Select Medical (SEM)

We aren’t fans of Select Medical. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why We Think Select Medical Will Underperform

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE:SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

- Sales over the last five years were less profitable as its earnings per share fell by 9.3% annually while its revenue was flat

- Sales stagnated over the last five years and signal the need for new growth strategies

- 6× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Select Medical’s quality is inadequate. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Select Medical

Select Medical is trading at $16.25 per share, or 13.1x forward P/E. Select Medical’s multiple may seem like a great deal among healthcare peers, but we think there are valid reasons why it’s this cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Select Medical (SEM) Research Report: Q4 CY2025 Update

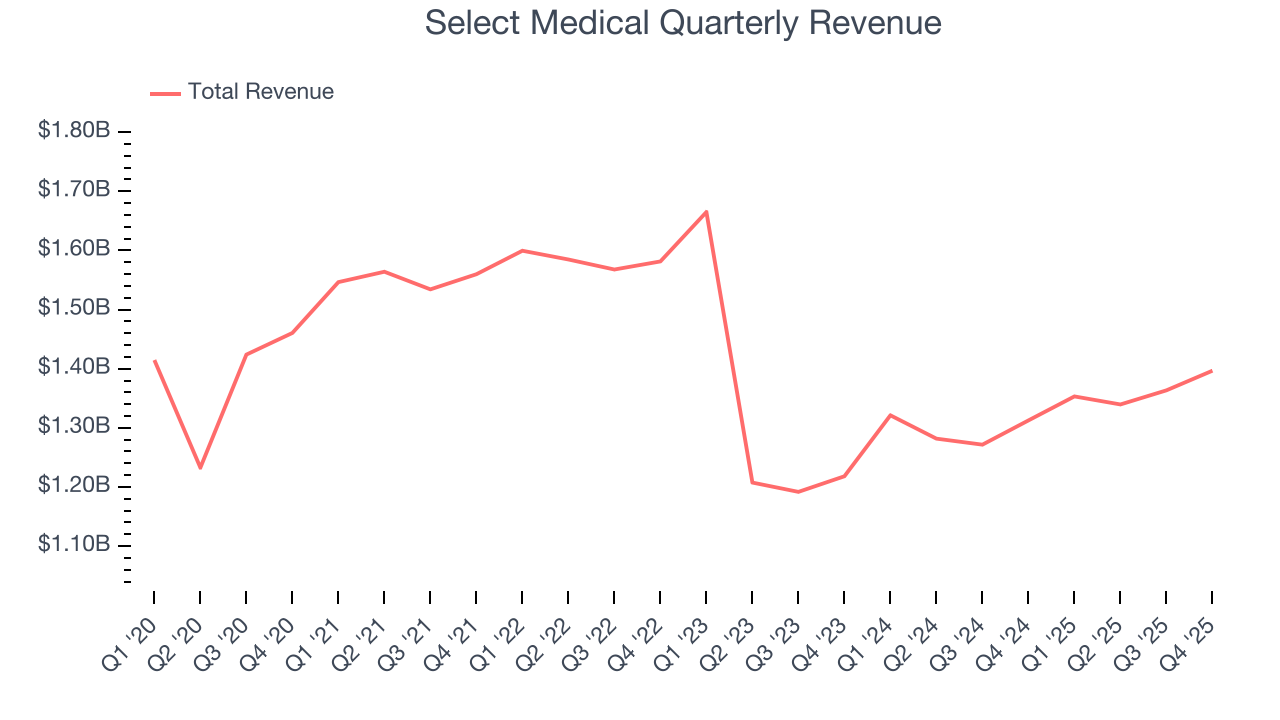

Healthcare services company Select Medical (NYSE:SEM) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 6.4% year on year to $1.40 billion. The company’s full-year revenue guidance of $5.7 billion at the midpoint came in 0.8% above analysts’ estimates. Its GAAP profit of $0.16 per share was 33.8% below analysts’ consensus estimates.

Select Medical (SEM) Q4 CY2025 Highlights:

- Revenue: $1.40 billion vs analyst estimates of $1.37 billion (6.4% year-on-year growth, 2.3% beat)

- EPS (GAAP): $0.16 vs analyst expectations of $0.24 (33.8% miss)

- Adjusted EBITDA: $104.7 million vs analyst estimates of $129.6 million (7.5% margin, 19.2% miss)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $1.27 at the midpoint, missing analyst estimates by 7.2%

- EBITDA guidance for the upcoming financial year 2026 is $530 million at the midpoint, below analyst estimates of $556.1 million

- Operating Margin: 4.6%, up from 1.6% in the same quarter last year

- Free Cash Flow Margin: 0.4%, down from 4.7% in the same quarter last year

- Sales Volumes rose 3% year on year (-4.8% in the same quarter last year)

- Market Capitalization: $2.02 billion

Company Overview

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE:SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

Select Medical's business is organized into four distinct segments, each addressing different healthcare needs. The Critical Illness Recovery Hospital segment operates facilities certified as long-term care hospitals (LTCHs), serving patients with complex medical conditions requiring extended recovery periods, typically following intensive care. These patients often have serious conditions affecting multiple organ systems, with an average stay of about a month.

The Rehabilitation Hospital segment provides comprehensive physical medicine and rehabilitation programs for patients recovering from conditions like brain and spinal cord injuries, strokes, and orthopedic issues. These inpatient facilities are certified as IRFs (Inpatient Rehabilitation Facilities) by Medicare.

Through its Outpatient Rehabilitation segment, Select Medical delivers physical, occupational, and speech therapy services at clinics typically located in medical complexes or retail settings. These facilities treat patients with musculoskeletal impairments from accidents, sports injuries, or post-surgical conditions, helping them regain functional abilities.

The Concentra segment focuses on occupational health, operating centers and onsite clinics at employer workplaces. Services include treating work-related injuries, conducting pre-employment physicals, substance abuse testing, and providing preventative care. This segment is particularly important for industries with higher workplace injury risks, such as transportation, manufacturing, and construction.

Select Medical generates revenue primarily through reimbursements from Medicare, commercial insurance, workers' compensation programs, and other healthcare payors. The company has announced plans to separate its Concentra business into a standalone public company by the end of 2024, which would create two distinct publicly traded healthcare entities.

4. Outpatient & Specialty Care

The outpatient and specialty care industry delivers targeted medical services in non-hospital settings that are often cost-effective compared to inpatient alternatives. This means that they are more desired as rising healthcare costs and ways to combat them become more and more top-of-mind. Outpatient and specialty care providers boast revenue streams that are stable due to the recurring nature of treatment for chronic conditions and long-term patient relationships. However, their reliance on government reimbursement programs like Medicare means stroke-of-the-pen risk. Additionally, scaling a network of facilities can be capital-intensive with uneven return profiles amid competition from integrated healthcare systems. Looking ahead, the industry is positioned to grow as demand for outpatient services expands, driven by aging populations, a rising prevalence of chronic diseases, and a shift toward value-based care models. Tailwinds include advancements in medical technology that support more complex procedures in outpatient settings and the increasing focus on preventive care, which can be aided by data and AI. However, headwinds such as reimbursement rate cuts, labor shortages, and the financial strain of digitization may temper growth.

Select Medical's competitors include Encompass Health Corporation (NYSE: EHC), which operates in the inpatient rehabilitation and home health segments, ScionHealth, which runs long-term acute care hospitals, and U.S. Physical Therapy (NYSE: USPH) in the outpatient rehabilitation space.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $5.45 billion in revenue over the past 12 months, Select Medical has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

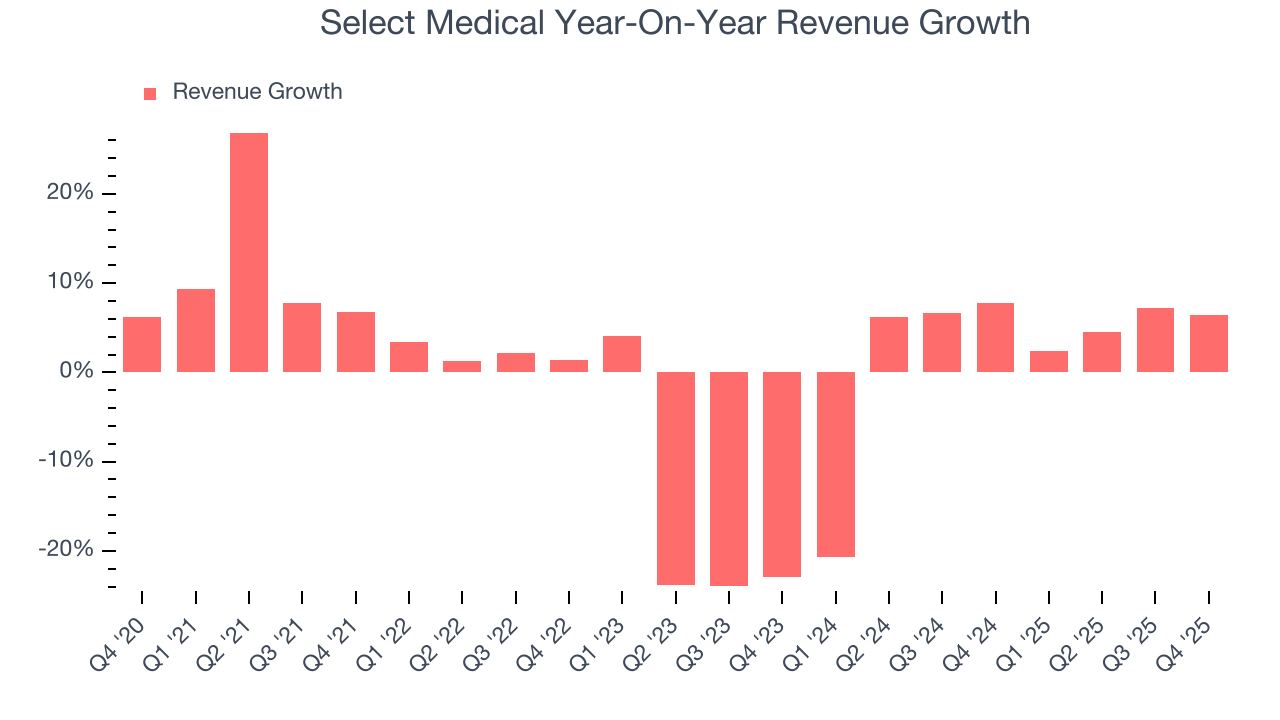

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Select Medical struggled to consistently increase demand as its $5.45 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of lacking business quality.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Select Medical’s annualized revenue growth of 1.6% over the last two years is above its five-year trend, which is encouraging.

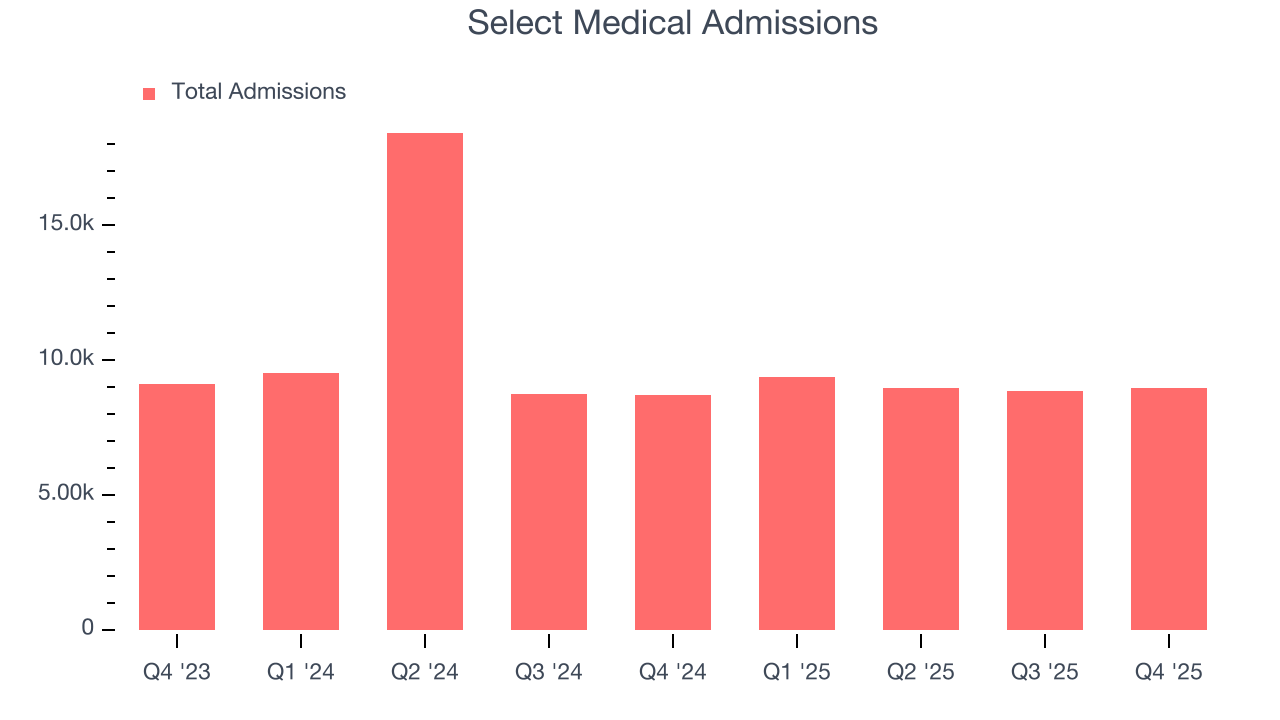

Select Medical also reports its number of admissions, which reached 8,950 in the latest quarter. Over the last two years, Select Medical’s admissions averaged 10.7% year-on-year declines. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Select Medical reported year-on-year revenue growth of 6.4%, and its $1.40 billion of revenue exceeded Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

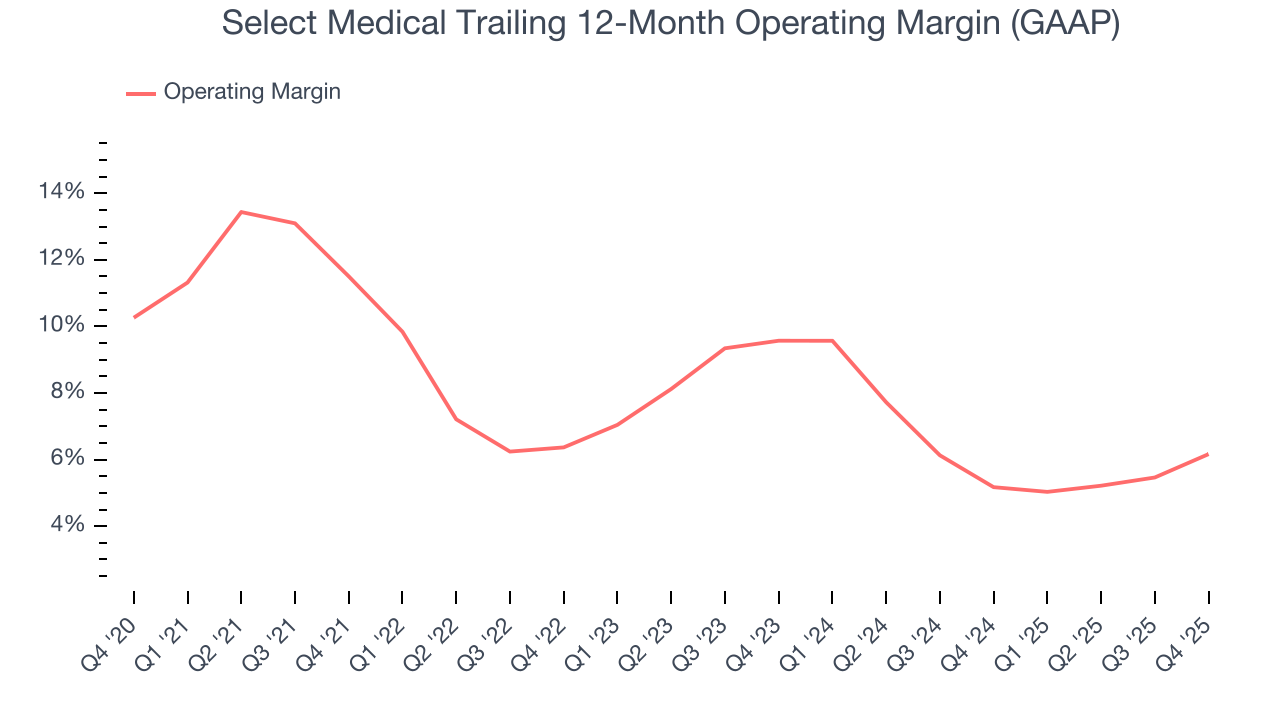

Select Medical was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.8% was weak for a healthcare business.

Analyzing the trend in its profitability, Select Medical’s operating margin decreased by 5.3 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.4 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Select Medical generated an operating margin profit margin of 4.6%, up 3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

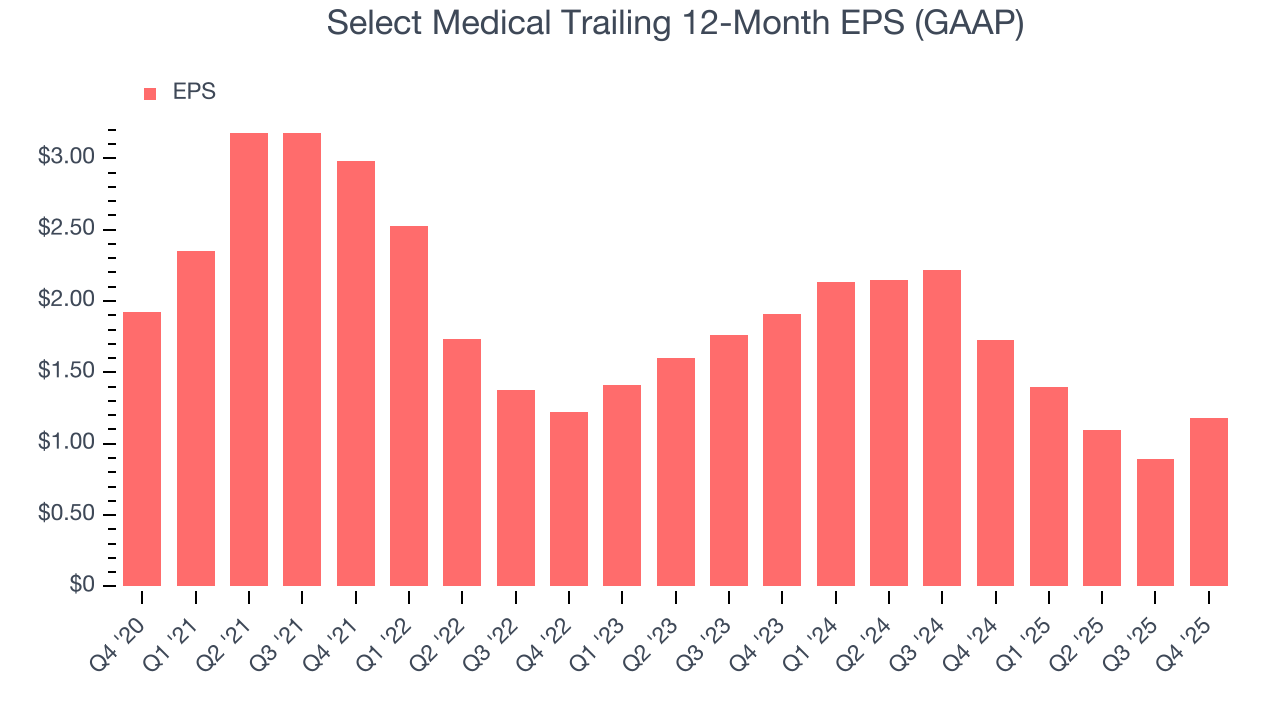

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Select Medical, its EPS declined by 9.4% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

We can take a deeper look into Select Medical’s earnings to better understand the drivers of its performance. As we mentioned earlier, Select Medical’s operating margin expanded this quarter but declined by 5.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Select Medical reported EPS of $0.16, up from negative $0.13 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Select Medical’s full-year EPS of $1.18 to grow 16.1%.

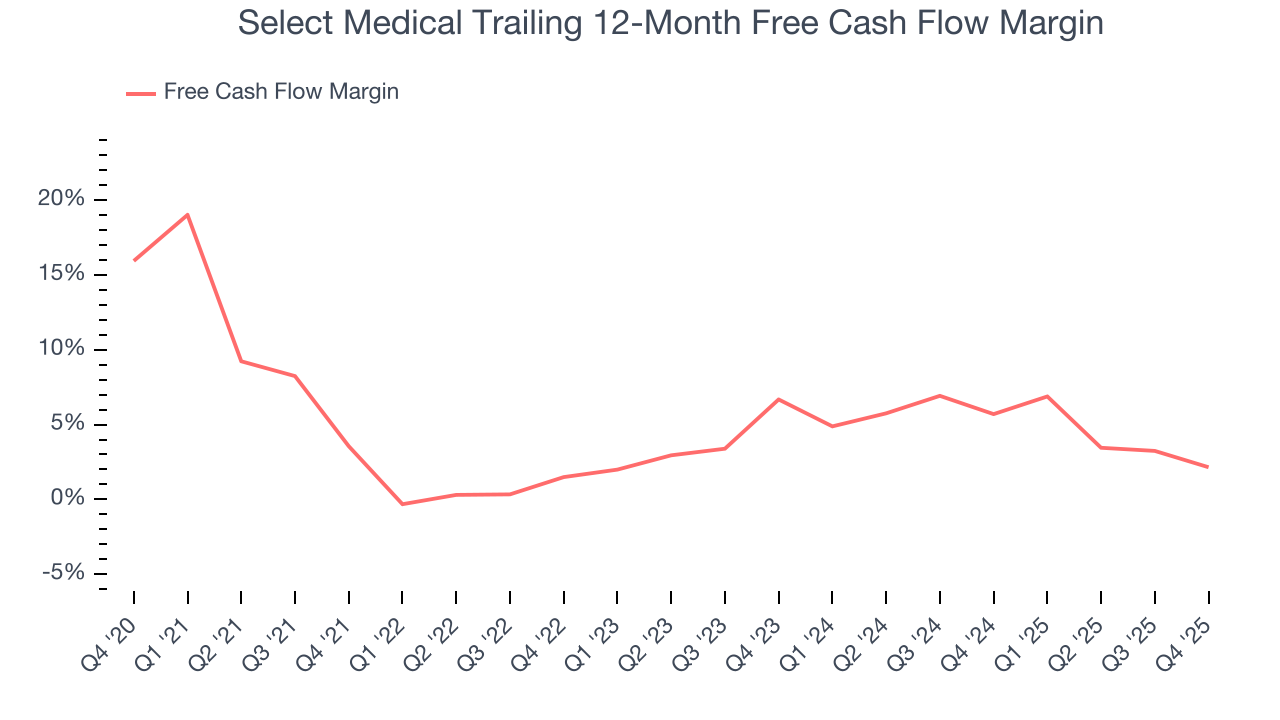

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Select Medical has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.8%, subpar for a healthcare business.

Taking a step back, we can see that Select Medical’s margin dropped by 1.4 percentage points during that time. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle.

Select Medical broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 4.3 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

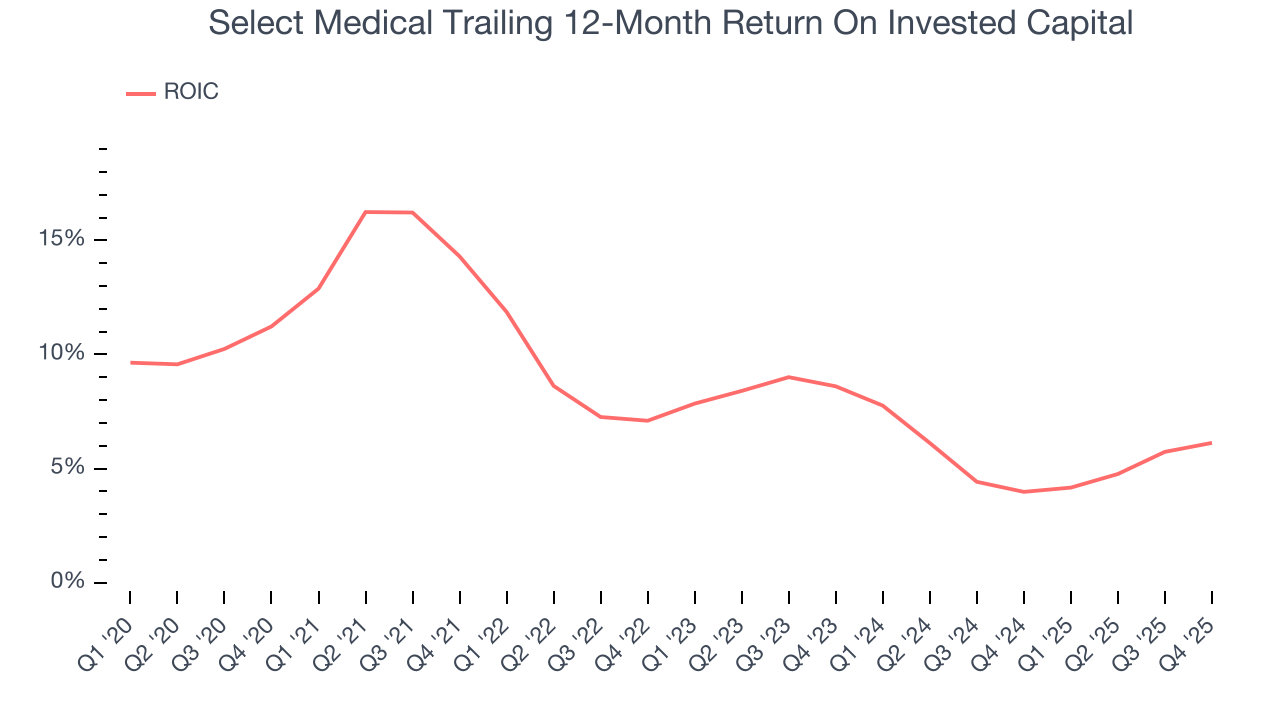

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Select Medical’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 8%, slightly better than typical healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Select Medical’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

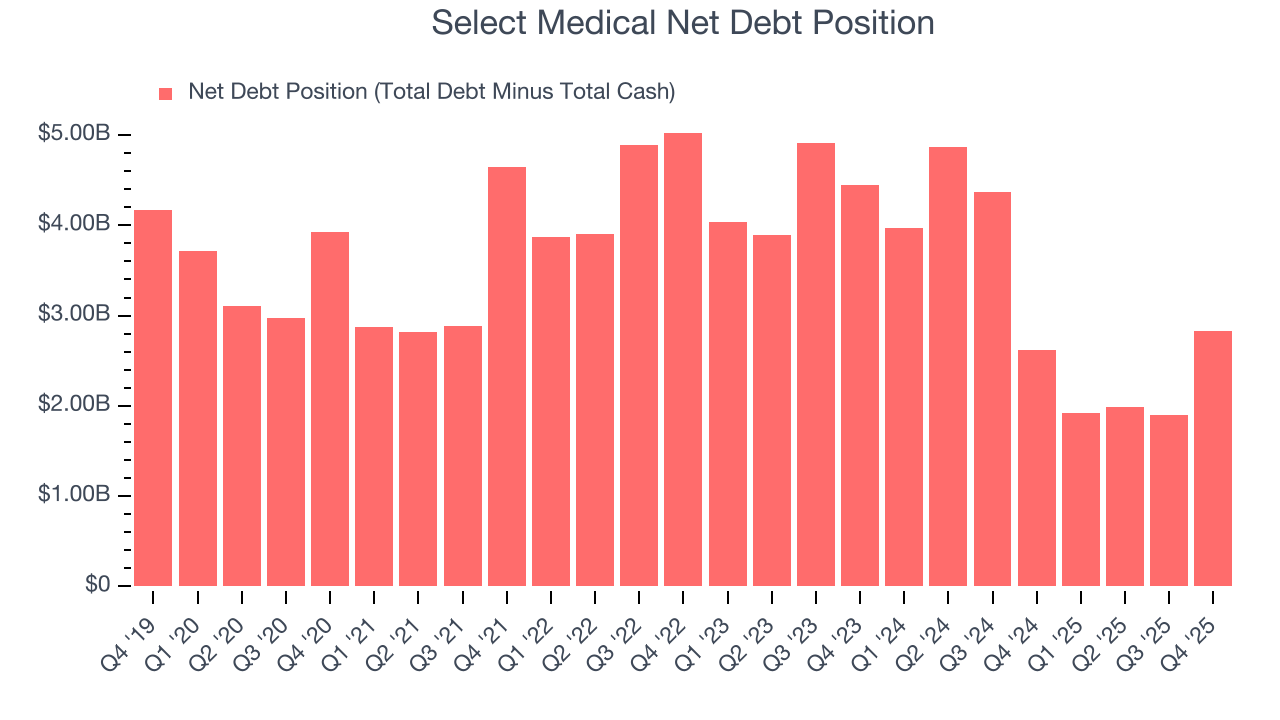

11. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Select Medical’s $2.85 billion of debt exceeds the $26.52 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $493.2 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Select Medical could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Select Medical can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Select Medical’s Q4 Results

It was encouraging to see Select Medical beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.8% to $15.48 immediately following the results.

13. Is Now The Time To Buy Select Medical?

Updated: March 14, 2026 at 12:09 AM EDT

Before deciding whether to buy Select Medical or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Select Medical’s business quality ultimately falls short of our standards. To kick things off, its revenue growth was uninspiring over the last five years. On top of that, Select Medical’s declining EPS over the last five years makes it a less attractive asset to the public markets, and its admissions declined.

Select Medical’s P/E ratio based on the next 12 months is 13.1x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $16.63 on the company (compared to the current share price of $16.25).