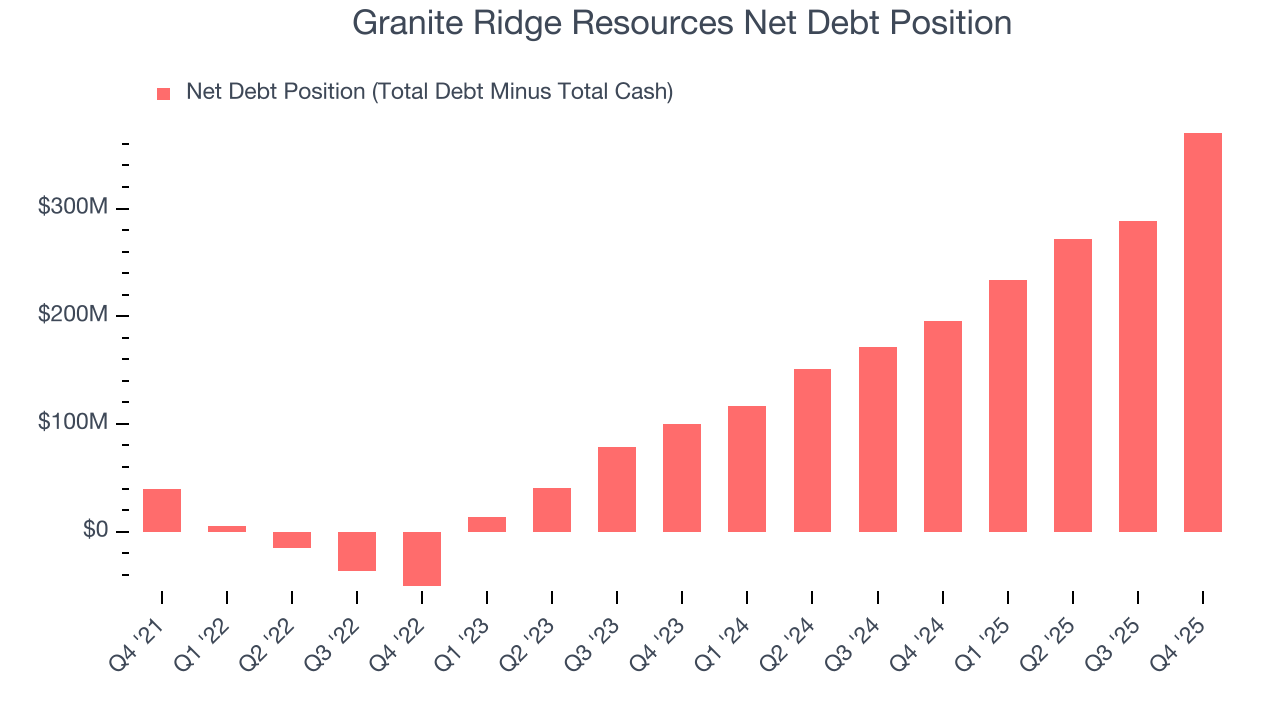

Granite Ridge Resources reported $14.85 million of cash and $385.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $315 million of EBITDA over the last 12 months, we view Granite Ridge Resources’s 1.2× net-debt-to-EBITDA ratio as safe. We also see its $25.5 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Granite Ridge Resources’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded up 1.6% to $5.37 immediately after reporting.

12. Is Now The Time To Buy Granite Ridge Resources?

Updated: March 18, 2026 at 1:17 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Granite Ridge Resources.

When it comes to Granite Ridge Resources’s business quality, there are some positives, but it ultimately falls short. To begin with, the its revenue growth over the last four years was average for the sector, and analysts believe it can continue growing at these levels. And while Granite Ridge Resources’s free cash flow volatility compared to commodity price volatility is bottom-tier in the sector, leading to highly volatile free cash flow, its admirable gross margin indicates excellent unit economics.

Granite Ridge Resources’s P/E ratio based on the next 12 months is 13.5x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $6.20 on the company (compared to the current share price of $5.32).