Boston Beer (SAM)

We’re cautious of Boston Beer. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Boston Beer Will Underperform

Known for its flavorful beverages challenging the status quo, Boston Beer (NYSE:SAM) is a pioneer in craft brewing and a symbol of American innovation in the alcoholic beverage industry.

- Products aren't resonating with the market as its revenue declined by 2% annually over the last three years

- Estimated sales for the next 12 months are flat and imply a softer demand environment

- A silver lining is that its unique products and pricing power are reflected in its top-tier gross margin of 46.4%

Boston Beer doesn’t satisfy our quality benchmarks. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Boston Beer

At $224.90 per share, Boston Beer trades at 23x forward P/E. Not only is Boston Beer’s multiple richer than most consumer staples peers, but it’s also expensive for its revenue characteristics.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Boston Beer (SAM) Research Report: Q4 CY2025 Update

Beer company Boston Beer (NYSE:SAM) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 4.1% year on year to $385.7 million. Its GAAP loss of $2.12 per share was 15.3% above analysts’ consensus estimates.

Boston Beer (SAM) Q4 CY2025 Highlights:

- Revenue: $385.7 million vs analyst estimates of $386.3 million (4.1% year-on-year decline, in line)

- EPS (GAAP): -$2.12 vs analyst estimates of -$2.50 (15.3% beat)

- Operating Margin: -8.6%, up from -13.9% in the same quarter last year

- Market Capitalization: $2.34 billion

Company Overview

Known for its flavorful beverages challenging the status quo, Boston Beer (NYSE:SAM) is a pioneer in craft brewing and a symbol of American innovation in the alcoholic beverage industry.

The company was founded in 1984 by Jim Koch in Boston, Massachusetts. Koch had a vision to reintroduce traditional brewing techniques and artisanal flavors to American consumers, catalyzing a craft beer revolution.

In this context, it’s quite fitting that Boston Beer’s first brand was named after Samuel Adams, an American Founding Father and revolutionary patriot. Samuel Adams Boston Lager is the flagship brand in Boston Beer’s portfolio, which also includes other household names like Truly Hard Seltzer and Angry Orchard hard cider.

Boston Beer’s diversity of beverage types helps it adapt to changing market dynamics and consumer demands. It also positions itself well to capitalize on trends in the beverage industry.

The company’s influence extends across the United States and select international markets. To get its products into the hands of consumers, it leverages a network of distributors and retailers. This includes partnerships with bars, restaurants, supermarkets, and liquor stores.

4. Beverages, Alcohol, and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Competitors include Anheuser-Busch Inbev (NYSE:BUD), Constellation Brands (NYSE:STZ), and Molson Coors (NYSE:TAP) along with international companies such as Asahi, Carlsberg, and Heineken.

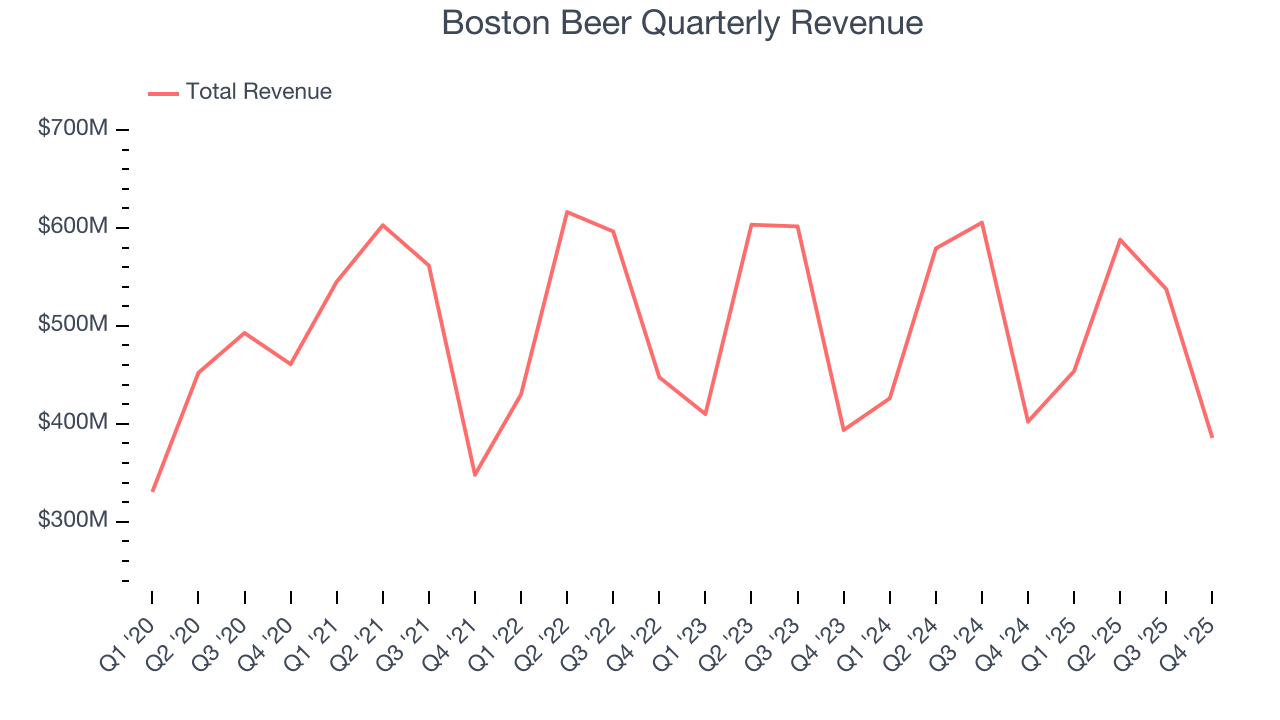

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.96 billion in revenue over the past 12 months, Boston Beer is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Boston Beer’s revenue declined by 2% per year over the last three years, a rough starting point for our analysis.

This quarter, Boston Beer reported a rather uninspiring 4.1% year-on-year revenue decline to $385.7 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection suggests its newer products will fuel better top-line performance, it is still below the sector average.

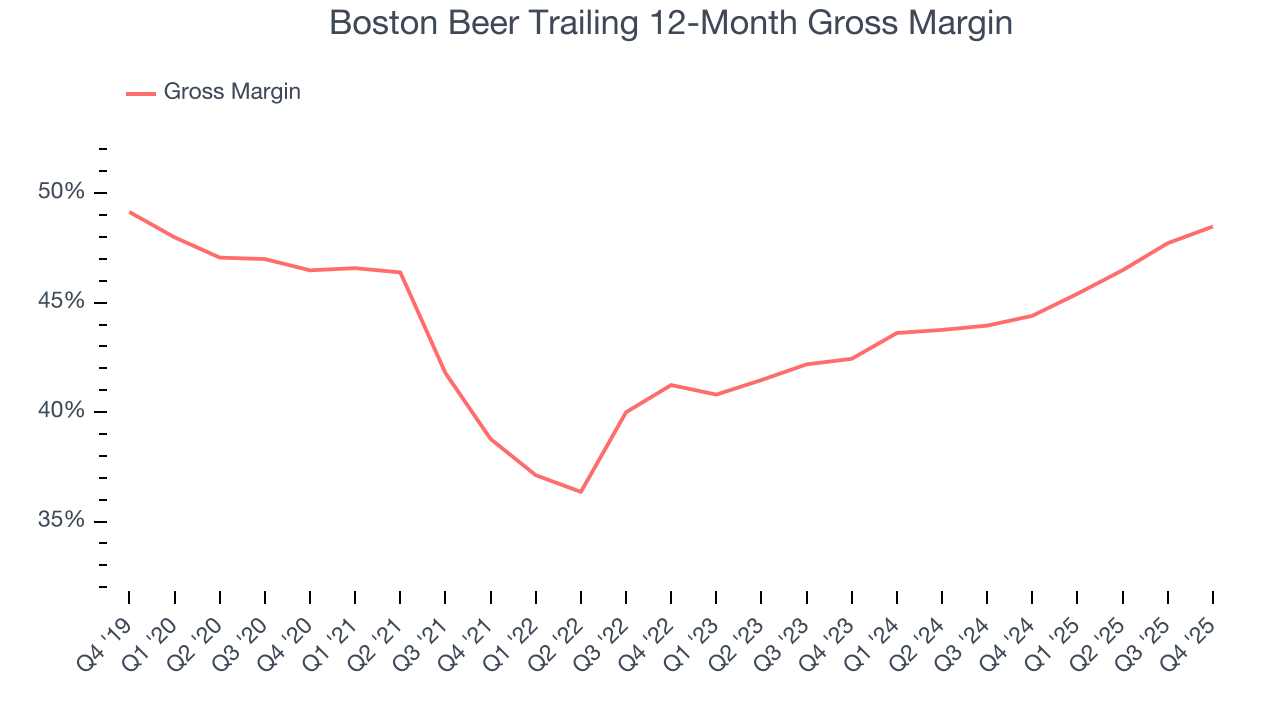

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Boston Beer has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 46.4% gross margin over the last two years. That means for every $100 in revenue, only $53.59 went towards paying for raw materials, production of goods, transportation, and distribution.

Boston Beer produced a 43.5% gross profit margin in Q4 , marking a 3.5 percentage point increase from 39.9% in the same quarter last year. Boston Beer’s full-year margin has also been trending up over the past 12 months, increasing by 4.1 percentage points. If this move continues, it could suggest better unit economics due to some combination of stable to improving pricing power and input costs (such as raw materials).

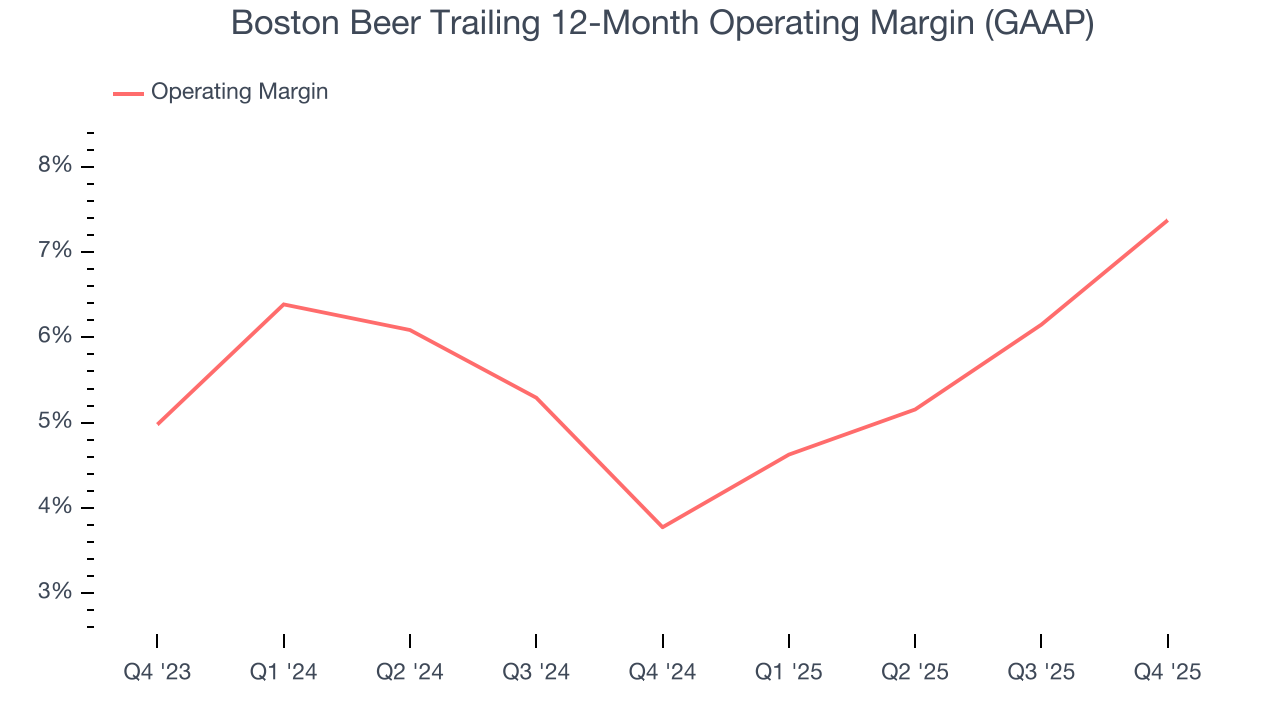

7. Operating Margin

Boston Beer was profitable over the last two years but held back by its large cost base. Its average operating margin of 5.6% was weak for a consumer staples business. This result is surprising given its high gross margin as a starting point.

On the plus side, Boston Beer’s operating margin rose by 3.6 percentage points over the last year.

This quarter, Boston Beer generated an operating margin profit margin of negative 8.6%, up 5.4 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

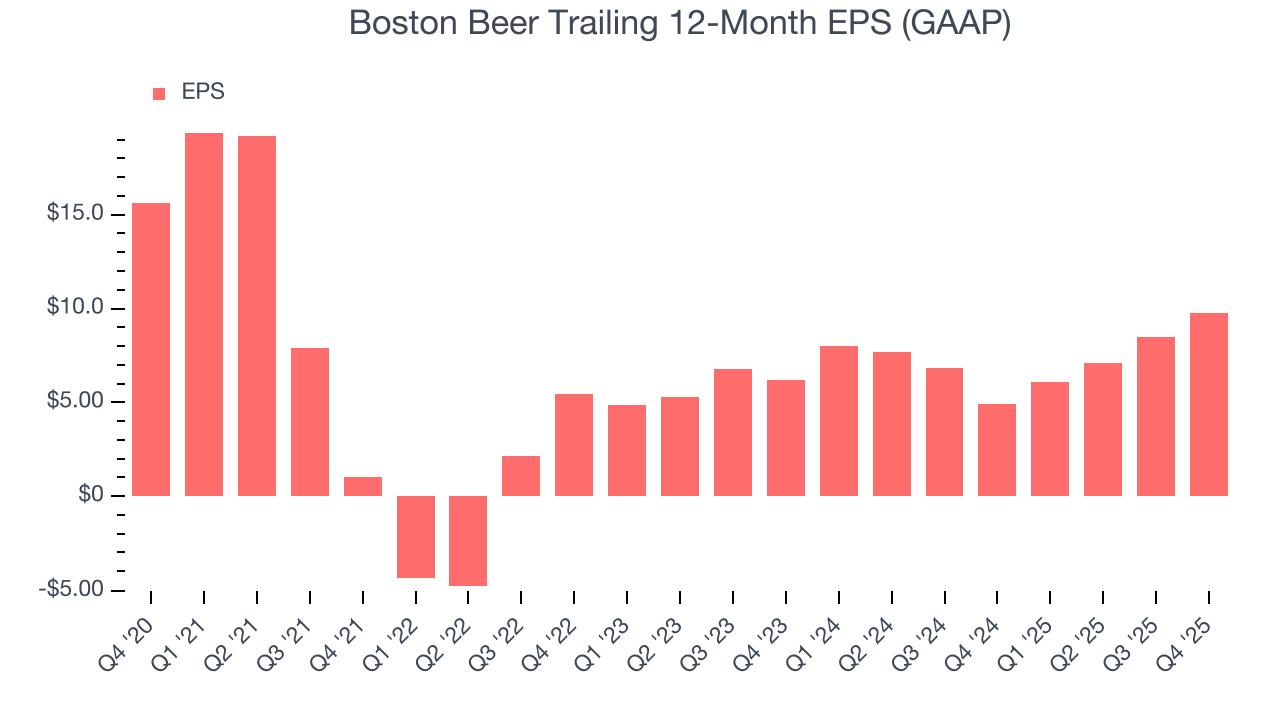

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Boston Beer’s EPS grew at a spectacular 21.5% compounded annual growth rate over the last three years, higher than its 2% annualized revenue declines. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q4, Boston Beer reported EPS of negative $2.12, up from negative $3.38 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Boston Beer’s full-year EPS of $9.77 to grow 6.6%.

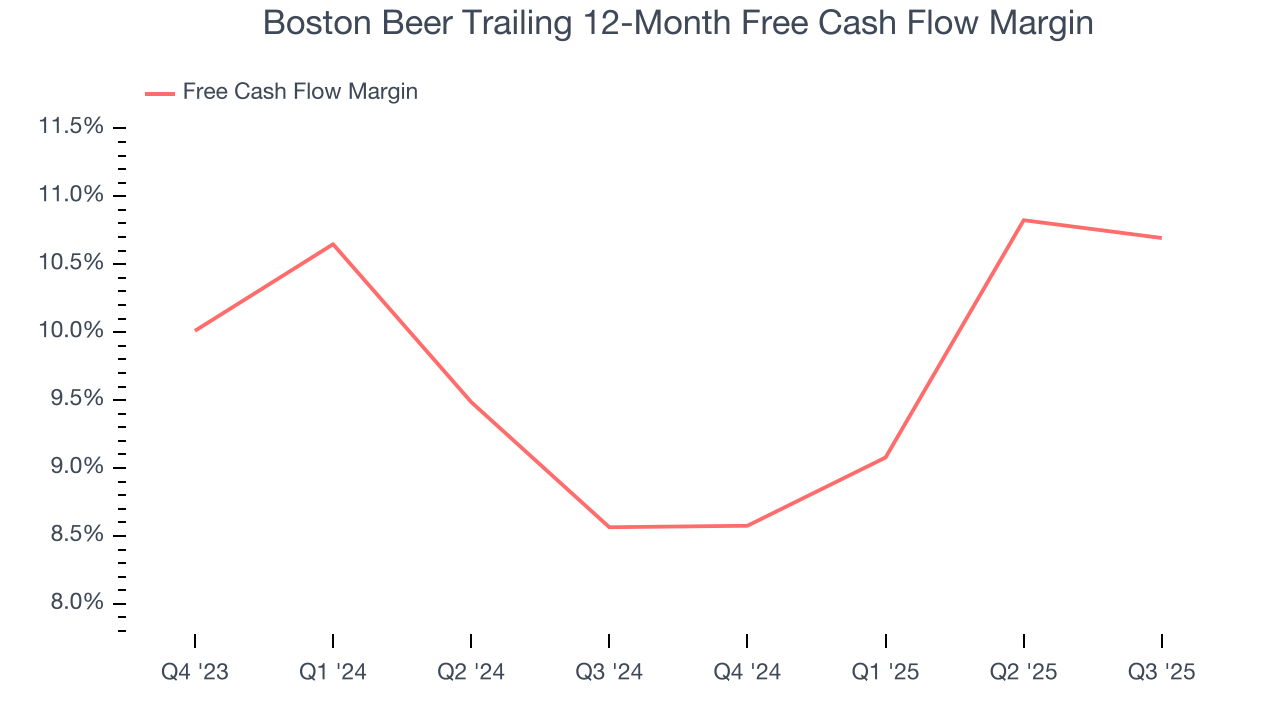

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Boston Beer has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.2% over the last two years, quite impressive for a consumer staples business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

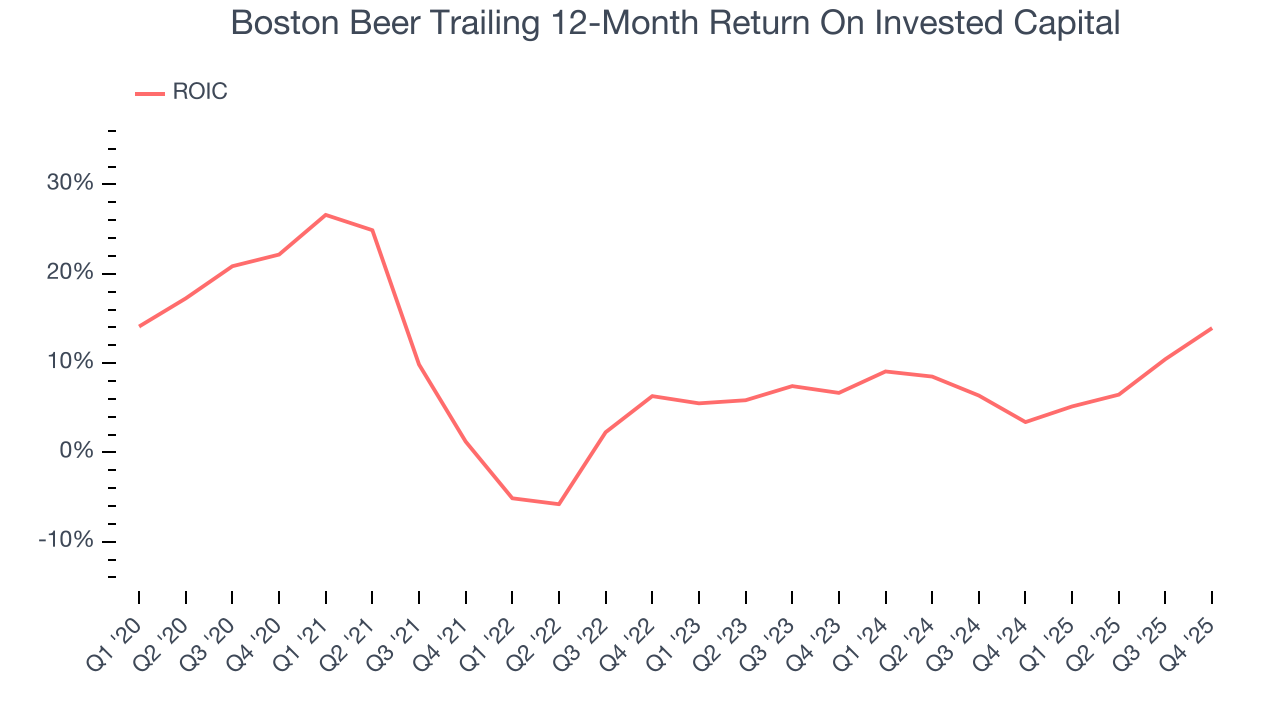

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Boston Beer historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.3%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

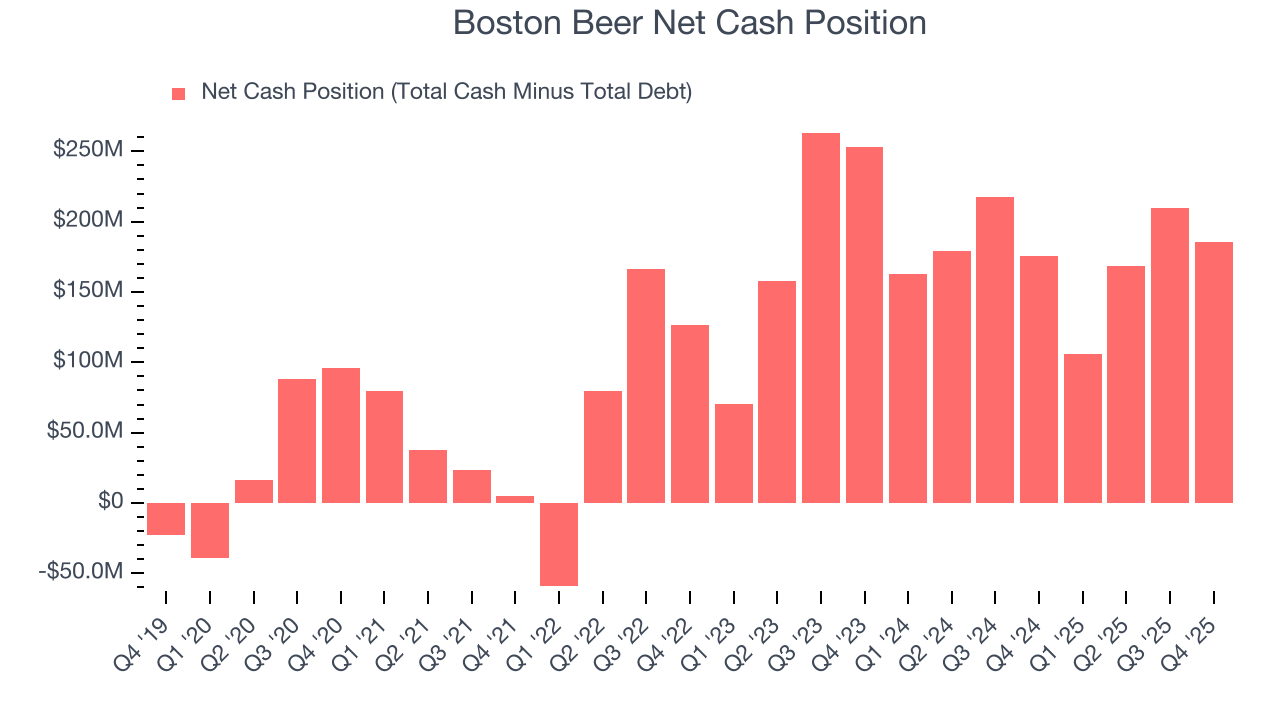

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Boston Beer is a profitable, well-capitalized company with $223.4 million of cash and $37.87 million of debt on its balance sheet. This $185.5 million net cash position is 8.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Boston Beer’s Q4 Results

We enjoyed seeing Boston Beer beat analysts’ gross margin expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $227.46 immediately after reporting.

13. Is Now The Time To Buy Boston Beer?

Updated: March 23, 2026 at 10:44 PM EDT

Before deciding whether to buy Boston Beer or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Boston Beer isn’t a terrible business, but it doesn’t pass our bar. For starters, its revenue has declined over the last three years. While its expanding operating margin shows the business has become more efficient, the downside is its projected EPS for the next year is lacking. On top of that, its brand caters to a niche market.

Boston Beer’s P/E ratio based on the next 12 months is 23x. This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $237.44 on the company (compared to the current share price of $224.90).