Howard Hughes Holdings (HHH)

Howard Hughes Holdings is in for a bumpy ride. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Howard Hughes Holdings Will Underperform

Named after the eccentric business magnate and aviator whose legacy lives on in real estate development, Howard Hughes Holdings (NYSE:HHH) develops, owns, and manages master-planned communities and commercial properties across the United States.

- Low returns on capital reflect management’s struggle to allocate funds effectively

- 21.5% annual revenue growth over the last five years was slower than its consumer discretionary peers

- 6× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Howard Hughes Holdings doesn’t satisfy our quality benchmarks. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Howard Hughes Holdings

At $65.71 per share, Howard Hughes Holdings trades at 2.3x forward price-to-sales. The market typically values companies like Howard Hughes Holdings based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Howard Hughes Holdings (HHH) Research Report: Q4 CY2025 Update

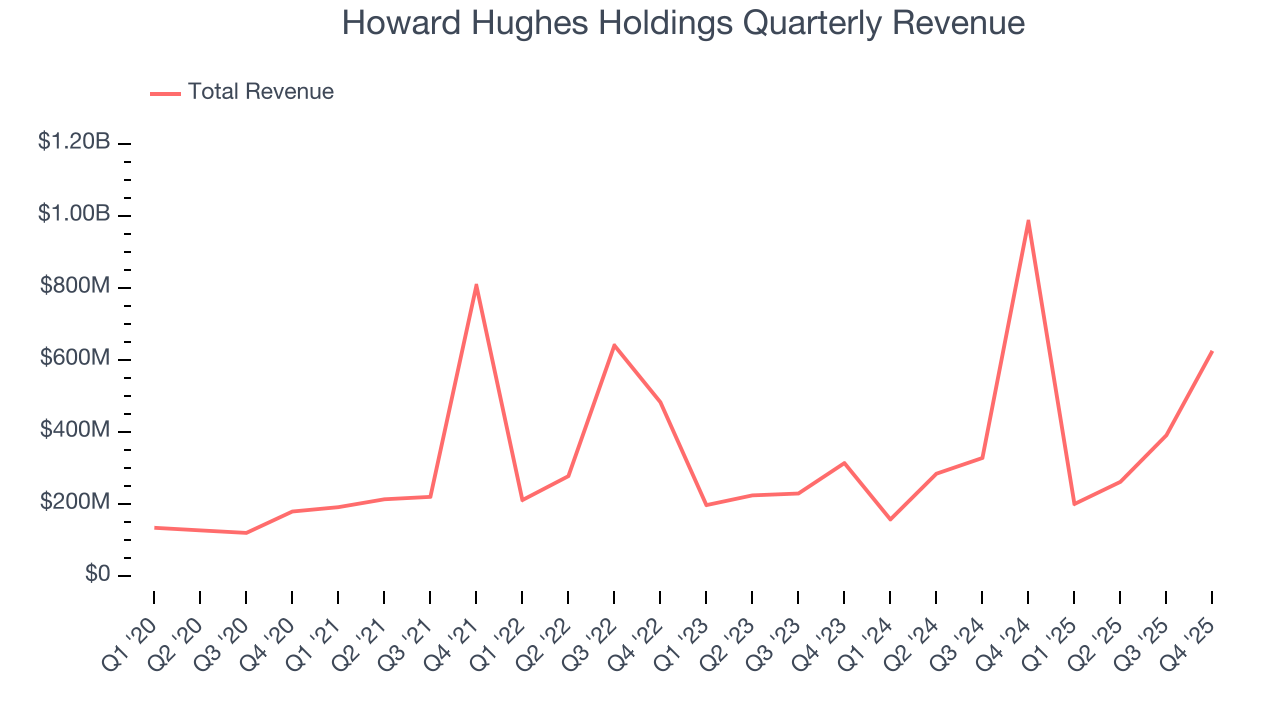

Real estate developer Howard Hughes Holdings (NYSE:HHH) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 36.5% year on year to $624.4 million. Its GAAP profit of $0.10 per share was 75.1% below analysts’ consensus estimates.

Howard Hughes Holdings (HHH) Q4 CY2025 Highlights:

- Revenue: $624.4 million vs analyst estimates of $592.1 million (36.5% year-on-year decline, 5.5% beat)

- EPS (GAAP): $0.10 vs analyst expectations of $0.40 (75.1% miss)

- Adjusted EBITDA: $75.68 million (12.1% margin, 75.5% year-on-year decline)

- Operating Margin: 4.2%, down from 26.5% in the same quarter last year

- Market Capitalization: $4.90 billion

Company Overview

Named after the eccentric business magnate and aviator whose legacy lives on in real estate development, Howard Hughes Holdings (NYSE:HHH) develops, owns, and manages master-planned communities and commercial properties across the United States.

The company operates through a unique three-segment business model that creates a continuous value-creation cycle. It begins with its Master Planned Communities (MPCs) segment, where it develops expansive mixed-use communities spanning approximately 101,000 gross acres across five states. Notable communities include Summerlin in Las Vegas and Bridgeland near Houston, which consistently rank among the nation's top-selling MPCs.

When commercial development opportunities arise within these communities, Howard Hughes transitions the land to its Strategic Developments segment, constructing office buildings, retail centers, multifamily properties, and other commercial assets. Upon completion, these properties move to the Operating Assets segment, generating recurring income that funds further development.

This integrated approach allows Howard Hughes to control the entire real estate lifecycle. For example, in Summerlin, the company might sell residential lots to homebuilders while simultaneously developing Downtown Summerlin, a retail and entertainment district that enhances the community's appeal and increases residential land values. The company also develops luxury projects like The Summit, an exclusive community created in partnership with Discovery Land Company, and Ward Village in Hawaii, a high-end coastal neighborhood featuring condominium towers alongside retail and entertainment spaces.

4. Consumer Discretionary - Real Estate Services

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Real estate services companies provide brokerage, property management, appraisal, and advisory services, earning transaction-based commissions and recurring management fees. Tailwinds include long-term housing demand driven by demographic growth, technology platforms that expand market access, and commercial real estate complexity that sustains advisory needs. Headwinds are pronounced: rising interest rates directly suppress transaction volumes by reducing housing affordability and commercial deal activity. Commission-rate compression, driven by discount brokerages and regulatory changes, erodes per-transaction revenue. The industry is highly cyclical, with revenue swings amplified by leverage. PropTech (property technology) disruptors threaten traditional intermediary models.

Howard Hughes Holdings competes with large-scale real estate developers and operators including Brookfield Properties (NYSE:BPY), Simon Property Group (NYSE:SPG), and Related Companies (private), as well as regional developers in its various markets.

5. Revenue Growth

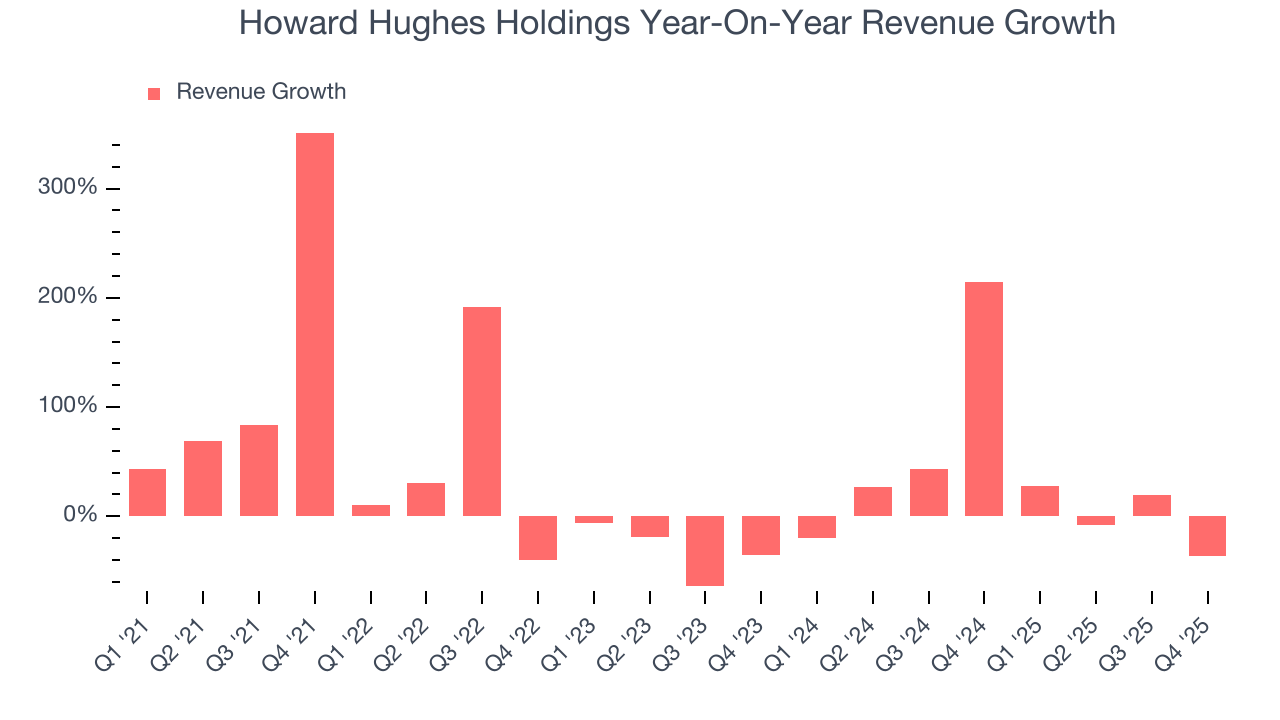

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Howard Hughes Holdings grew its sales at a 21.5% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Howard Hughes Holdings’s annualized revenue growth of 23.9% over the last two years is above its five-year trend, which is encouraging.

This quarter, Howard Hughes Holdings’s revenue fell by 36.5% year on year to $624.4 million but beat Wall Street’s estimates by 5.5%.

Looking ahead, sell-side analysts expect revenue to grow 18.5% over the next 12 months, a deceleration versus the last two years. Still, this projection is healthy and suggests the market is forecasting success for its products and services.

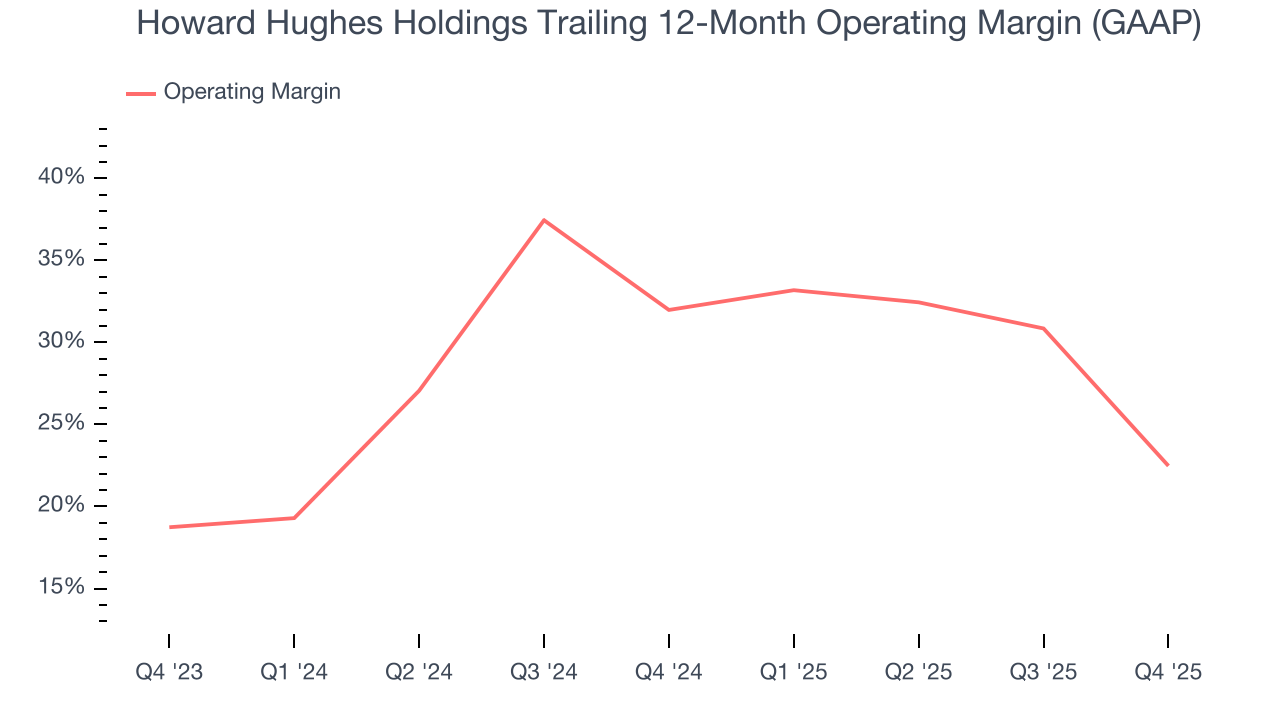

6. Operating Margin

Howard Hughes Holdings’s operating margin has been trending down over the last 12 months and averaged 27.6% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Howard Hughes Holdings generated an operating margin profit margin of 4.2%, down 22.3 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

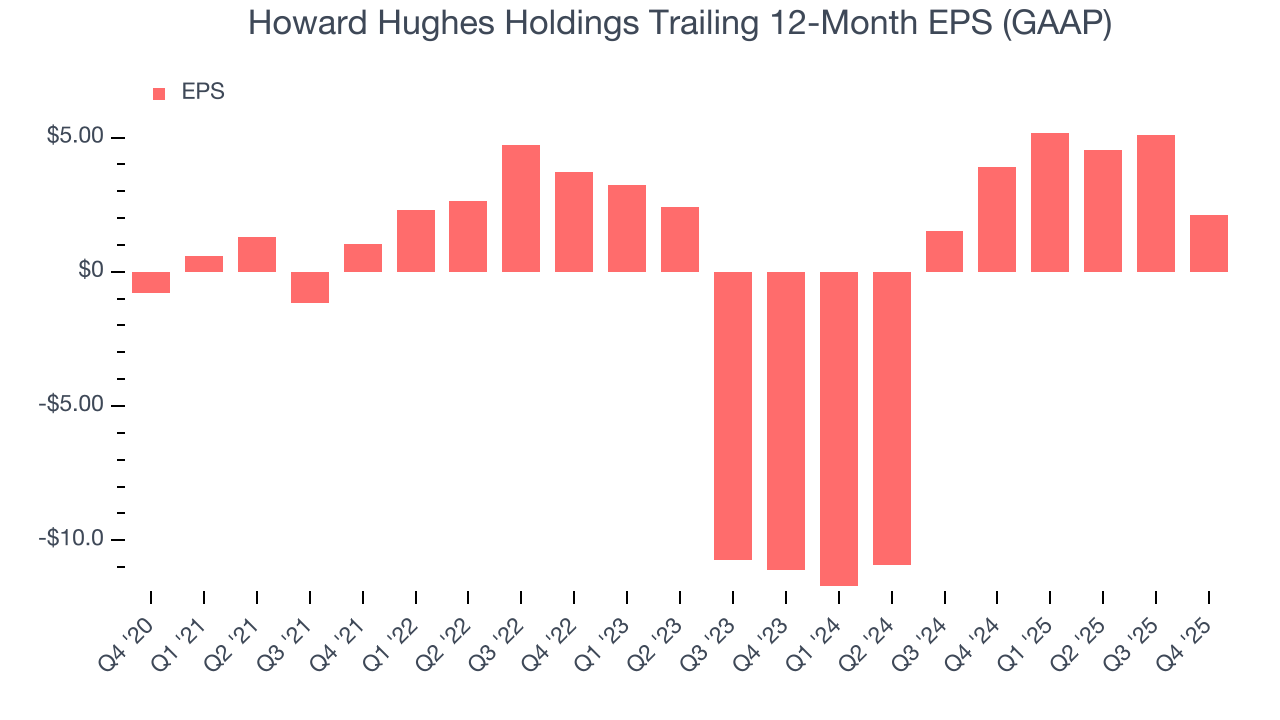

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Howard Hughes Holdings’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Howard Hughes Holdings reported EPS of $0.10, down from $3.10 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Howard Hughes Holdings’s full-year EPS of $2.11 to grow 88.2%.

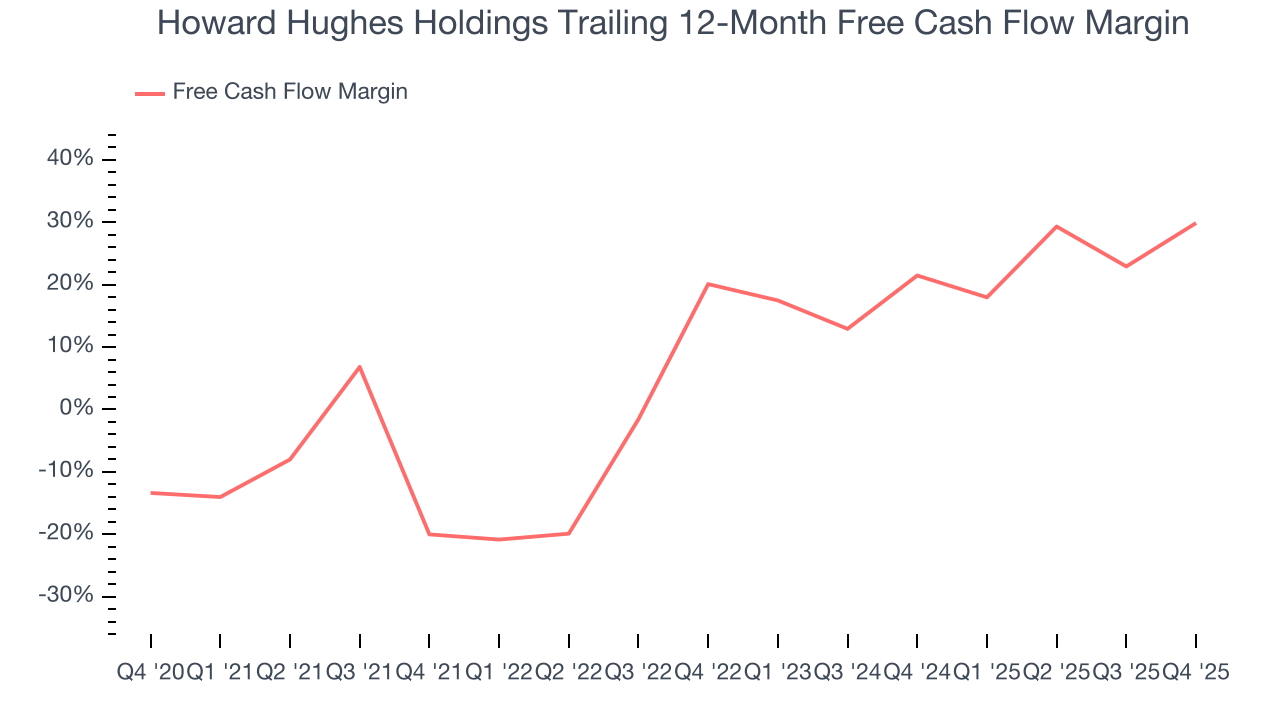

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Howard Hughes Holdings has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 25.3%, subpar for a consumer discretionary business.

Howard Hughes Holdings’s free cash flow clocked in at $356.2 million in Q4, equivalent to a 57% margin. This result was good as its margin was 22.9 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

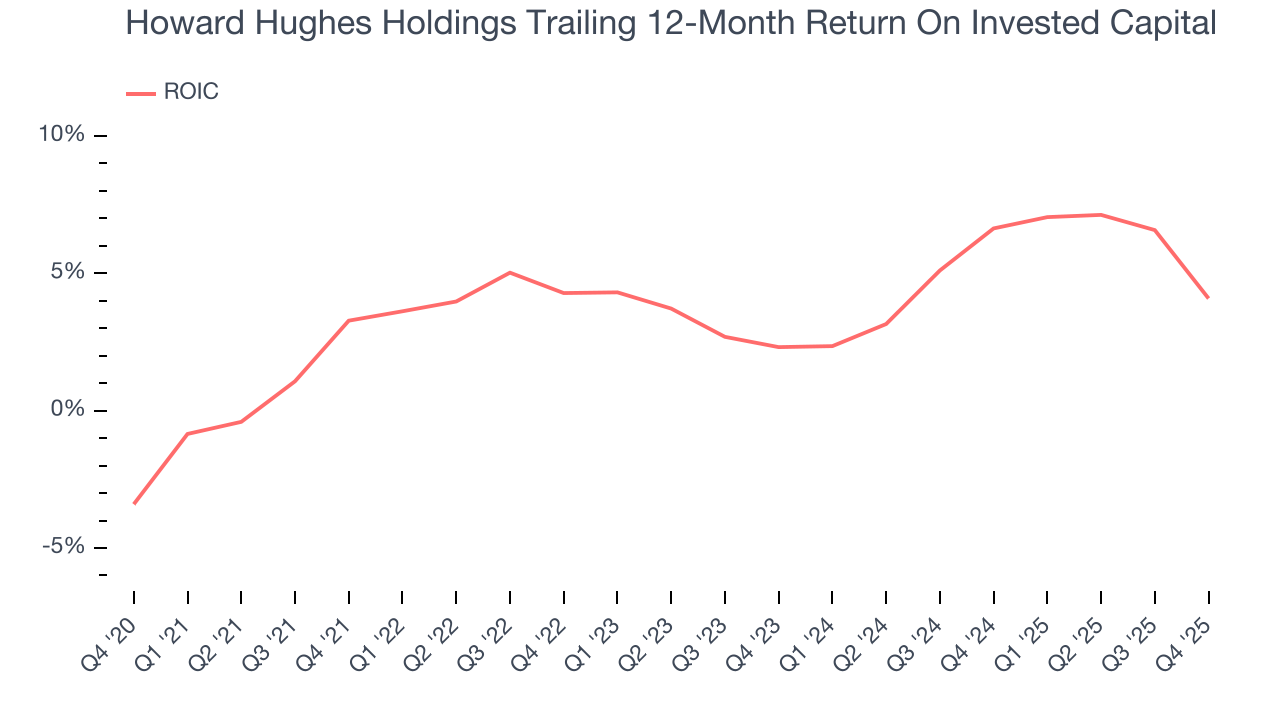

9. Return on Invested Capital (ROIC)

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Howard Hughes Holdings historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.1%, lower than the typical cost of capital (how much it costs to raise money) for consumer discretionary companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Howard Hughes Holdings’s ROIC averaged 1.6 percentage point increases each year over the last few years. This is a good sign, and we hope the company can continue improving.

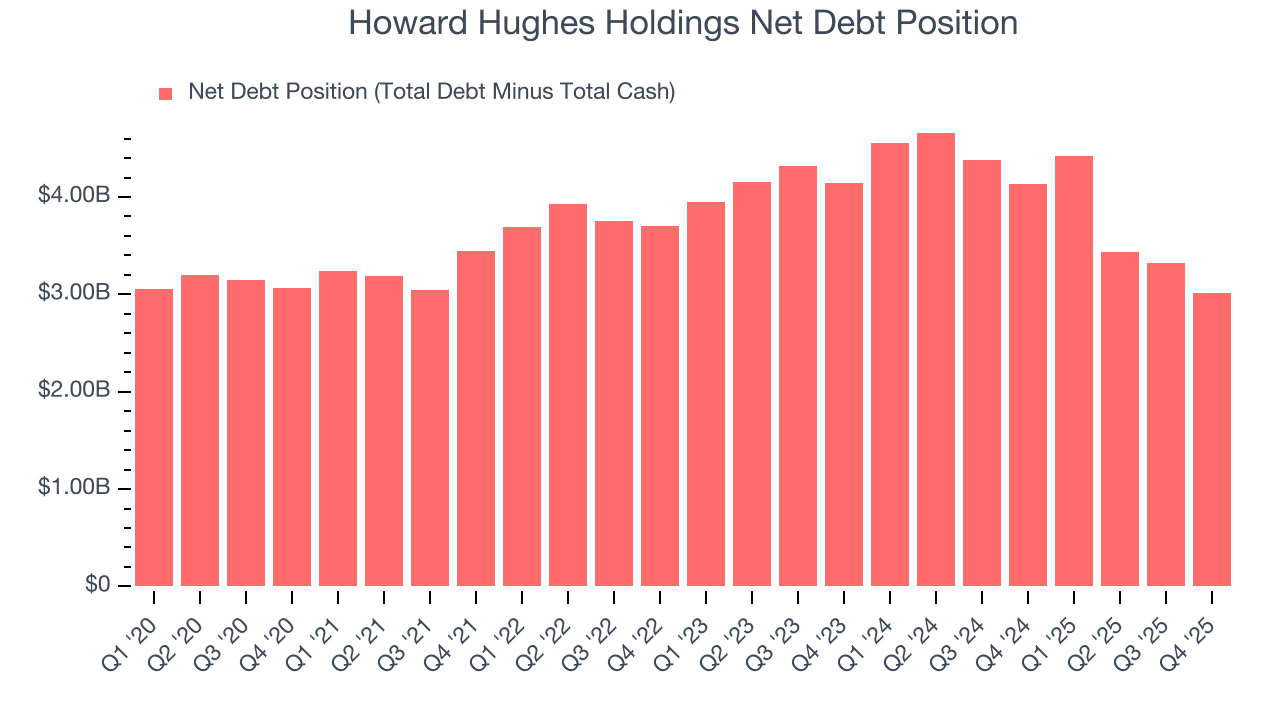

10. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Howard Hughes Holdings’s $5.11 billion of debt exceeds the $2.10 billion of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $489.8 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Howard Hughes Holdings could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Howard Hughes Holdings can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Howard Hughes Holdings’s Q4 Results

We enjoyed seeing Howard Hughes Holdings beat analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this was a weaker quarter. The stock remained flat at $81.49 immediately following the results.

12. Is Now The Time To Buy Howard Hughes Holdings?

Updated: March 26, 2026 at 12:45 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We see the value of companies helping consumers, but in the case of Howard Hughes Holdings, we’re out. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its low free cash flow margins give it little breathing room.

Howard Hughes Holdings’s forward price-to-sales ratio is 2.3x. The market typically values companies like Howard Hughes Holdings based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere.

Wall Street analysts have a consensus one-year price target of $94.67 on the company (compared to the current share price of $65.71).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.