Jefferies (JEF)

We wouldn’t recommend Jefferies. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Jefferies Will Underperform

Tracing its roots back to 1962 and rebranded from Leucadia National Corporation in 2018, Jefferies Financial Group (NYSE:JEF) is a global investment banking and capital markets firm that provides advisory services, securities trading, and asset management to corporations, institutions, and wealthy individuals.

- Earnings per share fell by 7.2% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Loan losses and capital returns have eroded its tangible book value per share this cycle as its tangible book value per share declined by 3% annually over the last two years

- High net-debt-to-EBITDA ratio of 16× increases the risk of forced asset sales or dilutive financing if operational performance weakens

Jefferies falls short of our expectations. There are more promising prospects in the market.

Why There Are Better Opportunities Than Jefferies

At $39.90 per share, Jefferies trades at 0.8x forward P/E. This multiple expensive for its subpar fundamentals.

We’d rather invest in companies with elite fundamentals than questionable ones with open questions and big downside risks. The durable earnings power of high-quality businesses helps us sleep well at night.

3. Jefferies (JEF) Research Report: Q1 CY2026 Update

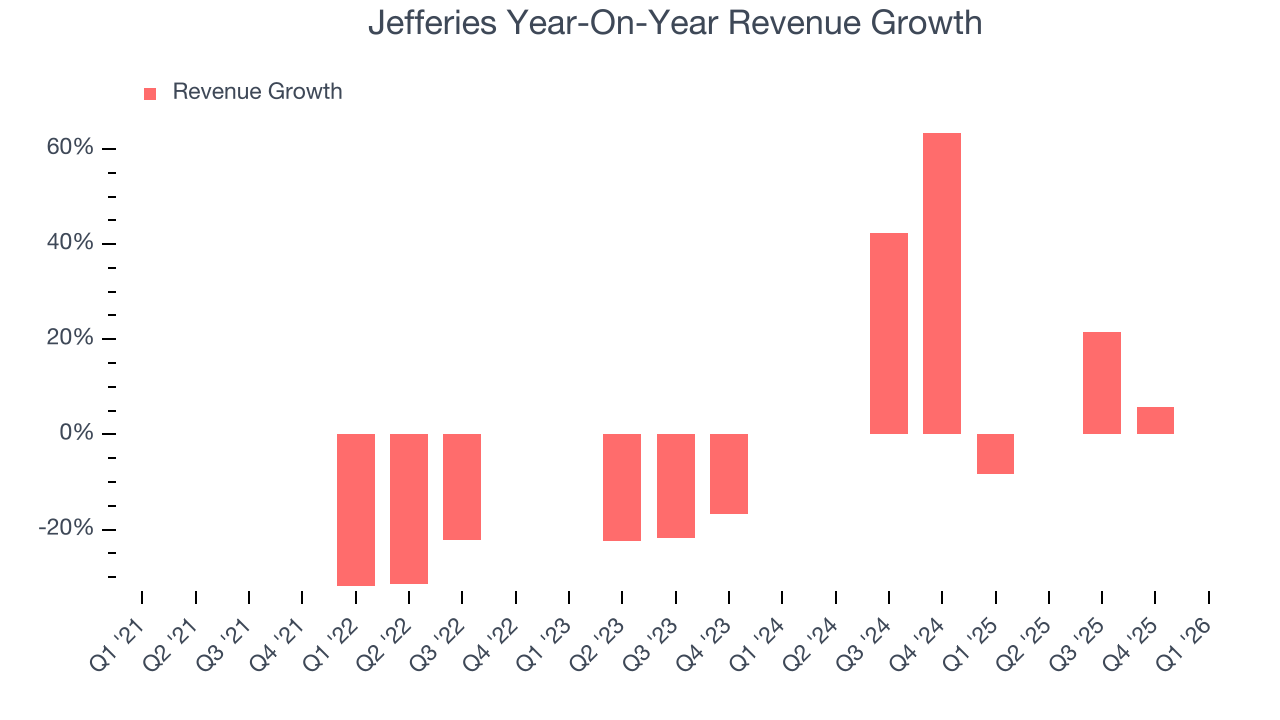

Investment banking firm Jefferies Financial Group (NYSE:JEF) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 26.6% year on year to $2.02 billion. Its GAAP profit of $0.70 per share was 23.3% below analysts’ consensus estimates.

Jefferies (JEF) Q1 CY2026 Highlights:

- Revenue: $2.02 billion vs analyst estimates of $1.99 billion (26.6% year-on-year growth, 1.4% beat)

- Pre-tax Profit: $212.2 million (10.5% margin)

- EPS (GAAP): $0.70 vs analyst expectations of $0.91 (23.3% miss)

- Tangible Book Value per Share: $34.24 vs analyst estimates of $34.53 (15.7% year-on-year decline, 0.8% miss)

- Market Capitalization: $8.38 billion

Company Overview

Tracing its roots back to 1962 and rebranded from Leucadia National Corporation in 2018, Jefferies Financial Group (NYSE:JEF) is a global investment banking and capital markets firm that provides advisory services, securities trading, and asset management to corporations, institutions, and wealthy individuals.

Jefferies operates through two main segments: Investment Banking and Capital Markets, and Asset Management. The Investment Banking division offers a comprehensive suite of services including mergers and acquisitions advice, debt restructuring, and both equity and debt underwriting. For example, when a mid-sized technology company wants to go public, Jefferies might guide them through the IPO process, helping determine pricing and connecting them with institutional investors.

The firm's Capital Markets business spans equities and fixed income, where Jefferies acts as both agent and market maker, executing trades for clients while providing research and market insights. Its fixed income division trades everything from government bonds to high-yield debt and structured products, with Jefferies serving as a Primary Dealer for U.S. government securities.

Through strategic joint ventures, the company has expanded its capabilities. Jefferies Finance, a 50/50 partnership with Massachusetts Mutual Life Insurance, focuses on leveraged finance and loan management, while Berkadia, a joint venture with Berkshire Hathaway, specializes in commercial real estate financing and investment sales.

The Asset Management segment operates primarily under the Leucadia Asset Management umbrella, offering institutional clients access to various investment strategies across different asset classes. The firm often invests its own capital alongside clients in these strategies. Jefferies maintains a strategic alliance with Sumitomo Mitsui Financial Group, enhancing its global reach, particularly in Japanese markets where SMBC owned approximately 15.8% of Jefferies' common stock as of late 2024.

4. Investment Banking & Brokerage

Investment banks and brokerages facilitate capital raises, mergers and acquisitions, and securities trading. The sector benefits from corporate activity during economic expansion, increased retail trading participation, and advisory opportunities in emerging sectors. Headwinds include economic cycle vulnerability affecting deal flow, compressed trading commissions due to electronic platforms, and regulatory capital requirements constraining certain higher-risk activities.

Jefferies Financial Group competes with major global investment banks including Goldman Sachs (NYSE:GS), Morgan Stanley (NYSE:MS), JPMorgan Chase (NYSE:JPM), and Bank of America's Merrill Lynch (NYSE:BAC), as well as boutique investment banks like Evercore (NYSE:EVR) and Lazard (NYSE:LAZ).

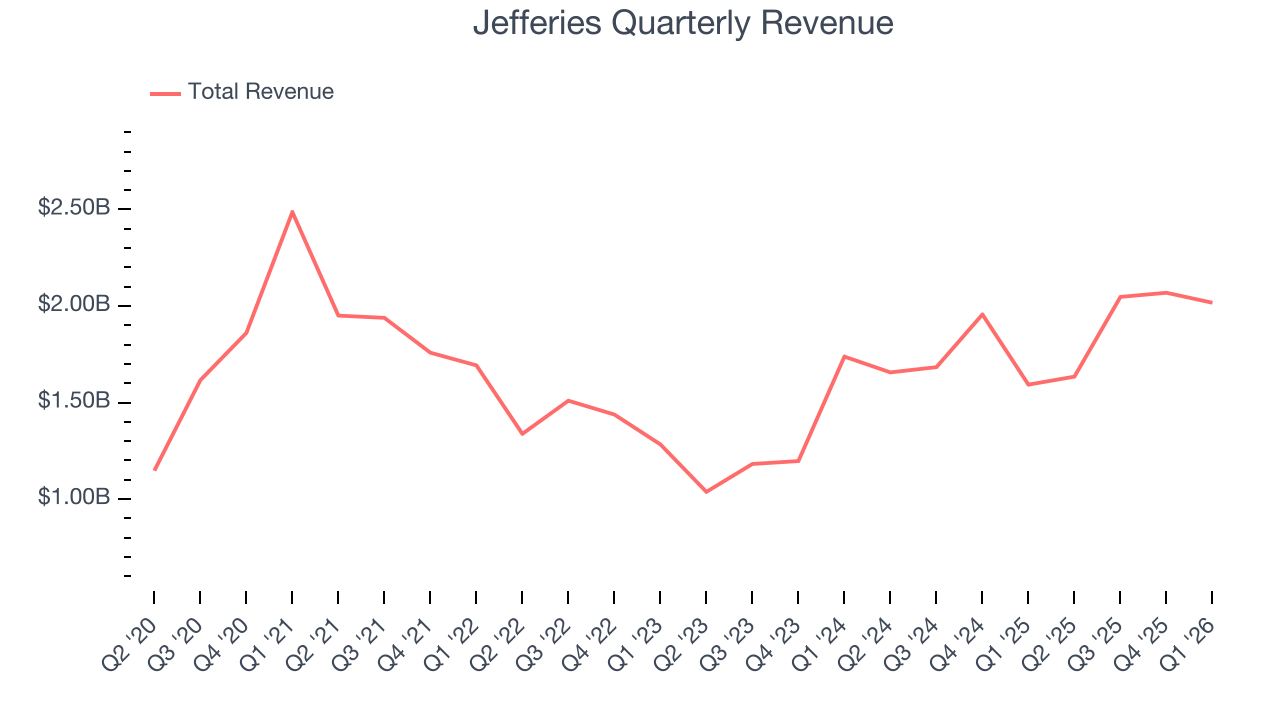

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Jefferies grew its revenue at a sluggish 1.8% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Jefferies’s annualized revenue growth of 22.8% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Jefferies reported robust year-on-year revenue growth of 26.6%, and its $2.02 billion of revenue topped Wall Street estimates by 1.4%.

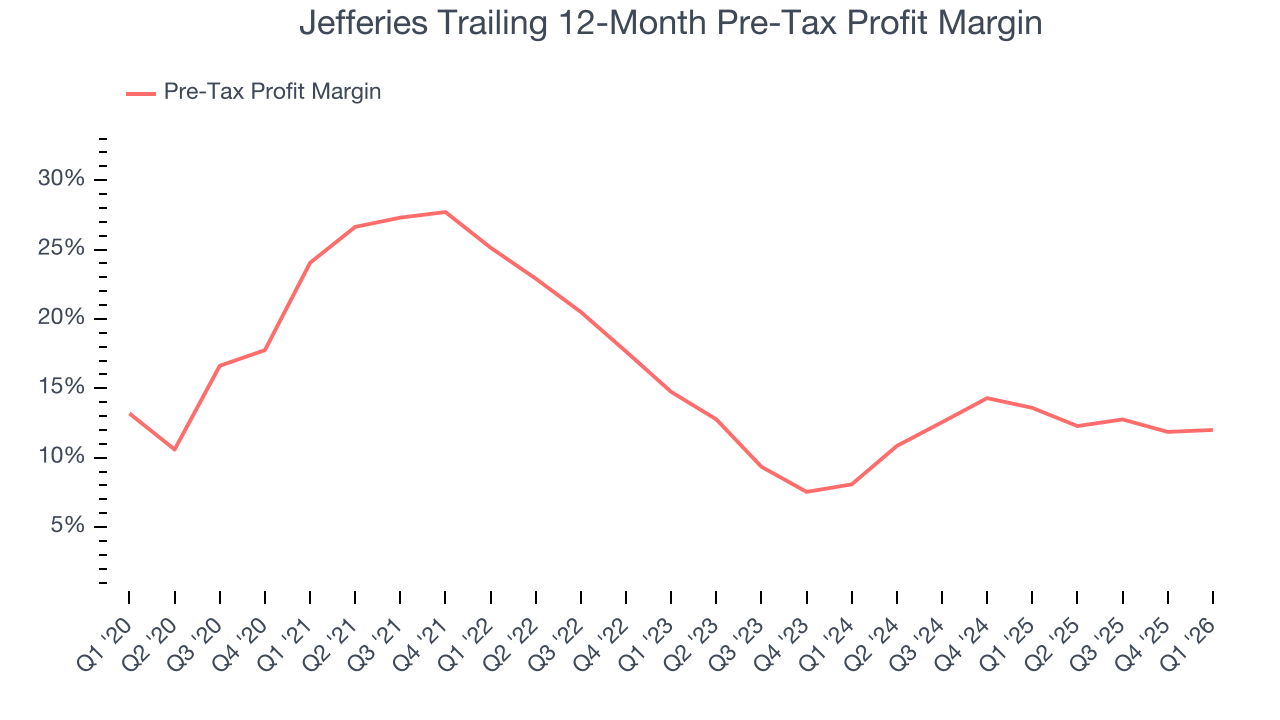

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Investment Banking & Brokerage companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last five years, Jefferies’s pre-tax profit margin has risen by 12 percentage points, going from 25.1% to 12%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 3.9 percentage points on a two-year basis.

Jefferies’s pre-tax profit margin came in at 10.5% this quarter. This result was 1 percentage points better than the same quarter last year.

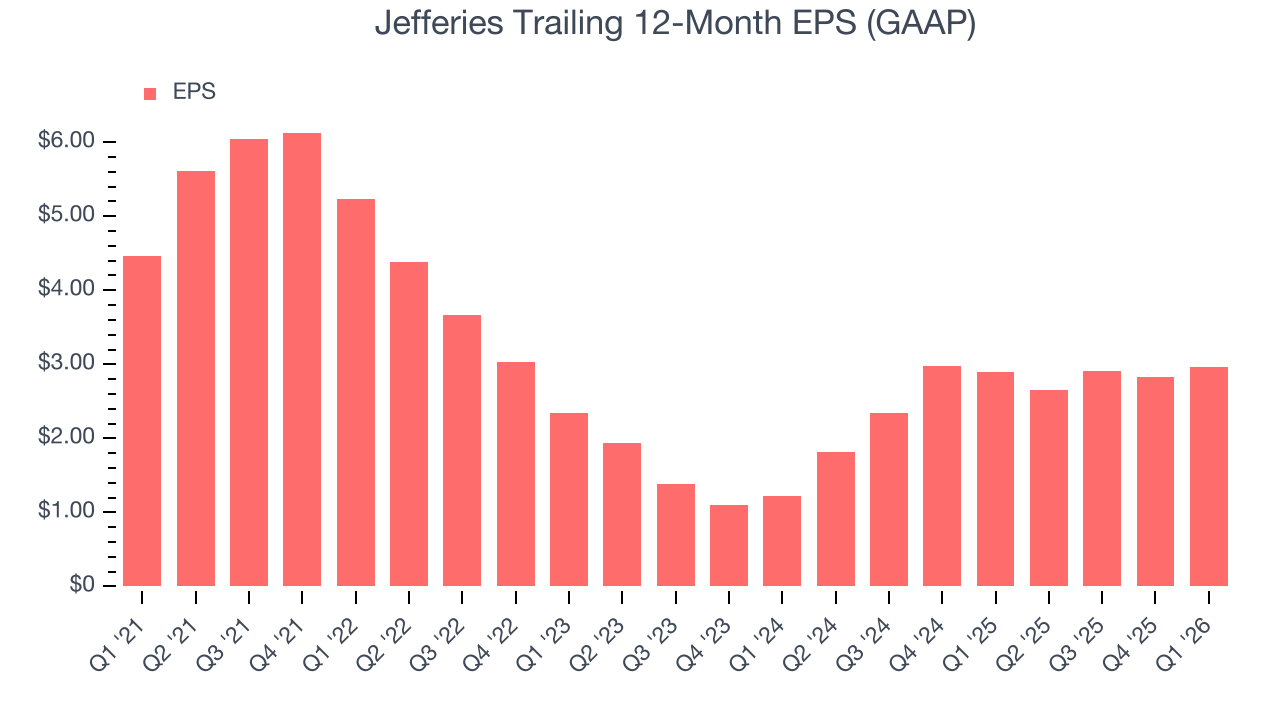

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Jefferies, its EPS declined by 7.9% annually over the last five years while its revenue grew by 1.8%. This tells us the company became less profitable on a per-share basis as it expanded due to factors such as interest expenses and taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Jefferies, its two-year annual EPS growth of 55.8% was higher than its five-year trend. This acceleration made it one of the faster-growing financials companies in recent history.

In Q1, Jefferies reported EPS of $0.70, up from $0.57 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Jefferies’s full-year EPS of $2.96 to grow 45.5%.

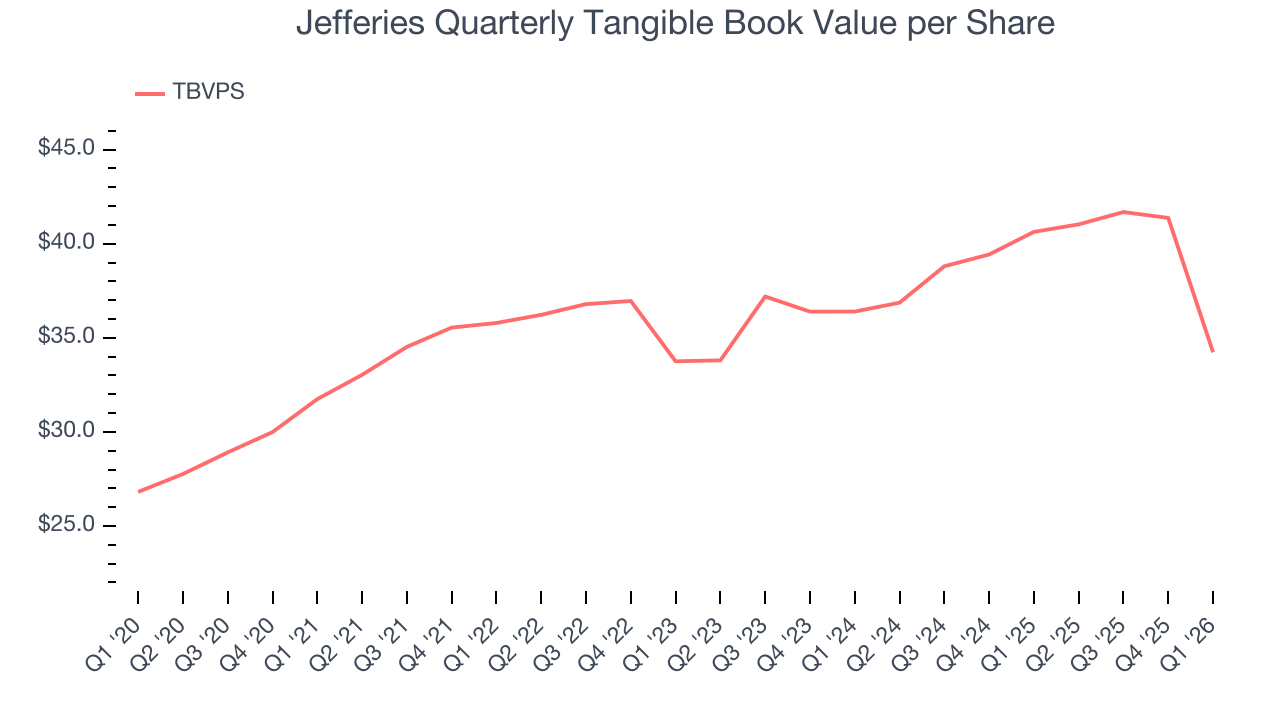

8. Tangible Book Value Per Share (TBVPS)

Diversified financial companies operate across multiple business segments, from investment banking and trading to wealth management and specialized lending. Their valuations hinge on balance sheet quality and the ability to compound shareholder equity across these diverse operations.

This explains why tangible book value per share (TBVPS) is a premier metric for the sector. TBVPS provides concrete per-share net worth that investors can trust when evaluating companies with complex, multi-faceted business models. Traditional metrics like EPS are helpful but face distortion from the complexity of diversified operations, M&A activity, and various accounting rules that can obscure true performance across multiple business lines.

Jefferies’s TBVPS grew at a sluggish 1.5% annual clip over the last five years. On a two-year basis, however, dynamics have changed as TBVPS dropped by 3% annually ($36.40 to $34.24 per share).

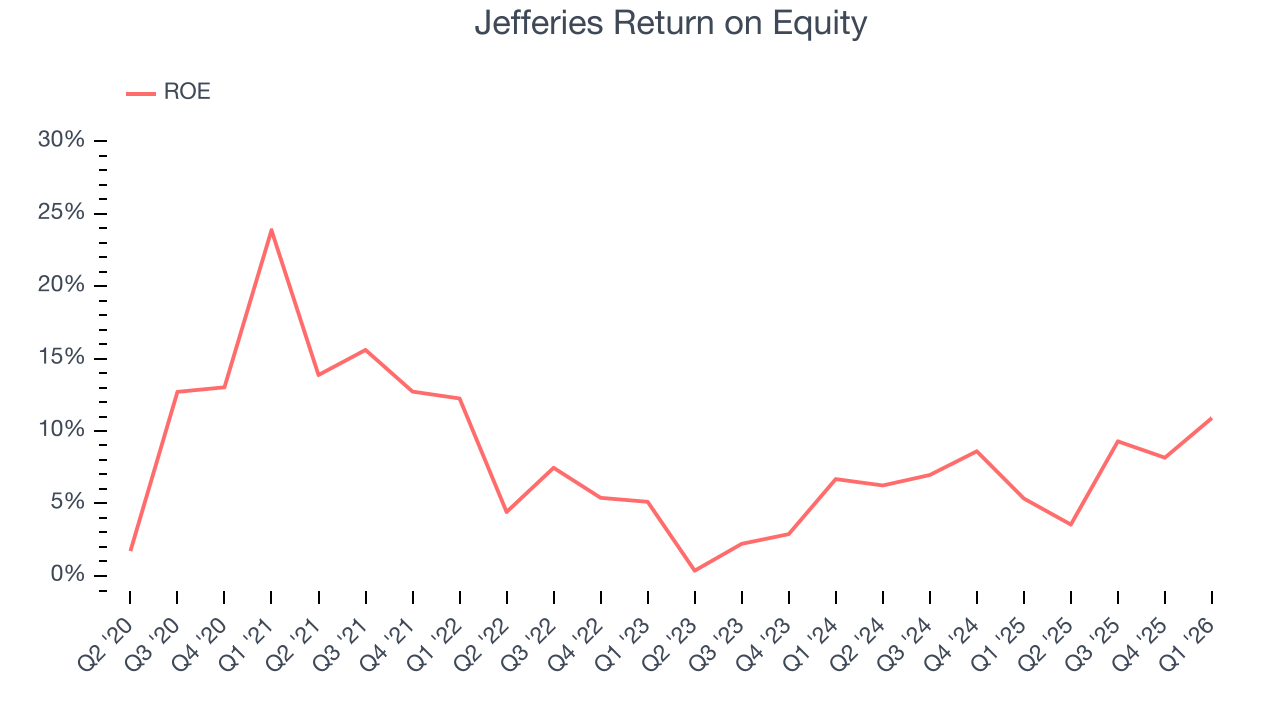

9. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Jefferies has averaged an ROE of 7.4%, uninspiring for a company operating in a sector where the average shakes out around 10%.

10. Balance Sheet Risk

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Jefferies has no debt, so leverage is not an issue here.

11. Key Takeaways from Jefferies’s Q1 Results

It was good to see Jefferies narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this quarter could have been better. The stock traded down 2% to $39.21 immediately following the results.

12. Is Now The Time To Buy Jefferies?

Updated: March 26, 2026 at 12:30 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Jefferies.

Jefferies falls short of our quality standards. To begin with, its revenue growth was weak over the last five years. On top of that, Jefferies’s declining pre-tax profit margin shows the business has become less efficient, and its declining EPS over the last five years makes it a less attractive asset to the public markets.

Jefferies’s P/E ratio based on the next 12 months is 0.8x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $55 on the company (compared to the current share price of $39.90).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.