Lumen (LUMN)

Lumen is up against the odds. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lumen Will Underperform

With approximately 350,000 route miles of fiber optic cable spanning North America and the Asia Pacific, Lumen Technologies (NYSE:LUMN) operates a vast fiber optic network that provides communications, cloud connectivity, security, and IT solutions to businesses and consumers.

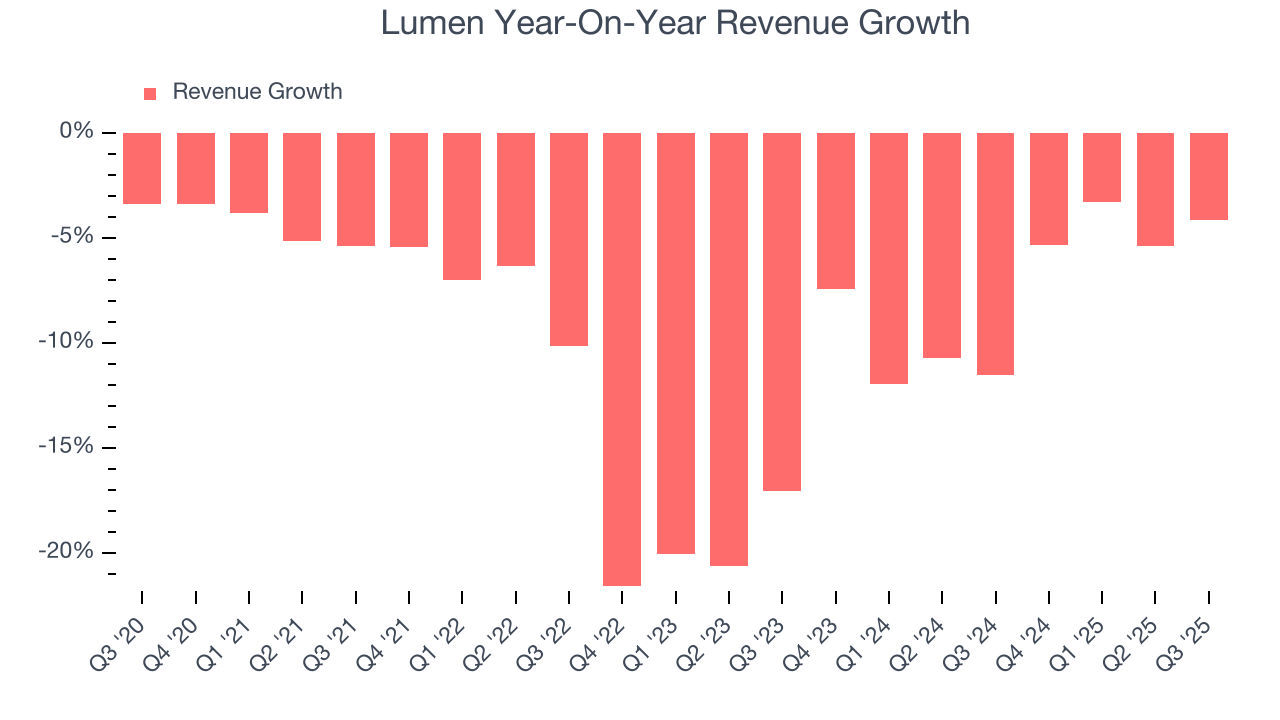

- Sales tumbled by 9.5% annually over the last five years, showing market trends are working against its favor during this cycle

- Sales were less profitable over the last five years as its earnings per share fell by 16.8% annually, worse than its revenue declines

- Forecasted revenue decline of 7.7% for the upcoming 12 months implies demand will fall even further

Lumen is in the penalty box. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Lumen

Lumen’s stock price of $8.60 implies a valuation ratio of 7.4x forward EV-to-EBITDA. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Lumen (LUMN) Research Report: Q3 CY2025 Update

Telecommunications infrastructure company Lumen Technologies (NYSE:LUMN) beat Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 4.2% year on year to $3.09 billion. Its non-GAAP loss of $0.20 per share was 25% above analysts’ consensus estimates.

Lumen (LUMN) Q3 CY2025 Highlights:

- Revenue: $3.09 billion vs analyst estimates of $3.06 billion (4.2% year-on-year decline, 0.9% beat)

- Adjusted EPS: -$0.20 vs analyst estimates of -$0.27 (25% beat)

- Adjusted EBITDA: $216 million vs analyst estimates of $761.7 million (7% margin, 71.6% miss)

- EBITDA guidance for the full year is $3.3 billion at the midpoint, below analyst estimates of $3.37 billion

- Operating Margin: -3.8%, down from 3.9% in the same quarter last year

- Free Cash Flow Margin: 47.6%, up from 37.2% in the same quarter last year

- Market Capitalization: $11.29 billion

Company Overview

With approximately 350,000 route miles of fiber optic cable spanning North America and the Asia Pacific, Lumen Technologies (NYSE:LUMN) operates a vast fiber optic network that provides communications, cloud connectivity, security, and IT solutions to businesses and consumers.

Lumen's network infrastructure serves as the backbone for its diverse portfolio of services. The company connects approximately 170,000 buildings directly to its fiber network, enabling high-speed, secure data transmission for enterprise customers. For residential and small business customers, Lumen offers internet connectivity through both fiber (branded as Quantum Fiber) and copper-based networks (under the CenturyLink brand).

Beyond basic connectivity, Lumen provides a comprehensive suite of technology solutions. Its edge computing services allow businesses to process data closer to where it's created, reducing latency for time-sensitive applications. A manufacturing company might use Lumen's edge computing to analyze production line data in real-time, enabling immediate adjustments to prevent defects. The company also offers cybersecurity services, helping organizations protect against increasingly sophisticated threats.

Lumen generates revenue through subscription-based service models, with pricing typically based on bandwidth, service level agreements, and additional features. Enterprise customers range from small businesses to global corporations requiring complex network solutions, while mass market customers include millions of residential internet subscribers.

The company organizes its business into strategic categories: "Grow" (emerging services like edge cloud and security), "Nurture" (established services like ethernet), and "Harvest" (legacy offerings like traditional voice). This approach allows Lumen to balance investment in future growth areas while maximizing returns from mature technologies.

Lumen faces ongoing challenges in transitioning from legacy copper networks to fiber infrastructure, particularly in rural areas where deployment costs are higher. The company must also navigate a complex regulatory environment, as telecommunications services are subject to oversight by the Federal Communications Commission and state regulatory commissions.

4. Terrestrial Telecommunication Services

Terrestrial telecommunication companies face an uphill battle, as they mostly sell into a deflationary market, where the price of moving a bit tends to decrease over time with better technology. Without dependable volume growth, revenue growth could be challenged. Unfortunately, broadband penetration in their core US market is quite high already. On the other hand, data consumption from streaming entertainment and 5G expansion could provide a floor on growth for the next number of years. As if that wasn't enough to worry about, competition is intense, with larger telecom providers and hyperscalers expanding their own networks.

Lumen Technologies competes with major telecommunications providers including AT&T (NYSE:T), Verizon (NYSE:VZ), and Comcast (NASDAQ:CMCSA), as well as fiber infrastructure specialists like Crown Castle (NYSE:CCI) and specialized enterprise service providers such as Zayo Group (private).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

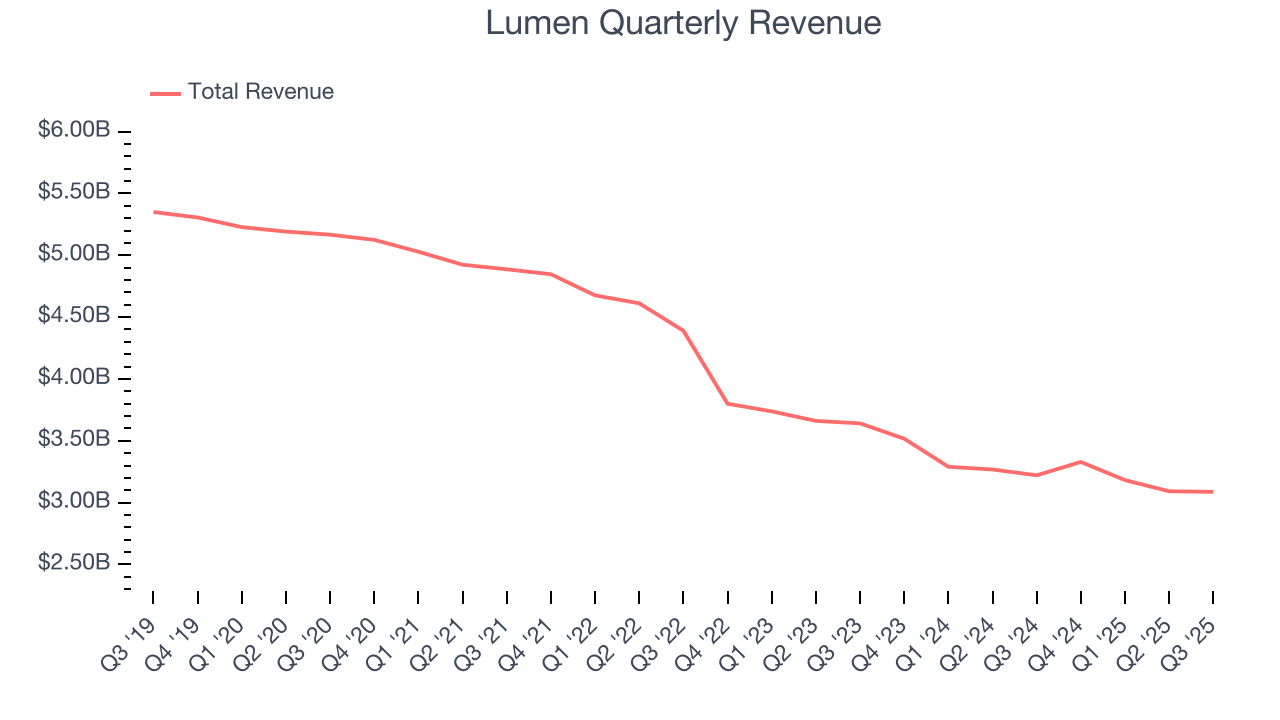

With $12.69 billion in revenue over the past 12 months, Lumen is larger than most business services companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To expand meaningfully, Lumen likely needs to tweak its prices, innovate with new offerings, or enter new markets.

As you can see below, Lumen’s revenue declined by 9.5% per year over the last five years, a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Lumen’s annualized revenue declines of 7.5% over the last two years suggest its demand continued shrinking.

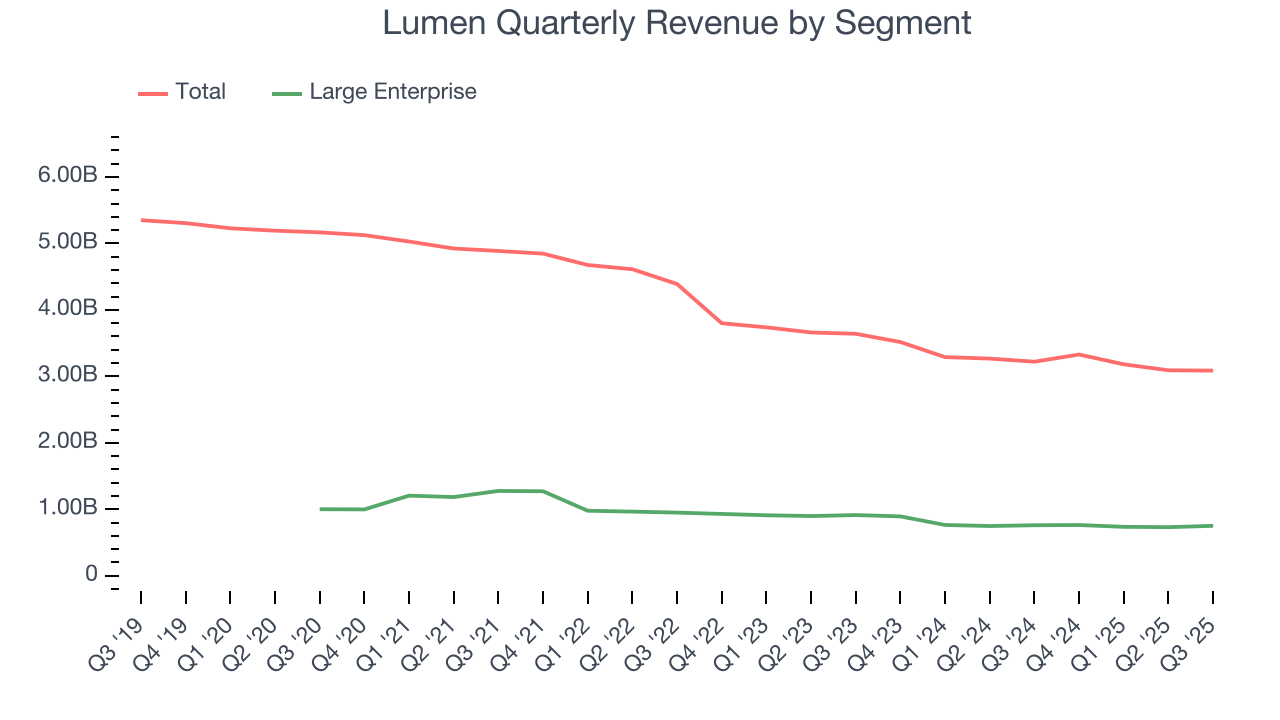

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Large Enterprise. Over the last two years, Lumen’s Large Enterprise revenue (services provided to businesses) averaged 9.4% year-on-year declines. This segment has lagged the company’s overall sales.

This quarter, Lumen’s revenue fell by 4.2% year on year to $3.09 billion but beat Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to decline by 7% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

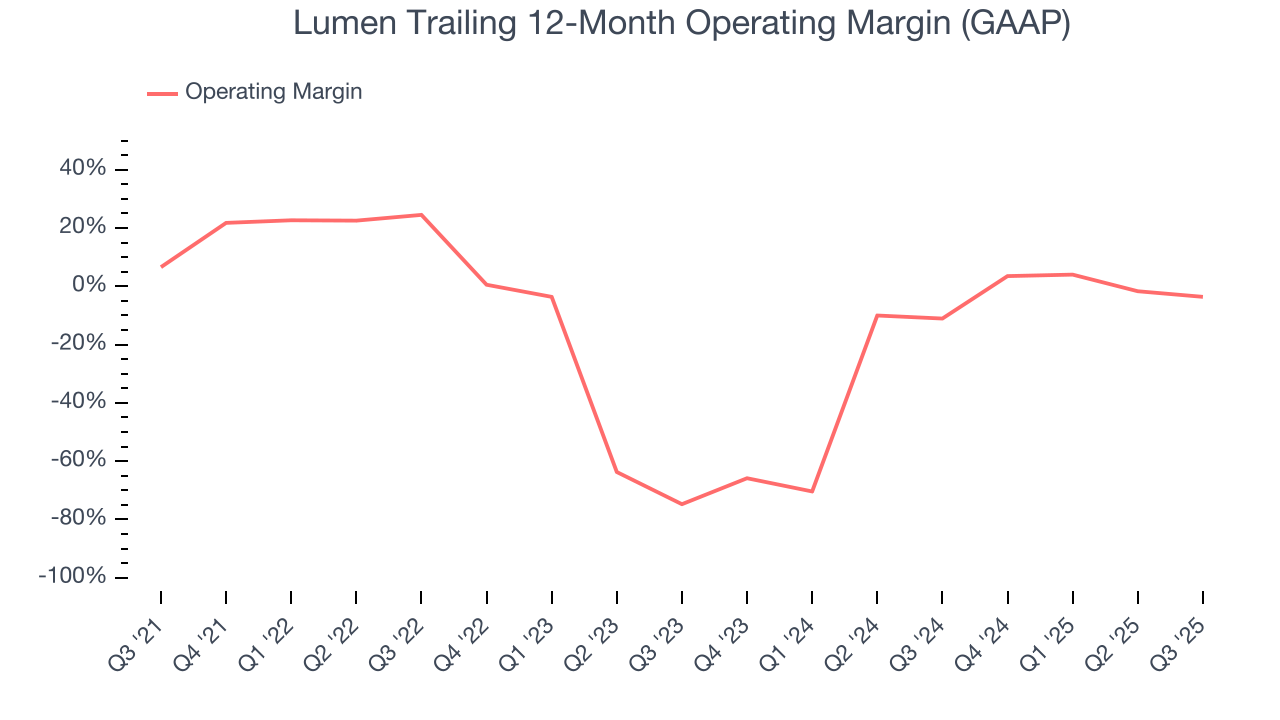

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Lumen’s high expenses have contributed to an average operating margin of negative 9% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Lumen’s operating margin decreased by 10.2 percentage points over the last five years. Lumen’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Lumen generated a negative 3.8% operating margin. The company's consistent lack of profits raise a flag.

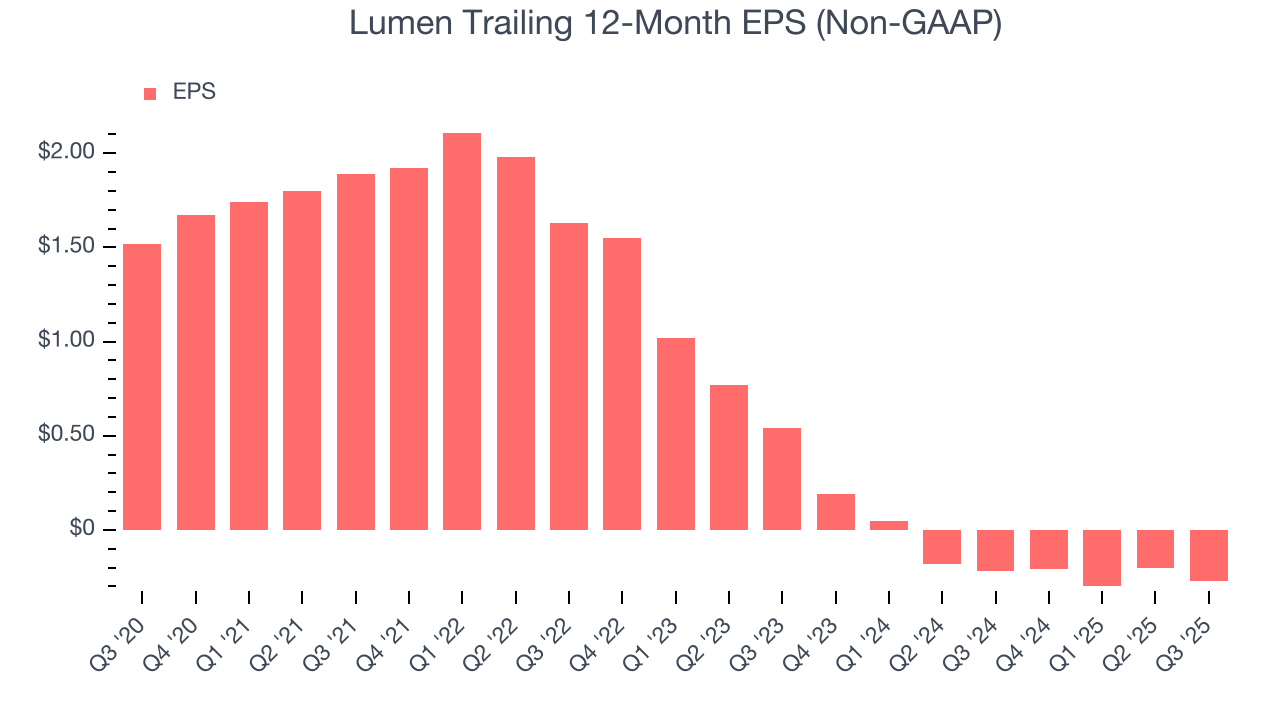

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Lumen, its EPS declined by 16.8% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

We can take a deeper look into Lumen’s earnings to better understand the drivers of its performance. As we mentioned earlier, Lumen’s operating margin declined by 10.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Lumen, its two-year annual EPS declines of 58.1% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Lumen reported adjusted EPS of negative $0.20, down from negative $0.13 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Lumen to perform poorly. Analysts forecast its full-year EPS of negative $0.27 will tumble to negative $0.87.

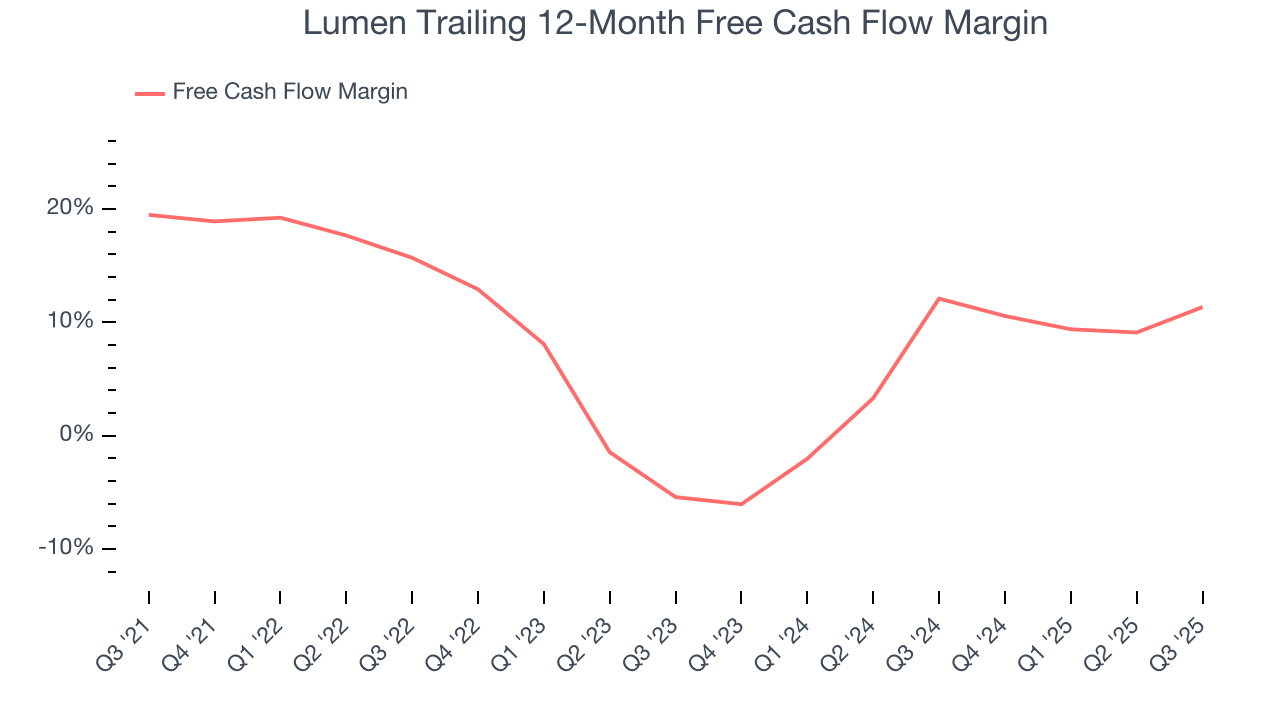

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Lumen has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.4% over the last five years, quite impressive for a business services business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Lumen’s margin dropped by 8.1 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Lumen’s free cash flow clocked in at $1.47 billion in Q3, equivalent to a 47.6% margin. This result was good as its margin was 10.4 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Lumen’s five-year average ROIC was negative 9.9%, meaning management lost money while trying to expand the business. Its returns were among the worst in the business services sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Lumen’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

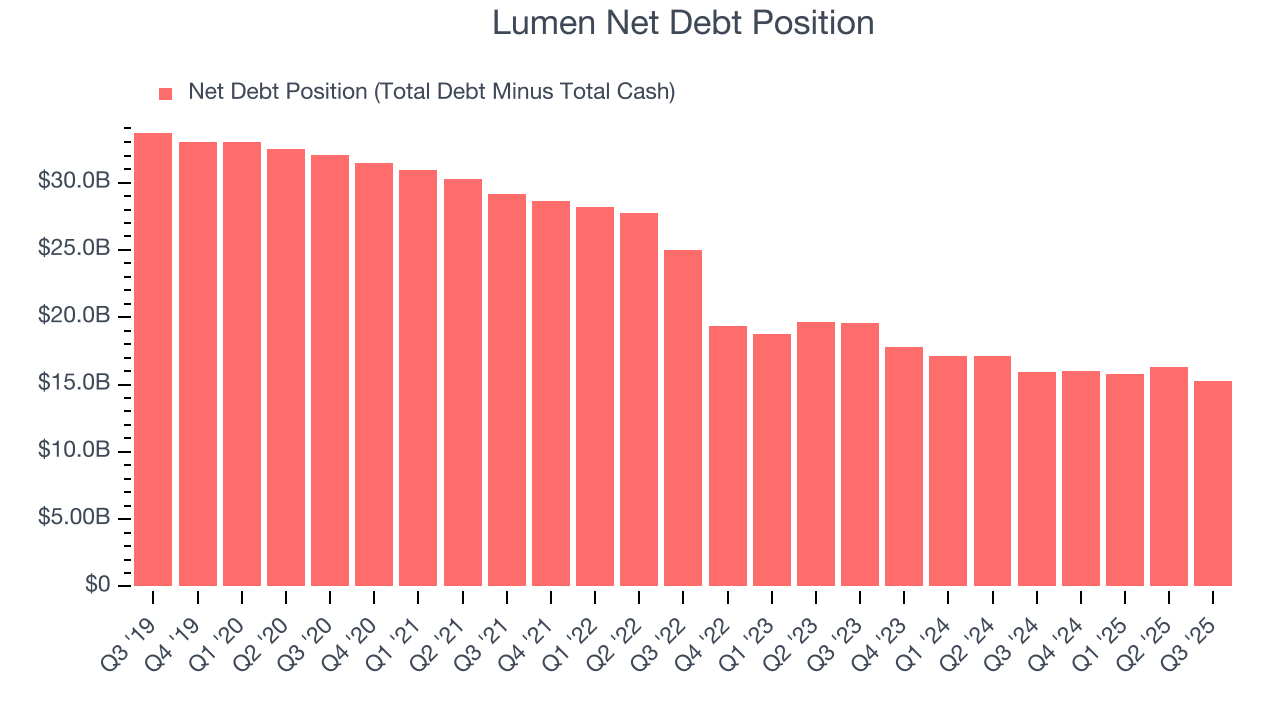

10. Balance Sheet Assessment

Lumen reported $2.40 billion of cash and $17.67 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $3.07 billion of EBITDA over the last 12 months, we view Lumen’s 5.0× net-debt-to-EBITDA ratio as safe. We also see its $1.29 billion of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Lumen’s Q3 Results

It was good to see Lumen beat analysts’ revenue and EPS expectations this quarter. On the other hand, its EBITDA and full-year EBITDA guidance fell short of Wall Street’s estimates. Zooming out, we think this quarter was mixed but featured some positives. The stock traded up 6.1% to $10.97 immediately after reporting.

12. Is Now The Time To Buy Lumen?

Updated: January 24, 2026 at 11:09 PM EST

Before deciding whether to buy Lumen or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Lumen falls short of our quality standards. To begin with, its revenue has declined over the last five years. And while its scale makes it a trusted partner with negotiating leverage, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Lumen’s EV-to-EBITDA ratio based on the next 12 months is 7.4x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $7.78 on the company (compared to the current share price of $8.60), implying they don’t see much short-term potential in Lumen.