Moelis (MC)

We’d invest in Moelis. Its superior revenue growth and returns on capital show it can achieve fast and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why We Like Moelis

Founded in 2007 by veteran banker Ken Moelis during the lead-up to the financial crisis, Moelis & Company (NYSE:MC) is an independent investment bank that provides strategic and financial advisory services to corporations, financial sponsors, governments, and sovereign wealth funds.

- Annual revenue growth of 32.5% over the past two years was outstanding, reflecting market share gains this cycle

- Performance over the past two years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 299% outpaced its revenue gains

- Stellar return on equity showcases management’s ability to surface highly profitable business ventures

We have an affinity for Moelis. This is one of the best financials stocks in our coverage.

Is Now The Time To Buy Moelis?

Moelis’s stock price of $73.71 implies a valuation ratio of 24.8x forward P/E. The lofty multiple means expectations are high for this company over the next six to twelve months.

Are you a fan of the company and believe in the bull case? If so, you can own a smaller position, as high-quality companies tend to outperform the market over a long-term period regardless of entry price.

3. Moelis (MC) Research Report: Q3 CY2025 Update

Investment banking firm Moelis & Company (NYSE:MC) missed Wall Street’s revenue expectations in Q3 CY2025, but sales rose 27.1% year on year to $356.9 million. Its non-GAAP profit of $0.68 per share was 14% above analysts’ consensus estimates.

Moelis (MC) Q3 CY2025 Highlights:

- Revenue: $356.9 million vs analyst estimates of $388.3 million (27.1% year-on-year growth, 8.1% miss)

- Pre-tax Profit: $82.31 million (23.1% margin, 209% year-on-year growth)

- Adjusted EPS: $0.68 vs analyst estimates of $0.60 (14% beat)

- Market Capitalization: $5.29 billion

Company Overview

Founded in 2007 by veteran banker Ken Moelis during the lead-up to the financial crisis, Moelis & Company (NYSE:MC) is an independent investment bank that provides strategic and financial advisory services to corporations, financial sponsors, governments, and sovereign wealth funds.

Moelis specializes in advising clients on their most critical financial decisions, with core services including mergers and acquisitions, recapitalizations, restructurings, and capital markets transactions. The firm operates with a collaborative approach rather than a commission-based structure, emphasizing quality of advice over transaction volume.

The company serves diverse clients ranging from large public multinational corporations to middle-market private companies across major industries including Technology, Healthcare, Energy, Consumer & Retail, Financial Institutions, and Real Estate. With offices in over 20 locations worldwide, Moelis combines local expertise with global capabilities to deliver integrated cross-border advisory services.

For example, when a multinational technology company considers acquiring a competitor, Moelis might evaluate strategic alternatives, assess potential targets, provide valuation analyses, and advise on transaction structure and timing. Similarly, for companies in financial distress, Moelis brings together capital structure specialists with industry experts to develop comprehensive solutions.

Beyond traditional M&A work, Moelis offers specialized services including shareholder defense against activist investors, special committee representation, private funds advisory, and expert witness services for major litigation. The firm generates revenue through advisory fees, which typically increase with the complexity and size of transactions.

Moelis differentiates itself through senior-level attention to all clients regardless of size, maintaining a focus on building long-term relationships rather than pursuing one-off transactions.

4. Investment Banking & Brokerage

Investment banks and brokerages facilitate capital raises, mergers and acquisitions, and securities trading. The sector benefits from corporate activity during economic expansion, increased retail trading participation, and advisory opportunities in emerging sectors. Headwinds include economic cycle vulnerability affecting deal flow, compressed trading commissions due to electronic platforms, and regulatory capital requirements constraining certain higher-risk activities.

Moelis & Company competes with other independent investment banks such as Lazard (NYSE:LAZ), Evercore (NYSE:EVR), and PJT Partners (NYSE:PJT), as well as the advisory divisions of larger financial institutions like Goldman Sachs (NYSE:GS) and Morgan Stanley (NYSE:MS).

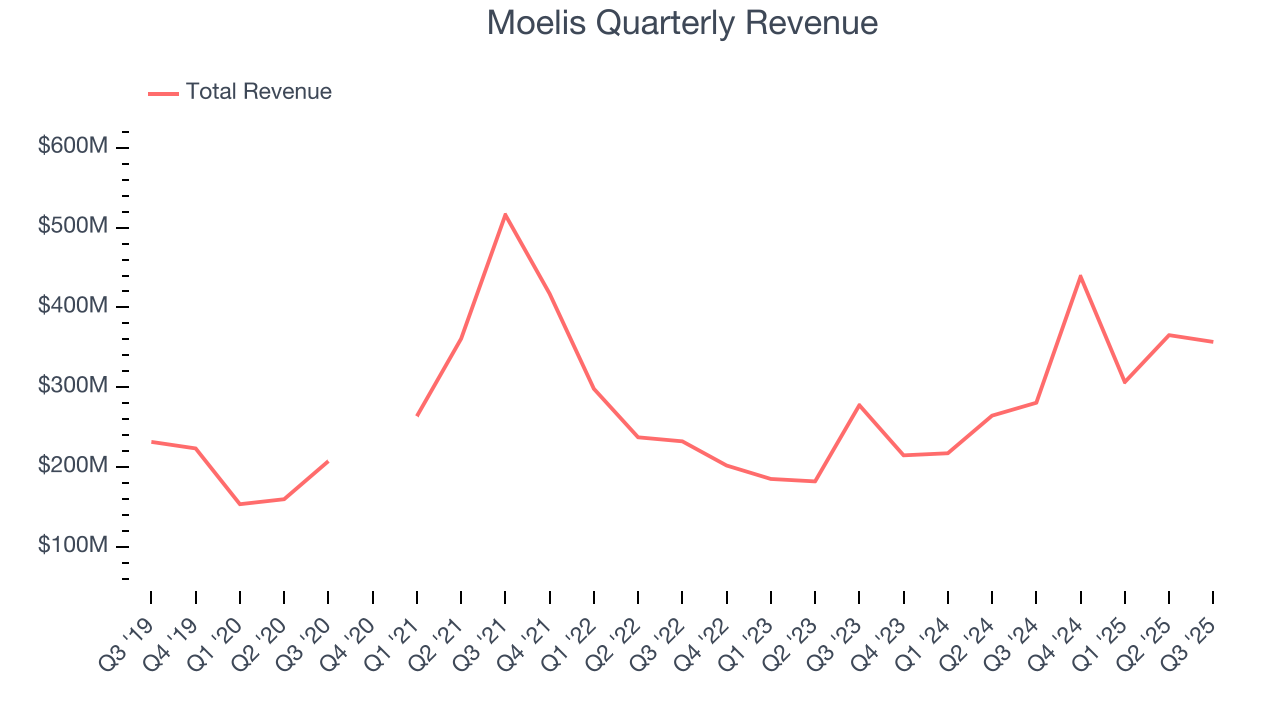

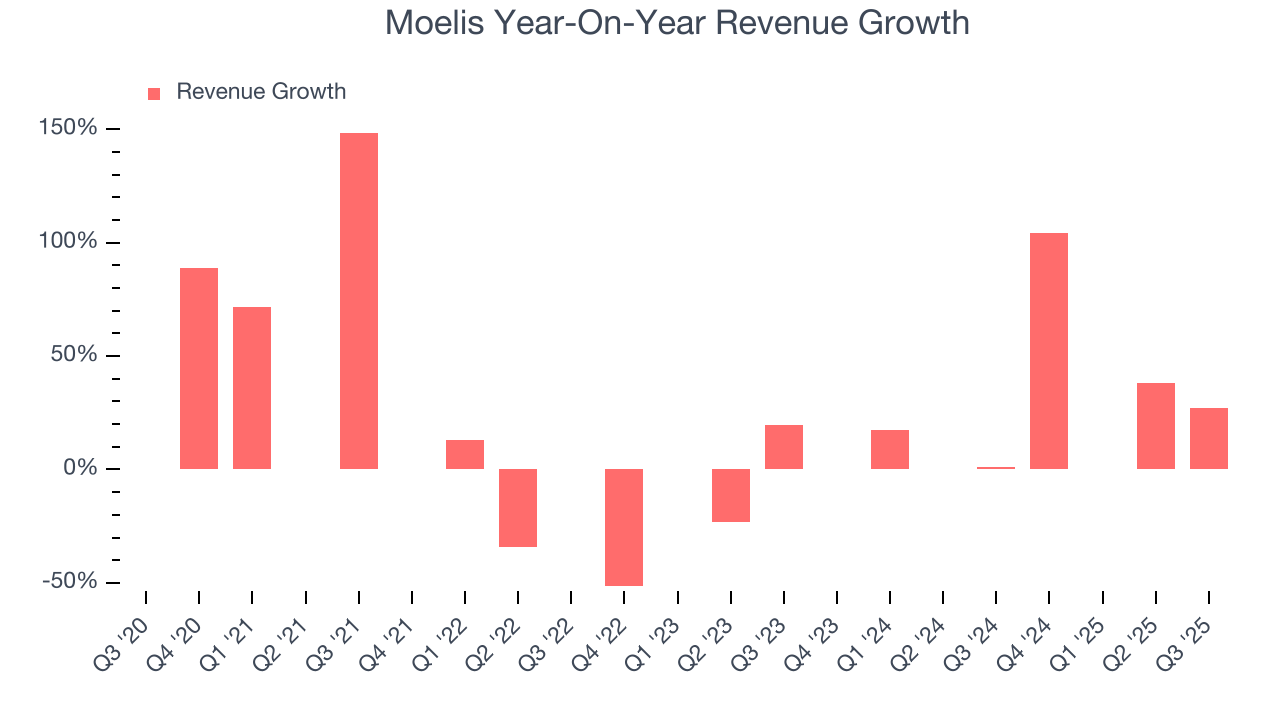

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Moelis’s revenue grew at an impressive 14.5% compounded annual growth rate over the last five years. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Moelis’s annualized revenue growth of 31.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Moelis generated an excellent 27.1% year-on-year revenue growth rate, but its $356.9 million of revenue fell short of Wall Street’s high expectations.

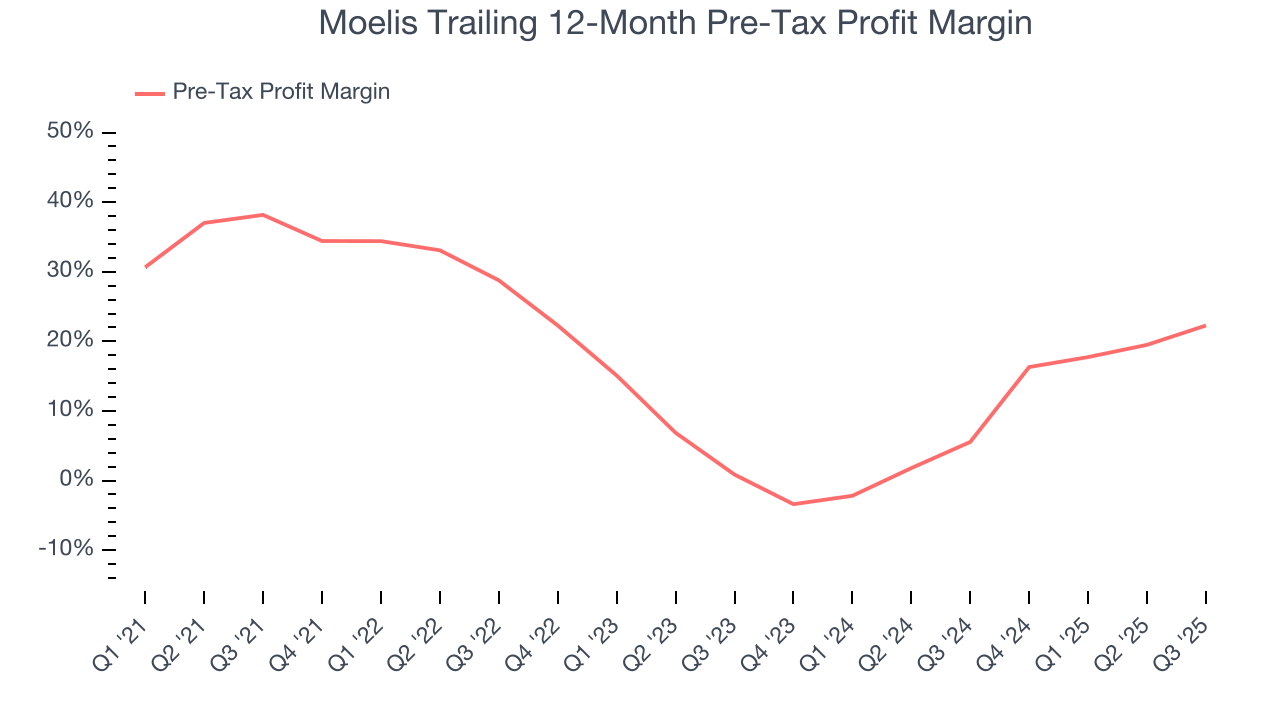

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Investment Banking & Brokerage companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because for financials businesses, interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company's control - should not.

Over the last four years, Moelis’s pre-tax profit margin has risen by 15.9 percentage points, going from 38.2% to 22.3%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 21.4 percentage points on a two-year basis.

In Q3, Moelis’s pre-tax profit margin was 23.1%. This result was 13.6 percentage points better than the same quarter last year.

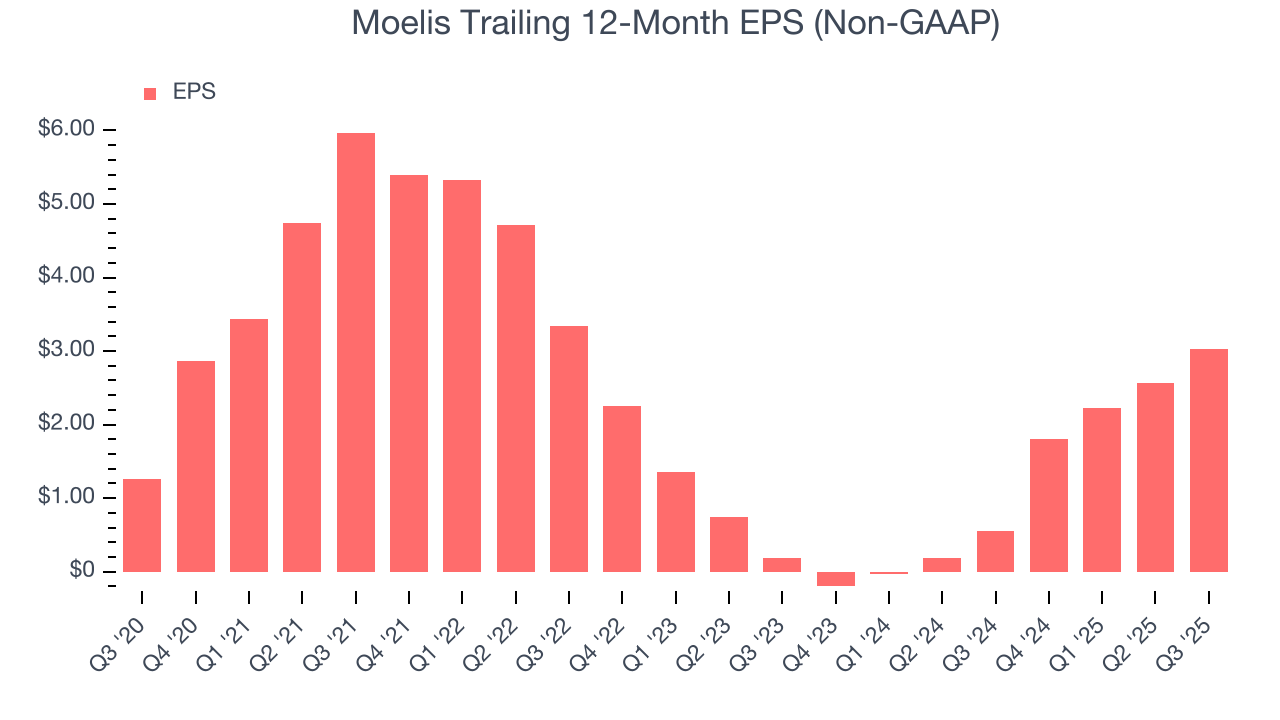

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Moelis’s EPS grew at a remarkable 19.2% compounded annual growth rate over the last five years, higher than its 14.5% annualized revenue growth. However, we take this with a grain of salt because its pre-tax profit margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from factors we consider non-core or less sustainable over the long term.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Moelis’s two-year annual EPS growth of 299% was fantastic and topped its 31.6% two-year revenue growth.

We can take a deeper look into Moelis’s earnings quality to better understand the drivers of its performance. Moelis’s pre-tax profit margin has expanded over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Moelis reported adjusted EPS of $0.68, up from $0.22 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Moelis’s full-year EPS of $3.03 to grow 2.2%.

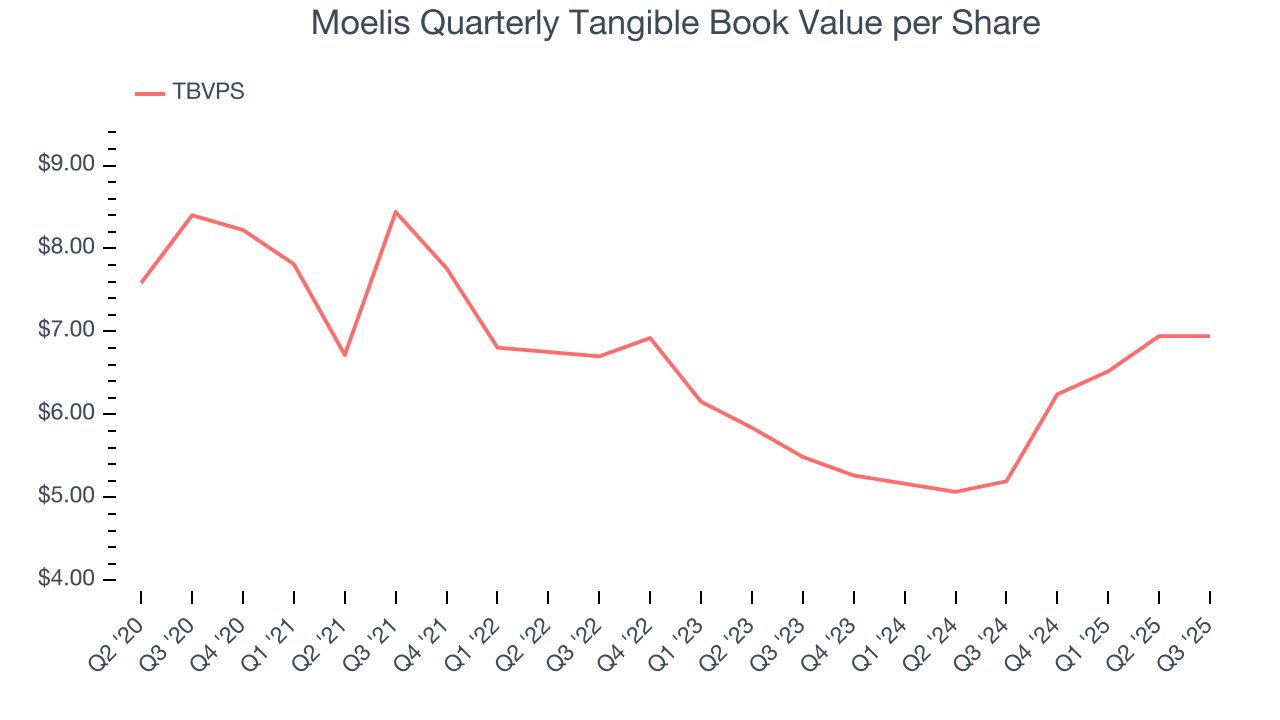

8. Tangible Book Value Per Share (TBVPS)

Financial institutions with multiple business lines manage complex balance sheets that span various financial activities. Market valuations reflect this operational complexity, prioritizing balance sheet strength and sustainable book value growth across all business segments.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark for the sector. This metric captures real, liquid net worth per share that reflects the institution’s overall financial health across all business lines. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to the complexity of multiple business lines, M&A activity, or accounting rules that vary across different financial services segments.

Moelis’s TBVPS declined at a 3.7% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 12.5% annually over the last two years from $5.49 to $6.94 per share.

9. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Moelis has averaged an ROE of 45.1%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Moelis has a strong competitive moat.

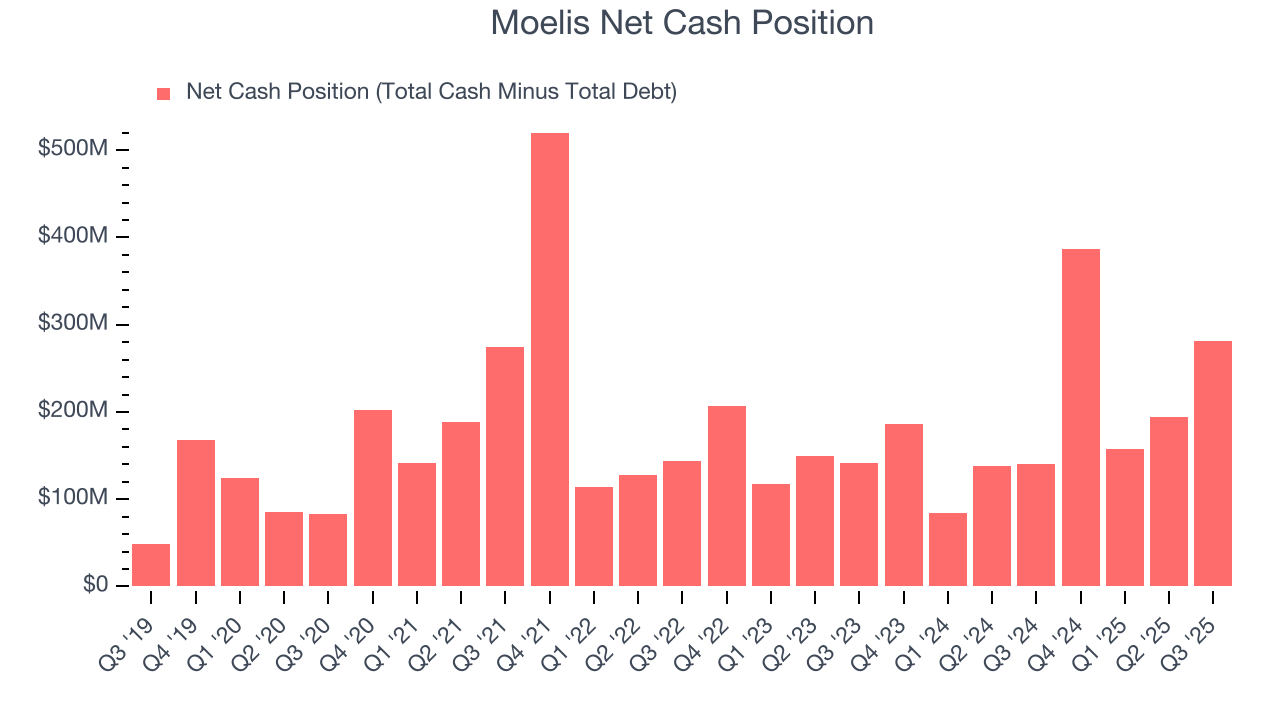

10. Balance Sheet Assessment

Moelis reported $281.6 million of cash and $0 of debt on its balance sheet in the most recent quarter.

Given the company has no debt, leverage is not an issue here.

11. Key Takeaways from Moelis’s Q3 Results

It was good to see Moelis beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed. Overall, this was a softer quarter. The stock traded down 3.1% to $64.75 immediately following the results.

12. Is Now The Time To Buy Moelis?

Updated: January 24, 2026 at 11:43 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Moelis is an amazing business ranking highly on our list. First of all, the company’s revenue growth was impressive over the last five years. And while its TBVPS has declined over the last five years, its stellar ROE suggests it has been a well-run company historically. Additionally, Moelis’s expanding pre-tax profit margin shows the business has become more efficient.

Moelis’s P/E ratio based on the next 12 months is 24.8x. This multiple isn’t necessarily cheap, but we’ll happily own Moelis as its fundamentals shine bright. We’re in the camp that investments like this should be held for at least three to five years to negate the short-term price volatility that can come with relatively high valuations.

Wall Street analysts have a consensus one-year price target of $79 on the company (compared to the current share price of $73.71).