Norwegian Cruise Line (NCLH)

Norwegian Cruise Line is in for a bumpy ride. Its negative returns on capital raise questions about its ability to allocate resources and generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Norwegian Cruise Line Will Underperform

With amenities like a full go-kart race track built into its ships, Norwegian Cruise Line (NYSE:NCLH) is a premier global cruise company.

- 7.2% annual revenue growth over the last two years was slower than its consumer discretionary peers

- Cash-burning history makes us doubt the long-term viability of its business model

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Norwegian Cruise Line doesn’t pass our quality test. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Norwegian Cruise Line

Norwegian Cruise Line’s stock price of $19.77 implies a valuation ratio of 8x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Norwegian Cruise Line (NCLH) Research Report: Q4 CY2025 Update

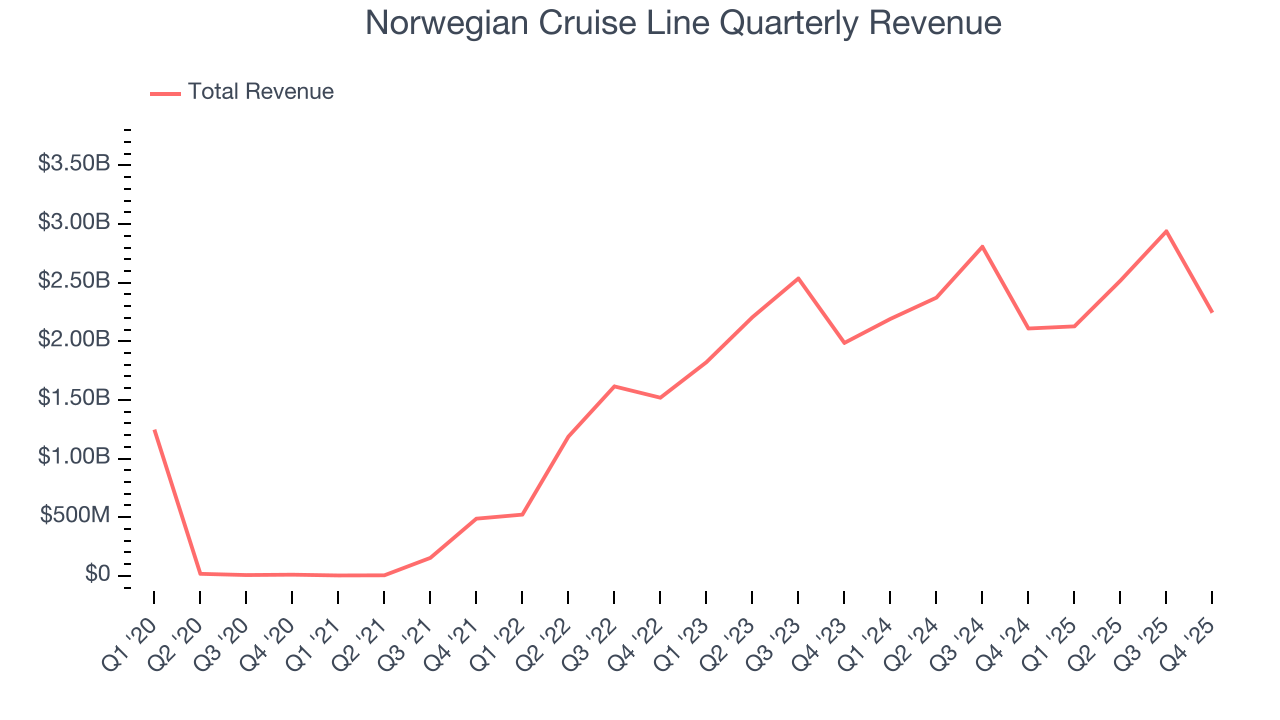

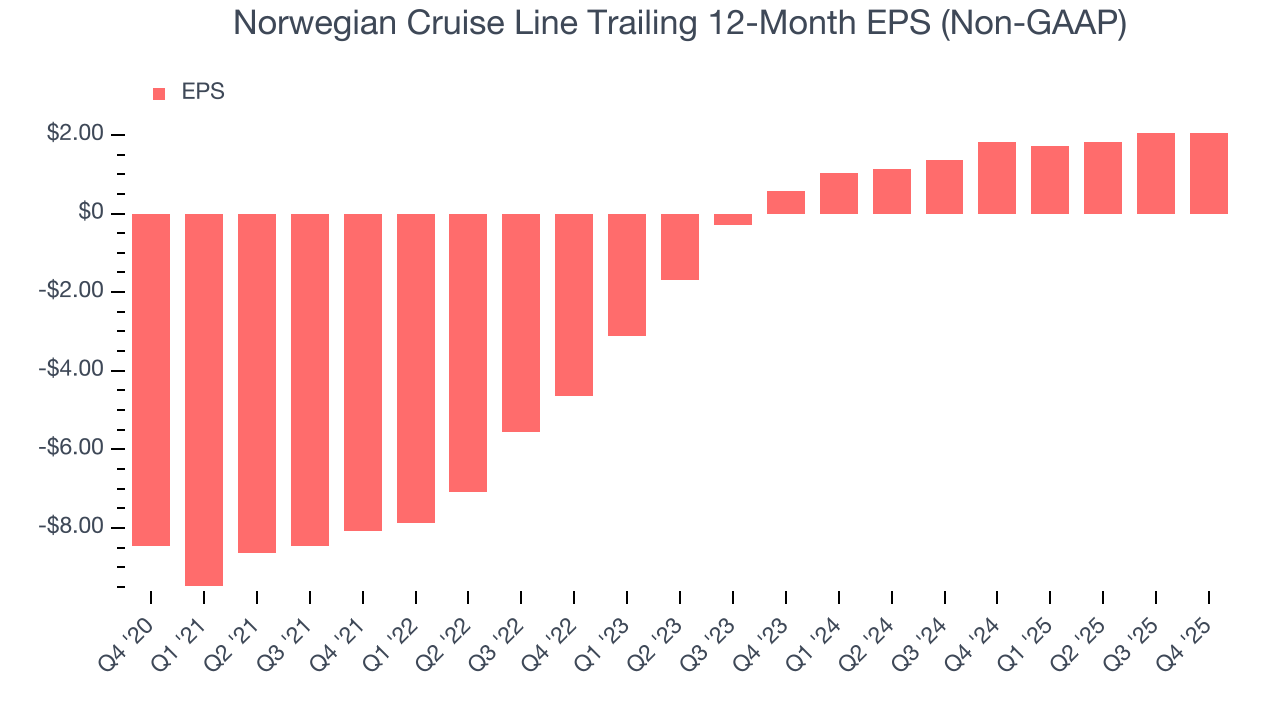

Cruise company Norwegian Cruise Line (NYSE:NCLH) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 6.4% year on year to $2.24 billion. Its non-GAAP profit of $0.28 per share was 5.5% above analysts’ consensus estimates.

Norwegian Cruise Line (NCLH) Q4 CY2025 Highlights:

- Revenue: $2.24 billion vs analyst estimates of $2.34 billion (6.4% year-on-year growth, 4.2% miss)

- Adjusted EPS: $0.28 vs analyst estimates of $0.27 (5.5% beat)

- Adjusted EBITDA: $563.9 million vs analyst estimates of $555.5 million (25.1% margin, 1.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.38 at the midpoint, missing analyst estimates by 8.3%

- EBITDA guidance for the upcoming financial year 2026 is $2.95 billion at the midpoint, below analyst estimates of $3.05 billion

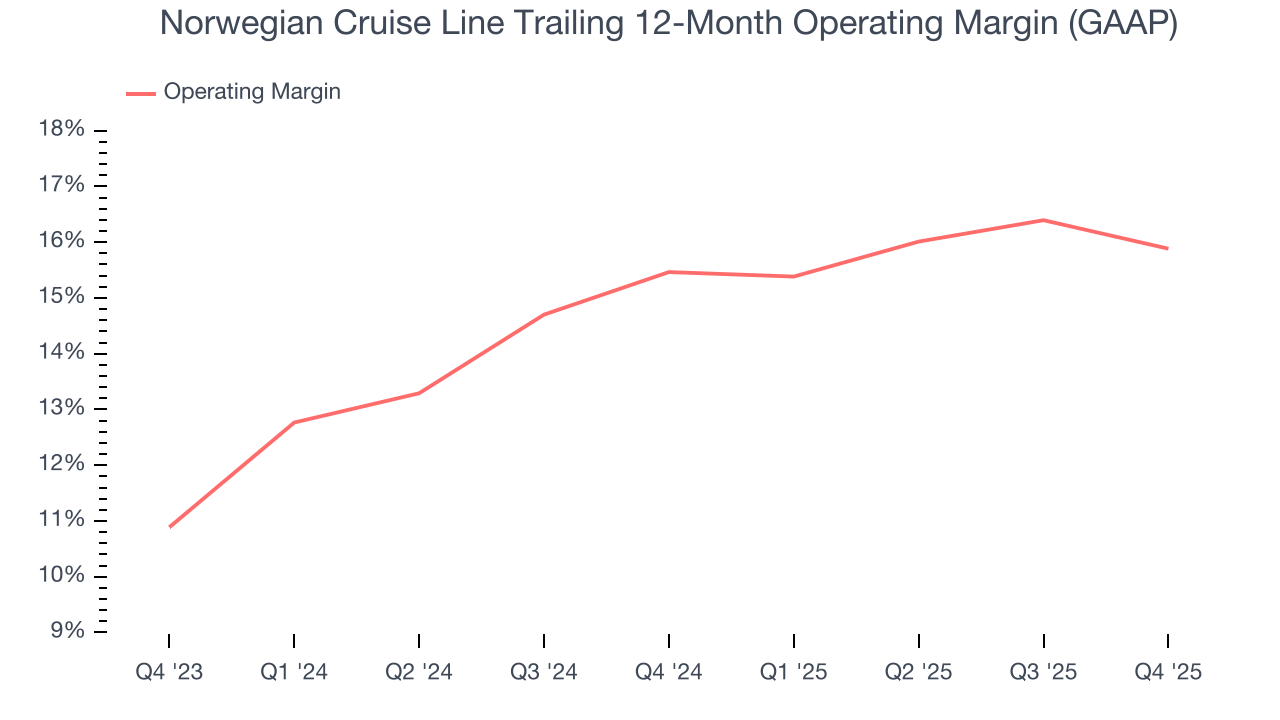

- Operating Margin: 8.3%, down from 10.2% in the same quarter last year

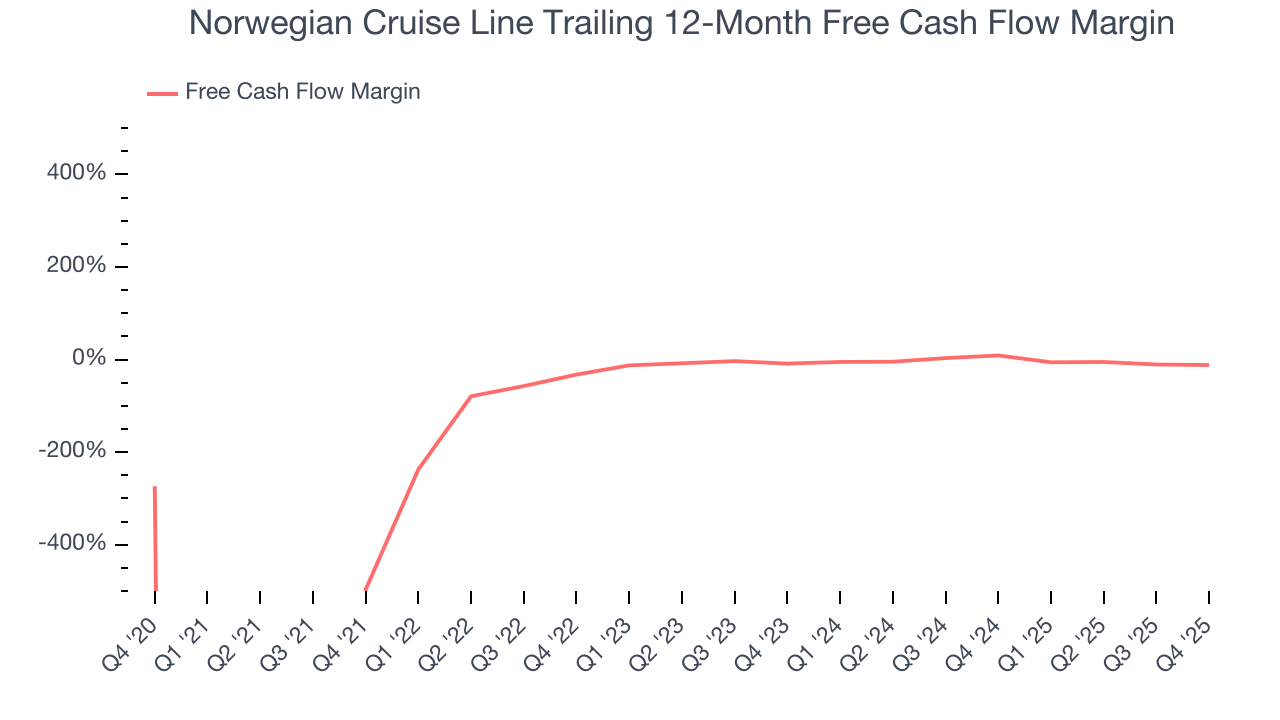

- Free Cash Flow Margin: 1%, down from 7.4% in the same quarter last year

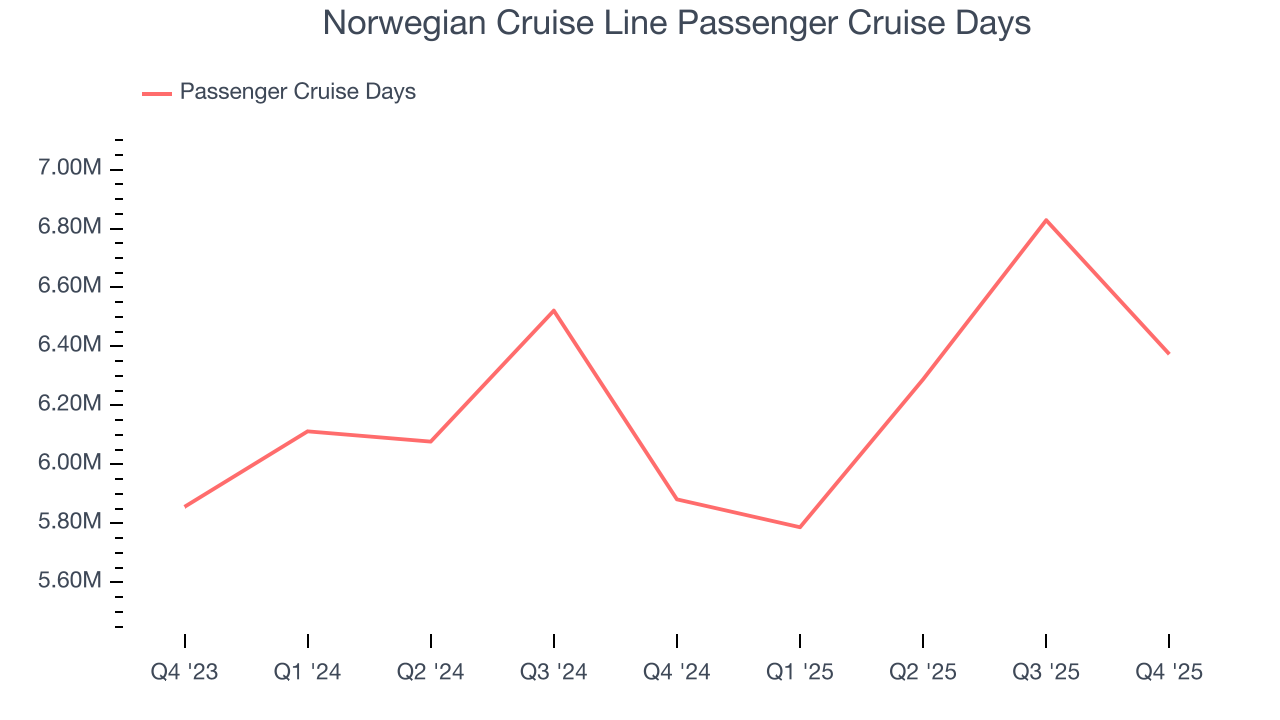

- Passenger Cruise Days: 6.37 million, up 492,289 year on year

- Market Capitalization: $11.29 billion

Company Overview

With amenities like a full go-kart race track built into its ships, Norwegian Cruise Line (NYSE:NCLH) is a premier global cruise company.

Norwegian Cruise Line's fleet consists of about 30 ships, each offering different guest experiences. The ships sail to over 490 destinations worldwide, including the Caribbean, Alaska, Europe, South America, and the Far East.

Norwegian Cruise Line pioneered the "Freestyle Cruising" category by offering guests the freedom and flexibility to design their ideal cruise vacation on their schedule. This resort-style cruise vacation has no fixed dining times, formal dress codes, or pre-assigned seating, along with a wealth of entertainment options and activities.

The company's ships offer an array of amenities and entertainment options including award-winning dining experiences, Broadway-style shows, water parks, and modern fitness centers. Norwegian Cruise Line is also known for its unique ship design, with many vessels featuring The Waterfront, a unique oceanfront promenade, and The Haven, an exclusive retreat with private amenities.

4. Consumer Discretionary - Travel and Vacation Providers

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Travel and vacation providers operate tour packages, cruise lines, online travel agencies, and vacation rental platforms, connecting consumers with leisure and business travel experiences. Tailwinds include robust post-pandemic travel demand, a consumer preference shift toward experiences over goods, and technology-enabled personalization improving conversion and loyalty. However, headwinds are significant: the industry is acutely sensitive to macroeconomic cycles, geopolitical instability, and fuel price volatility. Low switching costs mean fierce price competition, while capacity additions in segments like cruises can lead to oversupply. Regulatory burdens, weather disruptions, and public health risks further create episodic but potentially severe demand shocks.

Norwegian Cruise Line's primary competitors include Carnival (NYSE:CCL), Royal Caribbean (NYSE:RCL), Disney Cruise Line (owned by Disney NYSE:DIS), and private companies Viking Ocean Cruises and MSC Cruises.

5. Revenue Growth

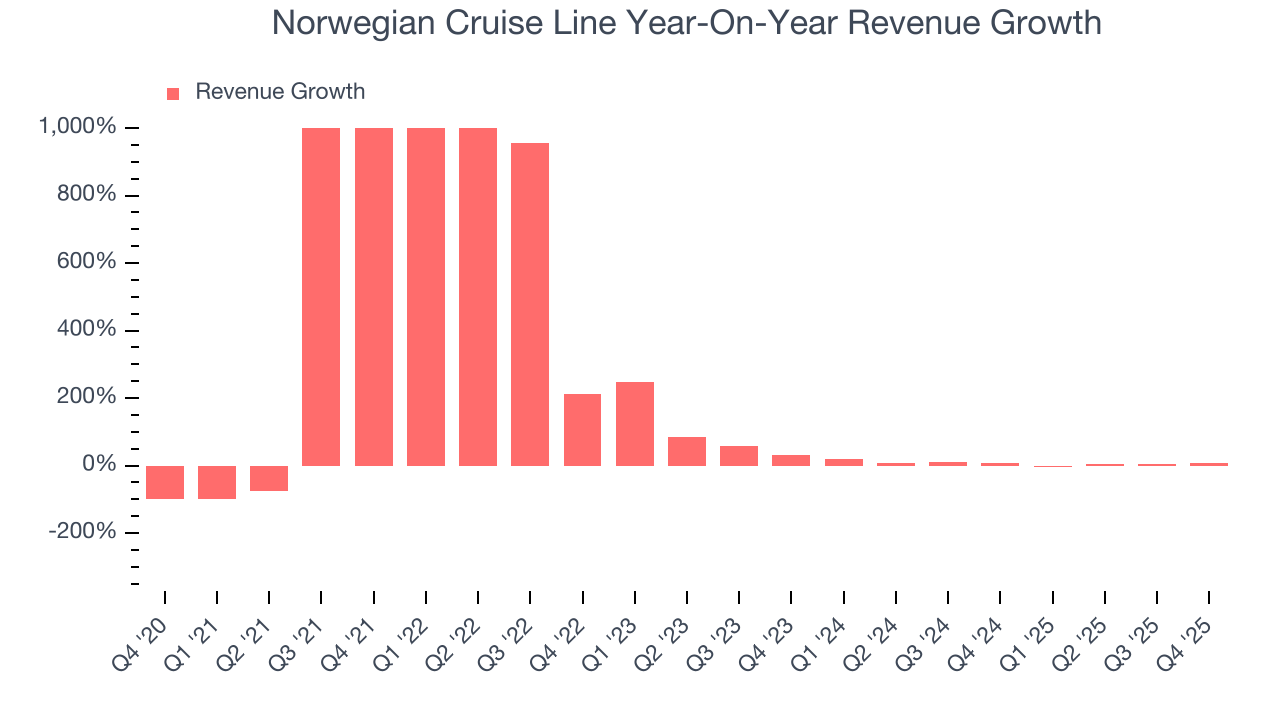

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Norwegian Cruise Line’s sales grew at a solid 50.3% compounded annual growth rate over the last five years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Norwegian Cruise Line’s recent performance shows its demand has slowed as its annualized revenue growth of 7.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Norwegian Cruise Line also discloses its number of passenger cruise days, which reached 6.37 million in the latest quarter. Over the last two years, Norwegian Cruise Line’s passenger cruise days averaged 2.3% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Norwegian Cruise Line’s revenue grew by 6.4% year on year to $2.24 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.6% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

6. Operating Margin

Norwegian Cruise Line’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 15.7% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, Norwegian Cruise Line generated an operating margin profit margin of 8.3%, down 1.9 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Norwegian Cruise Line’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Norwegian Cruise Line reported adjusted EPS of $0.28, up from $0.26 in the same quarter last year. This print beat analysts’ estimates by 5.5%. Over the next 12 months, Wall Street expects Norwegian Cruise Line’s full-year EPS of $2.06 to grow 24.1%.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Norwegian Cruise Line’s free cash flow broke even this quarter, the broader story hasn’t been so clean. Over the last two years, Norwegian Cruise Line’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.7%, meaning it lit $1.71 of cash on fire for every $100 in revenue.

Norwegian Cruise Line broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 6.4 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

Over the next year, analysts predict Norwegian Cruise Line will continue burning cash, albeit to a lesser extent. Their consensus estimates imply its free cash flow margin of negative 11.9% for the last 12 months will increase to negative 4.6%.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Norwegian Cruise Line’s five-year average ROIC was negative 1.2%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Norwegian Cruise Line’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

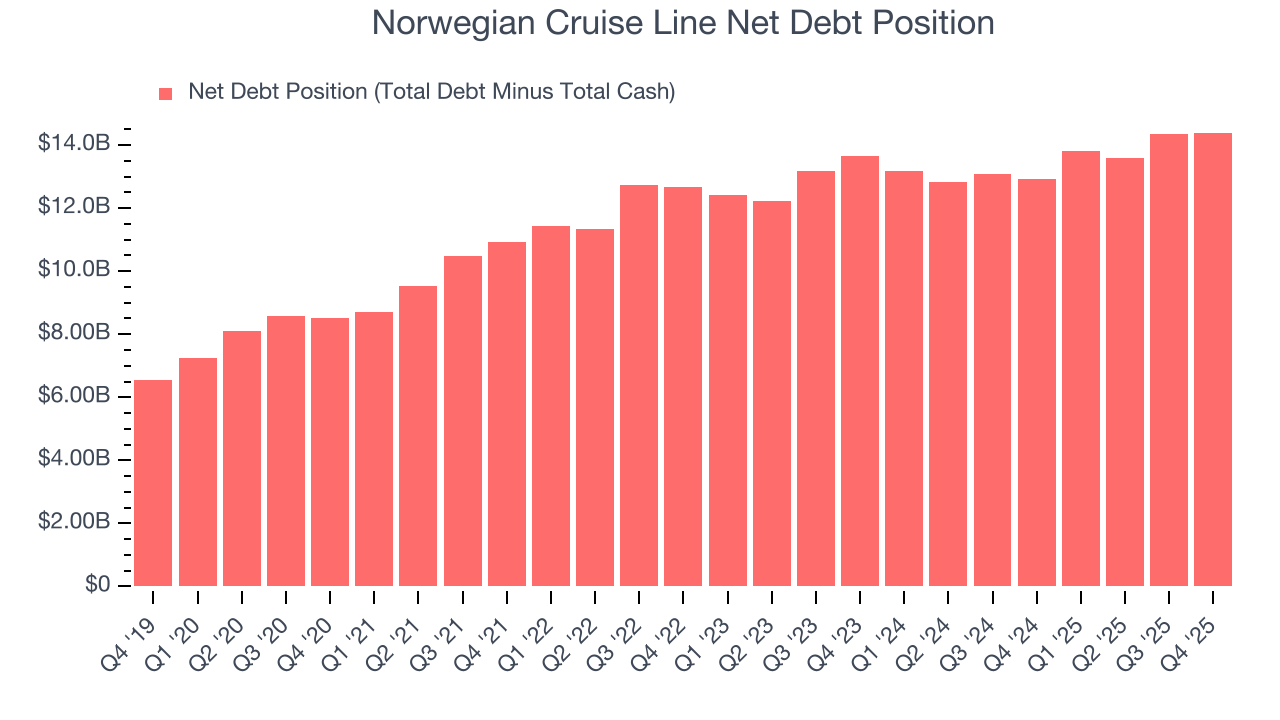

Norwegian Cruise Line burned through $1.17 billion of cash over the last year, and its $14.61 billion of debt exceeds the $209.9 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Norwegian Cruise Line’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Norwegian Cruise Line until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

11. Key Takeaways from Norwegian Cruise Line’s Q4 Results

It was good to see Norwegian Cruise Line provide EBITDA guidance for next quarter that slightly beat analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 7% to $23.07 immediately after reporting.

12. Is Now The Time To Buy Norwegian Cruise Line?

Updated: March 16, 2026 at 11:00 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We cheer for all companies serving everyday consumers, but in the case of Norwegian Cruise Line, we’ll be cheering from the sidelines. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its number of passenger cruise days has disappointed. And while the company’s Forecasted free cash flow margin suggests the company will have more capital to invest or return to shareholders next year, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Norwegian Cruise Line’s P/E ratio based on the next 12 months is 8x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $26.43 on the company (compared to the current share price of $19.77).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.