Hercules Capital (HTGC)

We’re cautious of Hercules Capital. Its decelerating revenue growth and even worse EPS performance give us little confidence it can beat the market.― StockStory Analyst Team

1. News

2. Summary

Why We Think Hercules Capital Will Underperform

Named after the mythological hero known for his strength, Hercules Capital (NYSE:HTGC) is a business development company that provides debt financing to venture capital-backed and growth-stage technology and life sciences companies.

- Performance over the past five years shows its incremental sales were less profitable, as its 6.5% annual earnings per share growth trailed its revenue gains

- A silver lining is that its stellar return on equity showcases management’s ability to surface highly profitable business ventures

Hercules Capital doesn’t check our boxes. There are better opportunities in the market.

Why There Are Better Opportunities Than Hercules Capital

Hercules Capital is trading at $18.37 per share, or 9.3x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Hercules Capital (HTGC) Research Report: Q3 CY2025 Update

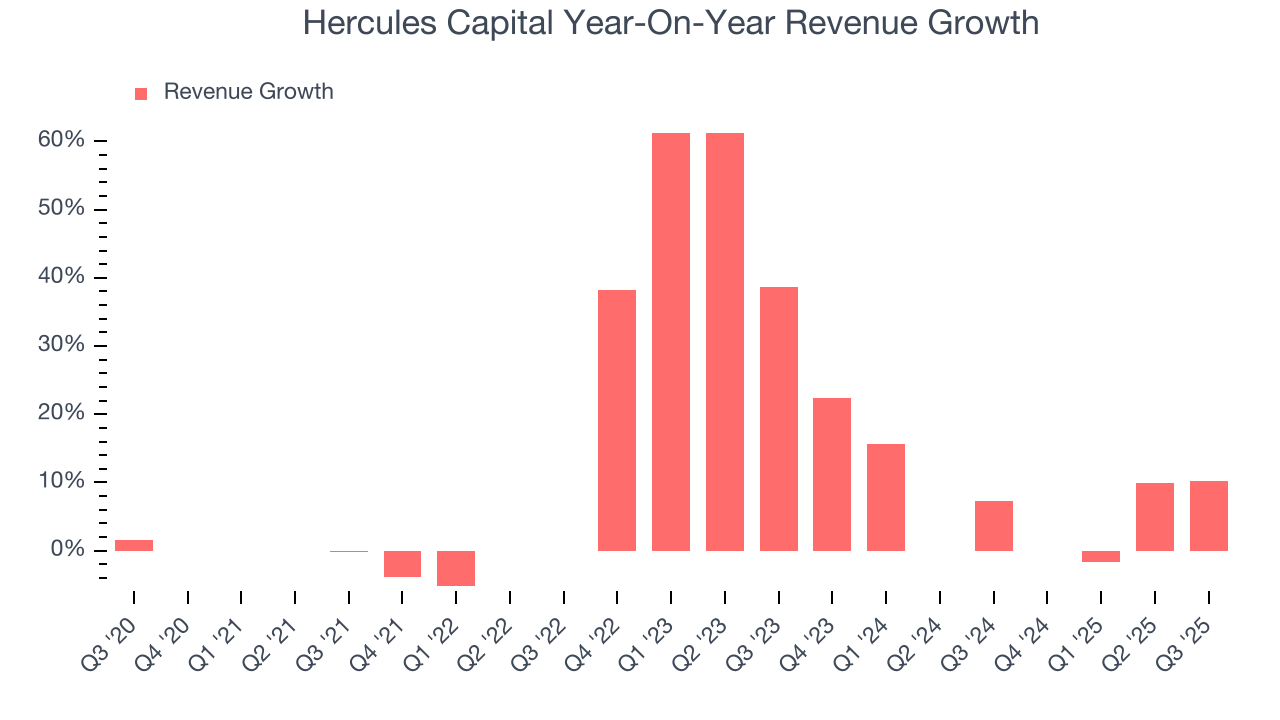

Specialty finance company Hercules Capital (NYSE:HTGC) met Wall Streets revenue expectations in Q3 CY2025, with sales up 10.3% year on year to $138.1 million. Its GAAP profit of $0.63 per share was 31.3% above analysts’ consensus estimates.

Hercules Capital (HTGC) Q3 CY2025 Highlights:

Company Overview

Named after the mythological hero known for his strength, Hercules Capital (NYSE:HTGC) is a business development company that provides debt financing to venture capital-backed and growth-stage technology and life sciences companies.

Hercules Capital operates as a specialty finance firm focused on providing senior secured loans to high-growth, innovative companies in technology, life sciences, and sustainable and renewable technology industries. These loans typically range from $15 million to $100 million and serve as an alternative to equity financing for companies that need capital but want to avoid further ownership dilution.

The company's business model centers on identifying promising ventures that have already secured equity backing from established venture capital firms. This approach allows Hercules to leverage the due diligence and oversight provided by these equity investors while offering complementary debt financing. For example, a biotech company that has completed early clinical trials might secure a Hercules loan to fund its Phase III trials without having to issue additional shares.

Hercules generates revenue primarily through interest payments on its loans, which typically carry higher rates than conventional bank financing, reflecting the higher risk profile of growth-stage companies. The firm also often receives warrant coverage or equity participation rights as part of its financing packages, providing potential upside if portfolio companies succeed.

As a business development company (BDC), Hercules operates under regulations requiring it to distribute at least 90% of its taxable income to shareholders as dividends. This structure makes it a potential income-generating investment vehicle. The company maintains investment professionals with deep sector expertise who evaluate potential borrowers based on their technology, market opportunity, management team, and existing investor support.

4. Specialty Finance

Specialty finance companies provide targeted lending or financial services for specific industries or needs. They benefit from expertise in particular sectors, often reduced competition in specialized niches, and tailored underwriting that can yield higher margins. Challenges include concentration risk in specific industries, difficulty achieving scale efficiencies, and potential vulnerability during sector-specific downturns affecting their specialized markets.

Hercules Capital competes with other business development companies like Ares Capital (NASDAQ:ARCC), TriplePoint Venture Growth (NYSE:TPVG), and Horizon Technology Finance (NASDAQ:HRZN), as well as with venture debt providers such as Silicon Valley Bank (now part of First Citizens BancShares) and specialized divisions of larger financial institutions.

5. Revenue Growth

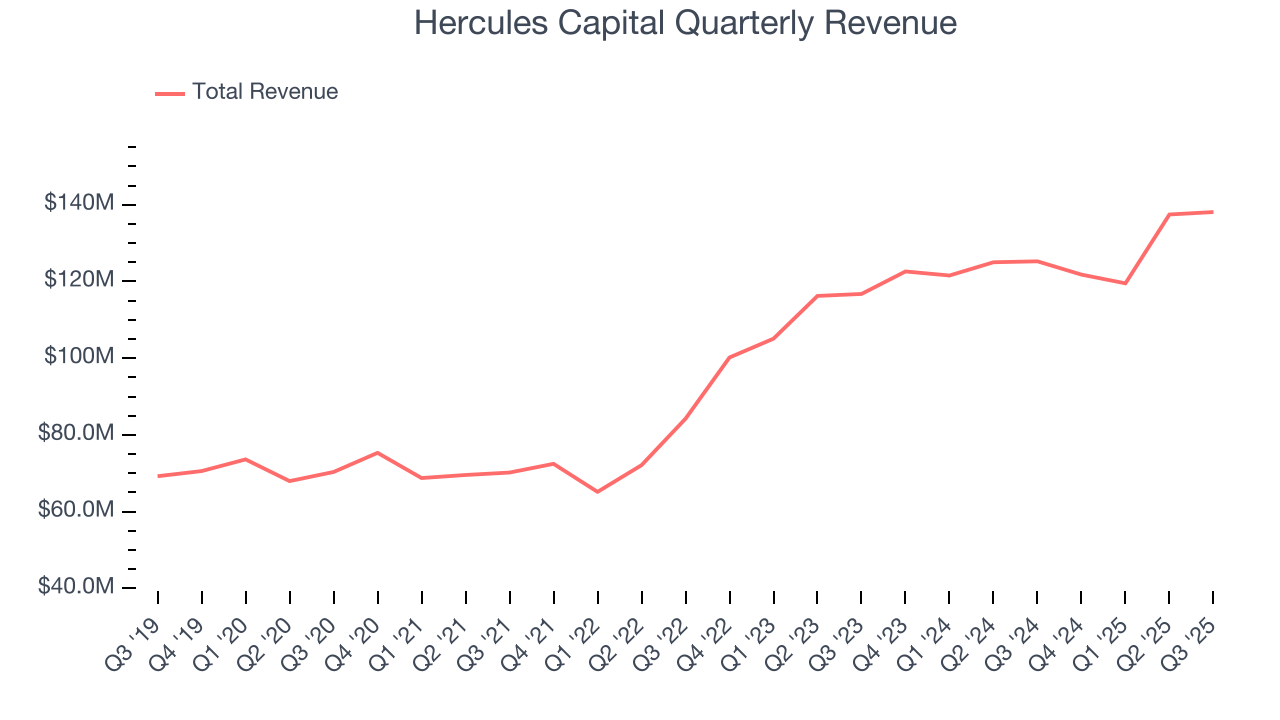

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Hercules Capital’s 12.8% annualized revenue growth over the last five years was solid. Its growth beat the average financials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Hercules Capital’s annualized revenue growth of 8.6% over the last two years is below its five-year trend, but we still think the results were respectable.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Hercules Capital’s year-on-year revenue growth was 10.3%, and its $138.1 million of revenue was in line with Wall Street’s estimates.

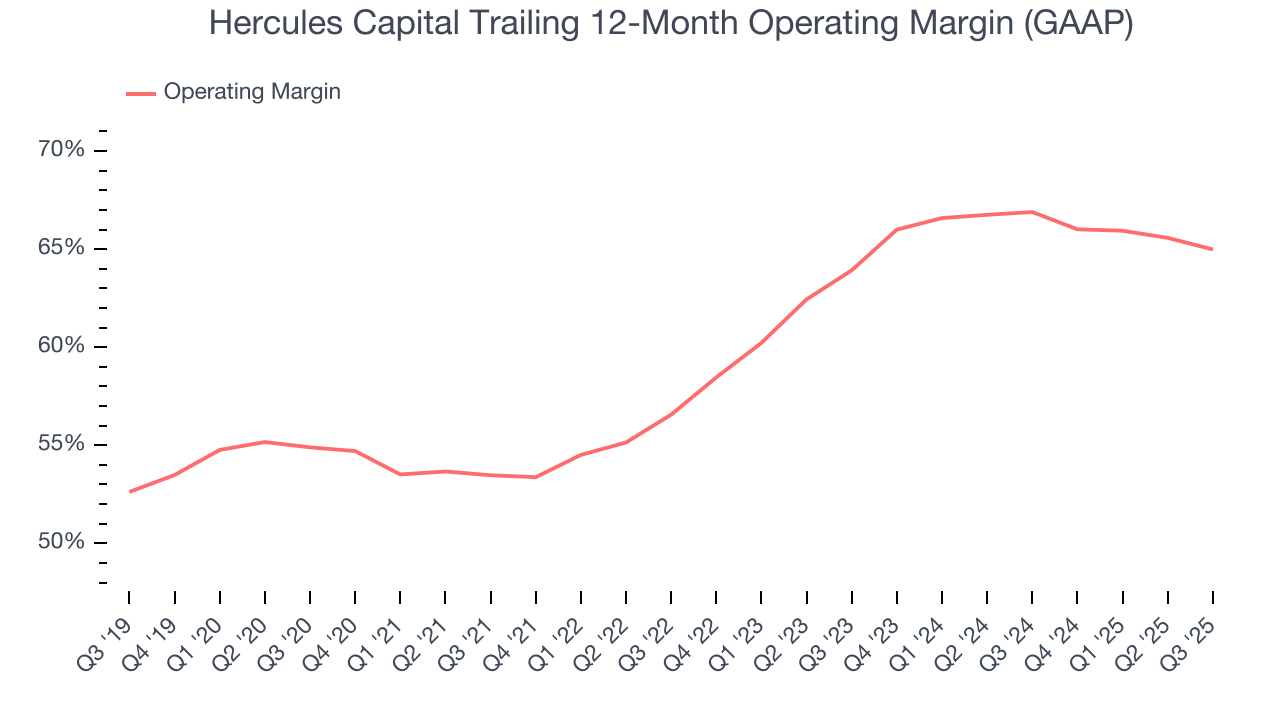

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Over the last five years, Hercules Capital’s operating margin has fallen by 11.5 percentage points, going from 53.5% to 65%. However, the company gave back some of its expense savings as its operating margin declined by 1.9 percentage points on a two-year basis.

Hercules Capital’s operating margin came in at 64.1% this quarter. This result was 2.3 percentage points worse than the same quarter last year.

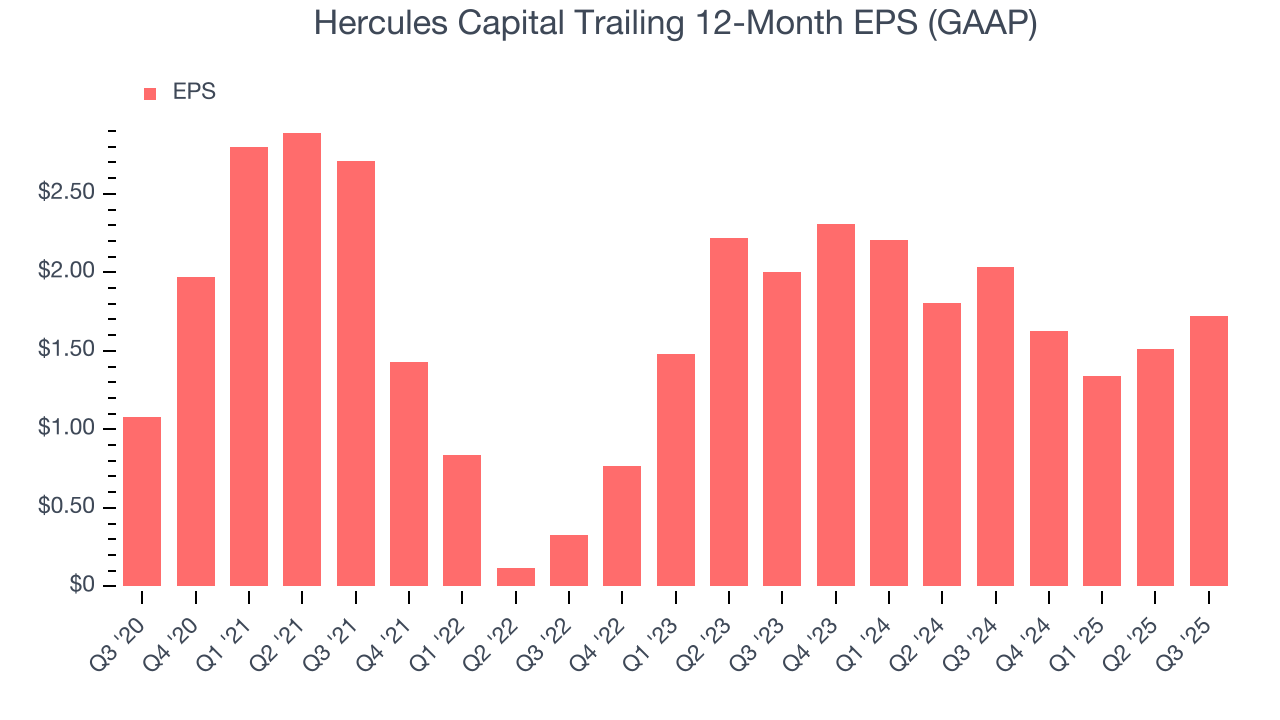

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Hercules Capital’s EPS grew at an unimpressive 9.8% compounded annual growth rate over the last five years, lower than its 12.8% annualized revenue growth. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Hercules Capital, its two-year annual EPS declines of 7.3% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Hercules Capital reported EPS of $0.63, up from $0.42 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

8. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Hercules Capital has averaged an ROE of 15.7%, healthy for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for Hercules Capital.

9. Balance Sheet Assessment

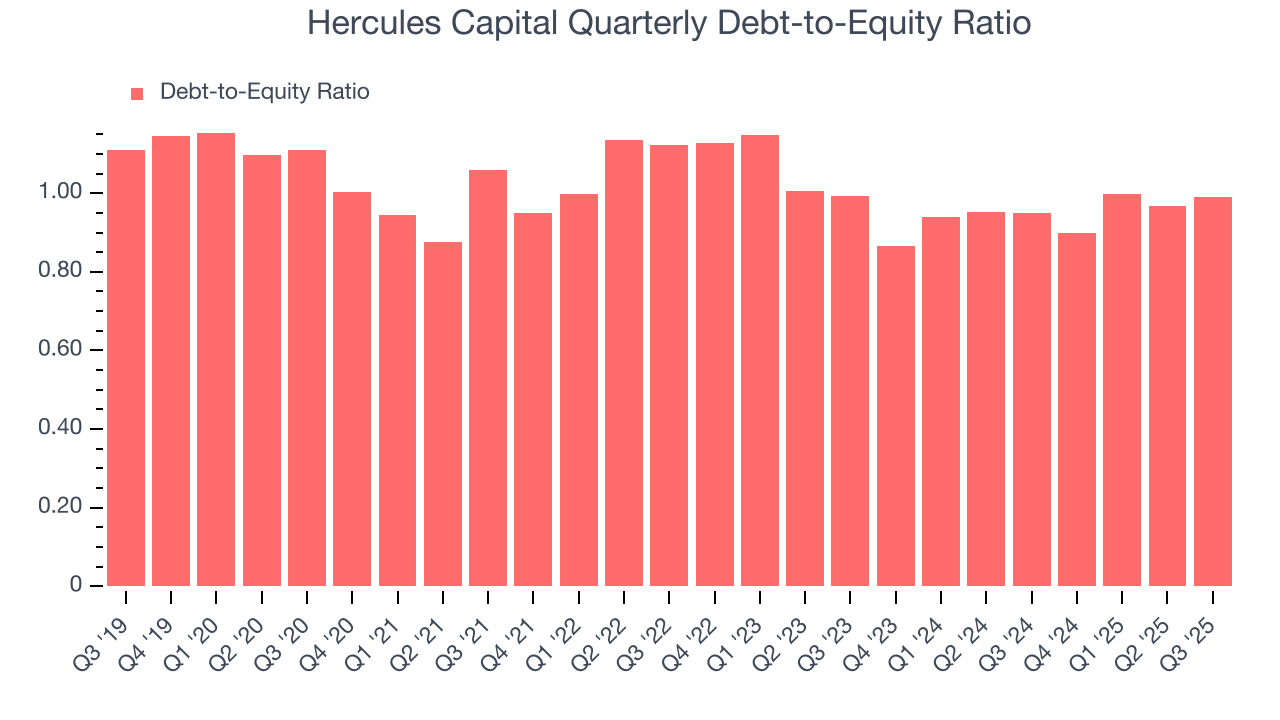

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Hercules Capital currently has $2.17 billion of debt and $2.19 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 1×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from Hercules Capital’s Q3 Results

It was good to see Hercules Capital beat analysts’ EPS expectations this quarter. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $17.85 immediately following the results.

11. Is Now The Time To Buy Hercules Capital?

Updated: January 30, 2026 at 1:31 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Hercules Capital’s business quality ultimately falls short of our standards. Although its revenue growth was solid over the last five years and Wall Street believes it will continue to grow, its unimpressive EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders.

Hercules Capital’s P/E ratio based on the next 12 months is 9.3x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $20.92 on the company (compared to the current share price of $18.38).