Ingersoll Rand (IR)

Ingersoll Rand doesn’t excite us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why Ingersoll Rand Is Not Exciting

Started with the invention of the steam drill, Ingersoll Rand (NYSE:IR) provides mission-critical air, gas, liquid, and solid flow creation solutions.

- Core business is underperforming as its organic revenue has disappointed over the past two years, suggesting it might need acquisitions to stimulate growth

- Below-average returns on capital indicate management struggled to find compelling investment opportunities

- A positive is that its powerful free cash flow generation enables it to reinvest its profits or return capital to investors consistently, and its rising cash conversion increases its margin of safety

Ingersoll Rand is in the penalty box. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Ingersoll Rand

Ingersoll Rand is trading at $96.73 per share, or 27.4x forward P/E. This valuation is fair for the quality you get, but we’re on the sidelines for now.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Ingersoll Rand (IR) Research Report: Q4 CY2025 Update

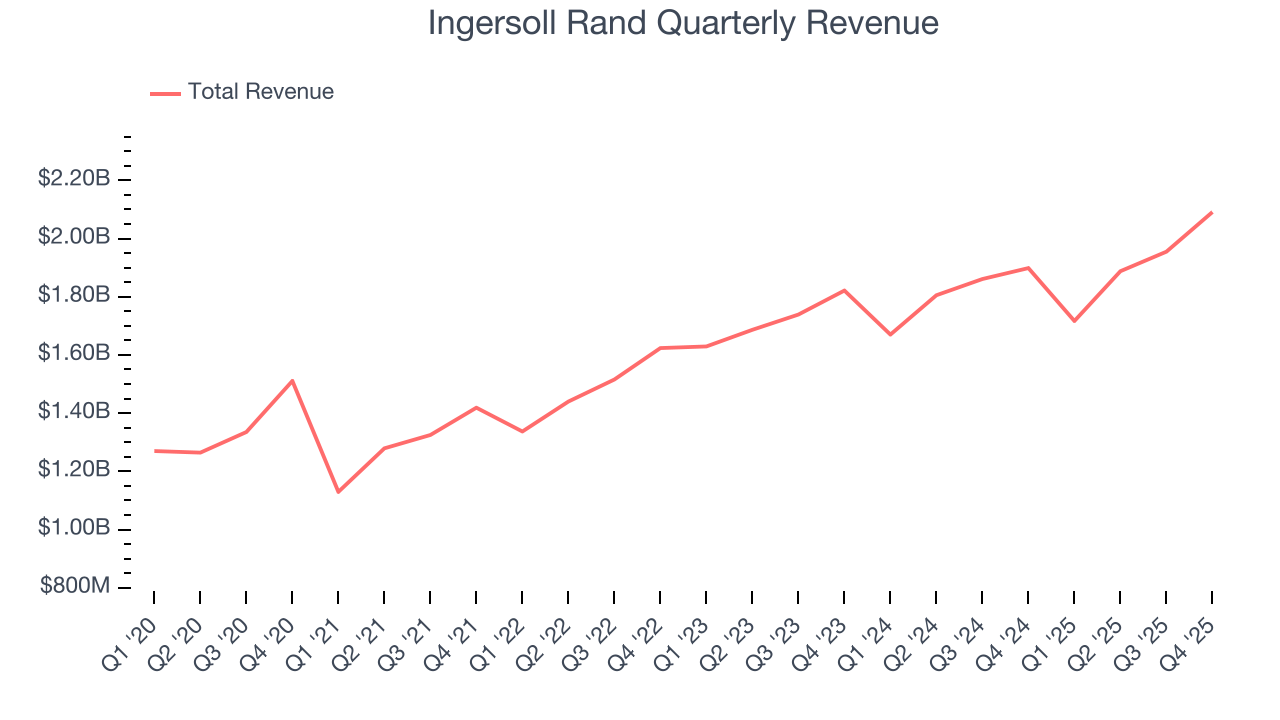

Industrial manufacturing company Ingersoll Rand (NYSE:IR) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 10.1% year on year to $2.09 billion. Its non-GAAP profit of $0.96 per share was 6.6% above analysts’ consensus estimates.

Ingersoll Rand (IR) Q4 CY2025 Highlights:

- Revenue: $2.09 billion vs analyst estimates of $2.04 billion (10.1% year-on-year growth, 2.6% beat)

- Adjusted EPS: $0.96 vs analyst estimates of $0.90 (6.6% beat)

- Adjusted EBITDA: $580.1 million vs analyst estimates of $560.3 million (27.7% margin, 3.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.51 at the midpoint, missing analyst estimates by 1.3%

- EBITDA guidance for the upcoming financial year 2026 is $2.16 billion at the midpoint, below analyst estimates of $2.19 billion

- Operating Margin: 18.7%, down from 20% in the same quarter last year

- Free Cash Flow Margin: 25.7%, similar to the same quarter last year

- Market Capitalization: $38.23 billion

Company Overview

Started with the invention of the steam drill, Ingersoll Rand (NYSE:IR) provides mission-critical air, gas, liquid, and solid flow creation solutions.

Ingersoll Rand is known for its range of industrial products, including air compressors and various construction and mining equipment. Today, the company manufactures an extensive range of compressors, pumps, vacuum, and blower products sold under many brands, including Gardner Denver and CompAir. These products are essential in industries such as life sciences, food and beverage, clean energy, and water treatment, where the cost of downtime is significant.

Due to this implication, customers place a high value on minimizing any operational downtime, allowing Ingersoll Rand to capitalize heavily on aftermarket parts and services associated with wear and tear replacement cycles of its products. Other examples of Ingersoll Rand products range from fastening systems and pneumatic bolting tools, used for the precision fastening of bolted joints in industrial machinery and vehicles, to liquid ring vacuum pumps and compressors, primarily used for applications such as flare gas recovery and chlorine compression.

Ingersoll Rand serves its customer base through a direct sales force for OEMs and end users requiring specialized support, complemented by a network of distributors for broader market coverage. It generates revenue through the sale of its products as well as its aftermarket services, which provide a source of recurring revenue.

The company pursues an aggressive acquisition strategy, consistently acquiring numerous companies to bolster its market position and expand its product portfolio. A notable example is its merger with Gardner Denver in 2020, which significantly expanded its capabilities in areas such as compression, blower, and vacuum technologies.

4. Gas and Liquid Handling

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Dover (NYSE:DOV), Xylem (NYSE:XYL), and Parker Hannifin (NYSE:PH).

5. Revenue Growth

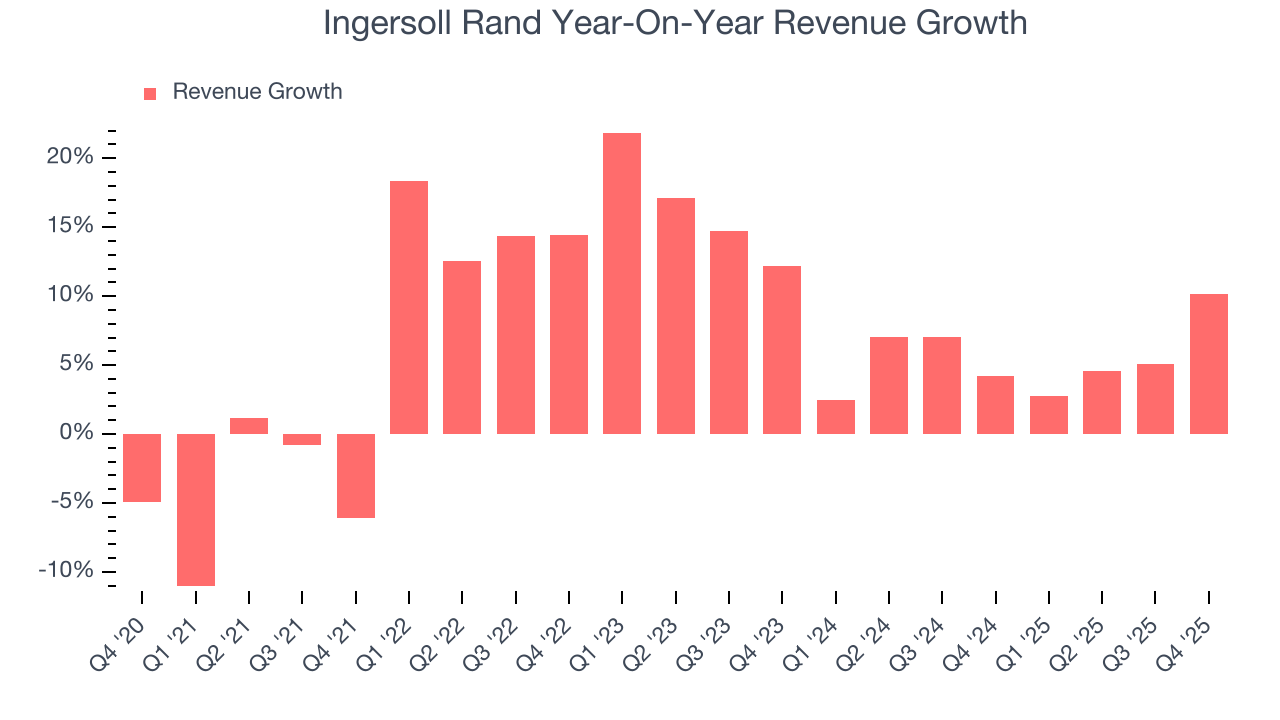

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Ingersoll Rand’s 7.3% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Ingersoll Rand’s recent performance shows its demand has slowed as its annualized revenue growth of 5.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Ingersoll Rand reported year-on-year revenue growth of 10.1%, and its $2.09 billion of revenue exceeded Wall Street’s estimates by 2.6%.

Looking ahead, sell-side analysts expect revenue to grow 4.1% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its products and services will see some demand headwinds.

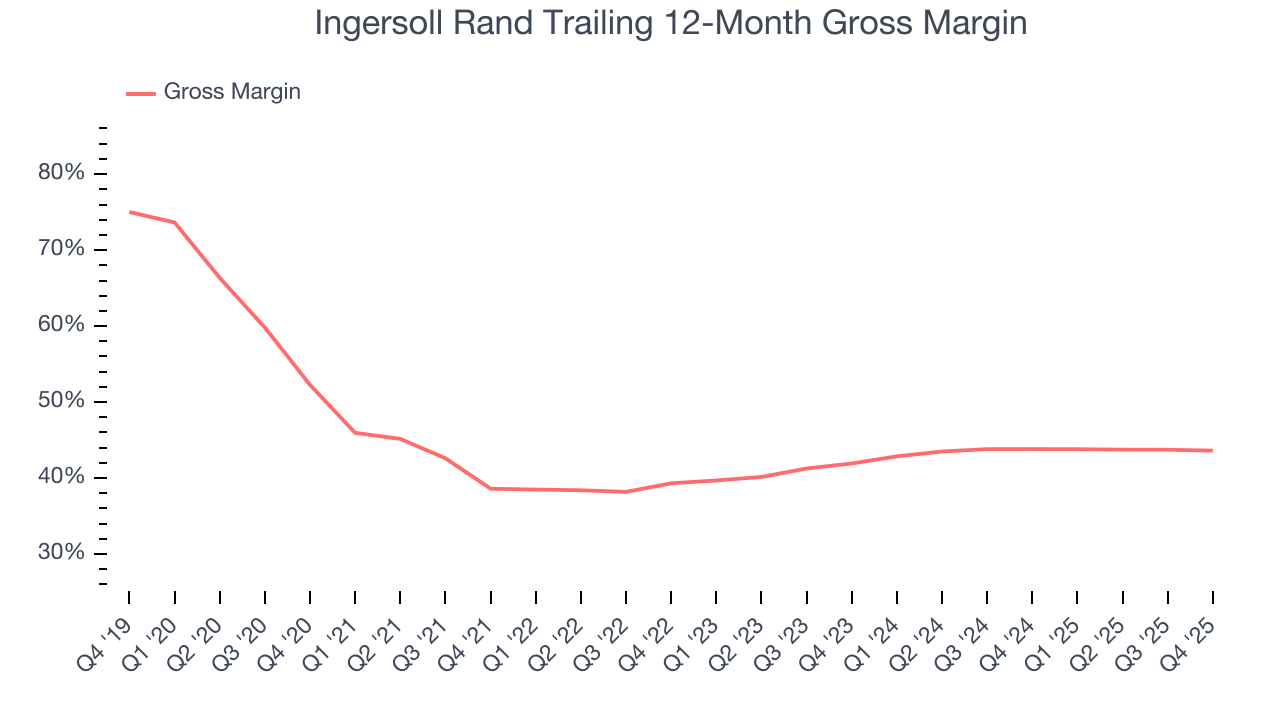

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Ingersoll Rand’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 41.7% gross margin over the last five years. Said differently, roughly $41.74 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

Ingersoll Rand produced a 42.6% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

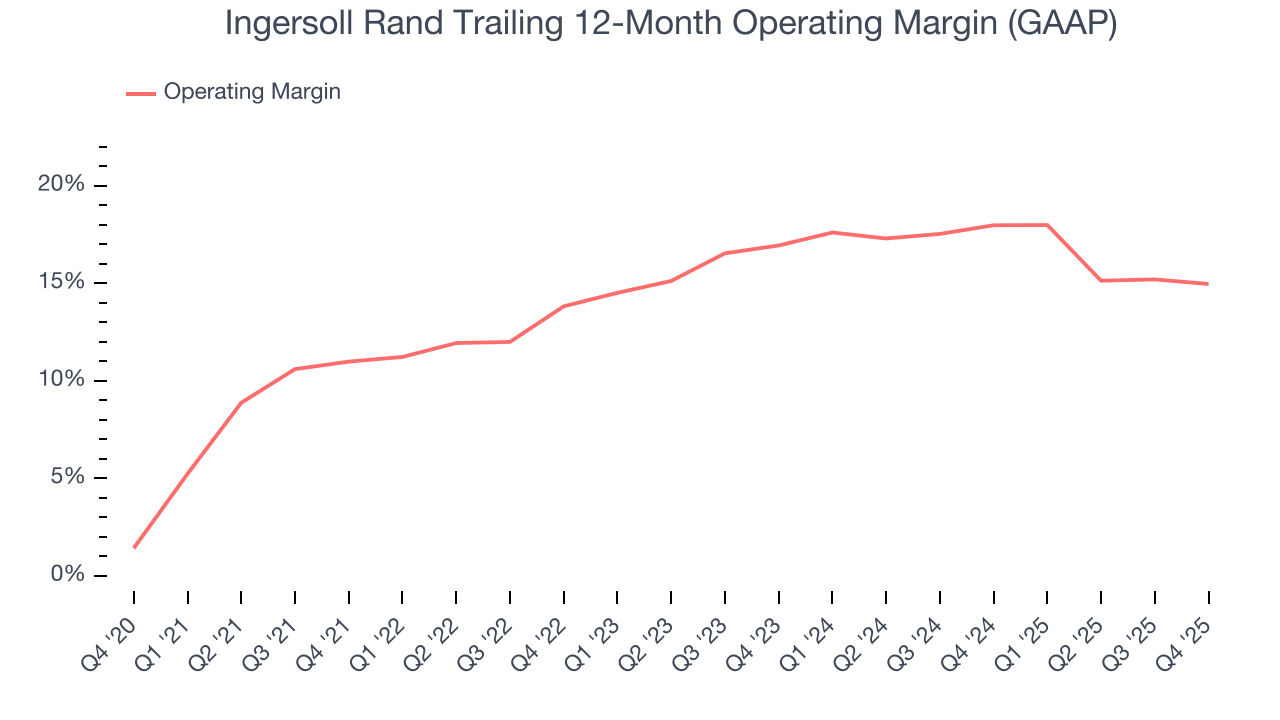

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Ingersoll Rand has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Ingersoll Rand’s operating margin rose by 4 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Ingersoll Rand generated an operating margin profit margin of 18.7%, down 1.3 percentage points year on year. Since Ingersoll Rand’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

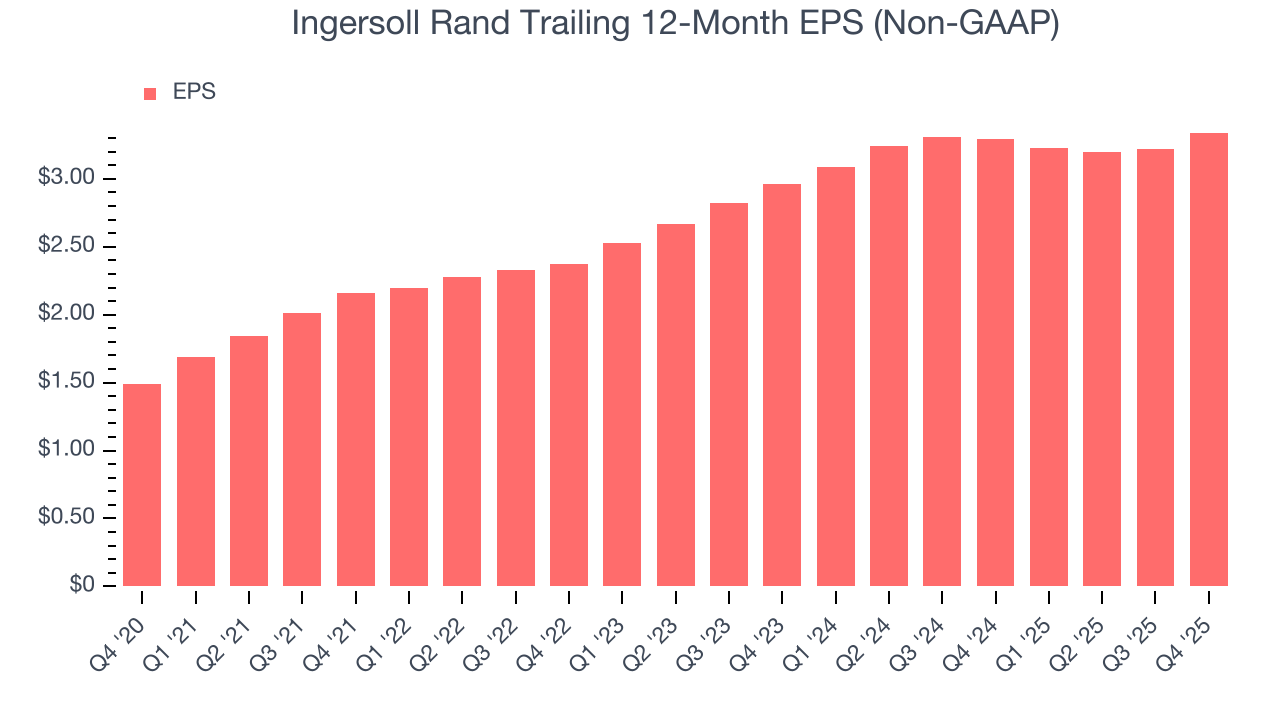

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

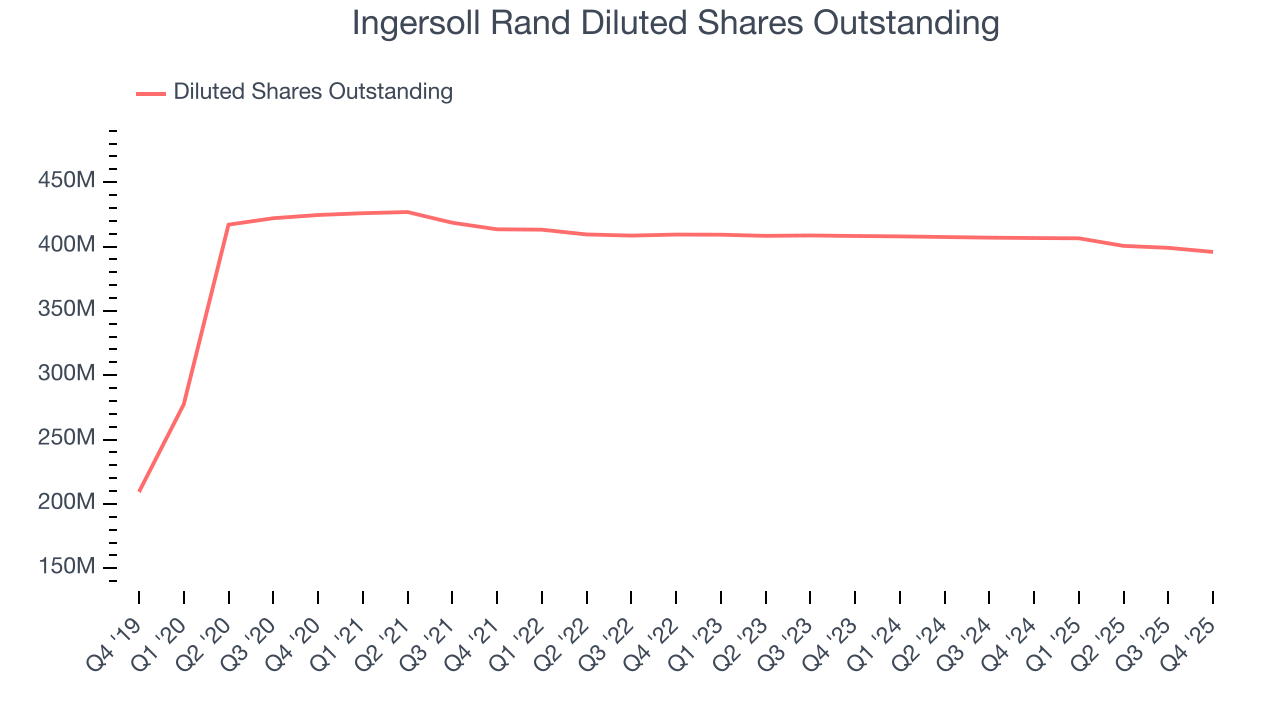

Ingersoll Rand’s EPS grew at an astounding 17.5% compounded annual growth rate over the last five years, higher than its 7.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Ingersoll Rand’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Ingersoll Rand’s operating margin declined this quarter but expanded by 4 percentage points over the last five years. Its share count also shrank by 6.8%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Ingersoll Rand, its two-year annual EPS growth of 6.2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Ingersoll Rand reported adjusted EPS of $0.96, up from $0.84 in the same quarter last year. This print beat analysts’ estimates by 6.6%. Over the next 12 months, Wall Street expects Ingersoll Rand’s full-year EPS of $3.34 to grow 6.6%.

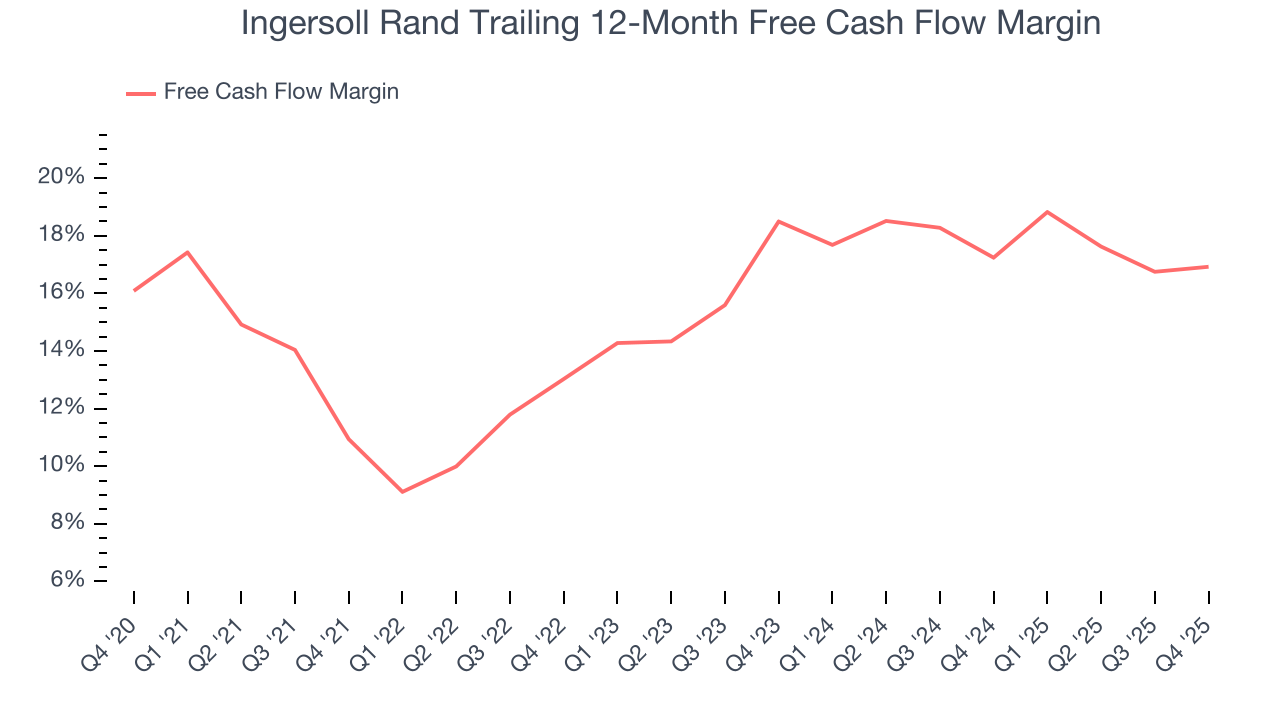

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Ingersoll Rand has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 15.7% over the last five years.

Taking a step back, we can see that Ingersoll Rand’s margin expanded by 6 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Ingersoll Rand’s free cash flow clocked in at $536.5 million in Q4, equivalent to a 25.7% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

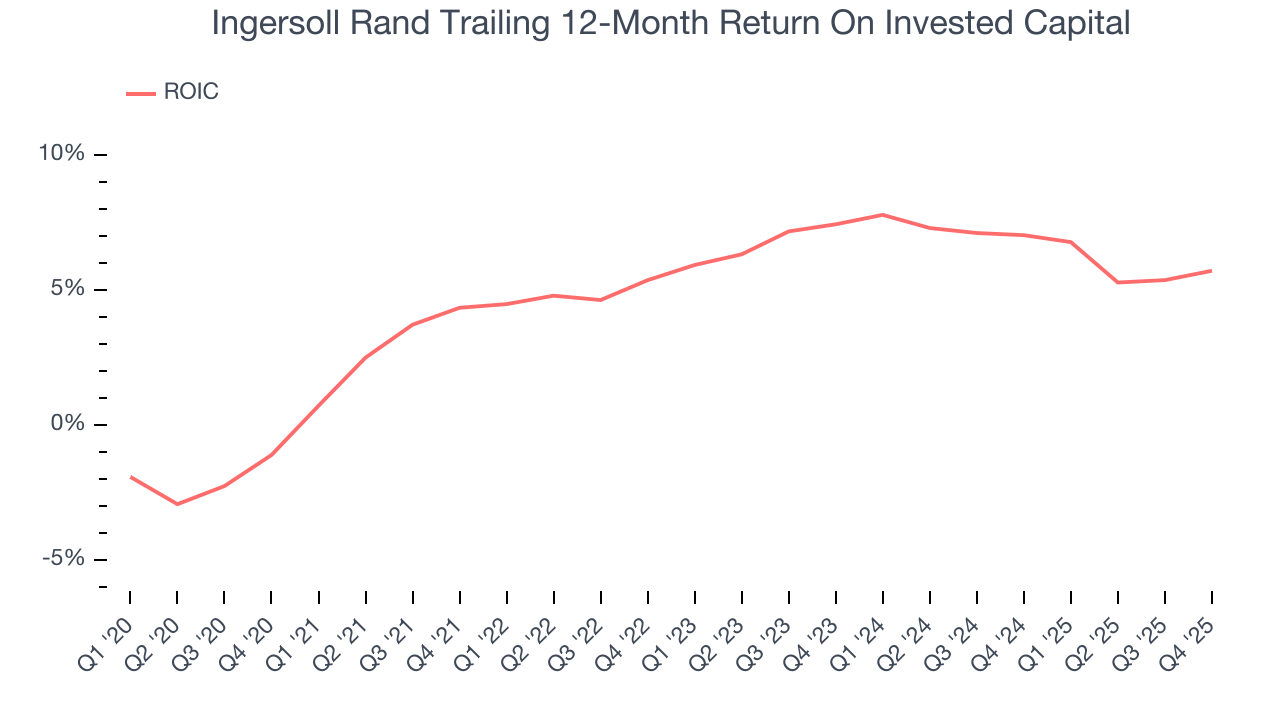

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Ingersoll Rand historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Ingersoll Rand’s ROIC increased by 1.5 percentage points annually each year over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

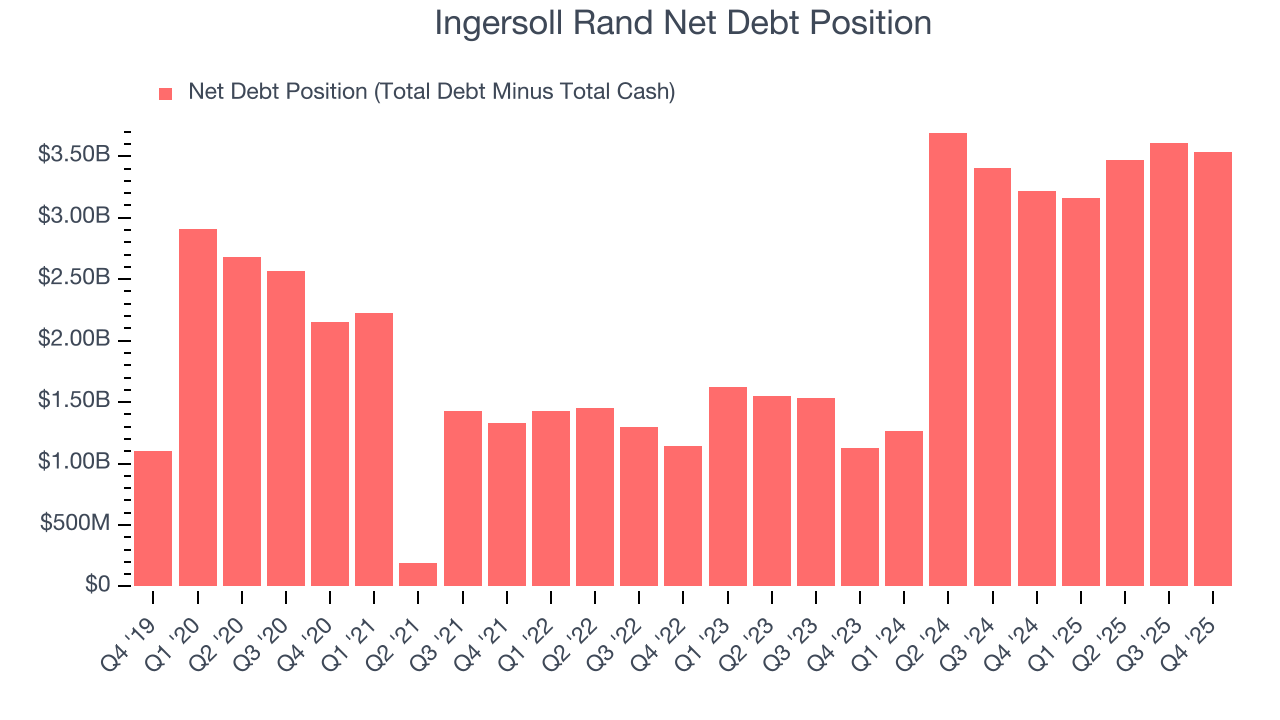

11. Balance Sheet Assessment

Ingersoll Rand reported $1.25 billion of cash and $4.78 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $2.09 billion of EBITDA over the last 12 months, we view Ingersoll Rand’s 1.7× net-debt-to-EBITDA ratio as safe. We also see its $109.9 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Ingersoll Rand’s Q4 Results

We enjoyed seeing Ingersoll Rand beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance slightly missed. Overall, this print had some key positives. The stock traded up 3.1% to $97.30 immediately following the results.

13. Is Now The Time To Buy Ingersoll Rand?

Updated: February 19, 2026 at 9:14 PM EST

Are you wondering whether to buy Ingersoll Rand or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Ingersoll Rand isn’t a bad business, but we’re not clamoring to buy it here and now. Although its revenue growth was mediocre over the last five years and analysts expect growth to slow over the next 12 months, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. We advise investors to be cautious with this one, however, as its organic revenue declined.

Ingersoll Rand’s P/E ratio based on the next 12 months is 27.4x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $100.64 on the company (compared to the current share price of $96.73).