Mueller Water Products (MWA)

Mueller Water Products is a compelling stock. It not only prints profits but also has increased its margins, showing its fundamentals are improving.― StockStory Analyst Team

1. News

2. Summary

Why We Like Mueller Water Products

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE:MWA) is a provider of water infrastructure products and flow control systems for various sectors.

- Incremental sales over the last five years have been highly profitable as its earnings per share increased by 20.1% annually, topping its revenue gains

- Excellent operating margin highlights the strength of its business model, and its rise over the last five years was fueled by some leverage on its fixed costs

- Industry-leading 12.7% return on capital demonstrates management’s skill in finding high-return investments, and its returns are climbing as it finds even more attractive growth opportunities

We’re fond of companies like Mueller Water Products. The valuation looks reasonable relative to its quality, so this could be an opportune time to invest in some shares.

Why Is Now The Time To Buy Mueller Water Products?

Mueller Water Products is trading at $27.74 per share, or 18.9x forward P/E. Valuation is lower than most companies in the industrials space, and we believe Mueller Water Products is attractively-priced for its quality.

Our work shows, time and again, that buying high-quality companies and holding them routinely leads to market outperformance. If you can get an attractive entry price, that’s icing on the cake.

3. Mueller Water Products (MWA) Research Report: Q4 CY2025 Update

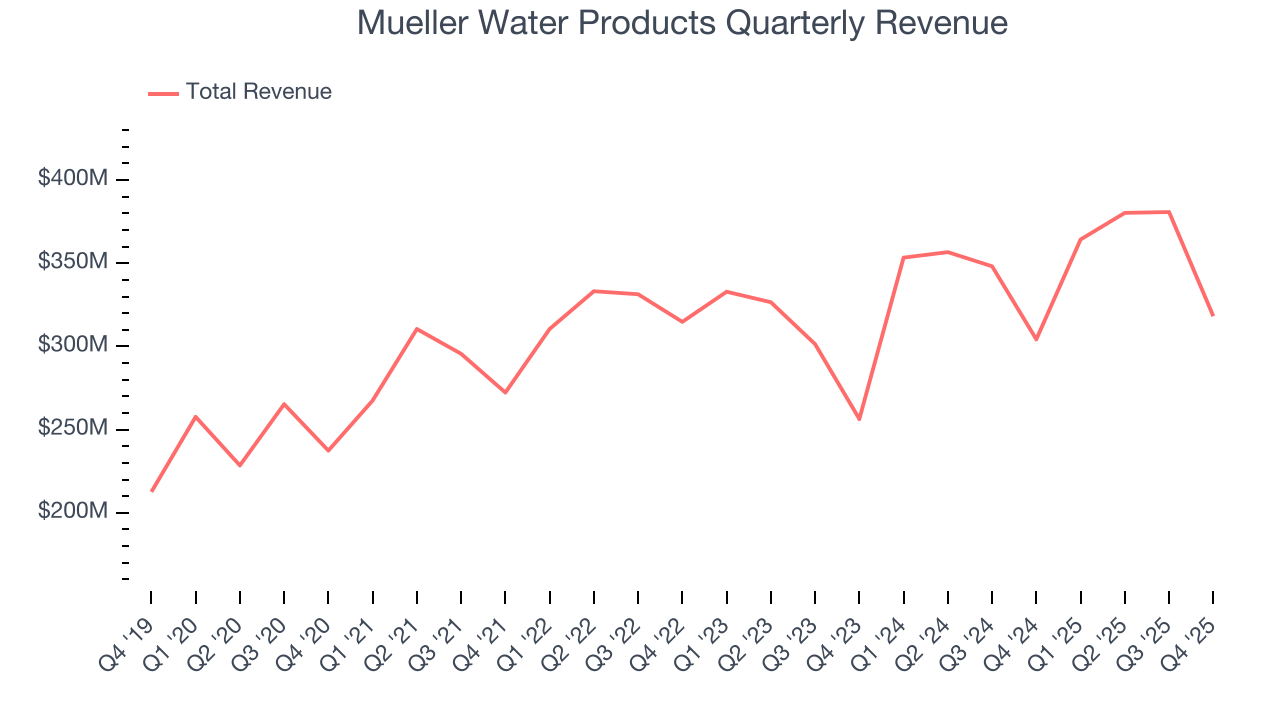

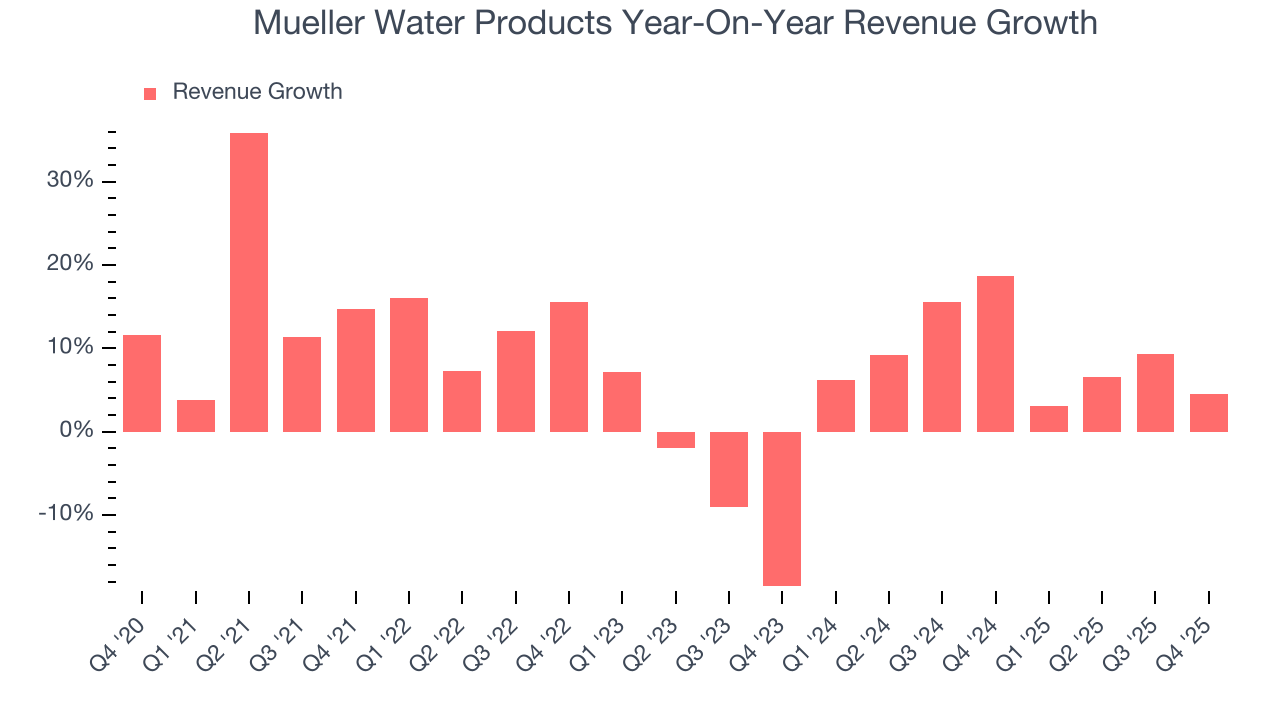

Water infrastructure products manufacturer Mueller Water Products reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 4.6% year on year to $318.2 million. The company’s full-year revenue guidance of $1.48 billion at the midpoint came in 0.8% above analysts’ estimates. Its non-GAAP profit of $0.29 per share was 10.1% above analysts’ consensus estimates.

Mueller Water Products (MWA) Q4 CY2025 Highlights:

- Revenue: $318.2 million vs analyst estimates of $311.9 million (4.6% year-on-year growth, 2% beat)

- Adjusted EPS: $0.29 vs analyst estimates of $0.26 (10.1% beat)

- Adjusted EBITDA: $72.1 million vs analyst estimates of $68.81 million (22.7% margin, 4.8% beat)

- The company lifted its revenue guidance for the full year to $1.48 billion at the midpoint from $1.46 billion, a 1.4% increase

- EBITDA guidance for the full year is $357.5 million at the midpoint, above analyst estimates of $349.4 million

- Operating Margin: 17.8%, up from 15.6% in the same quarter last year

- Free Cash Flow Margin: 13.8%, similar to the same quarter last year

- Market Capitalization: $4.31 billion

Company Overview

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE:MWA) is a provider of water infrastructure products and flow control systems for various sectors.

The company's offerings cater primarily to municipalities and the residential and non-residential construction industries. The company boasts one of the largest installed bases of iron gate valves and fire hydrants in the United States, with its products specified for use in the largest metropolitan areas across the country.

The company operates through two main segments: Water Flow Solutions and Water Management Solutions. The Water Flow Solutions segment focuses on iron gate valves, specialty valves, and service brass products. The Water Management Solutions segment encompasses fire hydrants, repair and installation services, natural gas products, metering solutions, leak detection technologies, and pressure management and control products.

The company generates income through a range of customers, including water utilities, fire protection systems, and construction contractors. A significant portion of Mueller's revenue comes from replacement and repair markets, providing a degree of stability to its income stream. The company's large installed base of products, particularly in fire hydrants and valves, contributes to recurring sales for replacement parts and upgrades.

The company's distribution strategy primarily involves selling through waterworks distributors in the United States and Canada. While Mueller has long-standing relationships with many key distributors, these relationships are generally non-exclusive.

4. Water Infrastructure

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Xylem (NYSE:XYL), A.O. Smith (NYSE:AOS), and Watts Water (NYSE:WTS).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Mueller Water Products grew its sales at a decent 7.9% compounded annual growth rate. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Mueller Water Products’s annualized revenue growth of 8.9% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Mueller Water Products reported modest year-on-year revenue growth of 4.6% but beat Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

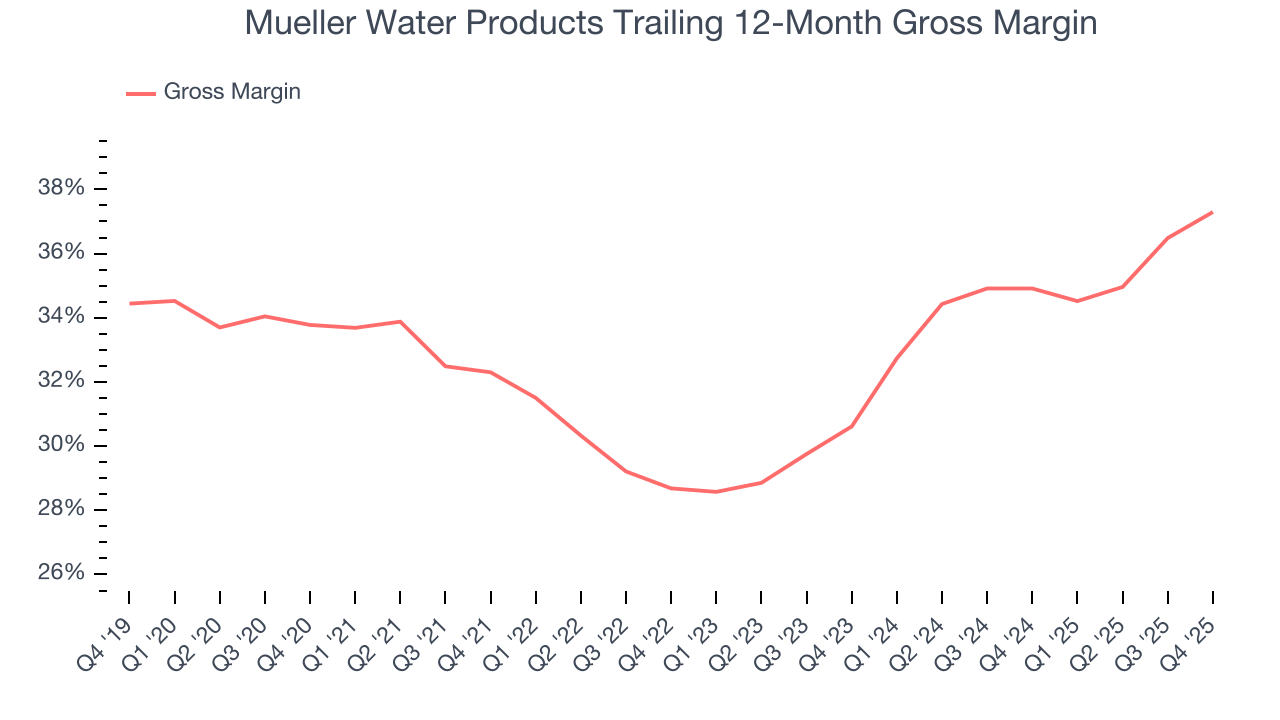

6. Gross Margin & Pricing Power

Mueller Water Products’s unit economics are better than the typical industrials business, signaling its products are somewhat differentiated through quality or brand.As you can see below, it averaged a decent 32.9% gross margin over the last five years. Said differently, Mueller Water Products paid its suppliers $67.08 for every $100 in revenue.

Mueller Water Products’s gross profit margin came in at 37.6% this quarter, up 3.8 percentage points year on year. Mueller Water Products’s full-year margin has also been trending up over the past 12 months, increasing by 2.4 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

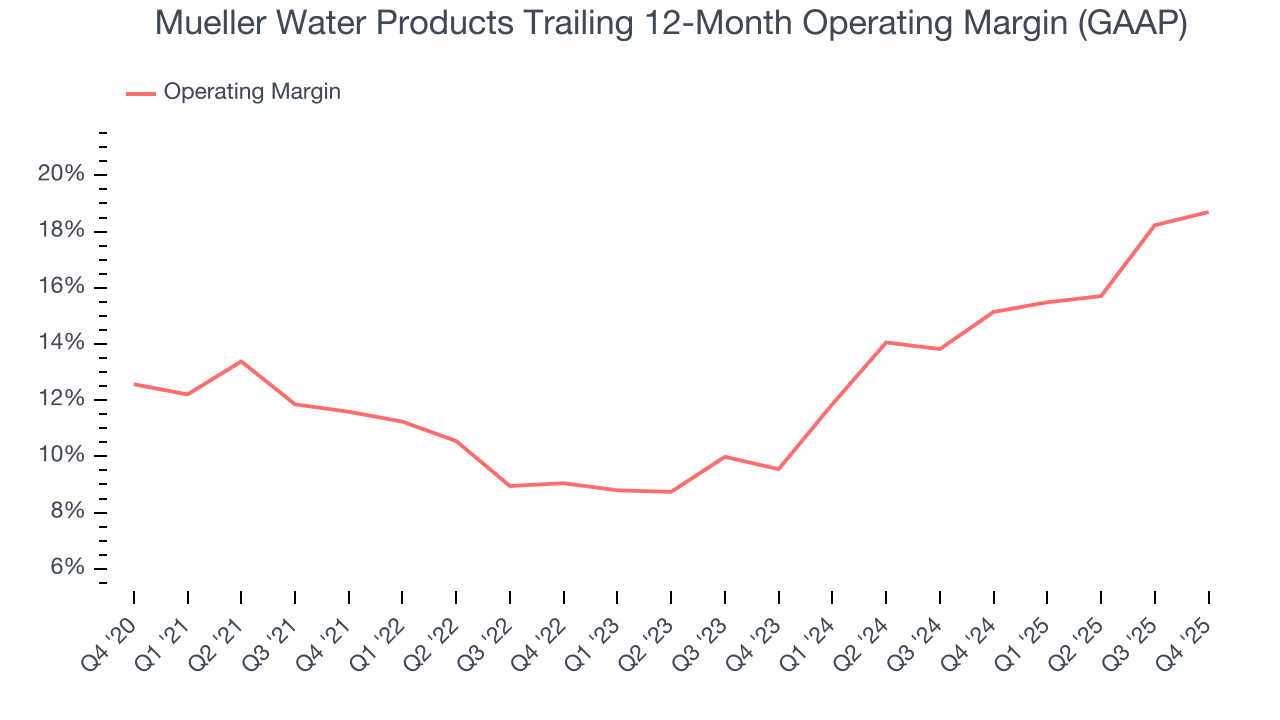

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Mueller Water Products has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 13%.

Looking at the trend in its profitability, Mueller Water Products’s operating margin rose by 7.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Mueller Water Products generated an operating margin profit margin of 17.8%, up 2.2 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

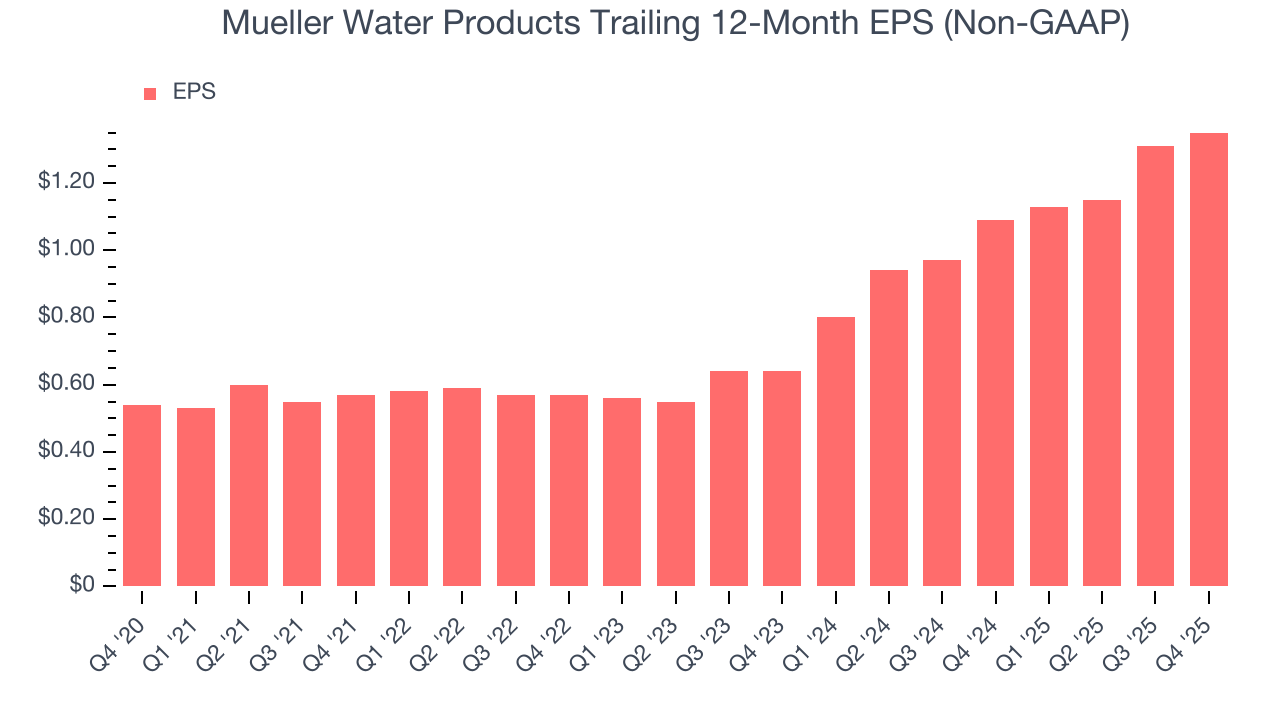

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Mueller Water Products’s EPS grew at an astounding 20.1% compounded annual growth rate over the last five years, higher than its 7.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Mueller Water Products’s earnings to better understand the drivers of its performance. As we mentioned earlier, Mueller Water Products’s operating margin expanded by 7.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Mueller Water Products, its two-year annual EPS growth of 45.2% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Mueller Water Products reported adjusted EPS of $0.29, up from $0.25 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Mueller Water Products’s full-year EPS of $1.35 to grow 7.3%.

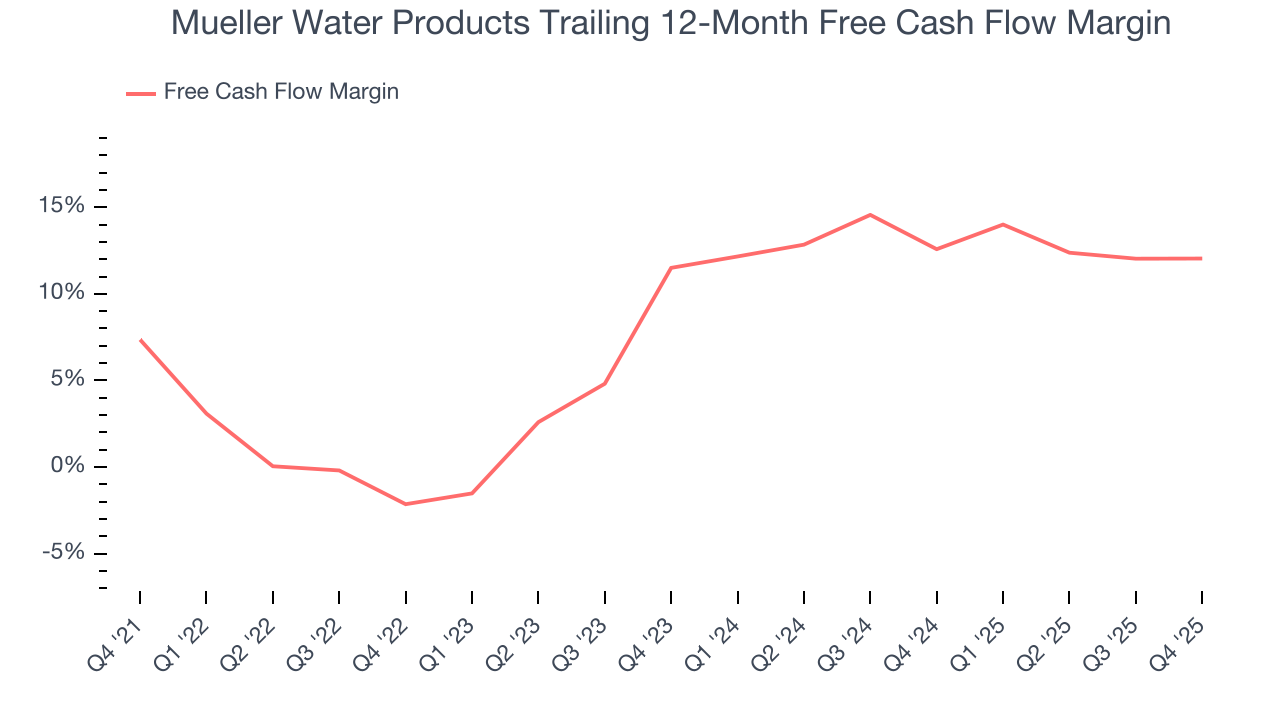

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Mueller Water Products has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 8.4% over the last five years, better than the broader industrials sector.

Taking a step back, we can see that Mueller Water Products’s margin expanded by 4.7 percentage points during that time. This is encouraging because it gives the company more optionality.

Mueller Water Products’s free cash flow clocked in at $44 million in Q4, equivalent to a 13.8% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

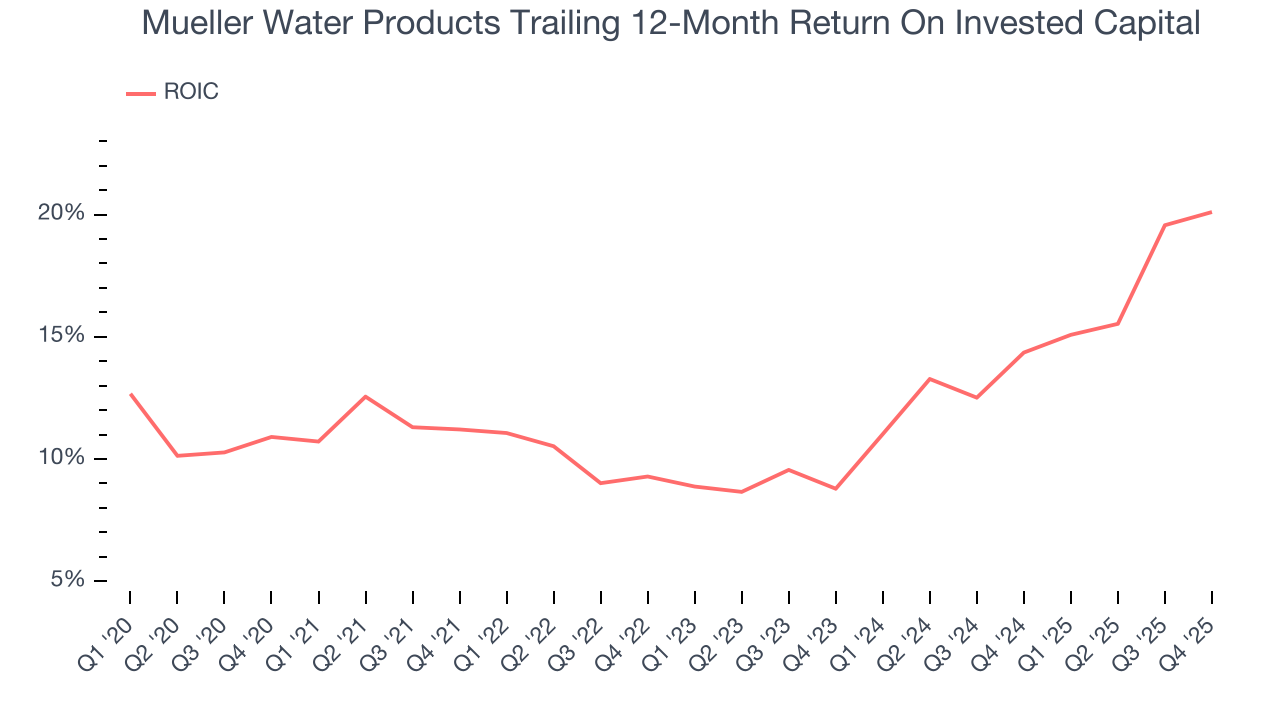

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Mueller Water Products’s five-year average ROIC was 12.7%, higher than most industrials businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Mueller Water Products’s has increased over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

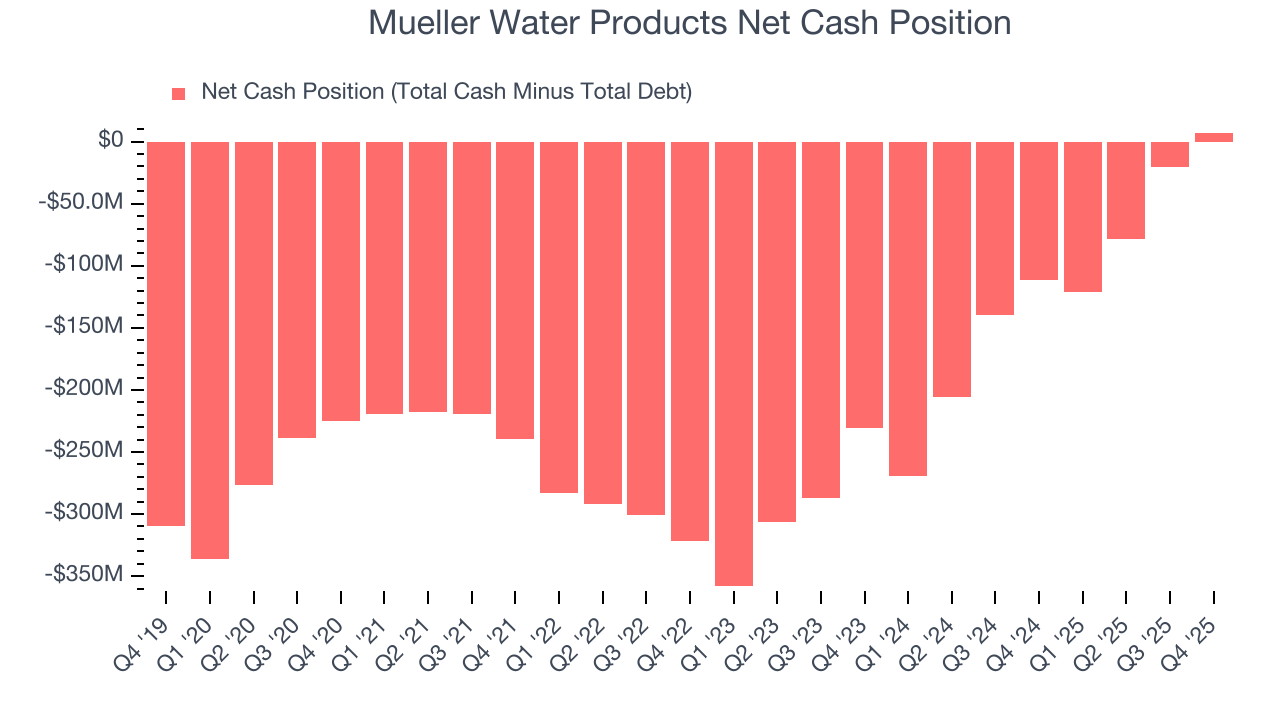

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Mueller Water Products is a profitable, well-capitalized company with $459.6 million of cash and $452.3 million of debt on its balance sheet. This $7.3 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Mueller Water Products’s Q4 Results

It was great to see Mueller Water Products’s full-year EBITDA guidance top analysts’ expectations. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $27.73 immediately after reporting.

13. Is Now The Time To Buy Mueller Water Products?

Updated: March 13, 2026 at 11:29 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Mueller Water Products.

There are multiple reasons why we think Mueller Water Products is an amazing business. For starters, its revenue growth was decent over the last five years. On top of that, its expanding operating margin shows the business has become more efficient, and its astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Mueller Water Products’s P/E ratio based on the next 12 months is 18.9x. Looking across the spectrum of industrials companies today, Mueller Water Products’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $30.33 on the company (compared to the current share price of $27.74), implying they see 9.4% upside in buying Mueller Water Products in the short term.