Lucky Strike (LUCK)

Lucky Strike keeps us up at night. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lucky Strike Will Underperform

Born from the transformation of traditional bowling alleys into modern entertainment destinations, Lucky Strike (NYSE:LUCK) operates bowling alleys and other entertainment venues with upscale amenities, arcade games, and food and beverage services across North America.

- 6.8% annual revenue growth over the last two years was slower than its consumer discretionary peers

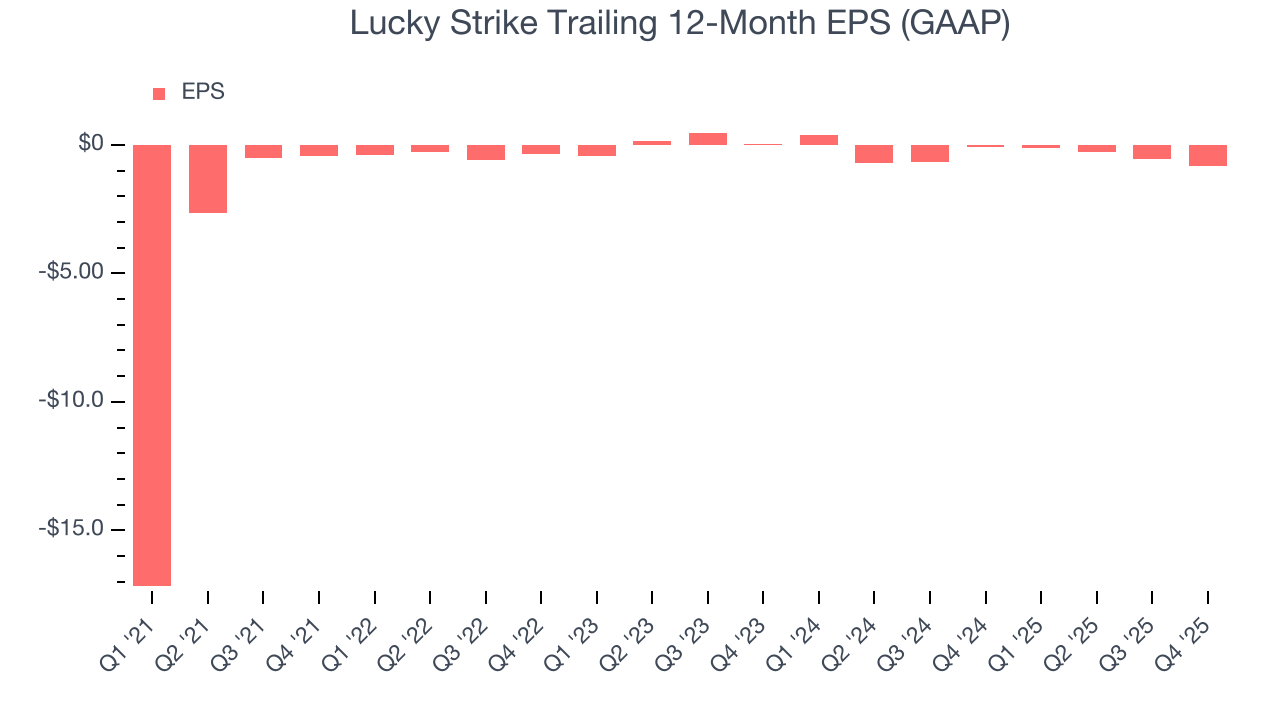

- Earnings per share have dipped by 21.7% annually over the past four years, which is concerning because stock prices follow EPS over the long term

- 7× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Lucky Strike’s quality doesn’t meet our expectations. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Lucky Strike

At $7.91 per share, Lucky Strike trades at 37.5x forward P/E. This multiple is higher than that of consumer discretionary peers; it’s also rich for the business quality. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Lucky Strike (LUCK) Research Report: Q4 CY2025 Update

Entertainment venue operator Lucky Strike (NYSE:LUCK) fell short of the market’s revenue expectations in Q4 CY2025 as sales rose 2.3% year on year to $306.9 million. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $1.29 billion at the midpoint. Its GAAP loss of $0.11 per share was significantly below analysts’ consensus estimates.

Lucky Strike (LUCK) Q4 CY2025 Highlights:

- Revenue: $306.9 million vs analyst estimates of $313.2 million (2.3% year-on-year growth, 2% miss)

- EPS (GAAP): -$0.11 vs analyst estimates of $0.01 (significant miss)

- Adjusted EBITDA: $77.47 million vs analyst estimates of $98.35 million (25.2% margin, 21.2% miss)

- The company reconfirmed its revenue guidance for the full year of $1.29 billion at the midpoint

- EBITDA guidance for the full year is $395 million at the midpoint, above analyst estimates of $386.7 million

- Operating Margin: 10.9%, down from 15.6% in the same quarter last year

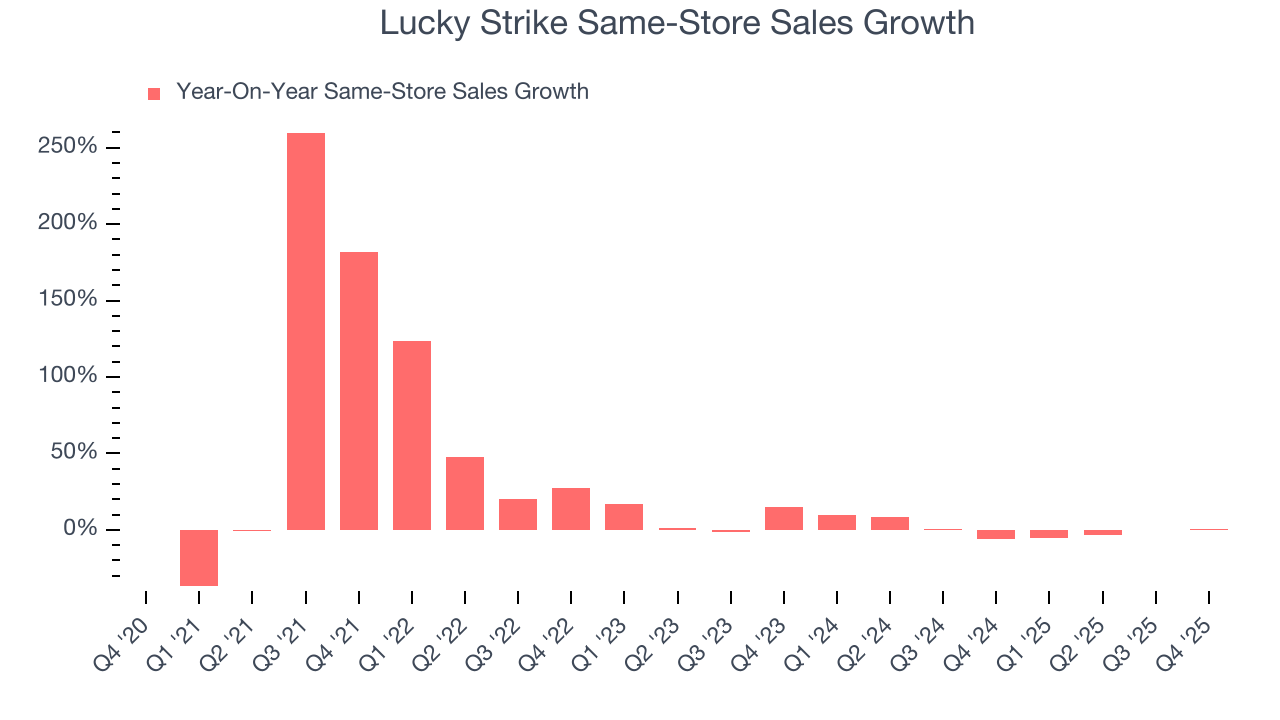

- Same-Store Sales were flat year on year (-6.2% in the same quarter last year)

- Market Capitalization: $1.01 billion

Company Overview

Born from the transformation of traditional bowling alleys into modern entertainment destinations, Lucky Strike (NYSE:LUCK) operates bowling alleys and other entertainment venues with upscale amenities, arcade games, and food and beverage services across North America.

Lucky Strike Entertainment's venues operate under several brand names, with its flagship Bowlero and Lucky Strike locations featuring premium offerings that elevate the bowling experience beyond the traditional alley concept. These upscale venues include lounge-style seating, expanded dining options, and enhanced customer service designed to appeal to both casual visitors and organized groups. A typical customer might reserve a lane for a corporate team-building event, enjoying craft cocktails and gourmet appetizers while bowling in a stylish, modern environment.

The company generates revenue through multiple streams: lane rentals, food and beverage sales, arcade game play, and event hosting services. Beyond bowling, Lucky Strike has diversified into other entertainment concepts, including Octane Raceway for go-kart enthusiasts and the Raging Waves water park, broadening its appeal across different entertainment preferences.

Acquisition forms a cornerstone of Lucky Strike's growth strategy, with the company actively purchasing existing venues and transforming them according to its premium entertainment model. This approach allows for rapid expansion while leveraging established locations in desirable markets. The company serves approximately 30 million customers annually across its North American footprint, which includes venues in the United States, Canada, and Mexico.

Lucky Strike also differentiates itself through technology integration, developing gaming applications and in-venue digital experiences that extend customer engagement beyond the physical visit. The company hosts both professional and amateur bowling tournaments, further cementing its position in the bowling community while creating additional revenue opportunities through event management and broadcasting.

4. Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Lucky Strike Entertainment competes with other entertainment venue operators like Dave & Buster's (NASDAQ:PLAY), Main Event Entertainment (owned by Dave & Buster's), Round One Entertainment, and regional family entertainment centers that combine dining, games, and activities.

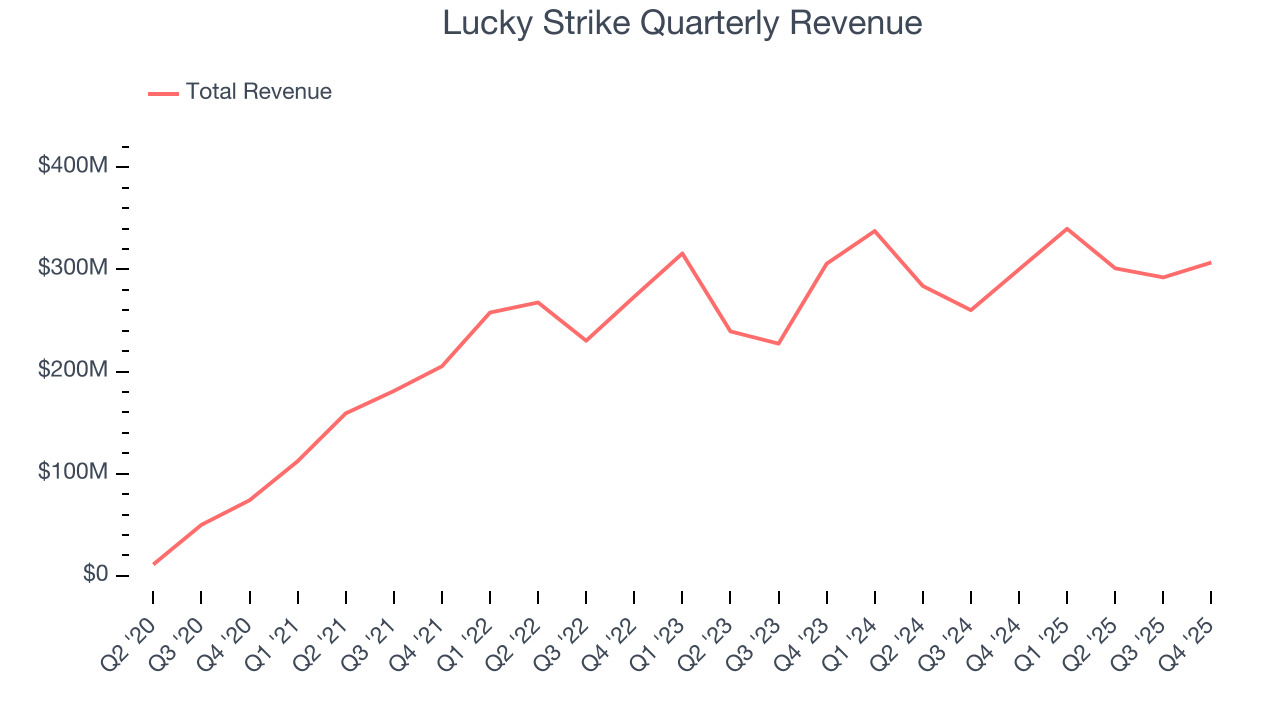

5. Revenue Growth

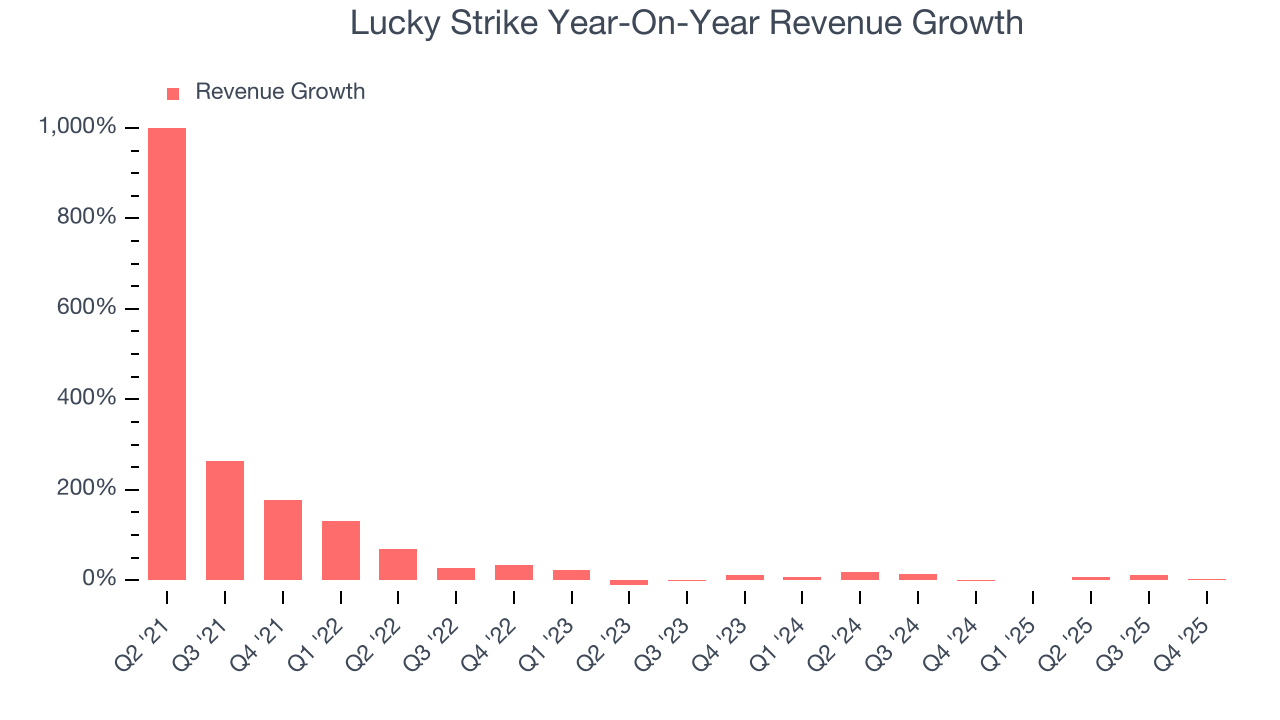

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Lucky Strike grew its sales at a solid 46.1% compounded annual growth rate. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Lucky Strike’s recent performance shows its demand has slowed as its annualized revenue growth of 6.8% over the last two years was below its five-year trend. Note that COVID hurt Lucky Strike’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can better understand the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Lucky Strike’s same-store sales were flat. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Lucky Strike’s revenue grew by 2.3% year on year to $306.9 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.2% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not lead to better top-line performance yet.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

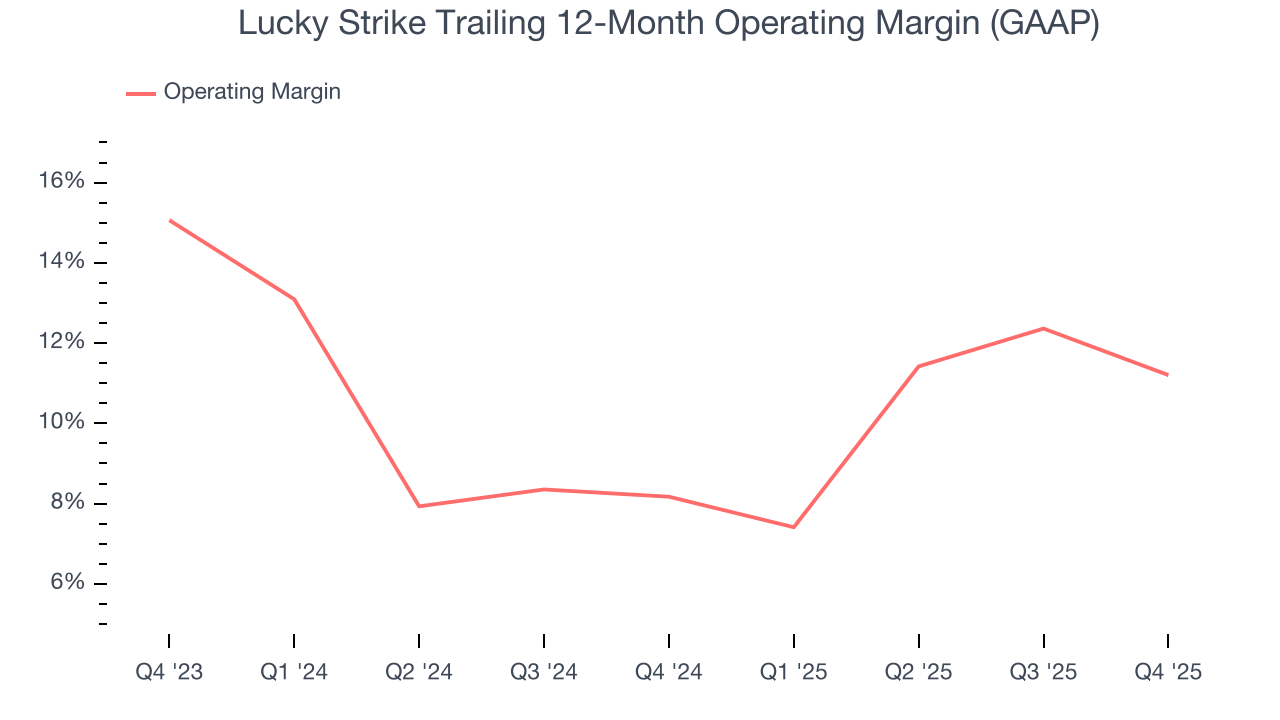

Lucky Strike’s operating margin has been trending up over the last 12 months and averaged 9.7% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, Lucky Strike generated an operating margin profit margin of 10.9%, down 4.8 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Lucky Strike’s full-year earnings are still negative, it reduced its losses and improved its EPS by 44.8% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, Lucky Strike reported EPS of negative $0.11, down from $0.16 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Lucky Strike’s full-year EPS of negative $0.80 will flip to positive $0.17.

8. Cash Is King

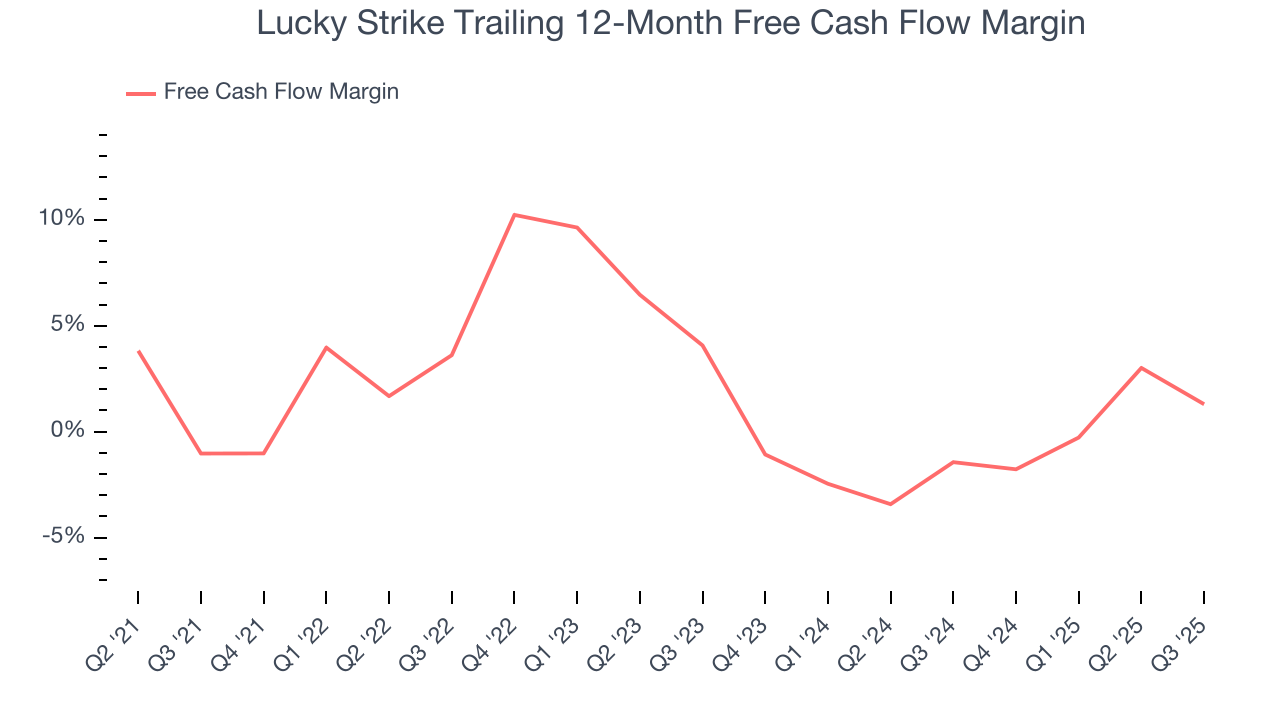

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Lucky Strike broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Lucky Strike historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 13.1%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Lucky Strike’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Lucky Strike’s $2.80 billion of debt exceeds the $95.91 million of cash on its balance sheet. Furthermore, its 8× net-debt-to-EBITDA ratio (based on its EBITDA of $356.1 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Lucky Strike could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Lucky Strike can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Lucky Strike’s Q4 Results

It was encouraging to see Lucky Strike’s full-year EBITDA guidance beat analysts’ expectations. On the other hand, its EPS missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.9% to $6.98 immediately after reporting.

12. Is Now The Time To Buy Lucky Strike?

Updated: March 29, 2026 at 10:51 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We see the value of companies helping consumers, but in the case of Lucky Strike, we’re out. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its same-store sales performance has disappointed. And while the company’s projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last four years makes it a less attractive asset to the public markets.

Lucky Strike’s P/E ratio based on the next 12 months is 37.5x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $11.11 on the company (compared to the current share price of $7.91).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.