OneMain (OMF)

We’re skeptical of OneMain. Its revenue growth has been weak and its profitability has caved, showing it’s struggling to adapt.― StockStory Analyst Team

1. News

2. Summary

Why We Think OneMain Will Underperform

Dating back to 1912 and formerly known as Springleaf, OneMain Holdings (NYSE:OMF) provides personal loans, auto financing, and credit cards to nonprime consumers who have limited access to traditional banking services.

- Annual earnings per share growth of 1.8% underperformed its revenue over the last five years, showing its incremental sales were less profitable

- Muted 1.9% annual tangible book value per share growth over the last five years shows its capital generation lagged behind its financials peers

OneMain’s quality is inadequate. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than OneMain

OneMain’s stock price of $51.93 implies a valuation ratio of 6.8x forward P/E. OneMain’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. OneMain (OMF) Research Report: Q4 CY2025 Update

Consumer finance company OneMain Holdings (NYSE:OMF) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 9.1% year on year to $1.29 billion. Its GAAP profit of $1.72 per share was 21.6% above analysts’ consensus estimates.

OneMain (OMF) Q4 CY2025 Highlights:

- Net Interest Income: $1.09 billion vs analyst estimates of $1.08 billion

- Revenue: $1.29 billion vs analyst estimates of $1.28 billion (9.1% year-on-year growth, 0.7% beat)

- Pre-tax Profit: $249 million (19.4% margin)

- EPS (GAAP): $1.72 vs analyst estimates of $1.41 (21.6% beat)

- Market Capitalization: $7.44 billion

Company Overview

Dating back to 1912 and formerly known as Springleaf, OneMain Holdings (NYSE:OMF) provides personal loans, auto financing, and credit cards to nonprime consumers who have limited access to traditional banking services.

OneMain operates at the intersection of traditional branch-based lending and modern digital financial services. The company's core business revolves around installment loans with fixed rates and terms typically between three and six years. These loans may be secured by automobiles or other collateral, or they may be unsecured, depending on the customer's profile and needs.

The company serves a distinct market segment—consumers with credit profiles that often prevent them from accessing loans through traditional banks or credit card companies. For example, a customer might come to OneMain when they need to consolidate high-interest debt, cover unexpected medical expenses, or finance home improvements but have been turned down by mainstream lenders.

OneMain's underwriting process combines automated credit decisioning with personalized assessment of a customer's ability to repay, including income verification and monthly budget analysis. For secured loans, the company obtains security interests in titled property like vehicles, providing additional protection against default.

Beyond personal loans, OneMain has expanded into point-of-sale auto financing through dealership partnerships and offers two credit card products—BrightWay and BrightWay+. The company also generates revenue through optional products such as credit insurance, which can cover loan payments if a borrower experiences disability, death, or involuntary unemployment.

OneMain's business model balances the higher risk of its customer base with higher interest rates than prime lenders, while providing financial wellness tools through its Trim by OneMain platform to help customers improve their financial health.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

OneMain Holdings competes with other nonprime consumer lenders such as Upstart (NASDAQ:UPST), LendingClub (NYSE:LC), and regional banks that offer personal loans. In the auto financing space, its competitors include Credit Acceptance Corporation (NASDAQ:CACC) and regional auto lenders focused on nonprime borrowers.

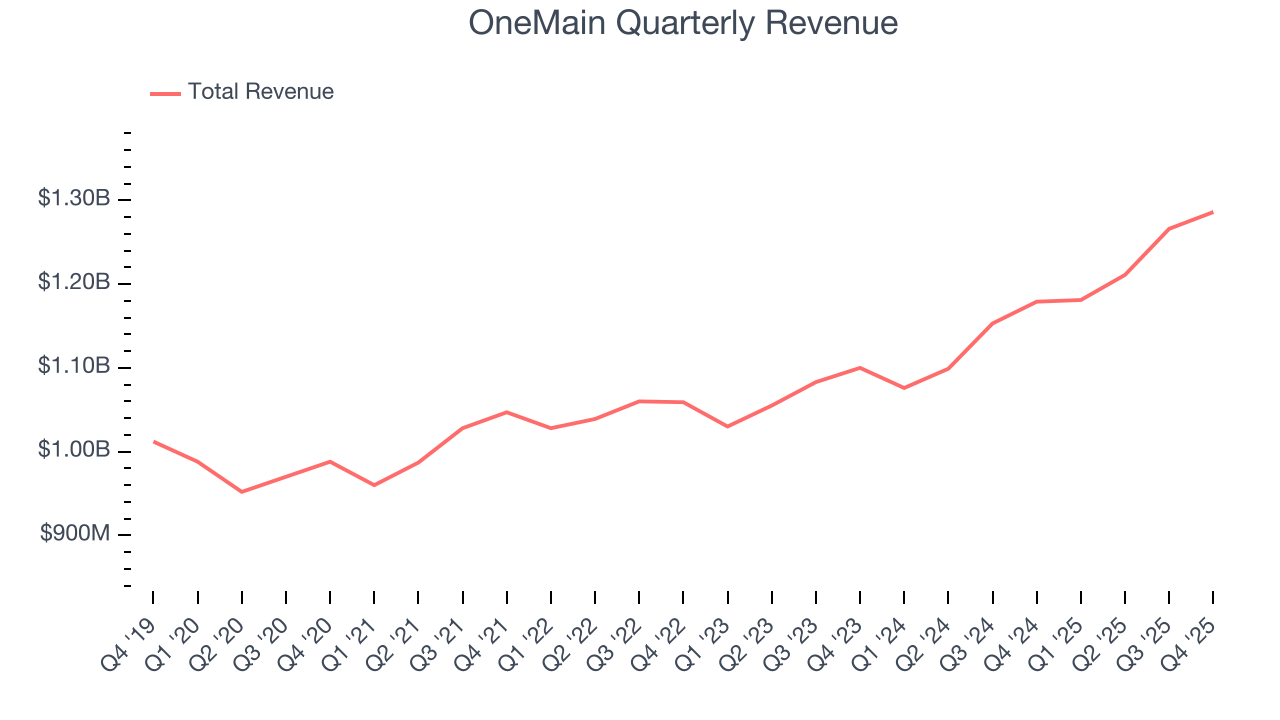

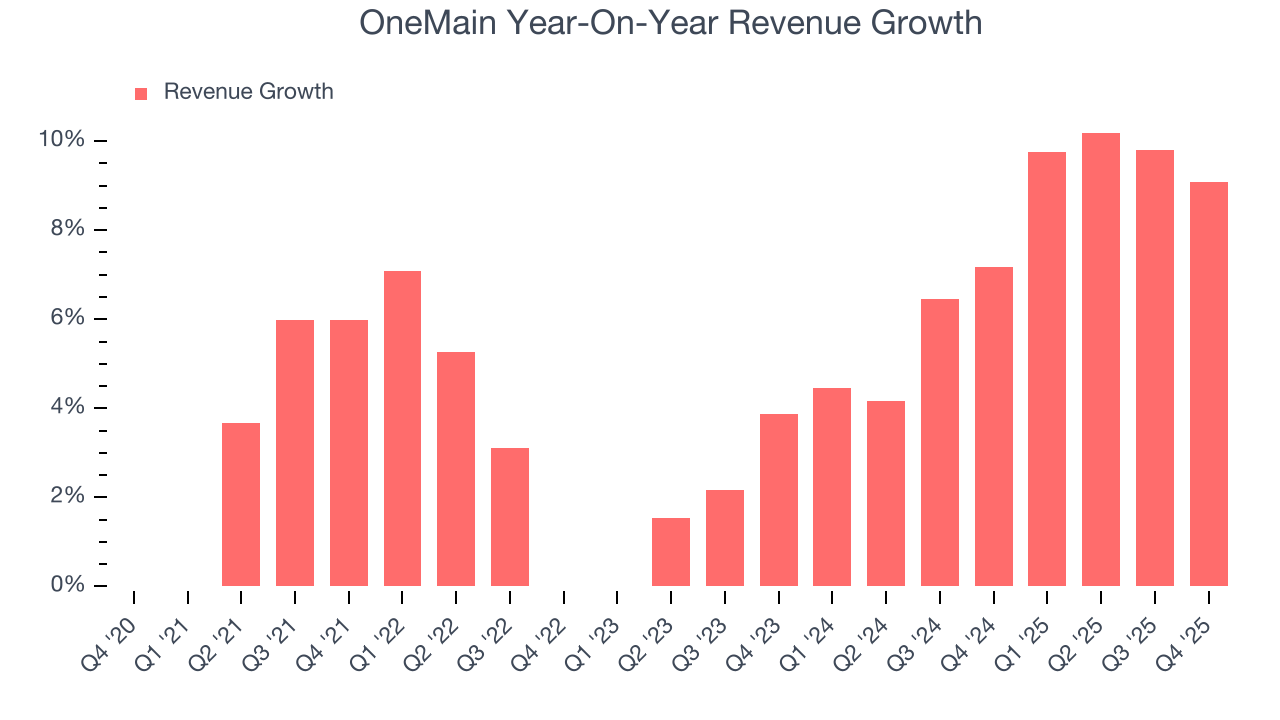

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, OneMain grew its revenue at a tepid 4.9% compounded annual growth rate. This was below our standard for the financials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. OneMain’s annualized revenue growth of 7.6% over the last two years is above its five-year trend, suggesting some bright spots.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, OneMain reported year-on-year revenue growth of 9.1%, and its $1.29 billion of revenue exceeded Wall Street’s estimates by 0.7%.

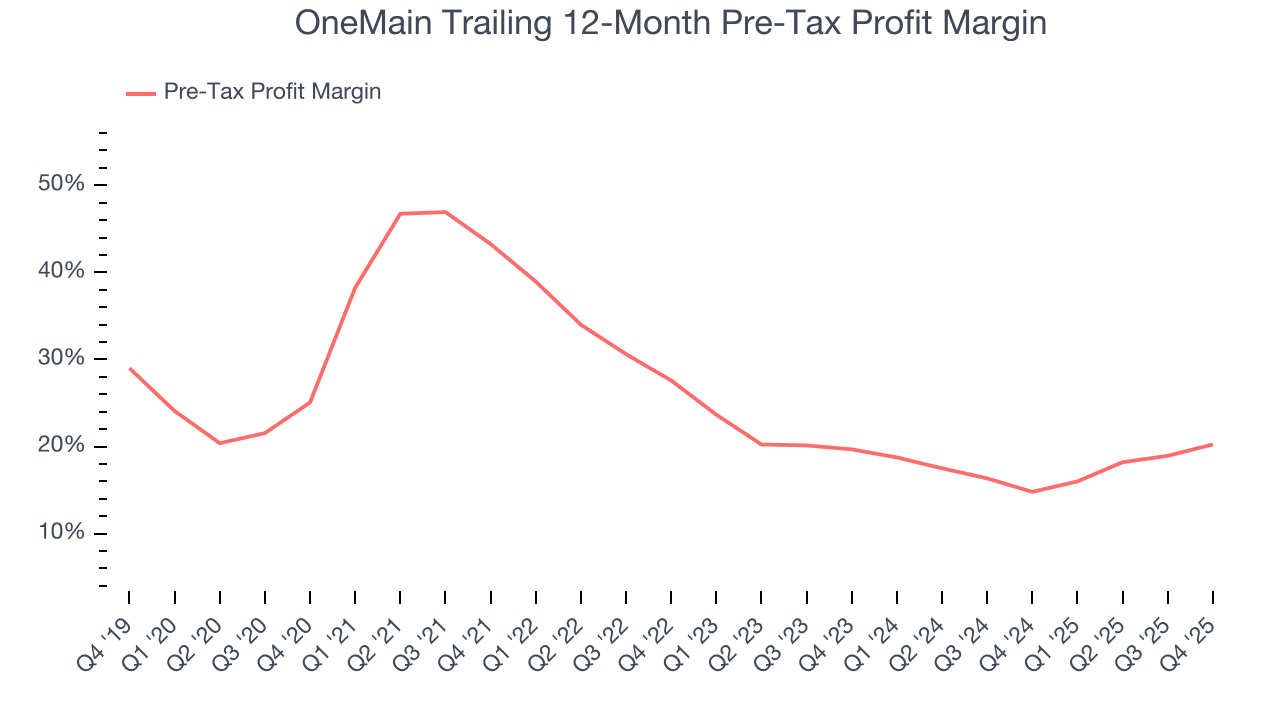

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because for financials businesses, interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company's control - should not.

Over the last five years, OneMain’s pre-tax profit margin has risen by 4.8 percentage points, going from 43.3% to 20.2%. Expenses have stabilized more recently as the company’s pre-tax profit margin was flat on a two-year basis.

In Q4, OneMain’s pre-tax profit margin was 19.4%. This result was 5.5 percentage points better than the same quarter last year.

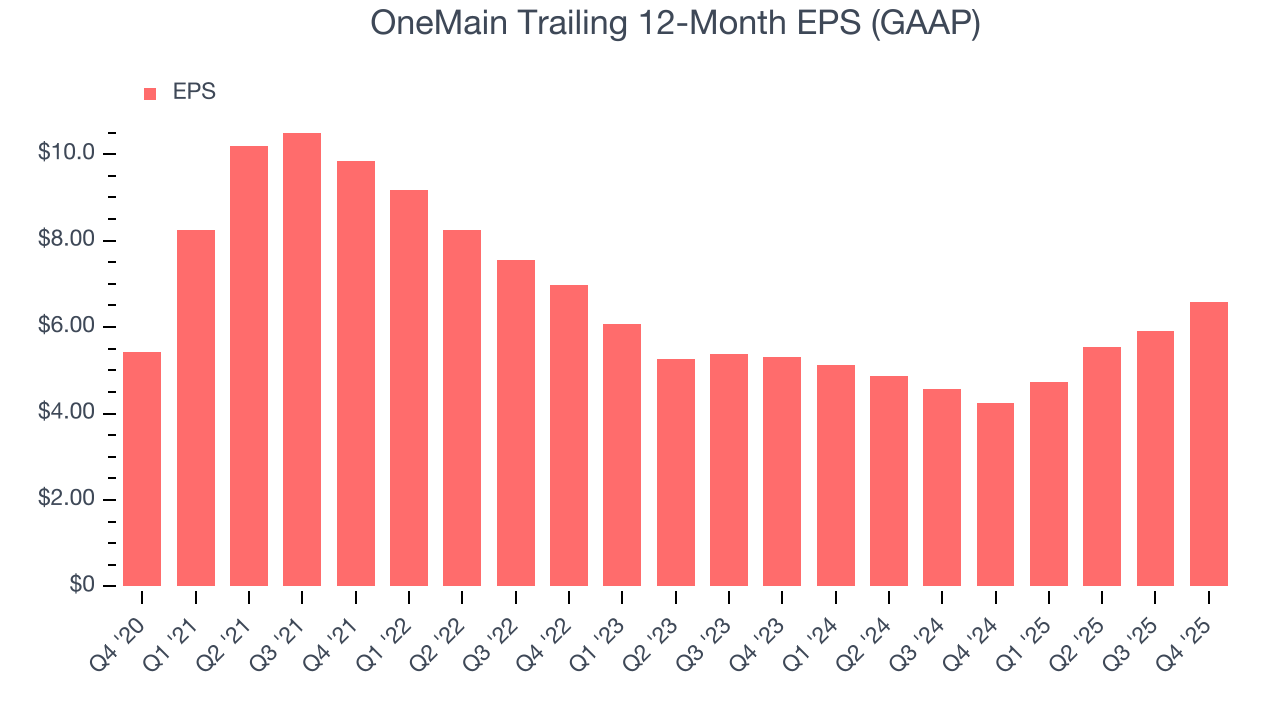

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

OneMain’s weak 3.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

OneMain’s two-year annual EPS growth of 11.2% was decent and topped its 7.6% two-year revenue growth.

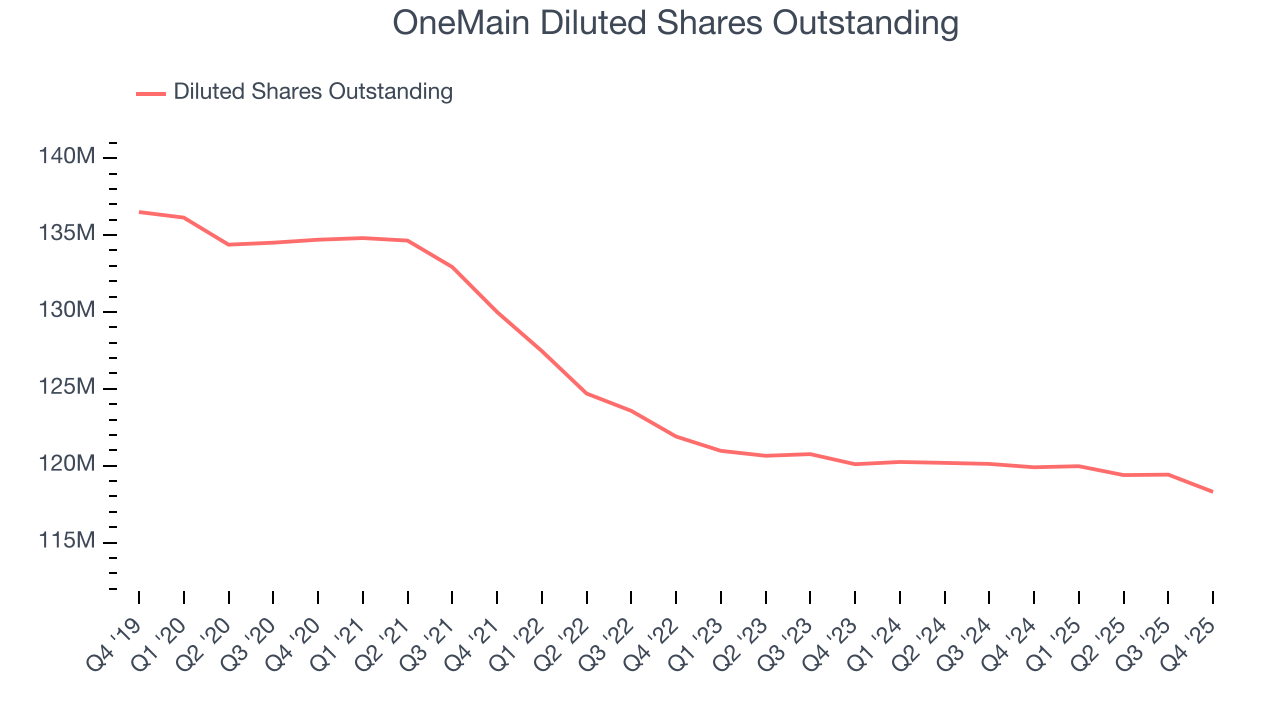

We can take a deeper look into OneMain’s earnings to better understand the drivers of its performance. A two-year view shows that OneMain has repurchased its stock, shrinking its share count by 1.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, OneMain reported EPS of $1.72, up from $1.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects OneMain’s full-year EPS of $6.57 to grow 17.7%.

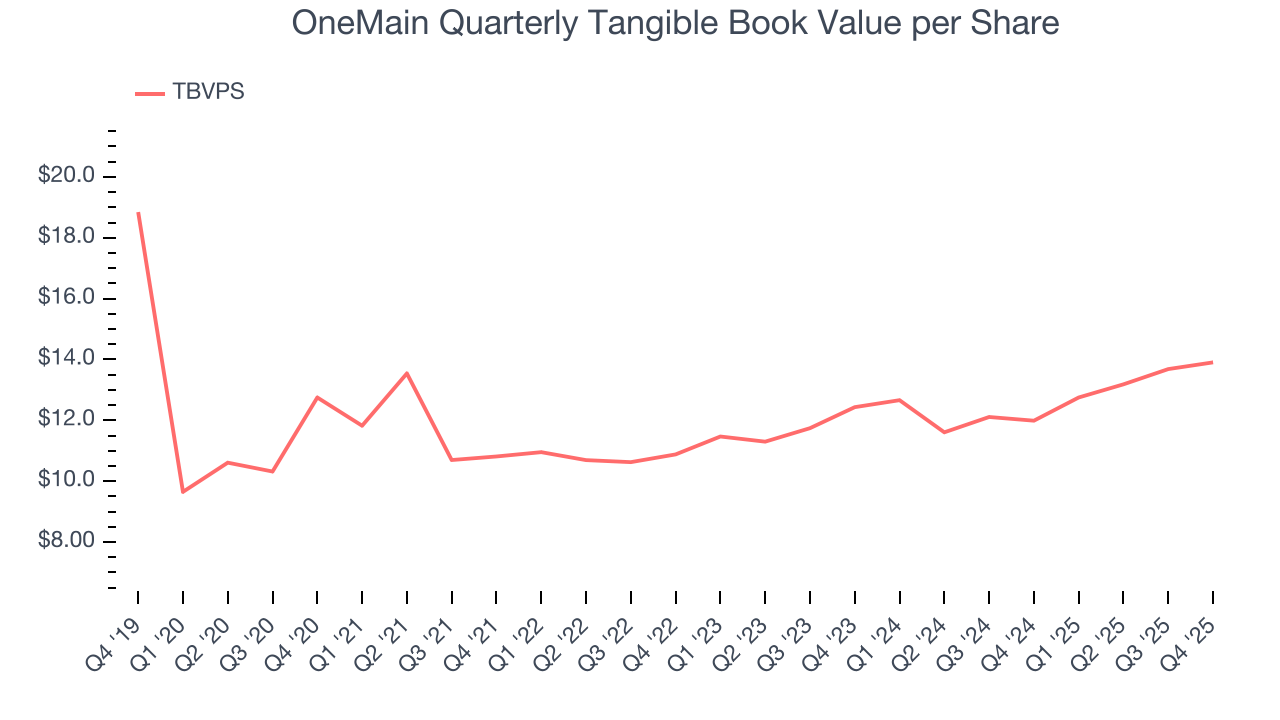

8. Tangible Book Value Per Share (TBVPS)

Financial institutions with multiple business lines manage complex balance sheets that span various financial activities. Market valuations reflect this operational complexity, prioritizing balance sheet strength and sustainable book value growth across all business segments.

This explains why tangible book value per share (TBVPS) is a premier metric for the sector. TBVPS provides concrete per-share net worth that investors can trust when evaluating companies with complex, multi-faceted business models. On the other hand, EPS is often distorted by the diverse nature of operations, mergers, and various accounting treatments across different business units. Book value provides clearer performance insights.

OneMain’s TBVPS grew at a sluggish 1.7% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 5.8% annually over the last two years from $12.43 to $13.91 per share.

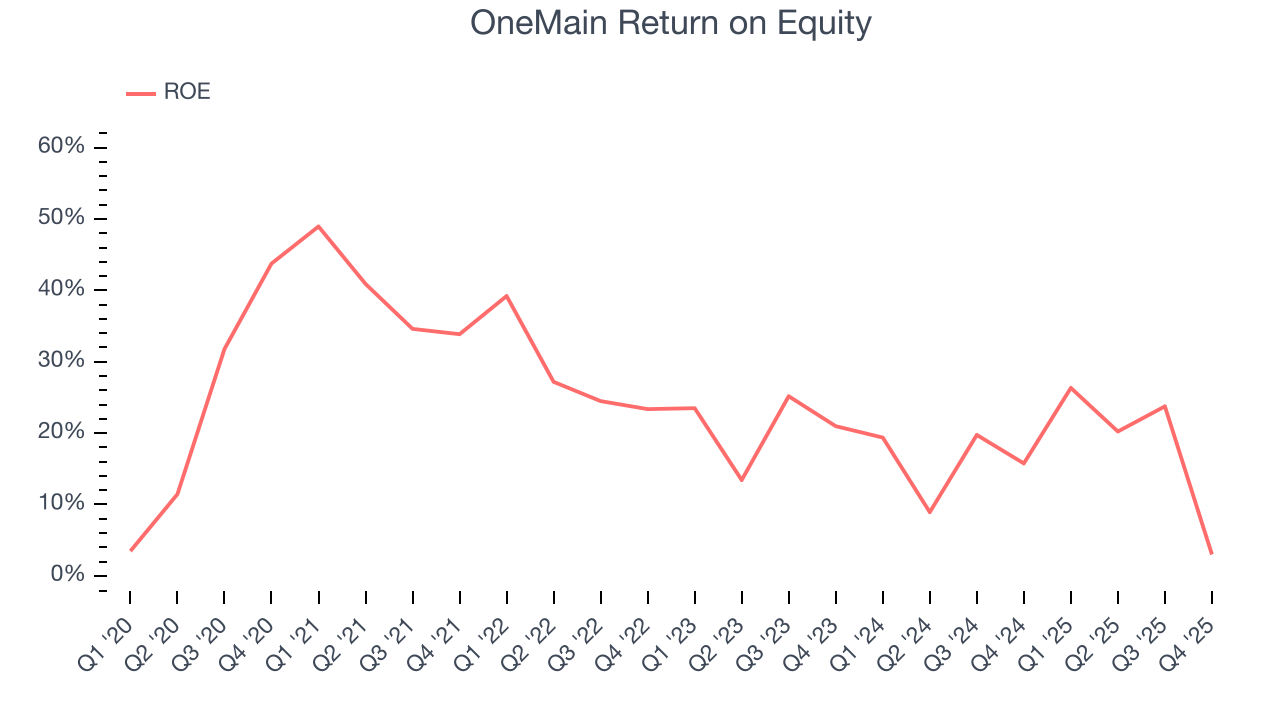

9. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, OneMain has averaged an ROE of 24.6%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for OneMain.

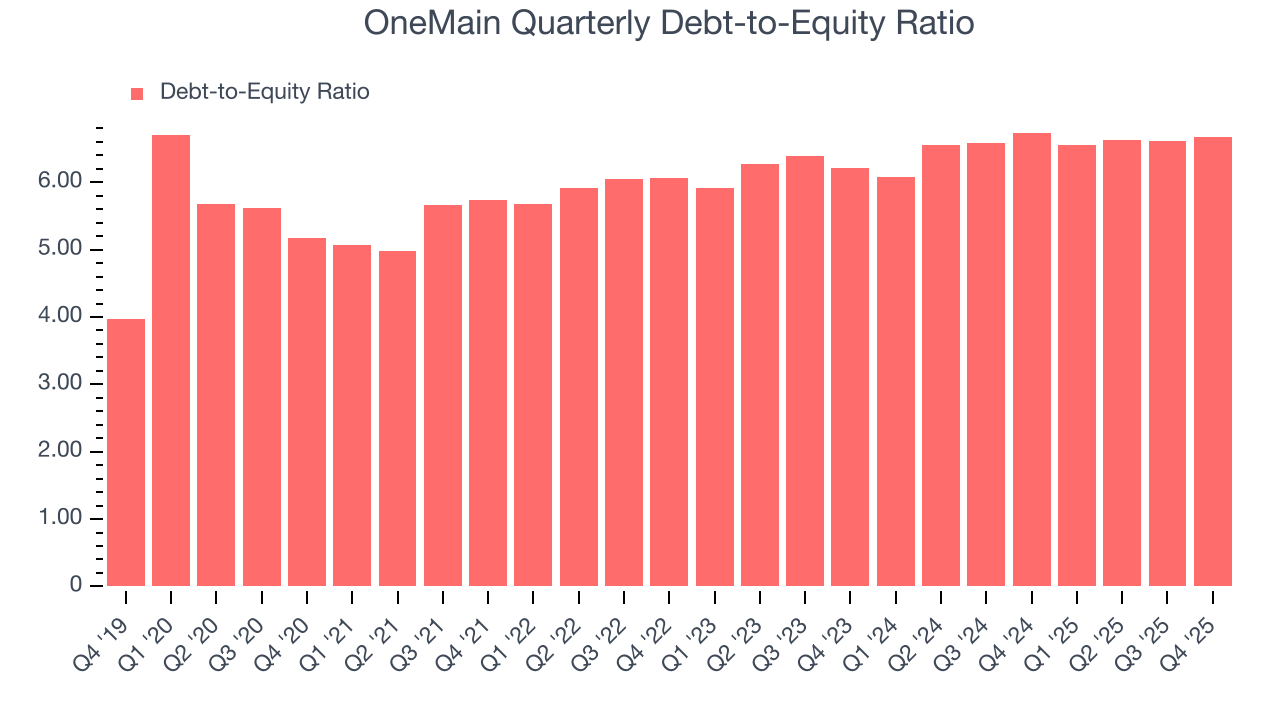

10. Balance Sheet Risk

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

OneMain currently has $22.69 billion of debt and $3.4 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 6.6×. We think this is dangerous - for a financials business, anything above 3.5× raises red flags.

11. Key Takeaways from OneMain’s Q4 Results

It was good to see OneMain beat analysts’ EPS expectations this quarter. We were also happy its net interest income narrowly outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 2.5% to $64.76 immediately after reporting.

12. Is Now The Time To Buy OneMain?

Updated: March 23, 2026 at 12:52 AM EDT

Before investing in or passing on OneMain, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

OneMain isn’t a terrible business, but it doesn’t pass our quality test. To begin with, its revenue growth was uninspiring over the last five years. While its stellar ROE suggests it has been a well-run company historically, the downside is its declining pre-tax profit margin shows the business has become less efficient. On top of that, its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders.

OneMain’s P/E ratio based on the next 12 months is 6.8x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $70.71 on the company (compared to the current share price of $51.93).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.