Ibotta (IBTA)

Ibotta is interesting. Its blend of high growth and outstanding profitability makes for a nice return algorithm.― StockStory Analyst Team

1. News

2. Summary

Why Ibotta Is Interesting

Originally launched as a way to make grocery shopping more rewarding for budget-conscious consumers, Ibotta (NYSE:IBTA) is a mobile shopping app that allows consumers to earn cash back on everyday purchases by completing tasks and submitting receipts.

- Impressive 23.3% annual revenue growth over the last three years indicates it’s winning market share this cycle

- Additional sales over the last three years increased its profitability as the 26.5% annual growth in its earnings per share outpaced its revenue

- One risk is its projected sales are flat for the next 12 months, implying demand will slow from its two-year trend

Ibotta is solid, but not perfect. If you’re a believer, the valuation looks reasonable.

Why Is Now The Time To Buy Ibotta?

Ibotta is trading at $29.05 per share, or 20.5x forward P/E. While this multiple is higher than most business services companies, we think the valuation is deserved for the revenue growth you get.

It could be a good time to invest if you see something the market doesn’t.

3. Ibotta (IBTA) Research Report: Q4 CY2025 Update

Cash-back rewards platform Ibotta (NYSE:IBTA) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 10% year on year to $88.53 million. On top of that, next quarter’s revenue guidance ($80 million at the midpoint) was surprisingly good and 7.9% above what analysts were expecting. Its GAAP loss of $0.04 per share was $0.02 below analysts’ consensus estimates.

Ibotta (IBTA) Q4 CY2025 Highlights:

- Revenue: $88.53 million vs analyst estimates of $83.14 million (10% year-on-year decline, 6.5% beat)

- EPS (GAAP): -$0.04 vs analyst estimates of -$0.02 ($0.02 miss)

- Adjusted EBITDA: $13.72 million vs analyst estimates of $11.36 million (15.5% margin, 20.7% beat)

- Revenue Guidance for Q1 CY2026 is $80 million at the midpoint, above analyst estimates of $74.14 million

- EBITDA guidance for Q1 CY2026 is $7 million at the midpoint, above analyst estimates of $6.40 million

- Operating Margin: -1.9%, down from 13.2% in the same quarter last year

- Free Cash Flow Margin: 18.8%, similar to the same quarter last year

- Total Redemptions: 73.98 million at quarter end

- Market Capitalization: $546.3 million

Company Overview

Originally launched as a way to make grocery shopping more rewarding for budget-conscious consumers, Ibotta (NYSE:IBTA) is a mobile shopping app that allows consumers to earn cash back on everyday purchases by completing tasks and submitting receipts.

Ibotta operates at the intersection of retail, advertising, and financial technology. The platform works by partnering with consumer packaged goods (CPG) companies, retailers, and brands who pay to promote their products through targeted offers on the Ibotta app. When users purchase these promoted items and verify their purchases by uploading receipts or linking loyalty accounts, they receive cash back rewards that can be transferred to their bank accounts or redeemed as gift cards.

The company's business model creates value for multiple stakeholders. For consumers, it provides financial incentives on purchases they would likely make anyway. For brands and retailers, it offers a performance-based marketing channel that drives sales and provides valuable consumer purchase data. Ibotta only gets paid when a consumer actually buys a product, making it an attractive alternative to traditional advertising for brands seeking measurable returns on their marketing investments.

A typical Ibotta user might open the app before heading to the grocery store, browse available offers (like $1 back on a specific brand of cereal or 50 cents back on any brand of milk), add these offers to their account, and then upload their receipt after shopping to claim their rewards. The company has expanded beyond groceries to include cash back opportunities at restaurants, travel sites, online retailers, and subscription services.

Ibotta's technology platform incorporates elements of machine learning to personalize offers based on user shopping patterns and preferences. The company has built an extensive network of partnerships with major retailers including Walmart, Target, Kroger, and Amazon, as well as with hundreds of consumer brands.

Beyond its consumer app, Ibotta also operates the Ibotta Performance Network (IPN), which extends its cash back offers to partner platforms and retailer websites, allowing brands to reach consumers through multiple digital touchpoints. This network approach has helped Ibotta scale its reach beyond its direct user base.

4. Advertising & Marketing Services

The sector is on the precipice of both disruption and growth as AI, programmatic advertising, and data-driven marketing reshape how things are done. For example, the advent of the Internet broadly and programmatic advertising specifically means that brand building is not a relationship business anymore but instead one based on data and technology, which could hurt traditional ad agencies. On the other hand, the companies in the sector that beef up their tech chops by automating the buying of ad inventory or facilitating omnichannel marketing, for example, stand to benefit. With or without advances in digitization and AI, the sector is still highly levered to the macro, and economic uncertainty may lead to fluctuating ad spend, particularly in cyclical industries.

Ibotta competes with other cash-back and shopping rewards platforms including Rakuten (formerly Ebates), Fetch Rewards, and Shopkick, as well as with credit card rewards programs and retailer-specific loyalty programs like Target Circle and Walmart+.

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

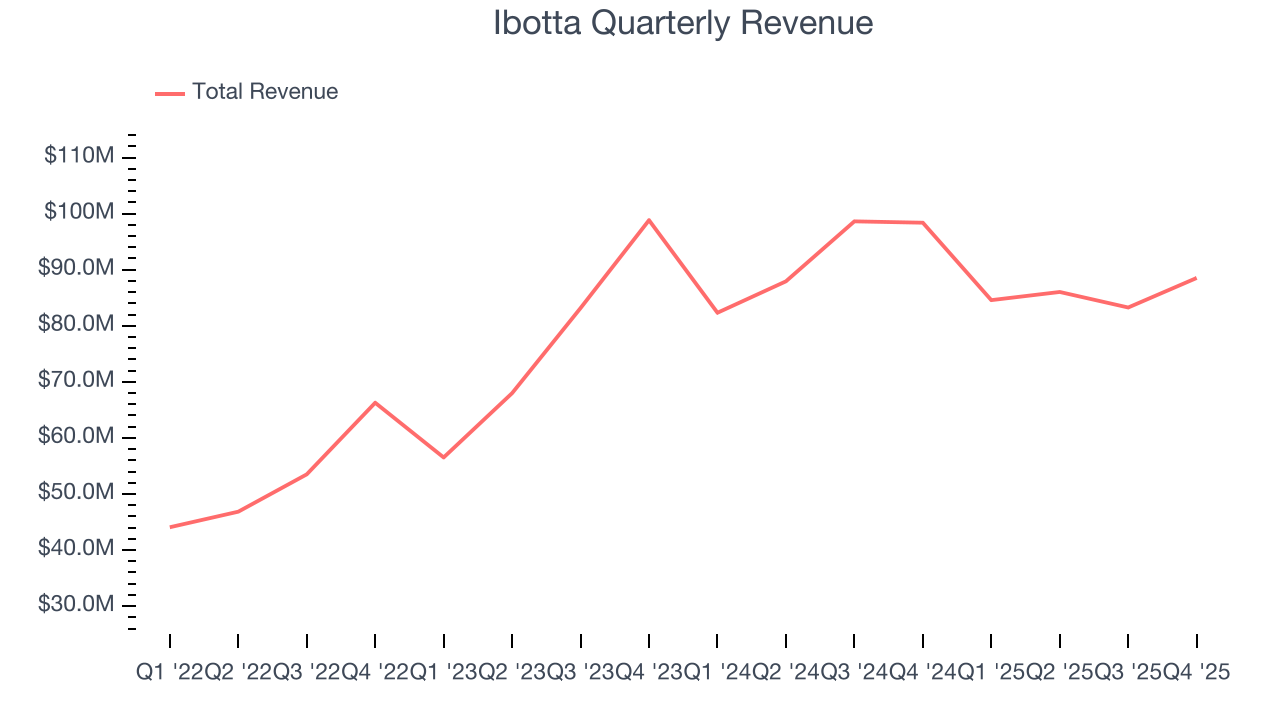

With $342.4 million in revenue over the past 12 months, Ibotta is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

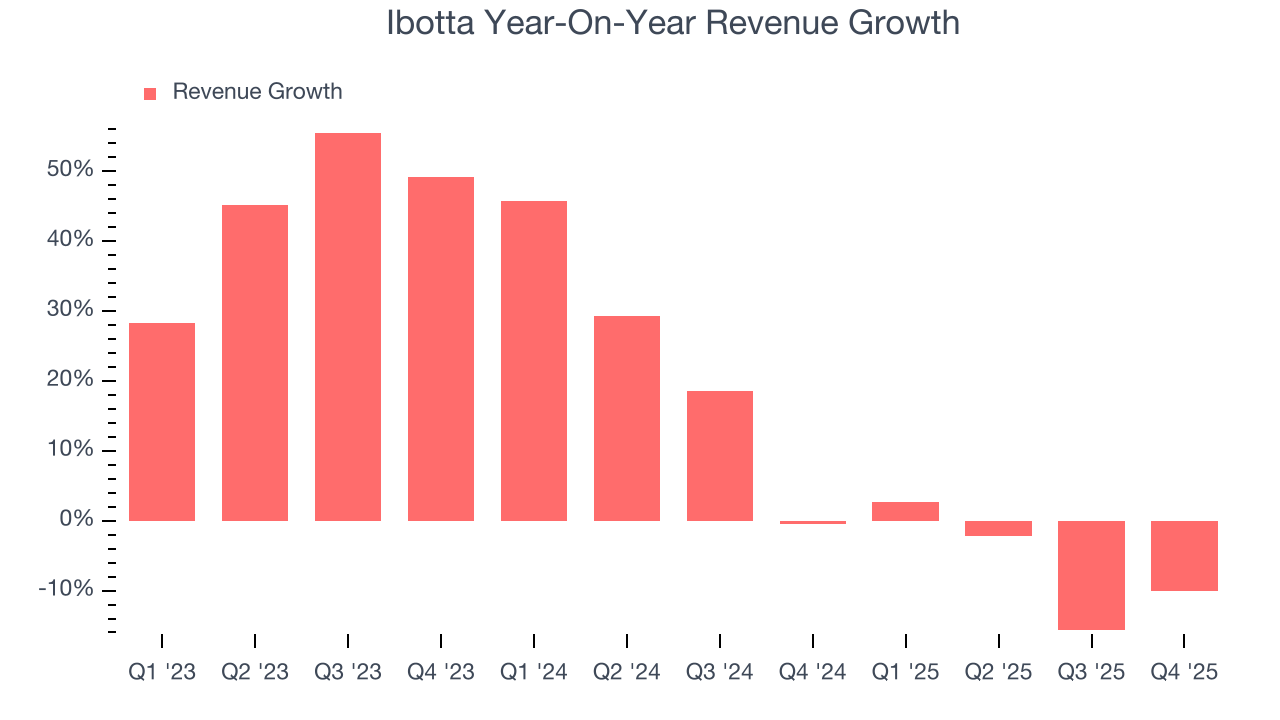

As you can see below, Ibotta grew its sales at an incredible 23.3% compounded annual growth rate over the last three years. This is an encouraging starting point for our analysis because it shows Ibotta’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. Ibotta’s annualized revenue growth of 5.7% over the last two years is below its three-year trend, but we still think the results were respectable.

This quarter, Ibotta’s revenue fell by 10% year on year to $88.53 million but beat Wall Street’s estimates by 6.5%. Company management is currently guiding for a 5.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 6.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

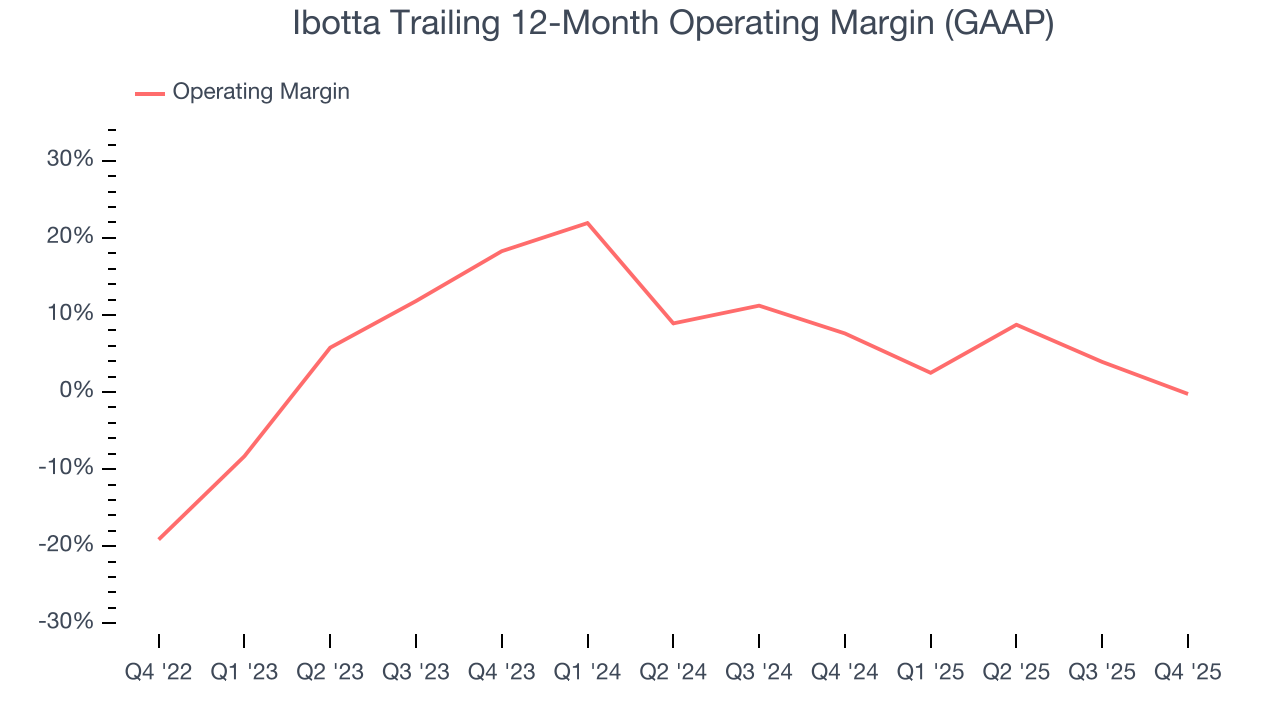

Ibotta was profitable over the last four years but held back by its large cost base. Its average operating margin of 3.5% was weak for a business services business.

On the plus side, Ibotta’s operating margin rose by 18.9 percentage points over the last four years, as its sales growth gave it immense operating leverage.

In Q4, Ibotta generated an operating margin profit margin of negative 1.9%, down 15 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

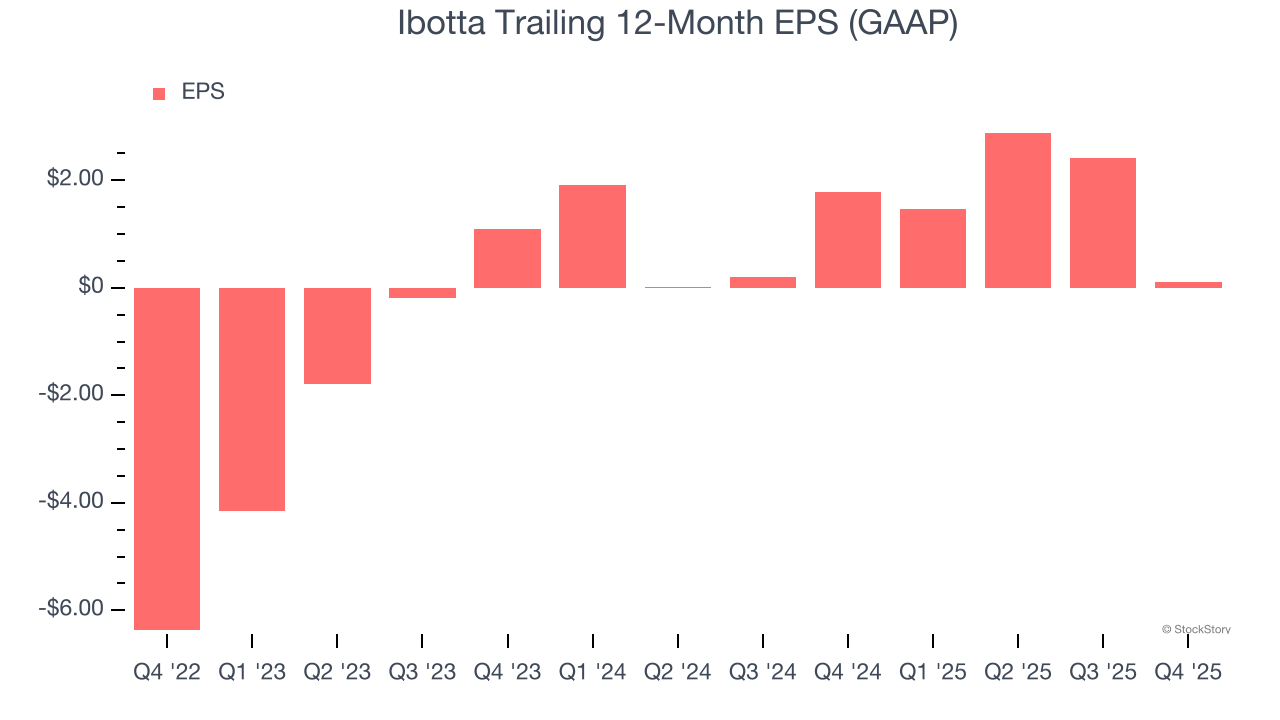

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Ibotta’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

In Q4, Ibotta reported EPS of negative $0.04, down from $2.27 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Ibotta to perform poorly. Analysts forecast its full-year EPS of $0.11 will invert to negative negative $0.64.

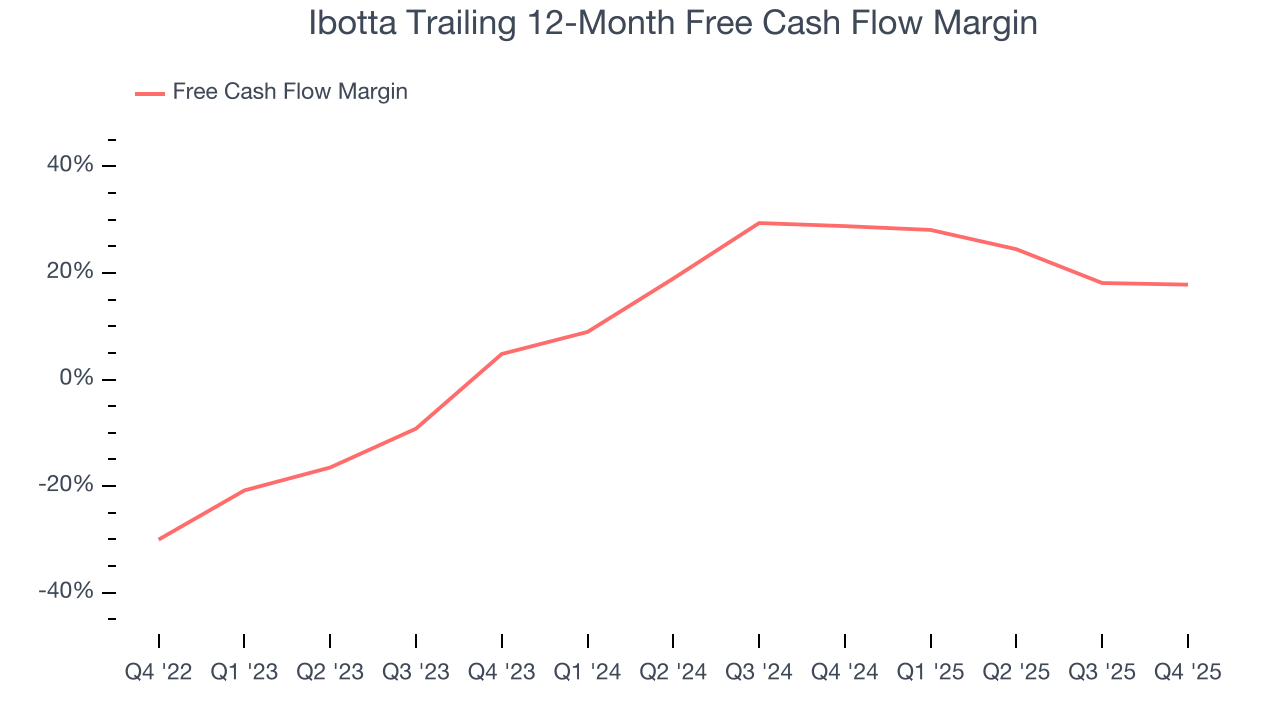

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Ibotta has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.6% over the last four years, quite impressive for a business services business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Ibotta’s margin expanded by 47.8 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Ibotta’s free cash flow clocked in at $16.63 million in Q4, equivalent to a 18.8% margin. This cash profitability was in line with the comparable period last year and above its four-year average.

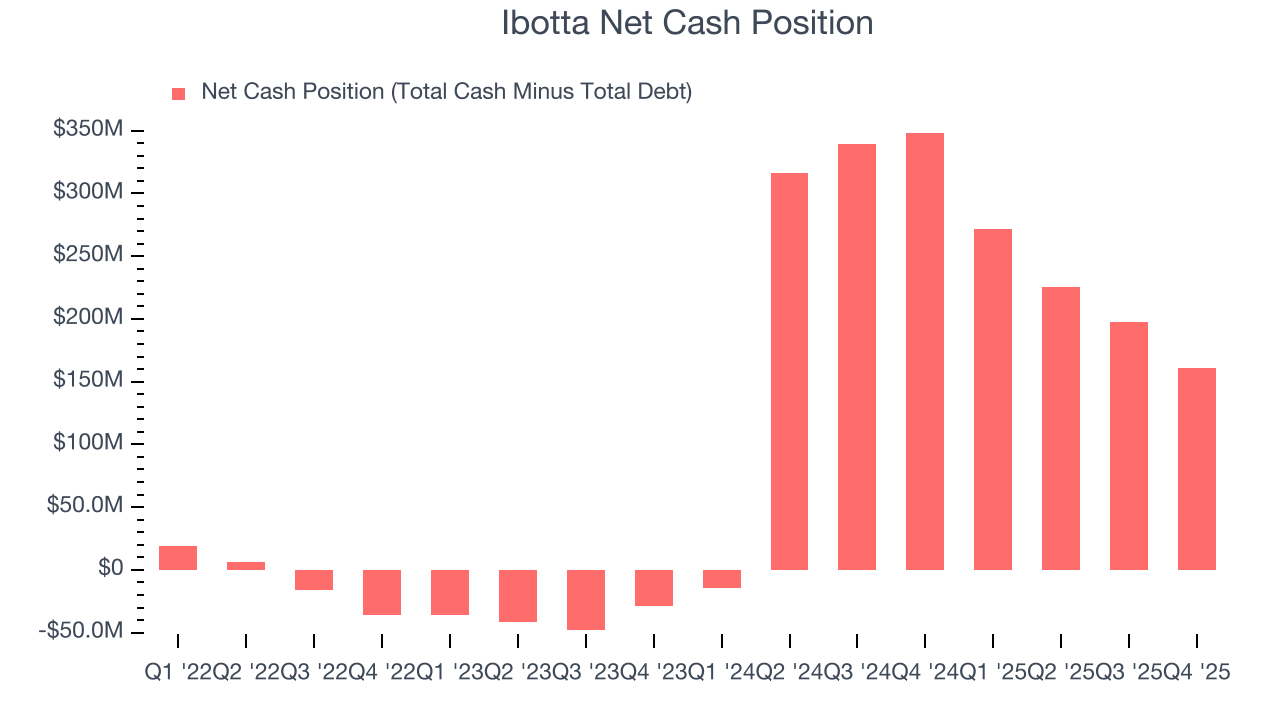

9. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Ibotta is a well-capitalized company with $186.6 million of cash and $25.5 million of debt on its balance sheet. This $161.1 million net cash position is 29.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

10. Key Takeaways from Ibotta’s Q4 Results

We were impressed by how significantly Ibotta blew past analysts’ revenue expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. On the other hand, its EPS was in line. Overall, this print had some key positives. The stock traded up 26.4% to $26 immediately following the results.

11. Is Now The Time To Buy Ibotta?

Updated: March 27, 2026 at 12:23 AM EDT

Before deciding whether to buy Ibotta or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

In our opinion, Ibotta is a good company. First off, its revenue growth was exceptional over the last three years. And while its projected EPS for the next year is lacking, its rising cash profitability gives it more optionality. On top of that, its expanding adjusted operating margin shows the business has become more efficient.

Ibotta’s P/E ratio based on the next 12 months is 20.5x. Looking at the business services space right now, Ibotta trades at a compelling valuation. For those confident in the business and its management team, this is a good time to invest.

Wall Street analysts have a consensus one-year price target of $27.86 on the company (compared to the current share price of $29.05).