Ralph Lauren (RL)

Ralph Lauren faces an uphill battle. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Ralph Lauren Will Underperform

Originally founded as a necktie company, Ralph Lauren (NYSE:RL) is an iconic American fashion brand known for its classic and sophisticated style.

- Annual revenue growth of 12.3% over the last five years was below our standards for the consumer discretionary sector

- Poor expense management has led to an operating margin that is below the industry average

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

Ralph Lauren’s quality is inadequate. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Ralph Lauren

At $327.16 per share, Ralph Lauren trades at 19x forward P/E. This multiple rich for the business quality. Not a great combination.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Ralph Lauren (RL) Research Report: Q4 CY2025 Update

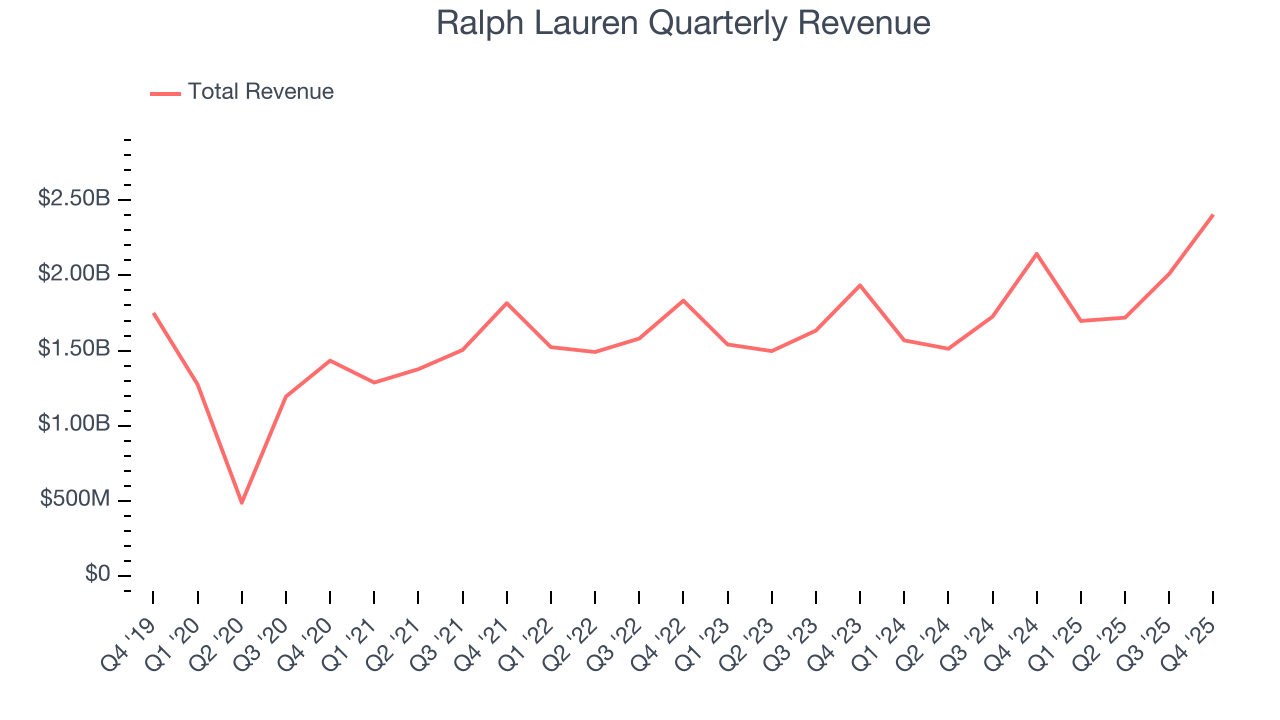

Fashion brand Ralph Lauren (NYSE:RL) announced better-than-expected revenue in Q4 CY2025, with sales up 12.2% year on year to $2.41 billion. Its non-GAAP profit of $6.22 per share was 7.1% above analysts’ consensus estimates.

Ralph Lauren (RL) Q4 CY2025 Highlights:

- Revenue: $2.41 billion vs analyst estimates of $2.32 billion (12.2% year-on-year growth, 3.7% beat)

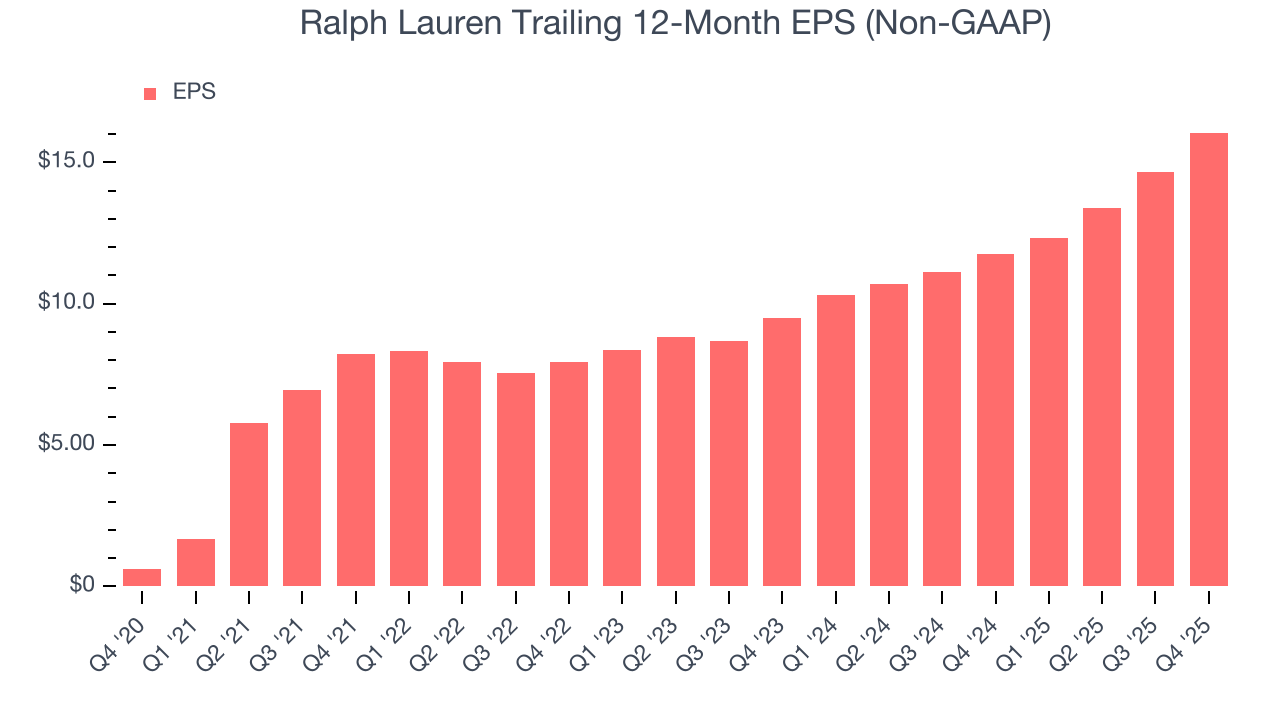

- Adjusted EPS: $6.22 vs analyst estimates of $5.81 (7.1% beat)

- Adjusted EBITDA: $530.9 million vs analyst estimates of $523.5 million (22.1% margin, 1.4% beat)

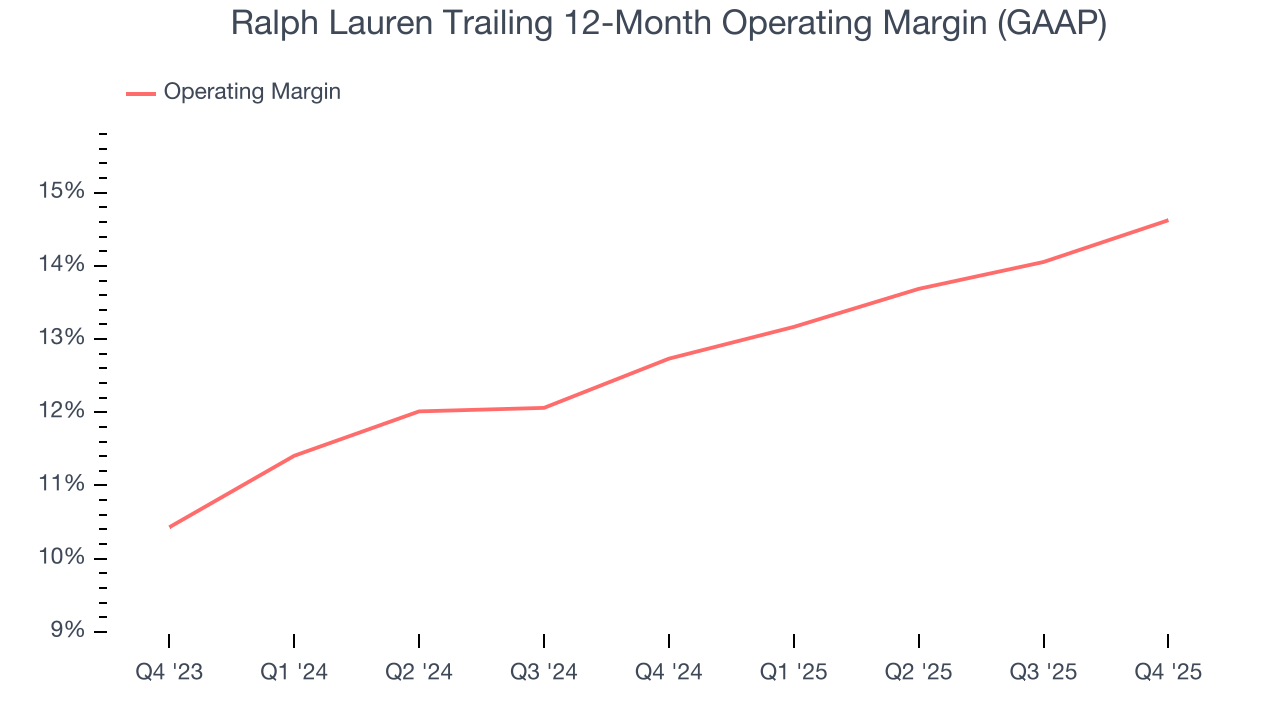

- Operating Margin: 19.6%, up from 18.2% in the same quarter last year

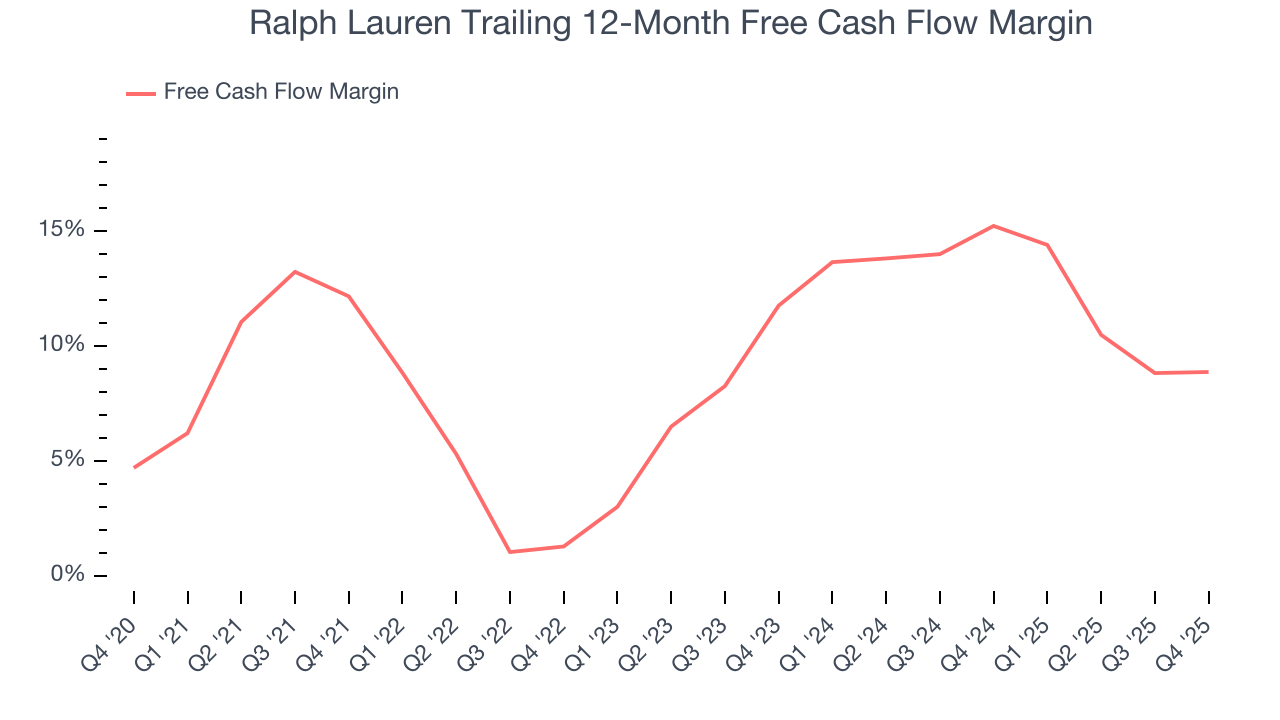

- Free Cash Flow Margin: 29.3%, down from 31.6% in the same quarter last year

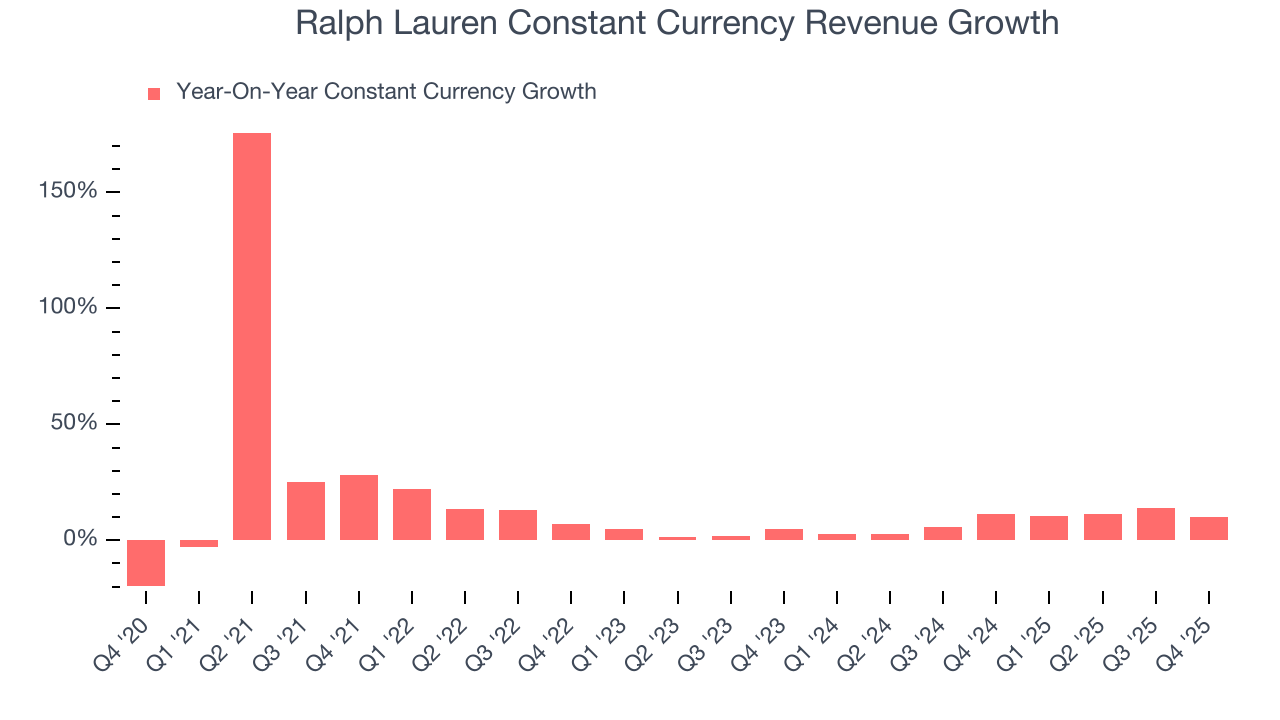

- Constant Currency Revenue rose 10% year on year (11.2% in the same quarter last year)

- Market Capitalization: $21.51 billion

Company Overview

Originally founded as a necktie company, Ralph Lauren (NYSE:RL) is an iconic American fashion brand known for its classic and sophisticated style.

Ralph Lauren is a global leader in the fashion industry with a quintessentially American style, recognizable for its classic, preppy, and sporty fashion. Featuring the iconic polo player logo, Ralph Lauren encompasses a wide range of clothing, from tailored suits to casual sportswear and accessories. Its flagship Polo Ralph Lauren brand caters to a high-end customer base, reflected in its products' premium prices.

Beyond clothing, Ralph Lauren offers an extensive portfolio of products that embody its distinct lifestyle vision. Ralph Lauren Home is known for luxurious home furnishings, bedding, and décor that mirror the same sophistication found in its fashion collections. The brand's fragrances and accessories have also been successful extensions to bring customers into the Ralph Lauren ecosystem.

Ralph Lauren products can be found in its retail stores, department stores, and online through popular e-commerce websites.

4. Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Ralph Lauren’s main domestic competitors are PVH Corp (NYSE:PVH), Tapestry (NYSE:TPR), and private company Stuart Weitzman. International competitors include Kering (OTCMKTS:PPRUY) which owns Gucci, Yves Saint Laurent, and Bottega Veneta, and LVMH (OTCMKTS:LVMUY) which owns Louis Vuitton, Dior, and Givenchy.

5. Revenue Growth

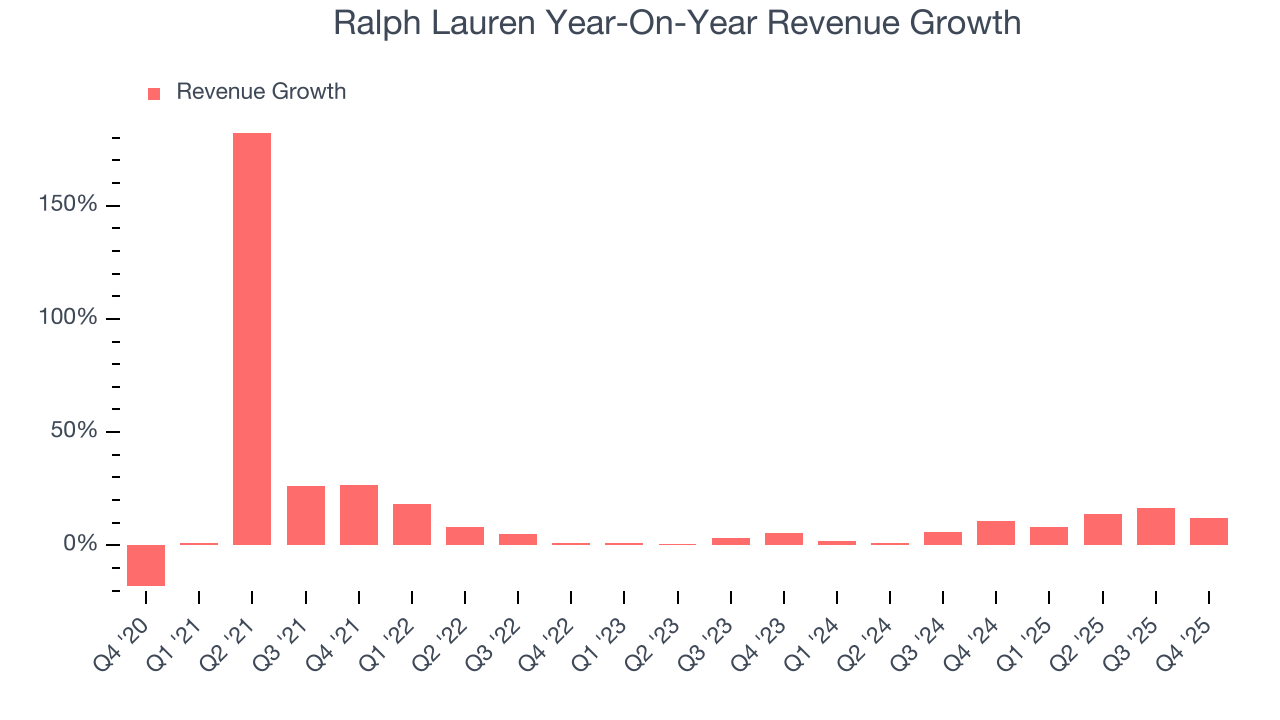

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Ralph Lauren grew its sales at a 12.3% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Ralph Lauren’s recent performance shows its demand has slowed as its annualized revenue growth of 8.9% over the last two years was below its five-year trend.

Ralph Lauren also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 8.5% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Ralph Lauren has properly hedged its foreign currency exposure.

This quarter, Ralph Lauren reported year-on-year revenue growth of 12.2%, and its $2.41 billion of revenue exceeded Wall Street’s estimates by 3.7%.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

6. Operating Margin

Ralph Lauren’s operating margin has risen over the last 12 months and averaged 13.7% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, Ralph Lauren generated an operating margin profit margin of 19.6%, up 1.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Ralph Lauren’s EPS grew at an astounding 92.3% compounded annual growth rate over the last five years, higher than its 12.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Ralph Lauren reported adjusted EPS of $6.22, up from $4.82 in the same quarter last year. This print beat analysts’ estimates by 7.1%. Over the next 12 months, Wall Street expects Ralph Lauren’s full-year EPS of $16.05 to grow 4.5%.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Ralph Lauren has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 11.9%, lousy for a consumer discretionary business.

Ralph Lauren’s free cash flow clocked in at $704 million in Q4, equivalent to a 29.3% margin. The company’s cash profitability regressed as it was 2.3 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

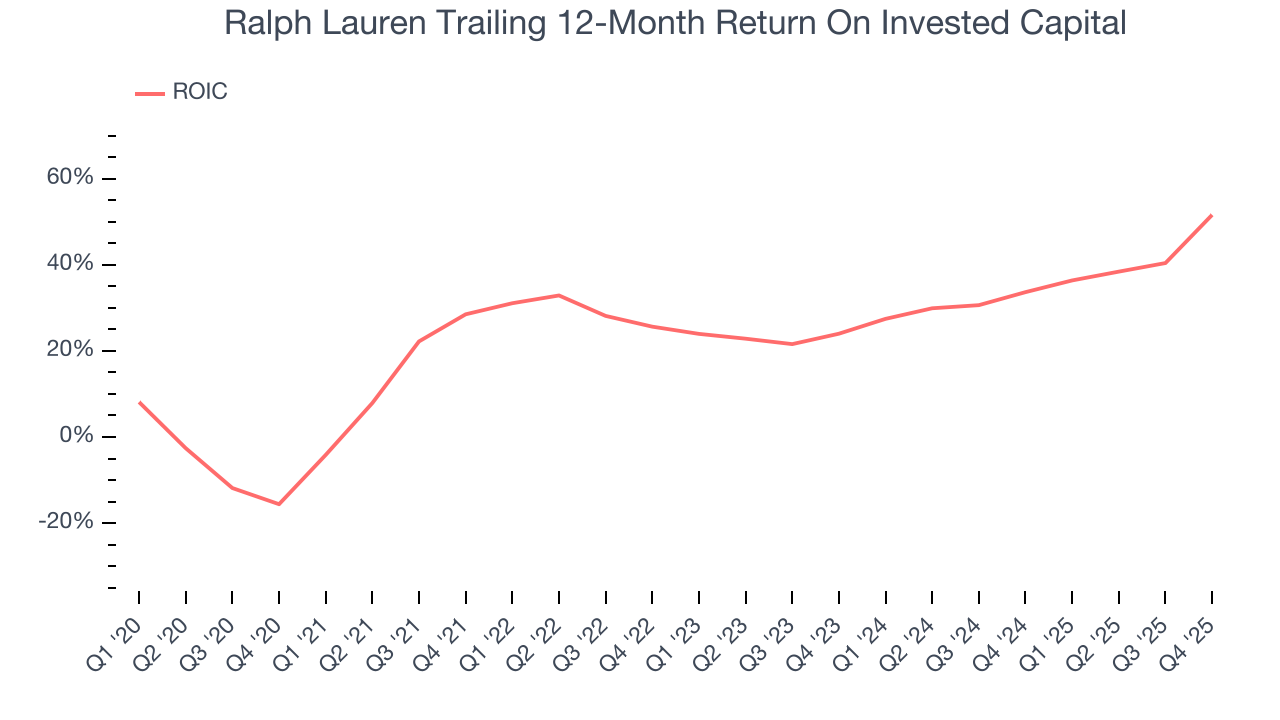

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Ralph Lauren historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 32.7%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Ralph Lauren’s ROIC has increased significantly over the last few years. This is a good sign, and we hope the company can continue improving.

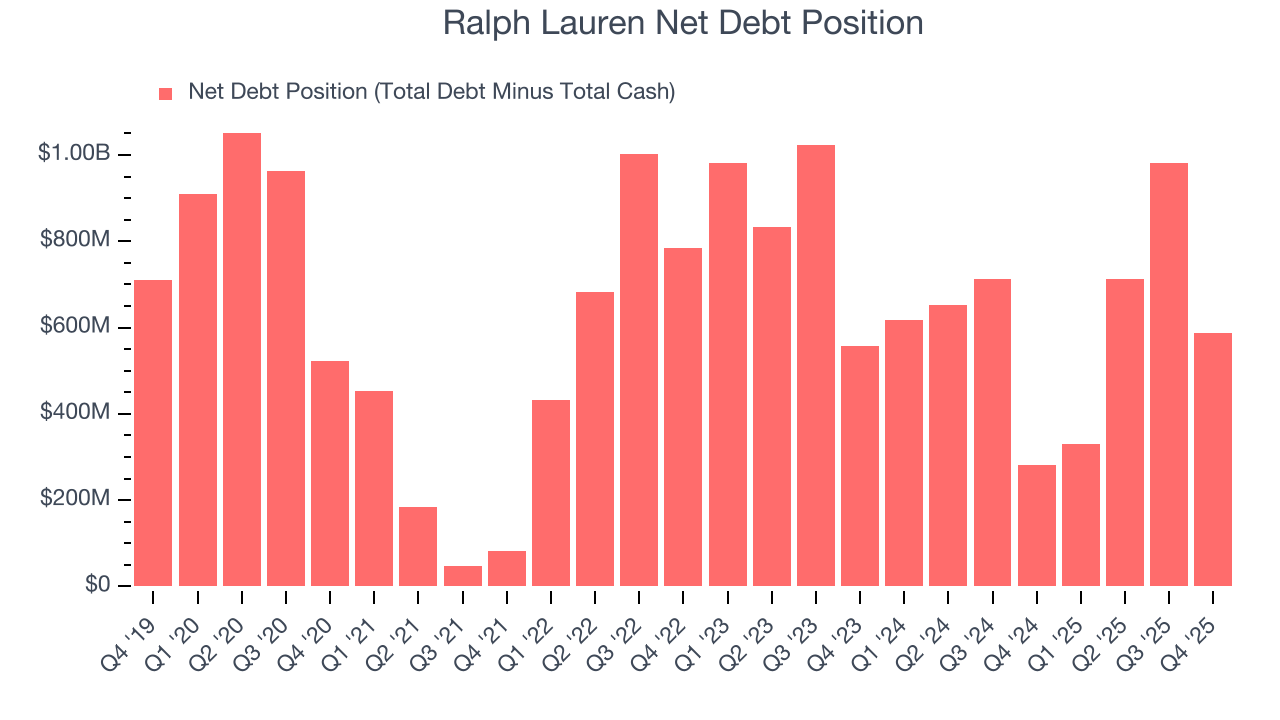

10. Balance Sheet Assessment

Ralph Lauren reported $2.25 billion of cash and $2.84 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.45 billion of EBITDA over the last 12 months, we view Ralph Lauren’s 0.4× net-debt-to-EBITDA ratio as safe. We also see its $11.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Ralph Lauren’s Q4 Results

We were impressed by how significantly Ralph Lauren blew past analysts’ constant currency revenue expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 7.6% to $327.87 immediately following the results.

12. Is Now The Time To Buy Ralph Lauren?

Updated: March 28, 2026 at 11:10 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Ralph Lauren.

We cheer for all companies serving everyday consumers, but in the case of Ralph Lauren, we’ll be cheering from the sidelines. While its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its constant currency sales performance has disappointed. On top of that, its projected EPS for the next year is lacking.

Ralph Lauren’s P/E ratio based on the next 12 months is 19x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $408.14 on the company (compared to the current share price of $327.16).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.