Helios (HLIO)

Helios keeps us up at night. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Helios Will Underperform

Founded on the principle of treating others as one wants to be treated, Helios (NYSE:HLIO) designs, manufactures, and sells motion and electronic control components for various sectors.

- Sales were flat over the last two years, indicating it’s failed to expand this cycle

- Core business is underperforming as its organic revenue has disappointed over the past two years, suggesting it might need acquisitions to stimulate growth

- Projected sales growth of 1.1% for the next 12 months suggests sluggish demand

Helios’s quality is lacking. There are more promising alternatives.

Why There Are Better Opportunities Than Helios

At $68.51 per share, Helios trades at 23.3x forward P/E. This multiple rich for the business quality. Not a great combination.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Helios (HLIO) Research Report: Q4 CY2025 Update

Motion control and electronic systems manufacturer Helios Technologies (NYSE:HLIO) announced better-than-expected revenue in Q4 CY2025, with sales up 17.4% year on year to $210.7 million. On top of that, next quarter’s revenue guidance ($220.5 million at the midpoint) was surprisingly good and 9.7% above what analysts were expecting. Its non-GAAP profit of $0.81 per share was 12.6% above analysts’ consensus estimates.

Helios (HLIO) Q4 CY2025 Highlights:

- Revenue: $210.7 million vs analyst estimates of $197.9 million (17.4% year-on-year growth, 6.4% beat)

- Adjusted EPS: $0.81 vs analyst estimates of $0.72 (12.6% beat)

- Adjusted EBITDA: $42.3 million vs analyst estimates of $40.16 million (20.1% margin, 5.3% beat)

- Revenue Guidance for Q1 CY2026 is $220.5 million at the midpoint, above analyst estimates of $201.1 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.75 at the midpoint, in line with analyst estimates

- Operating Margin: 12.2%, up from 7.4% in the same quarter last year

- Free Cash Flow Margin: 19.2%, up from 15.8% in the same quarter last year

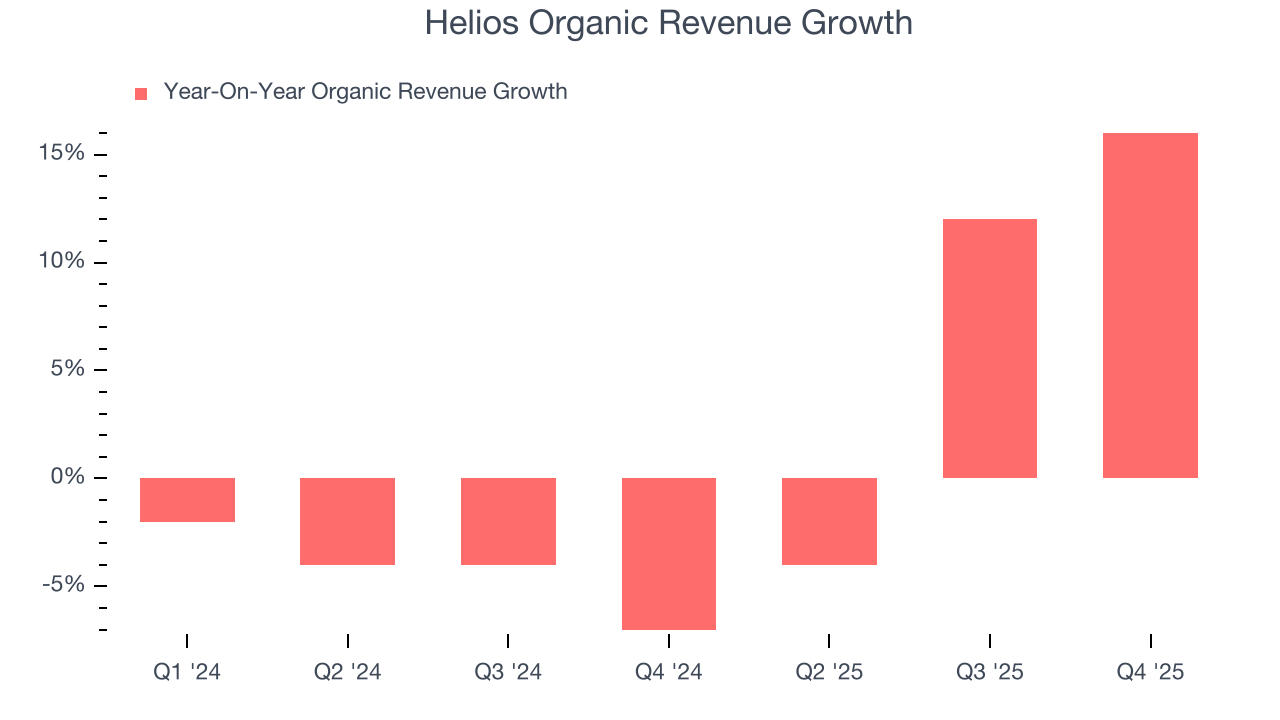

- Organic Revenue rose 16% year on year (miss)

- Market Capitalization: $2.36 billion

Company Overview

Founded on the principle of treating others as one wants to be treated, Helios (NYSE:HLIO) designs, manufactures, and sells motion and electronic control components for various sectors.

The company is structured into two main segments: Hydraulics and Electronics. These segments serve markets including construction, material handling, agriculture, industrial equipment, energy, recreational vehicles, marine, and health and wellness.

The Hydraulics segment produces components for controlling fluid flow and pressure in hydraulic systems, as well as products for fluid conveyance. This includes items such as cartridge valves, manifolds, and quick release couplings. The Electronics segment focuses on creating customized control systems, displays, wire harnesses, and software solutions for a range of applications.

Helios has been working to transition from a holding company model to an integrated operating company. This shift involves implementing the Helios Business System framework, which aims to enhance customer focus, global operations, market diversification, and talent development. However, the success and impact of this transition remain to be fully realized.

The company's revenue is derived from both segments, with Hydraulics typically contributing a larger share. Helios sells through direct channels to original equipment manufacturers (OEMs) and through distributor networks. The company has made several purchases in recent years, including NEM S.r.l., Joyonway, Taimi R&D, Daman Products Company, Schultes Precision Manufacturing, and i3 Product Development. These acquisitions aim to expand product offerings, enhance technological capabilities, and access new markets.

4. Gas and Liquid Handling

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Parker-Hannifin (NYSE:PH), Eaton (NYSE:ETN), and Rexnord (NYSE:RXN).

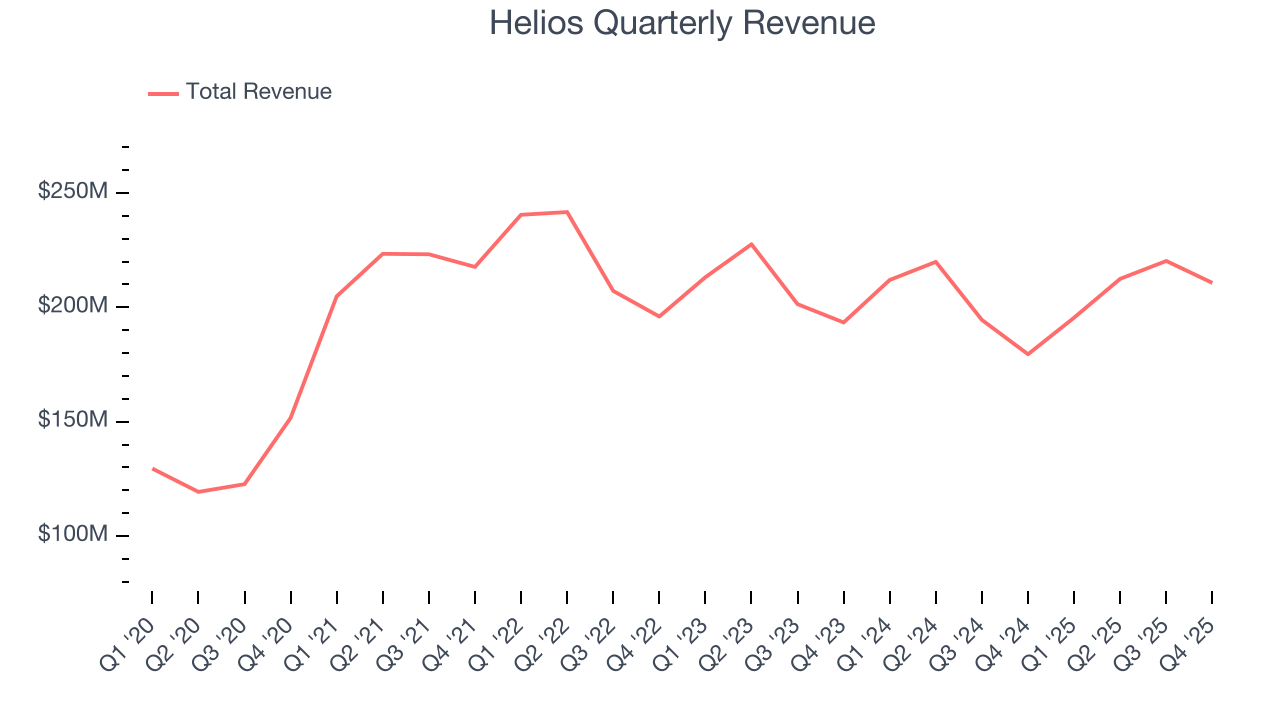

5. Revenue Growth

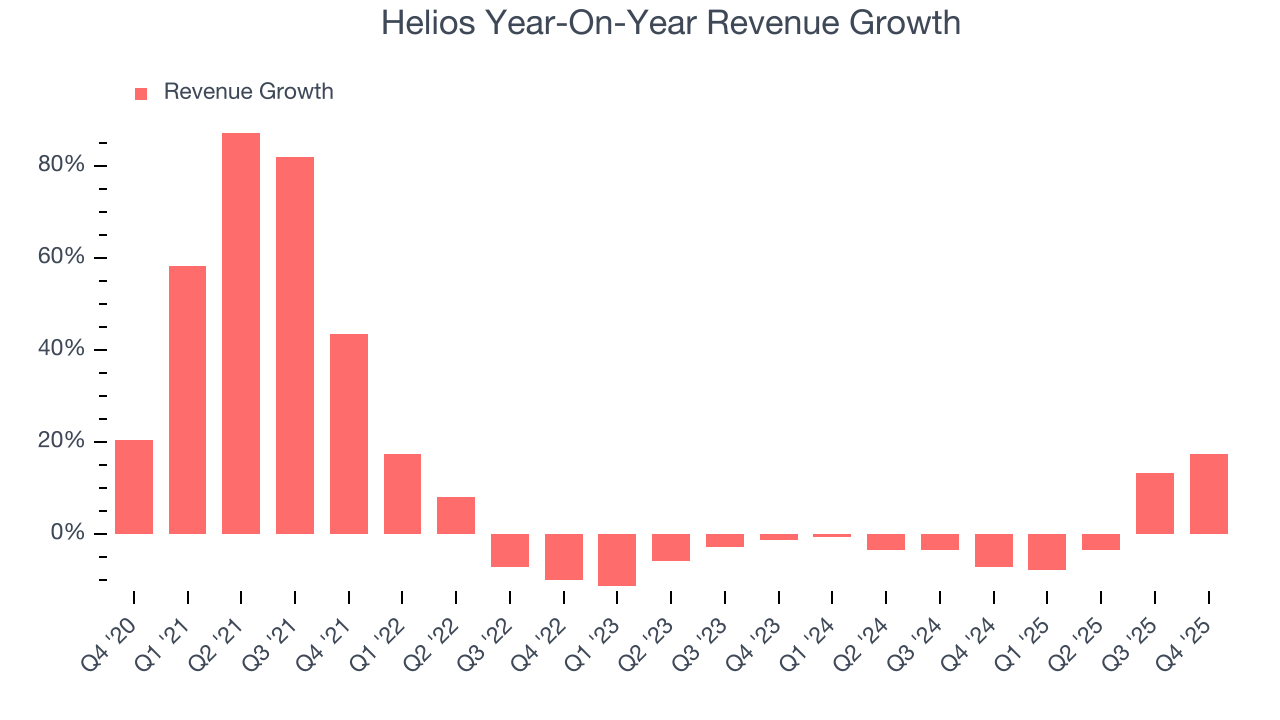

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Helios grew its sales at a solid 9.9% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Helios’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Helios’s organic revenue was flat. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Helios reported year-on-year revenue growth of 17.4%, and its $210.7 million of revenue exceeded Wall Street’s estimates by 6.4%. Company management is currently guiding for a 12.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 1.6% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

6. Gross Margin & Pricing Power

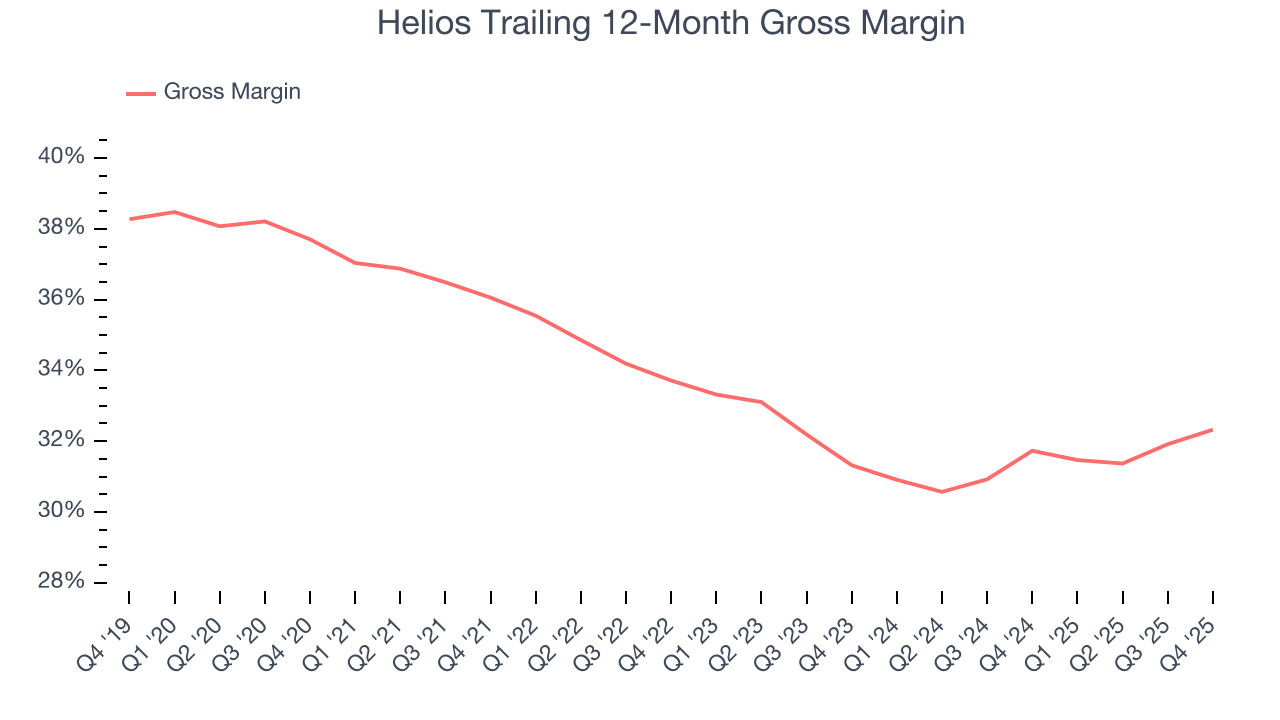

Helios’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 33.1% gross margin over the last five years. Said differently, Helios paid its suppliers $66.93 for every $100 in revenue.

In Q4, Helios produced a 33.6% gross profit margin, up 1.6 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

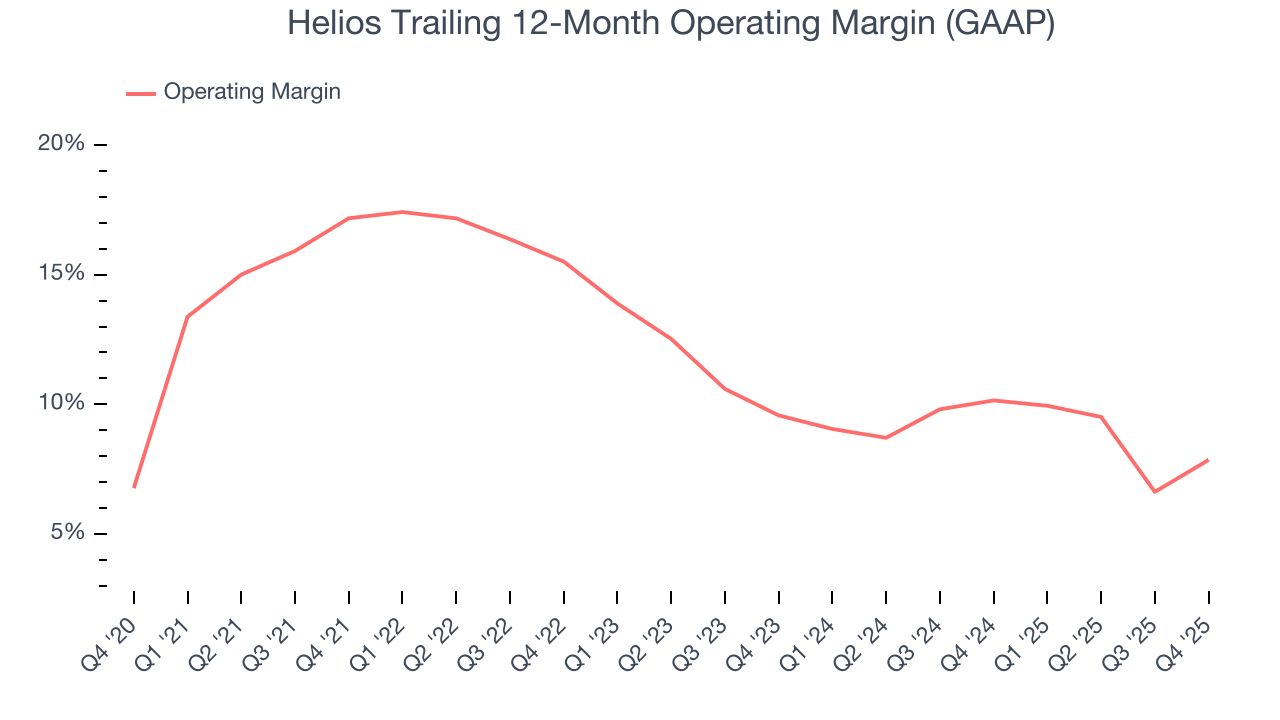

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Helios has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 12.1%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Helios’s operating margin decreased by 9.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Helios generated an operating margin profit margin of 12.2%, up 4.8 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

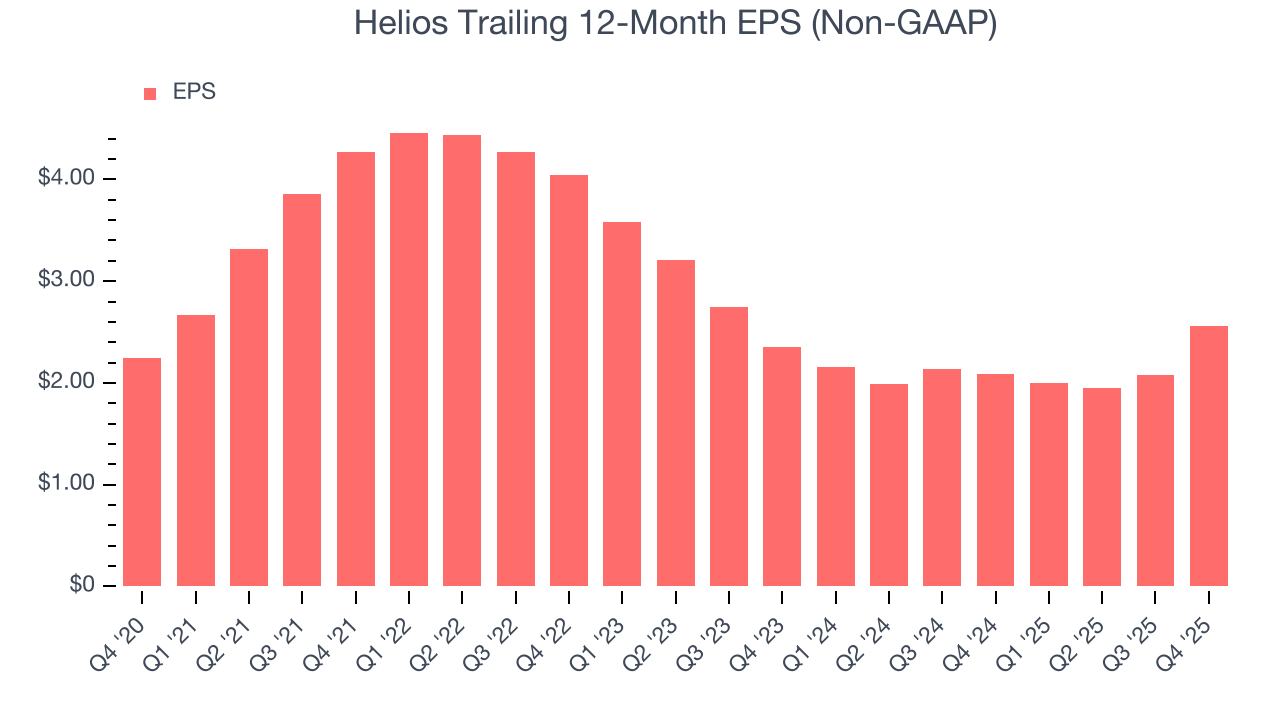

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Helios’s EPS grew at a weak 2.7% compounded annual growth rate over the last five years, lower than its 9.9% annualized revenue growth. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

Diving into the nuances of Helios’s earnings can give us a better understanding of its performance. As we mentioned earlier, Helios’s operating margin expanded this quarter but declined by 9.3 percentage points over the last five years. Its share count also grew by 3.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Helios, its two-year annual EPS growth of 4.4% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q4, Helios reported adjusted EPS of $0.81, up from $0.33 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Helios’s full-year EPS of $2.56 to grow 11.1%.

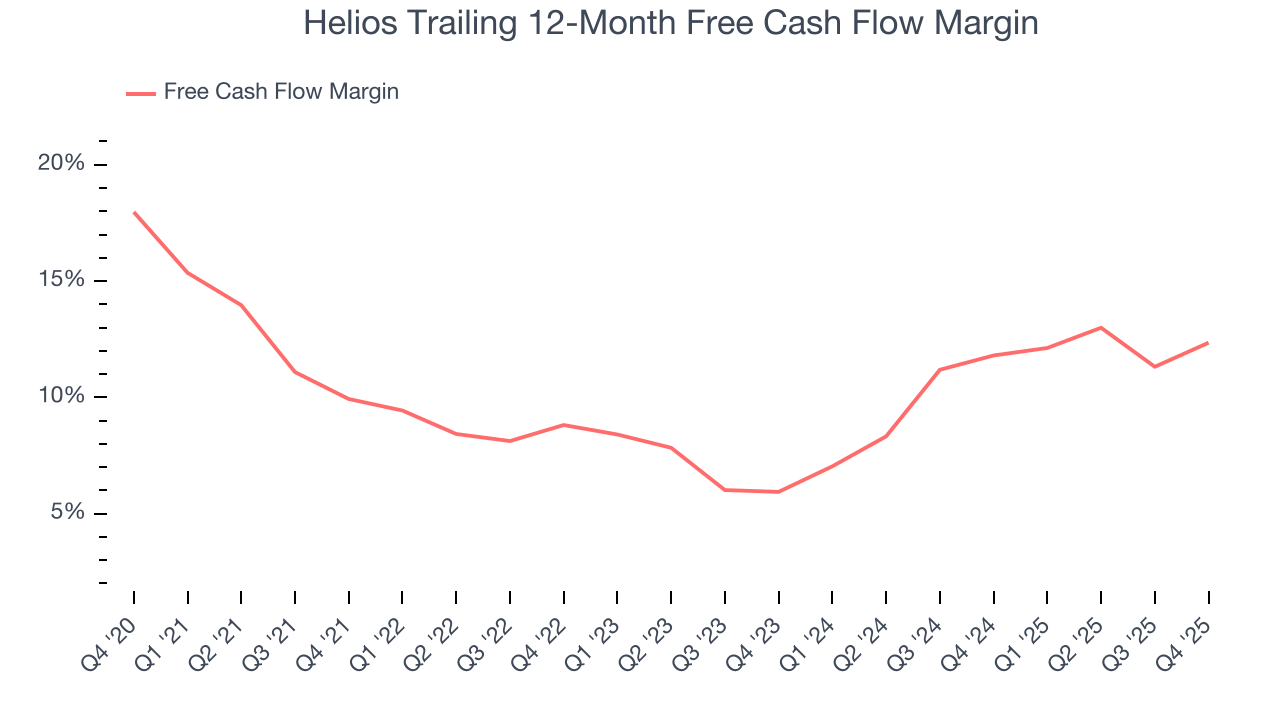

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Helios has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 9.7% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Helios’s margin expanded by 2.4 percentage points during that time. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Helios’s free cash flow clocked in at $40.5 million in Q4, equivalent to a 19.2% margin. This result was good as its margin was 3.5 percentage points higher than in the same quarter last year, building on its favorable historical trend.

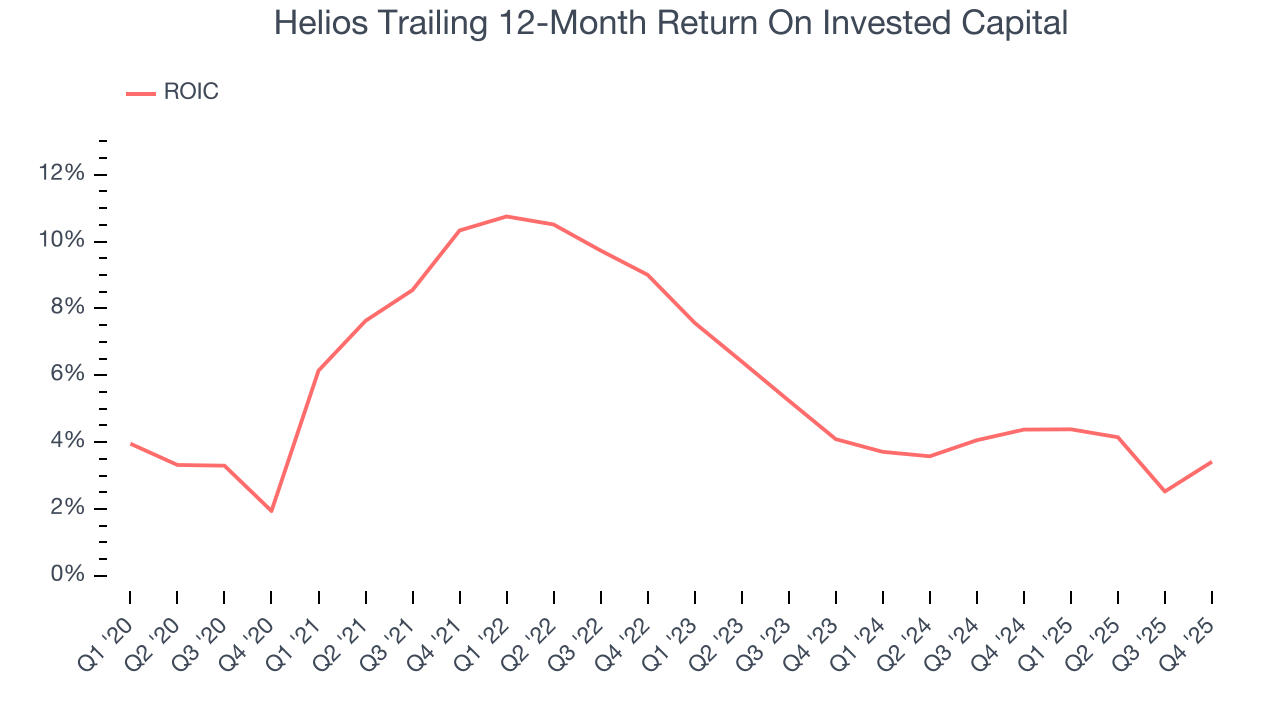

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Helios historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.2%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Helios’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

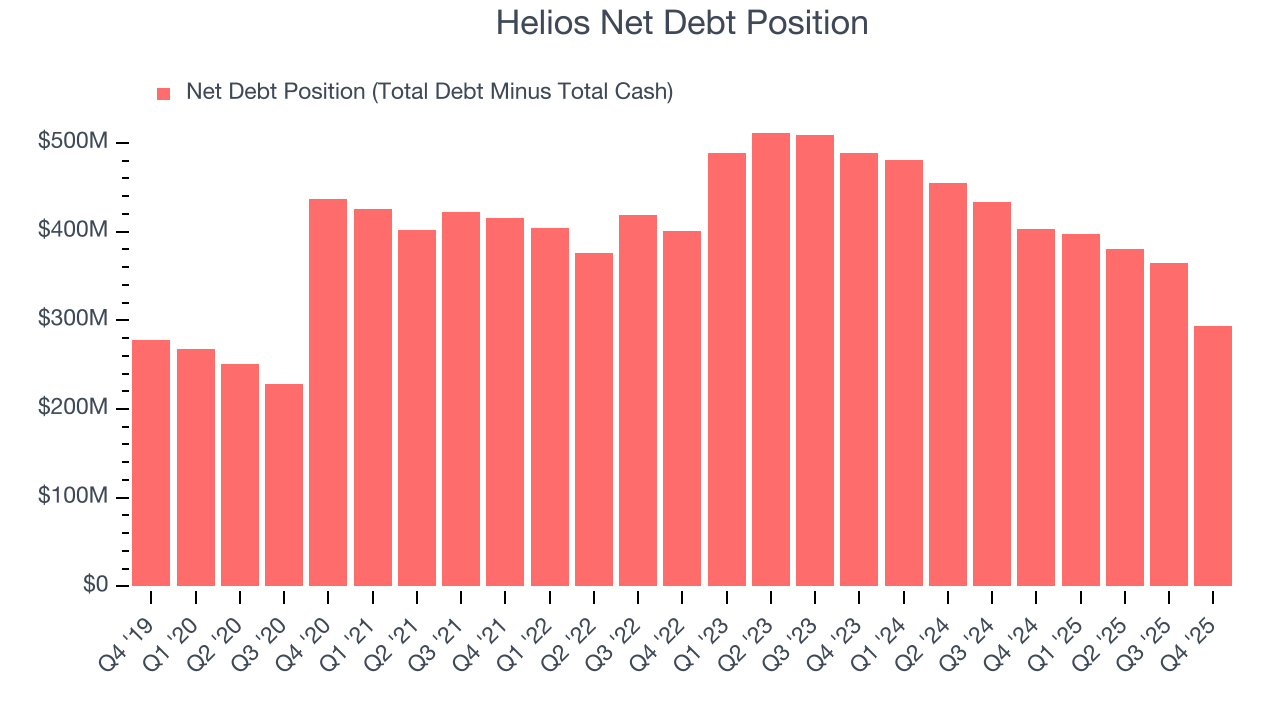

11. Balance Sheet Assessment

Helios reported $73 million of cash and $367.1 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $160.7 million of EBITDA over the last 12 months, we view Helios’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $20.7 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Helios’s Q4 Results

We were impressed by Helios’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its organic revenue was in line. Overall, we think this was still a solid quarter with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 1.8% to $73 immediately following the results.

13. Is Now The Time To Buy Helios?

Updated: March 24, 2026 at 11:35 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Helios.

We see the value of companies helping their customers, but in the case of Helios, we’re out. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its diminishing returns show management's prior bets haven't worked out. And while the company’s sturdy operating margins show it has disciplined cost controls, the downside is its declining operating margin shows the business has become less efficient.

Helios’s P/E ratio based on the next 12 months is 23.3x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $79.50 on the company (compared to the current share price of $68.51).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.