Offerpad (OPAD)

Offerpad is up against the odds. Its shrinking sales suggest demand is waning and its lousy free cash flow generation doesn’t do it any favors.― StockStory Analyst Team

1. News

2. Summary

Why We Think Offerpad Will Underperform

Known for giving homeowners cash offers within 24 hours, Offerpad (NYSE:OPAD) operates a tech-enabled platform specializing in direct home buying and selling solutions.

- Annual sales declines of 11.8% for the past five years show its products and services struggled to connect with the market

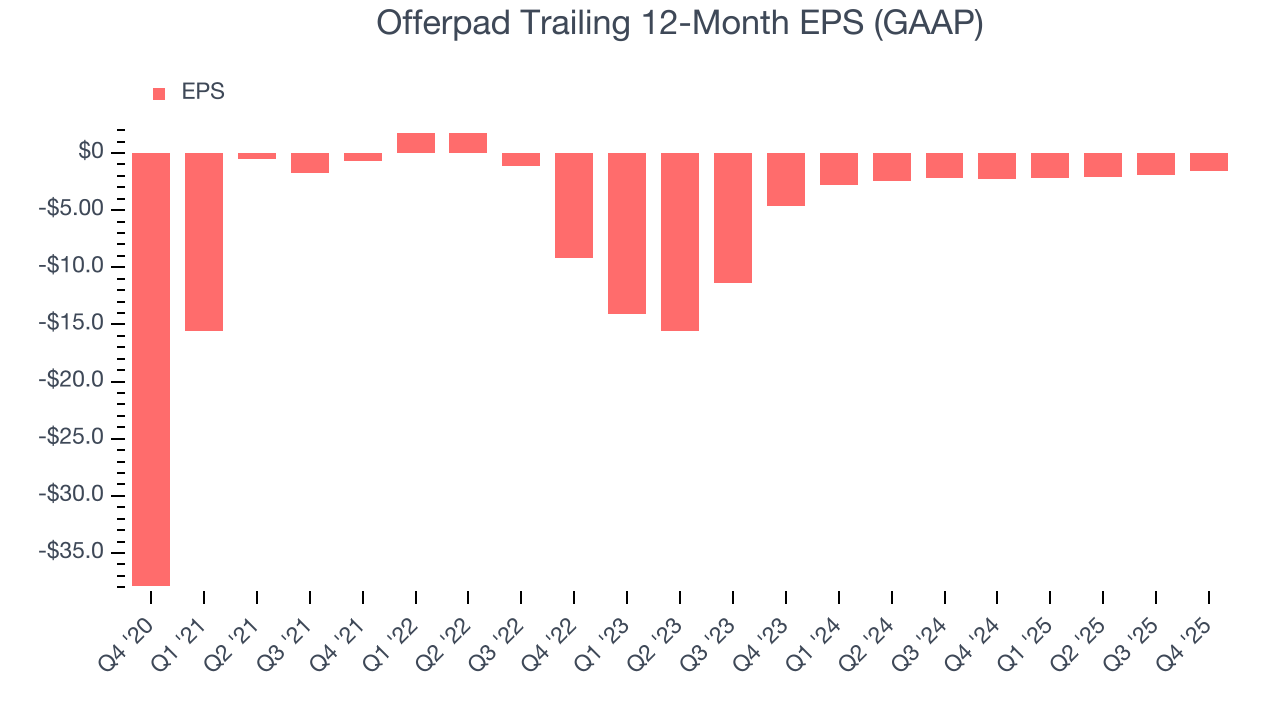

- Historically negative EPS raises concerns for risk-averse investors and makes its earnings potential harder to gauge

- EBITDA losses may force it to accept punitive lending terms or high-cost debt

Offerpad’s quality doesn’t meet our bar. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Offerpad

Offerpad is trading at $0.78 per share, or 0.1x forward price-to-sales. The market typically values companies like Offerpad based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

We’d rather pay up for companies with elite fundamentals than get a bargain on poor ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Offerpad (OPAD) Research Report: Q4 CY2025 Update

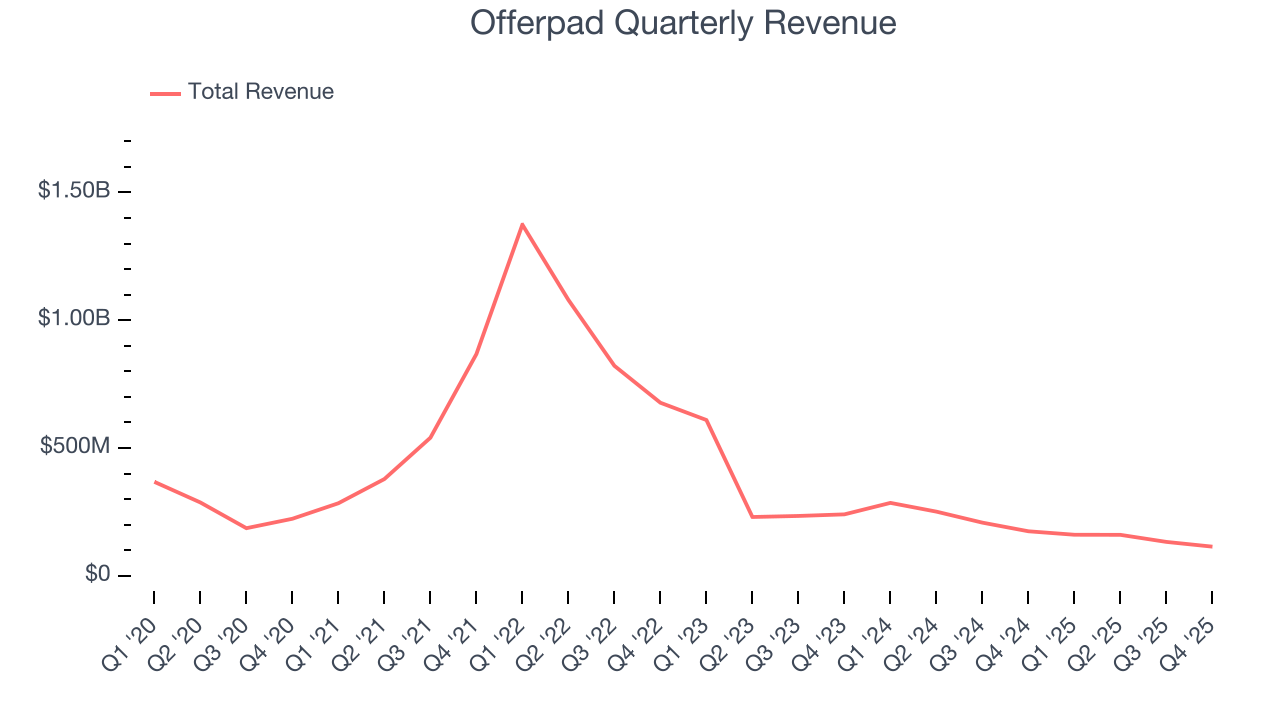

Technology real estate company Offerpad (NYSE:OPAD) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 34.5% year on year to $114.1 million. On the other hand, next quarter’s revenue guidance of $82.5 million was less impressive, coming in 40.3% below analysts’ estimates. Its GAAP loss of $0.24 per share was 12.5% above analysts’ consensus estimates.

Offerpad (OPAD) Q4 CY2025 Highlights:

- Revenue: $114.1 million vs analyst estimates of $113.6 million (34.5% year-on-year decline, in line)

- EPS (GAAP): -$0.24 vs analyst estimates of -$0.27 (12.5% beat)

- Adjusted EBITDA: -$6.9 million (-6% margin, 39.9% year-on-year growth)

- Revenue Guidance for Q1 CY2026 is $82.5 million at the midpoint, below analyst estimates of $138.1 million

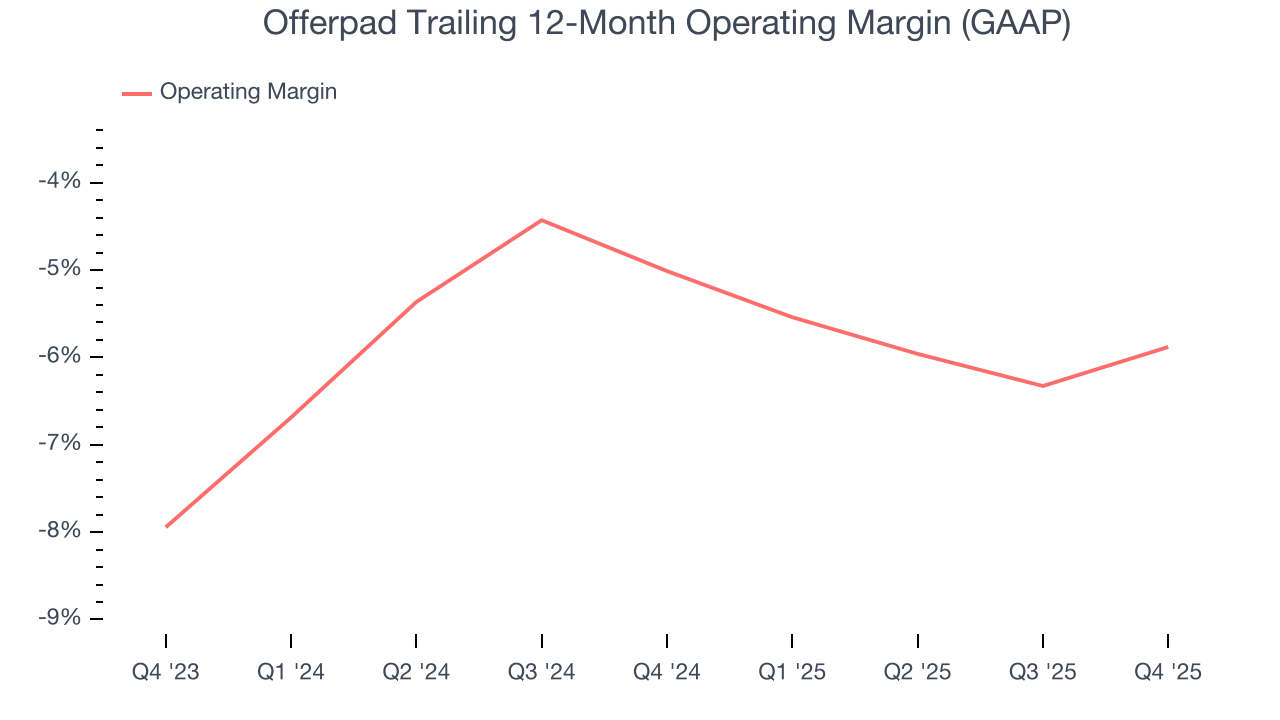

- Operating Margin: -6.4%, up from -7.8% in the same quarter last year

- Free Cash Flow Margin: 44.3%, up from 16.7% in the same quarter last year

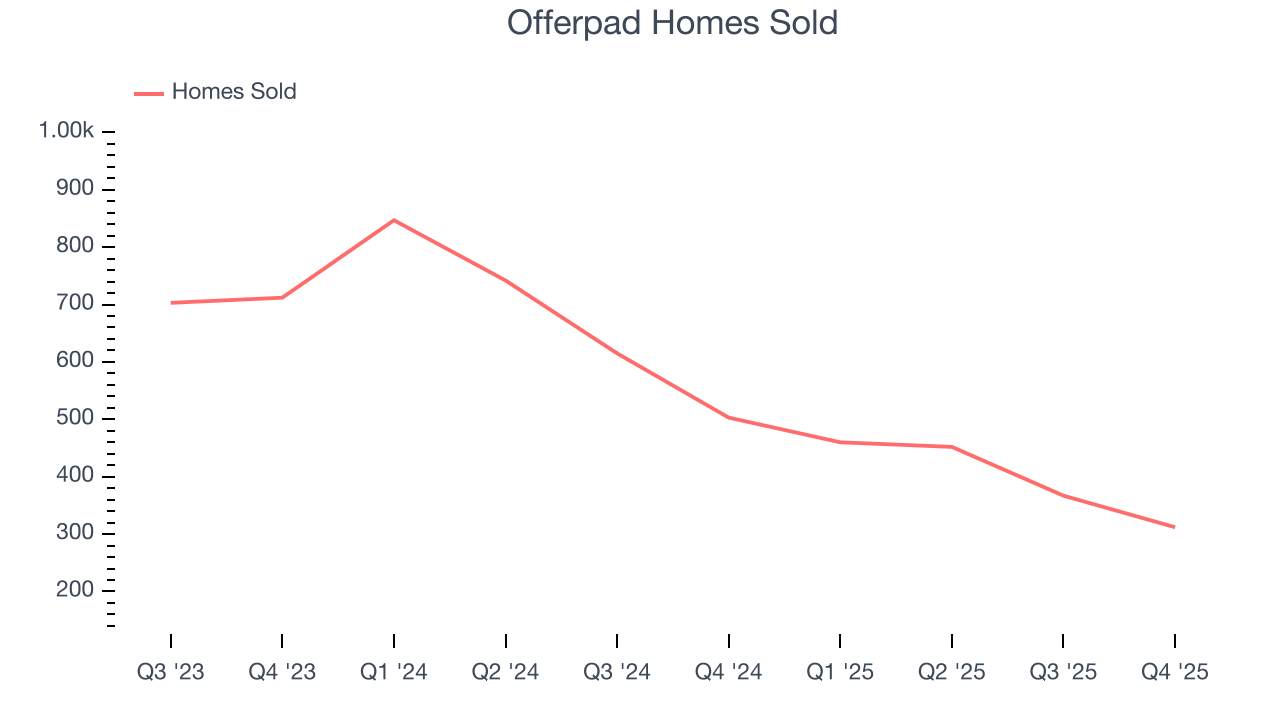

- Homes Sold: 312, down 191 year on year

- Market Capitalization: $38.71 million

Company Overview

Known for giving homeowners cash offers within 24 hours, Offerpad (NYSE:OPAD) operates a tech-enabled platform specializing in direct home buying and selling solutions.

Offerpad's core service revolves around its home buying model, where homeowners looking to sell can receive an instant cash offer on their property through Offerpad's website. This approach streamlines the traditional home selling process, offering a quick alternative to the conventional real estate market. After purchasing homes, Offerpad renovates them for resale, revitalizing properties and providing quality homes for future buyers.

A key aspect of Offerpad's business model is its use of technology. The company utilizes algorithms and data analytics to assess property values accurately and make competitive offers. This tech-driven approach enables Offerpad to operate efficiently and scale its services across various markets.

Offerpad's services extend beyond instant home buying. The company also provides traditional listing services for sellers who prefer to sell their homes on the open market. These services include home improvement advances, professional staging and listing, and a team of real estate experts to guide sellers through the process.

In addition to buying and selling homes, Offerpad has ventured into providing ancillary services related to real estate transactions. These include financing solutions through Offerpad Home Loans and other customer-centric services that aim to make the home buying and selling experience as seamless as possible.

4. Consumer Discretionary - Real Estate Services

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Real estate services companies provide brokerage, property management, appraisal, and advisory services, earning transaction-based commissions and recurring management fees. Tailwinds include long-term housing demand driven by demographic growth, technology platforms that expand market access, and commercial real estate complexity that sustains advisory needs. Headwinds are pronounced: rising interest rates directly suppress transaction volumes by reducing housing affordability and commercial deal activity. Commission-rate compression, driven by discount brokerages and regulatory changes, erodes per-transaction revenue. The industry is highly cyclical, with revenue swings amplified by leverage. PropTech (property technology) disruptors threaten traditional intermediary models.

Offerpad's primary competitors include Zillow (NASDAQ:ZG), Opendoor (NASDAQ:OPEN), Redfin (NASDAQ:RDFN), and eXp World (NASDAQ:EXPI).

5. Revenue Growth

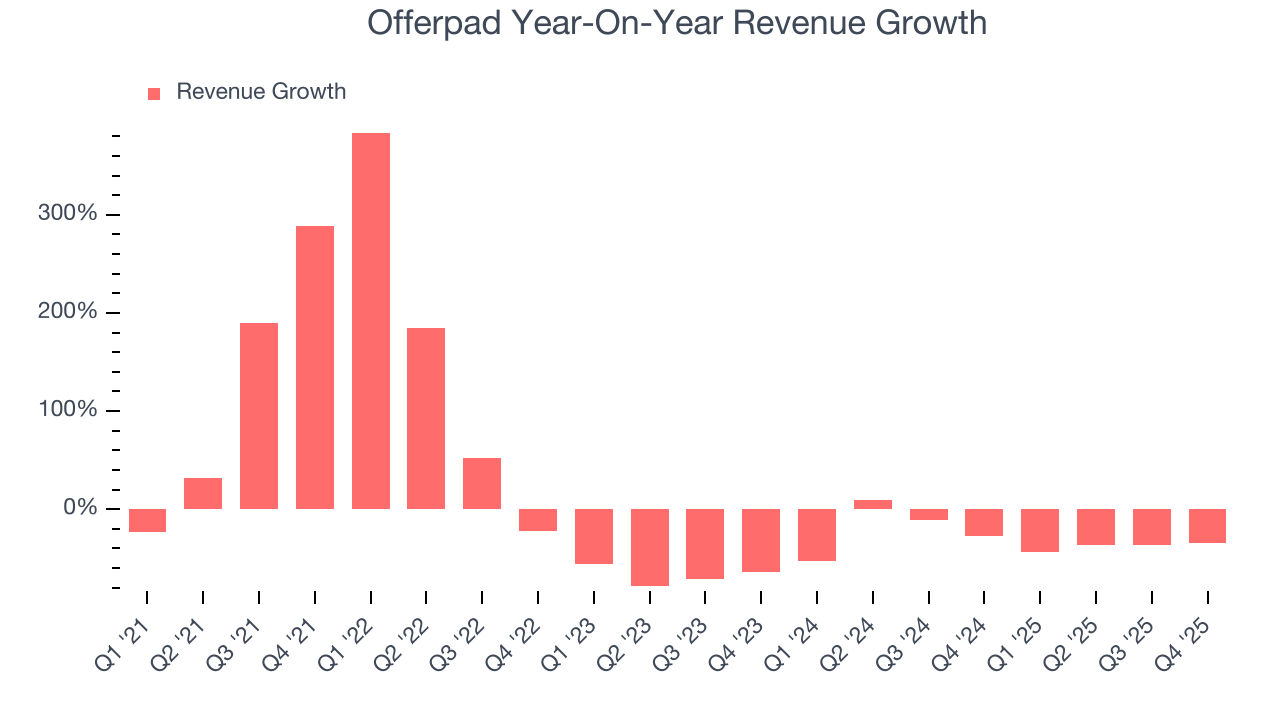

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Offerpad’s demand was weak over the last five years as its sales fell at a 11.8% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Offerpad’s recent performance shows its demand remained suppressed as its revenue has declined by 34.3% annually over the last two years.

Offerpad also discloses its number of homes sold and homes purchased, which clocked in at 312 and 110 in the latest quarter. Over the last two years, Offerpad’s homes sold averaged 34.2% year-on-year declines while its homes purchased averaged 53.4% year-on-year declines.

This quarter, Offerpad reported a rather uninspiring 34.5% year-on-year revenue decline to $114.1 million of revenue, in line with Wall Street’s estimates. Company management is currently guiding for a 48.7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

6. Operating Margin

Offerpad’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging negative 5.3% over the last two years. Unprofitable consumer discretionary companies that fail to improve their losses or grow sales rapidly deserve extra scrutiny. For the time being, it’s unclear if Offerpad’s business model is sustainable.

In Q4, Offerpad generated a negative 6.4% operating margin. The company's consistent lack of profits raise a flag.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Offerpad’s full-year earnings are still negative, it reduced its losses and improved its EPS by 47.2% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, Offerpad reported EPS of negative $0.24, up from negative $0.63 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Offerpad to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.55 will advance to negative $0.53.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

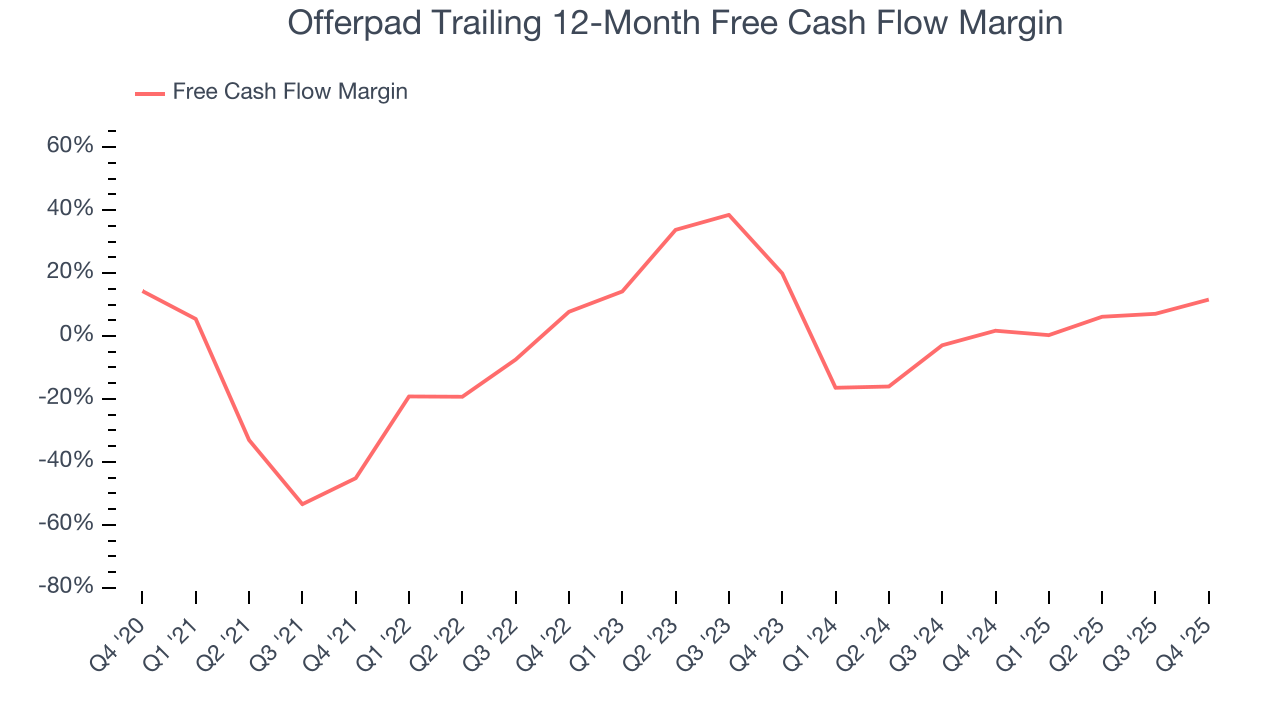

Offerpad has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.5%, lousy for a consumer discretionary business.

Offerpad’s free cash flow clocked in at $50.5 million in Q4, equivalent to a 44.3% margin. This result was good as its margin was 27.6 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts predict Offerpad will flip from cash-producing to cash-burning. Their consensus estimates imply its free cash flow margin of 11.6% for the last 12 months will decrease to negative 2.1%.

9. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

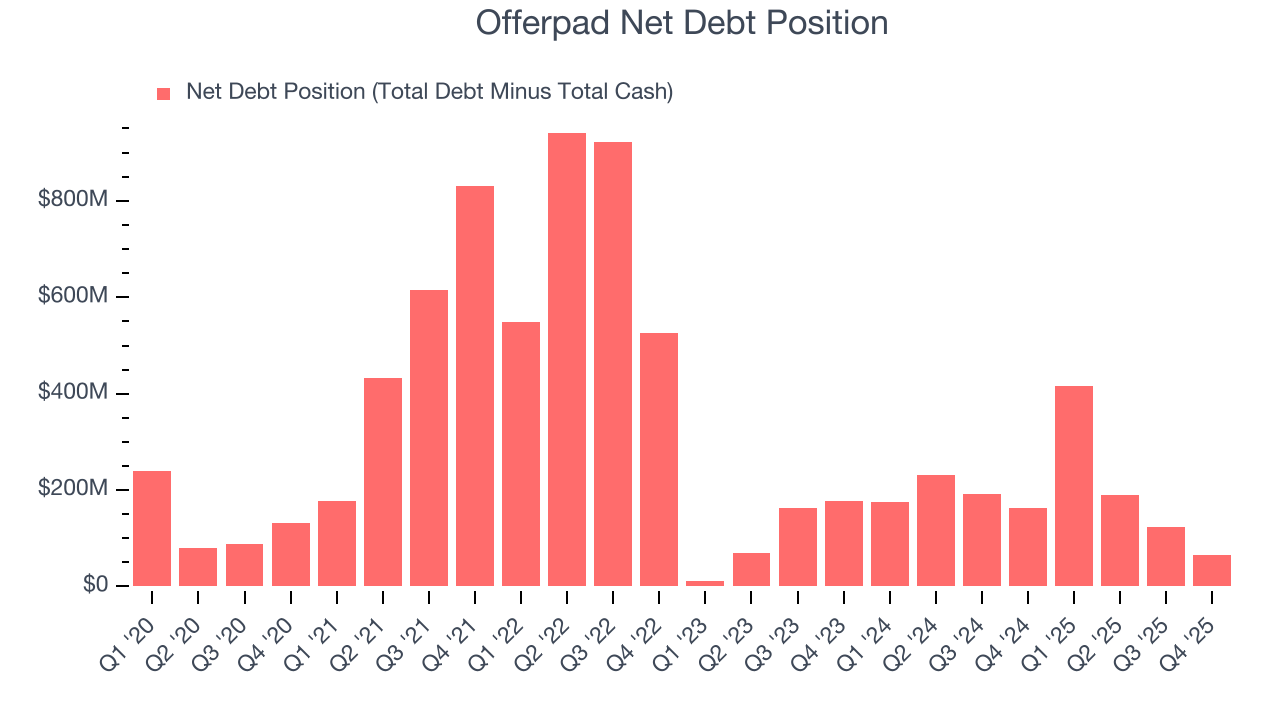

Offerpad posted negative $24.09 million of EBITDA over the last 12 months, and its $92.73 million of debt exceeds the $28.17 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Offerpad if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Offerpad can improve its profitability and remain cautious until then.

10. Key Takeaways from Offerpad’s Q4 Results

It was good to see Offerpad beat analysts’ EPS expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 4.9% to $0.79 immediately following the results.

11. Is Now The Time To Buy Offerpad?

Updated: February 27, 2026 at 10:39 PM EST

Before making an investment decision, investors should account for Offerpad’s business fundamentals and valuation in addition to what happened in the latest quarter.

We see the value of companies helping consumers, but in the case of Offerpad, we’re out. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its number of homes sold has disappointed. On top of that, its Forecasted free cash flow margin suggests the company will ramp up its investments next year.

Offerpad’s forward price-to-sales ratio is 0.1x. The market typically values companies like Offerpad based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $1.75 on the company (compared to the current share price of $0.78).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.