Soho House (SHCO)

Soho House faces an uphill battle. Its poor sales growth shows demand is soft and its negative returns on capital suggest it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Soho House Will Underperform

Boasting fancy locations in hubs such as NYC and Miami, Soho House (NYSE:SHCO) is a global hospitality brand offering exclusive private member clubs, hotels, and restaurants.

- 15.8% annual revenue growth over the last two years was slower than its consumer discretionary peers

- Persistent operating margin losses suggest the business manages its expenses poorly

- 5× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Soho House doesn’t fulfill our quality requirements. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Soho House

At $8.84 per share, Soho House trades at 10.8x forward EV-to-EBITDA. This valuation is fair for the quality you get, but we’re on the sidelines for now.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Soho House (SHCO) Research Report: Q3 CY2024 Update

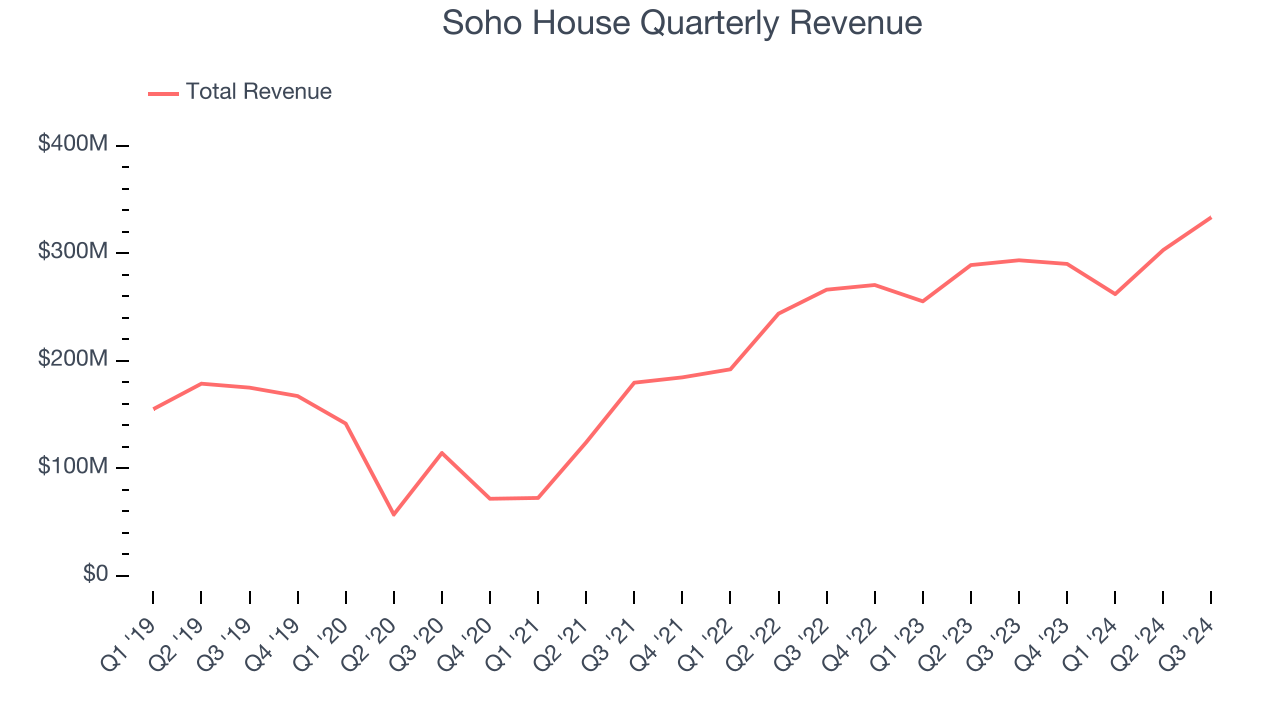

Social club operator Soho House (NYSE:SHCO) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 13.6% year on year to $333.4 million. On the other hand, the company’s full-year revenue guidance of $1.2 billion at the midpoint came in 2.2% below analysts’ estimates. Its non-GAAP loss of $0 per share increased from -$0.25 in the same quarter last year.

Soho House (SHCO) Q3 CY2024 Highlights:

- Revenue: $333.4 million vs analyst estimates of $332.3 million (13.6% year-on-year growth, in line)

- Adjusted EBITDA: $48.28 million vs analyst estimates of $47.39 million (14.5% margin, 1.9% beat)

- The company dropped its revenue guidance for the full year to $1.2 billion at the midpoint from $1.23 billion, a 2% decrease

- EBITDA guidance for the full year is $140 million at the midpoint, below analyst estimates of $159.1 million

- Operating Margin: 11.4%, up from -9.3% in the same quarter last year

- Free Cash Flow Margin: 2.6%, up from 1.4% in the same quarter last year

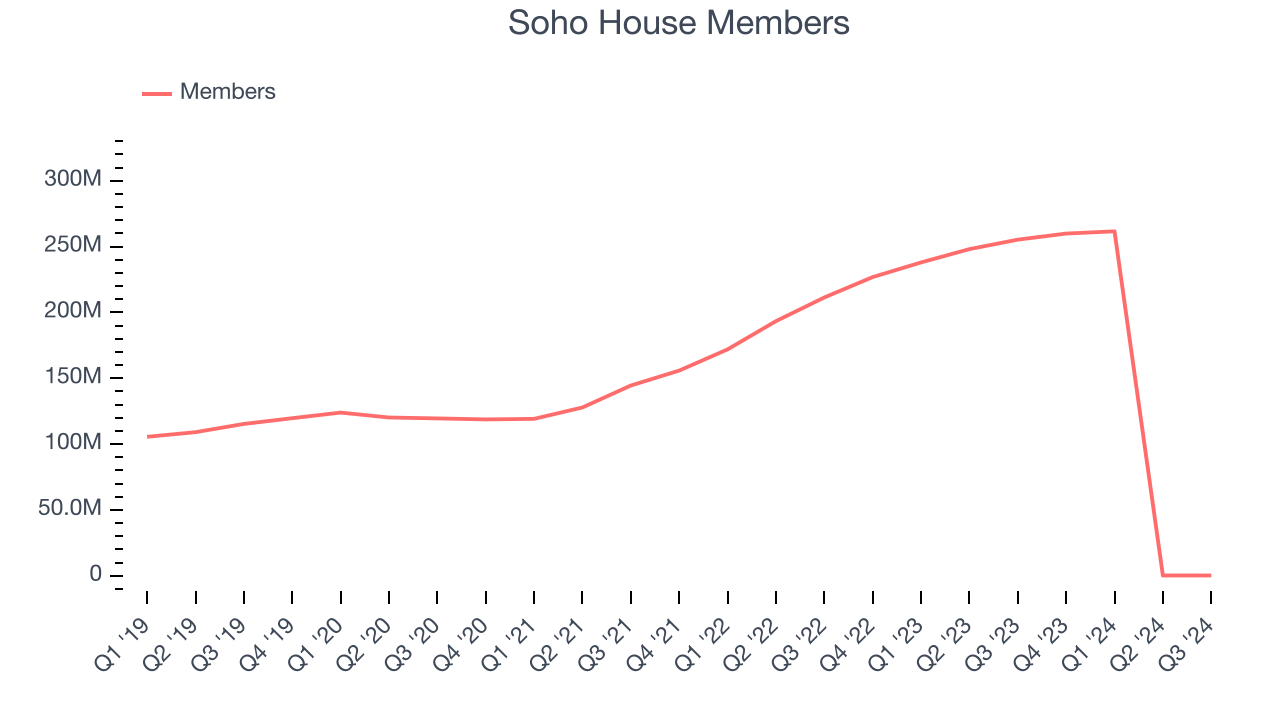

- Members: 267,494, down 255 million year on year

- Market Capitalization: $1.23 billion

Company Overview

Boasting fancy locations in hubs such as NYC and Miami, Soho House (NYSE:SHCO) is a global hospitality brand offering exclusive private member clubs, hotels, and restaurants.

Soho House began as a small, single-location private members' club for those in the film, media, and creative industries. Since then, the company has expanded its presence internationally, providing stylish, comfortable spaces for its creative community to socialize, work, and relax.

Today, Soho House operates nearly 30 clubs along with hotels, cinemas, spas, and workspaces. The "Houses", as they are known, are set in a variety of locations from bustling city centers to more rural, picturesque settings.

Each House is distinct, with interiors and experiences tailored to their local context. However, each shares a common thread of sophisticated and eclectic design, high-quality food and drink, and an atmosphere of exclusivity and comfort.

Membership to Soho House is selective, aiming to foster a diverse and dynamic community. Its members are granted access to its global network of Houses, along with benefits such as exclusive events, screenings, and workshops.

In recent years, Soho House has diversified its offerings even further to include public restaurants, branded home furnishings, and a line of skincare and grooming products, expanding its brand footprint in the consumer lifestyle sector.

4. Travel and Vacation Providers

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

Soho House's primary competitors include private companies The Groucho Club, The Hospital Club, Shoreditch House, The Arts Club, and The Ivy Club. Publicly traded competitors with slightly different business models include Marriott (NASDAQ:MAR), Hilton (NYSE:HLT), Hyatt (NYSE:H), and InterContinental Hotels (NYSE:IHG).

5. Revenue Growth

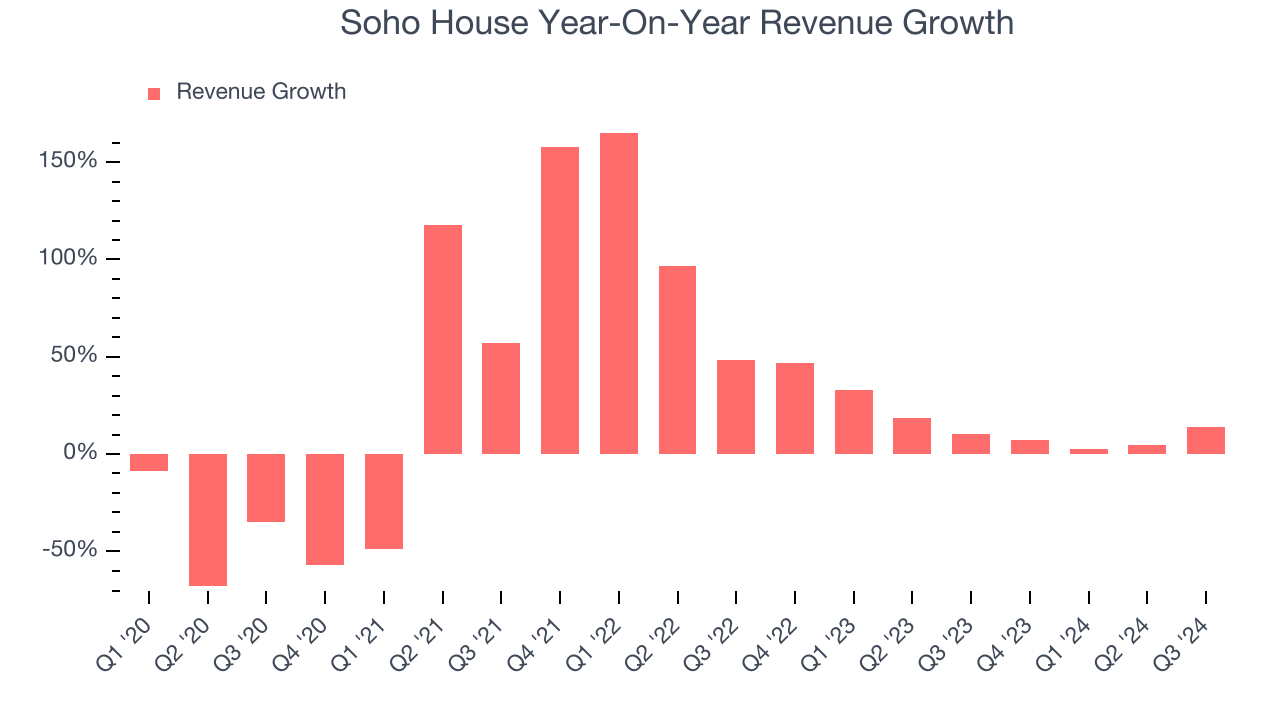

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Soho House grew its sales at a 12% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Soho House’s annualized revenue growth of 15.8% over the last two years is above its five-year trend, suggesting some bright spots.

We can better understand the company’s revenue dynamics by analyzing its number of members, which reached 267,494 in the latest quarter. Over the last two years, Soho House’s members averaged 5.3% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Soho House’s year-on-year revenue growth was 13.6%, and its $333.4 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

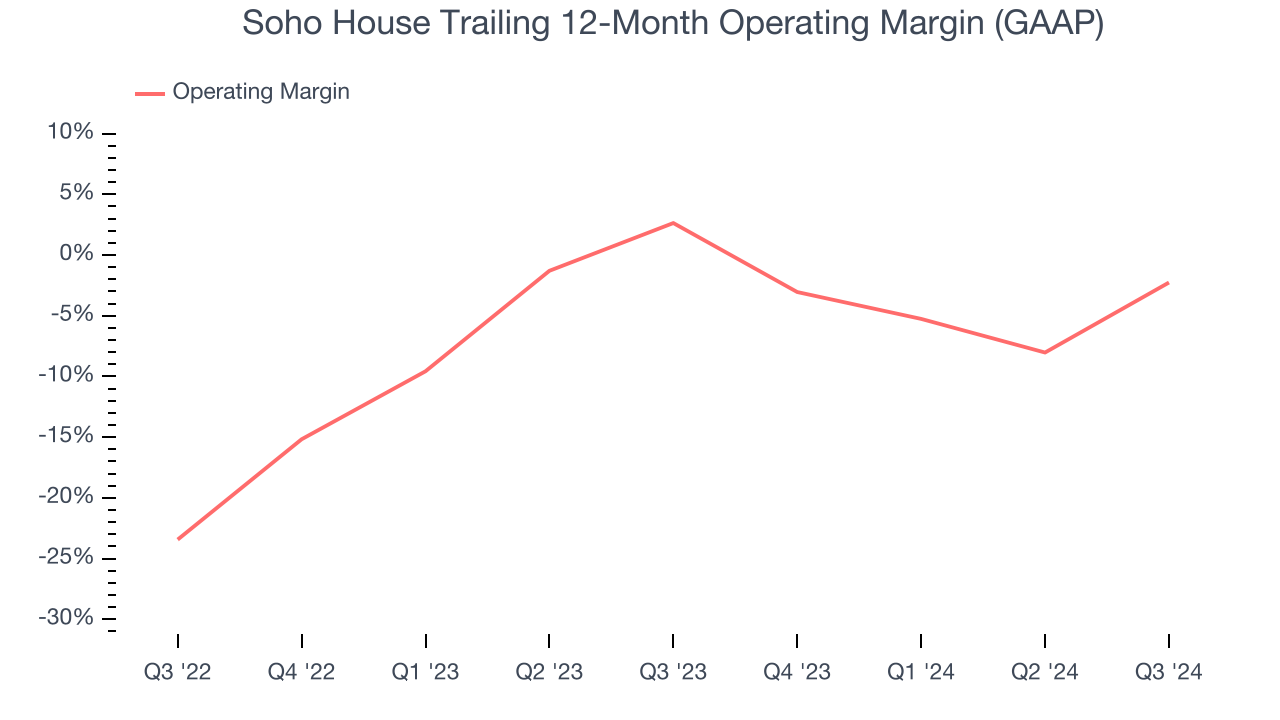

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Soho House’s operating margin has been trending down over the last 12 months, and it ended up breaking even over the last two years. The company’s performance was inadequate, showing its operating expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Soho House generated an operating margin profit margin of 11.4%, up 20.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Soho House’s full-year earnings are still negative, it reduced its losses and improved its EPS by 25.2% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability.

In Q3, Soho House reported EPS of $0, up from negative $0.22 in the same quarter last year. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

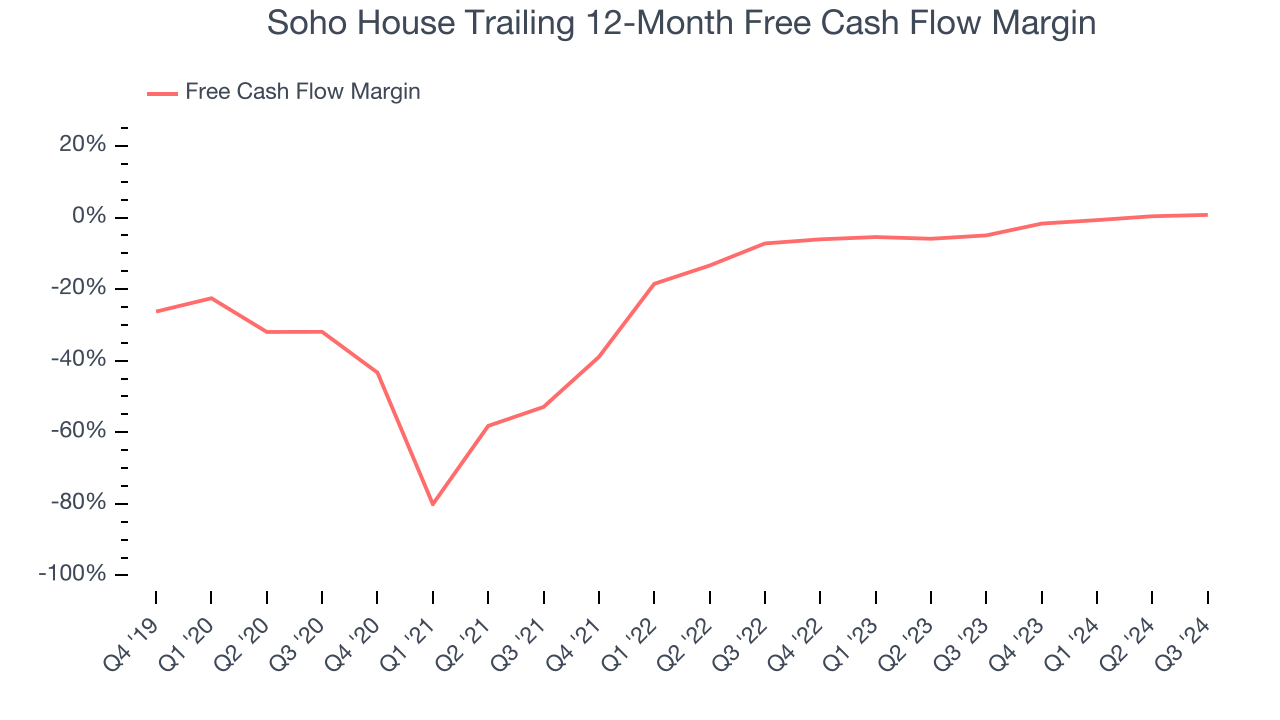

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Soho House posted positive free cash flow this quarter, the broader story hasn’t been so clean. Over the last two years, Soho House’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 2%, meaning it lit $2.01 of cash on fire for every $100 in revenue.

Soho House’s free cash flow clocked in at $8.77 million in Q3, equivalent to a 2.6% margin. This result was good as its margin was 1.2 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Soho House’s cash conversion will improve. Their consensus estimates imply its breakeven free cash flow margin for the last 12 months will increase to 3.9%, giving it more optionality.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Soho House’s five-year average ROIC was negative 22.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Soho House’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

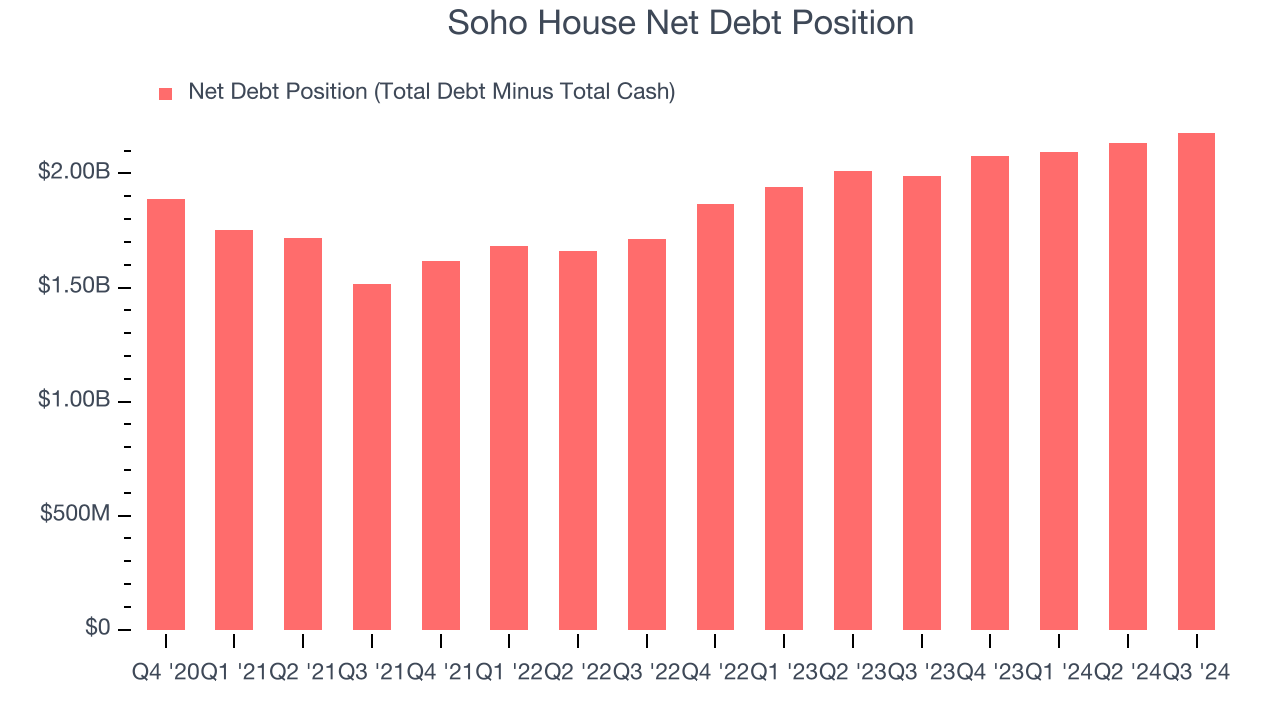

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Soho House’s $2.32 billion of debt exceeds the $142.8 million of cash on its balance sheet. Furthermore, its 16× net-debt-to-EBITDA ratio (based on its EBITDA of $134 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Soho House could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Soho House can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Soho House’s Q3 Results

We were impressed by how significantly Soho House blew past analysts’ adjusted operating income expectations this quarter. On the other hand, its number of members missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $6.31 immediately after reporting.

12. Is Now The Time To Buy Soho House?

Updated: November 25, 2025 at 10:11 PM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Soho House, you should also grasp the company’s longer-term business quality and valuation.

Soho House doesn’t pass our quality test. First off, its revenue growth was uninspiring over the last four years, and analysts expect its demand to deteriorate over the next 12 months. And while its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its number of members has disappointed. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Soho House’s EV-to-EBITDA ratio based on the next 12 months is 14.4x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $9 on the company (compared to the current share price of $8.85).