Snap (SNAP)

Snap is interesting. Although its sales growth has been weak, its profitability gives it the flexibility to ride out cycles.― StockStory Analyst Team

1. News

2. Summary

Why Snap Is Interesting

Founded by Stanford University students Evan Spiegel, Reggie Brown, and Bobby Murphy, and originally called Picaboo, Snapchat (NYSE: SNAP) is an image centric social media network.

- Additional sales over the last three years increased its profitability as the 27.9% annual growth in its earnings per share outpaced its revenue

- Disciplined cost controls and effective management have materialized in a strong EBITDA margin, and its profits increased over the last few years as it scaled

- One risk is its muted 8.8% annual revenue growth over the last three years shows its demand lagged behind its consumer internet peers

Snap almost passes our quality test. If you believe in the company, the valuation seems reasonable.

Why Is Now The Time To Buy Snap?

At $3.95 per share, Snap trades at 7.8x forward EV/EBITDA. When stacked up against other consumer internet companies, we think Snap’s multiple is fair for the fundamentals you get.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. Snap (SNAP) Research Report: Q4 CY2025 Update

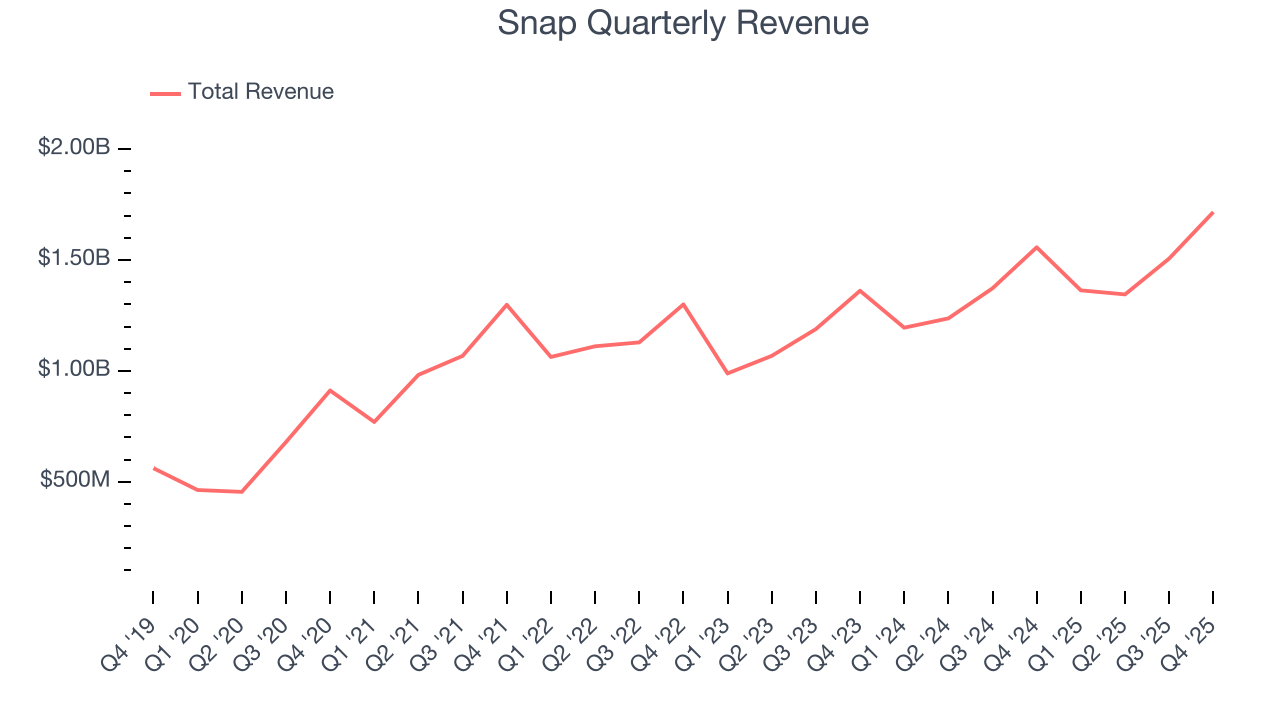

Social network Snapchat (NYSE: SNAP) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 10.2% year on year to $1.72 billion. Its GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Snap (SNAP) Q4 CY2025 Highlights:

- Revenue: $1.72 billion vs analyst estimates of $1.70 billion (10.2% year-on-year growth, 0.9% beat)

- EPS (GAAP): $0.03 vs analyst estimates of -$0.03 (significant beat)

- Adjusted EBITDA: $357.7 million vs analyst estimates of $299.2 million (20.8% margin, 19.5% beat)

- Operating Margin: 2.9%, up from -1.7% in the same quarter last year

- Free Cash Flow Margin: 12%, up from 6.2% in the previous quarter

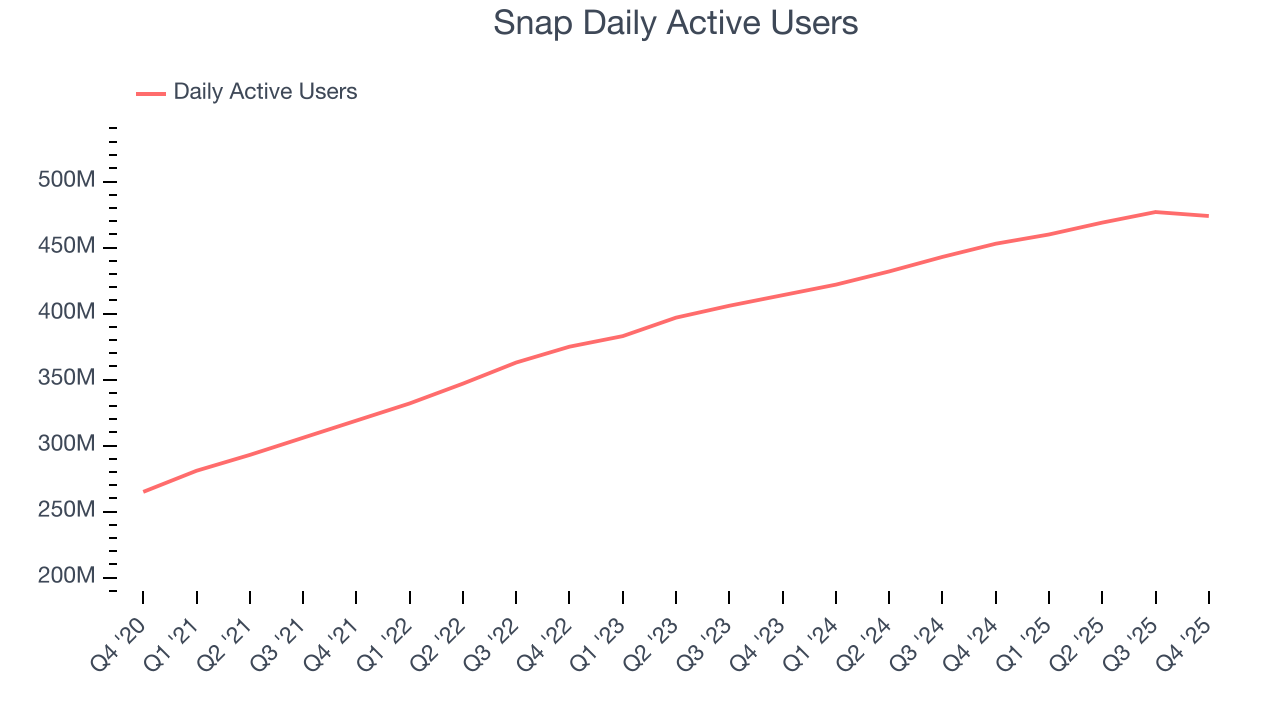

- Daily Active Users: 474 million, up 21 million year on year

- Market Capitalization: $10.49 billion

Company Overview

Founded by Stanford University students Evan Spiegel, Reggie Brown, and Bobby Murphy, and originally called Picaboo, Snapchat (NYSE: SNAP) is an image centric social media network.

Snapchat differentiates itself from other social networks through product innovation around Augmented Reality (AR), demographics, and the ephemeral nature of its messaging and Stories. Snapchat is a mobile first, camera centric image messaging app whose disappearing messages are meant to emphasize personal expression and living in the moment. The Snapchat platform has 5 distinct features: the main Camera tab, where users send snaps to friends, Communication (messaging/video calls), Snap Map (personalized map that shows friends and local businesses), Stories (content from users, news, and professionally generated content), and Spotlight (sort of a TikTok-like never ending spool of content Snapchat tailors to a user’s likes).

More so than other social networks, Snapchat is geared to digital natives, specifically 13-34 year olds. This is what makes the platform appealing to advertisers - its unique ability to address a hard to reach demographic at scale. The majority of under 35s in the US, Australia, and Western Europe use Snapchat. Originally built only for iOS, Snapchat introduced a version for Android in 2019, which is why rest of world adoption is still in its early stages. The reason advertisers have flocked to Snapchat is the very high ROI for advertisers: the cost of advertising on Snap remains low.

4. Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Snapchat (NYSE: SNAP) competes with fellow social media advertising platforms like Google (NASDAQ: GOOGL), Meta Platforms (NASDAQ:FB), Twitter (NYSE: TWTR), and Pinterest (NASDAQ: PINS)

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Snap grew its sales at a mediocre 8.8% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Snap.

This quarter, Snap reported year-on-year revenue growth of 10.2%, and its $1.72 billion of revenue exceeded Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to grow 14.4% over the next 12 months, an acceleration versus the last three years. This projection is noteworthy and suggests its newer products and services will catalyze better top-line performance.

6. Daily Active Users

User Growth

As a social network, Snap generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Snap’s daily active users, a key performance metric for the company, increased by 8.4% annually to 474 million in the latest quarter. This growth rate is decent for a consumer internet business and indicates people enjoy using its offerings.

In Q4, Snap added 21 million daily active users, leading to 4.6% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

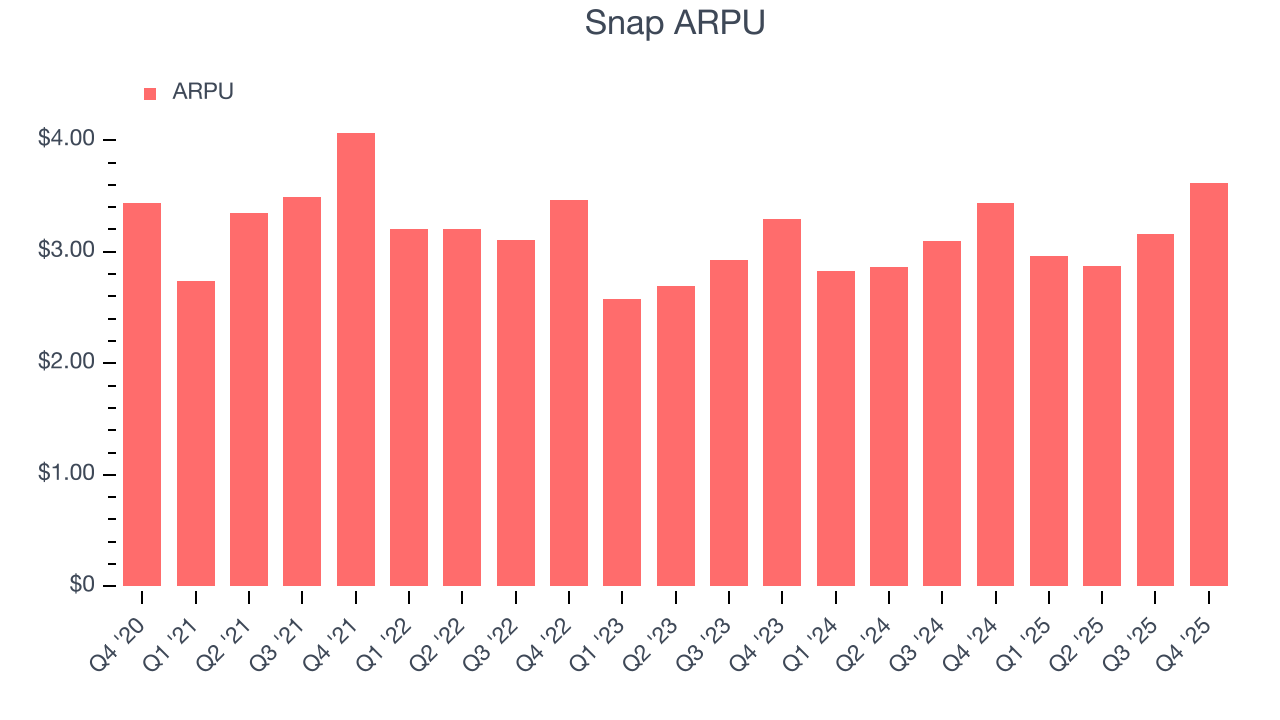

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Snap’s audience and its ad-targeting capabilities.

Snap’s ARPU growth has been mediocre over the last two years, averaging 4.8%. This isn’t great, but the increase in daily active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Snap tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, Snap’s ARPU clocked in at $3.62. It grew by 5.2% year on year, mirroring the performance of its daily active users.

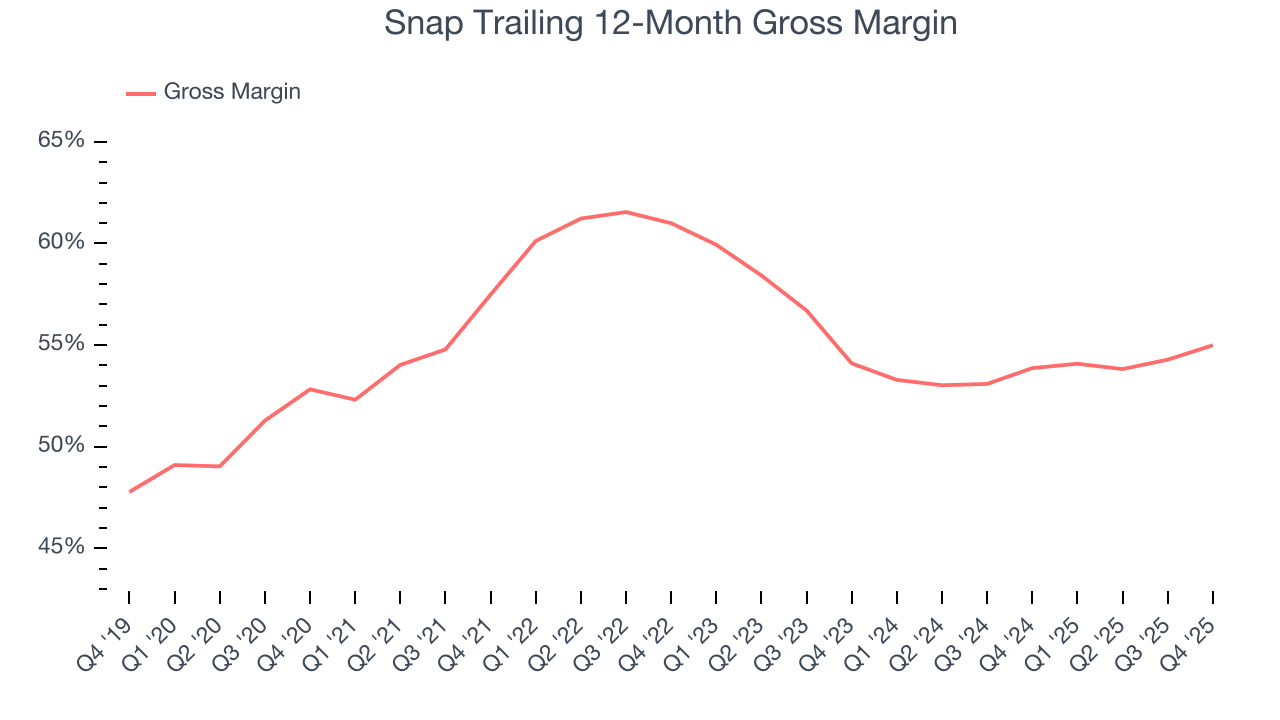

7. Gross Margin & Pricing Power

For social network businesses like Snap, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center, and other infrastructure expenses.

Snap’s gross margin is slightly below the average consumer internet company, giving it less room to invest in areas such as product and marketing to grow its presence. As you can see below, it averaged a 54.5% gross margin over the last two years. Said differently, Snap had to pay a chunky $45.54 to its service providers for every $100 in revenue.

In Q4, Snap produced a 59.1% gross profit margin, marking a 2.2 percentage point increase from 56.9% in the same quarter last year. Snap’s full-year margin has also been trending up over the past 12 months, increasing by 1.1 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

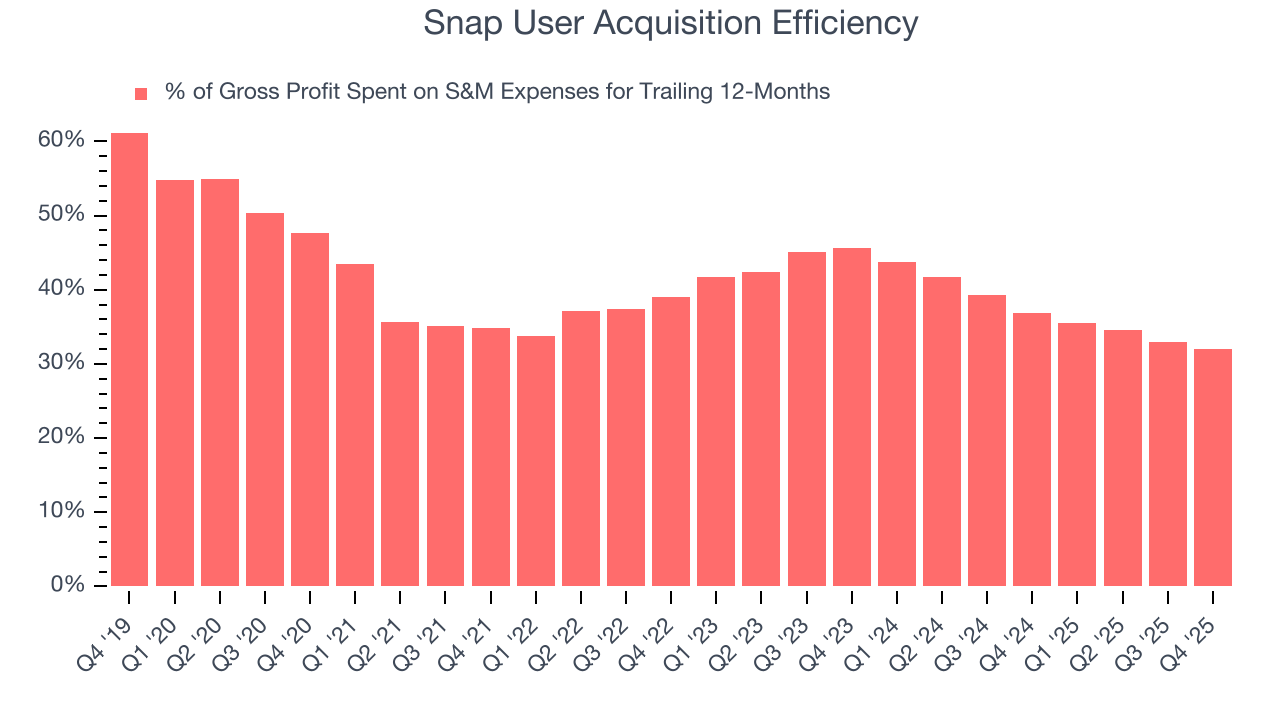

8. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Snap grow from a combination of product virality, paid advertisement, and incentives.

Snap is quite efficient at acquiring new users, spending only 32.1% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that Snap has a highly differentiated product offering, giving it the freedom to invest its resources into new growth initiatives.

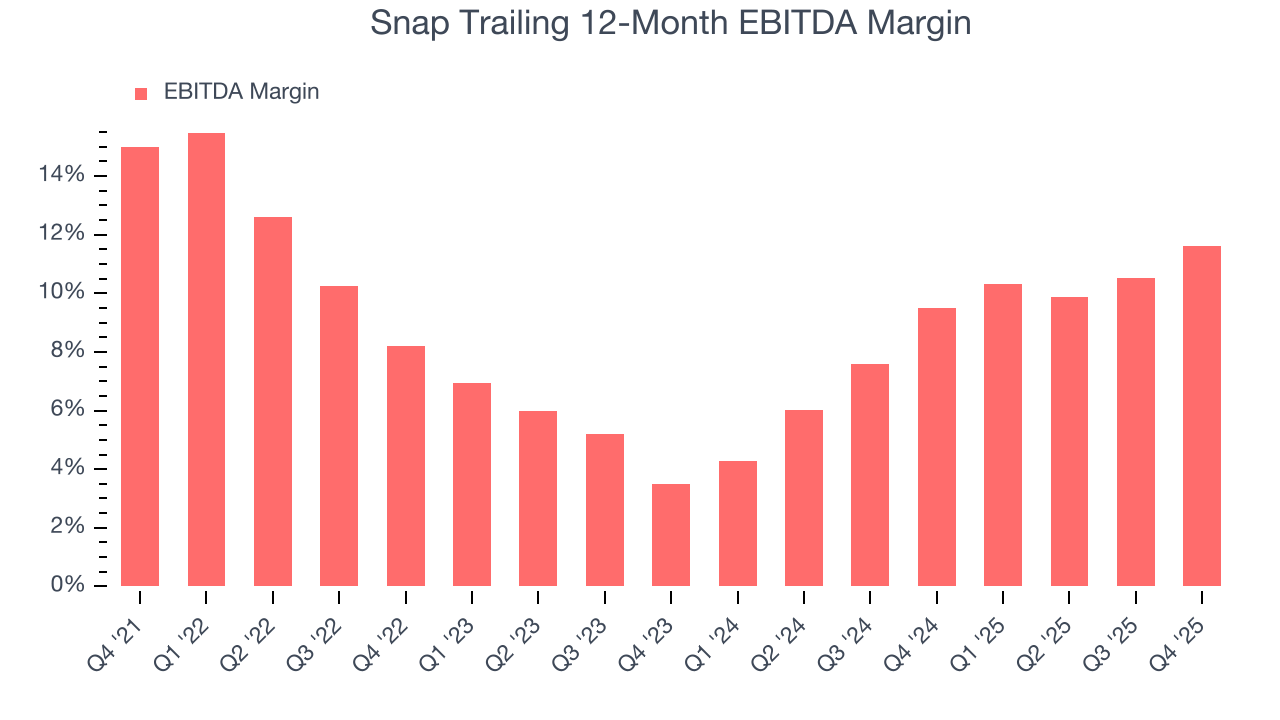

9. EBITDA

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Snap has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer internet sector, boasting an average EBITDA margin of 10.6%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Snap’s EBITDA margin rose by 3.4 percentage points over the last few years, as its sales growth gave it operating leverage.

In Q4, Snap generated an EBITDA margin profit margin of 20.8%, up 3.1 percentage points year on year. The increase was encouraging, and because its EBITDA margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

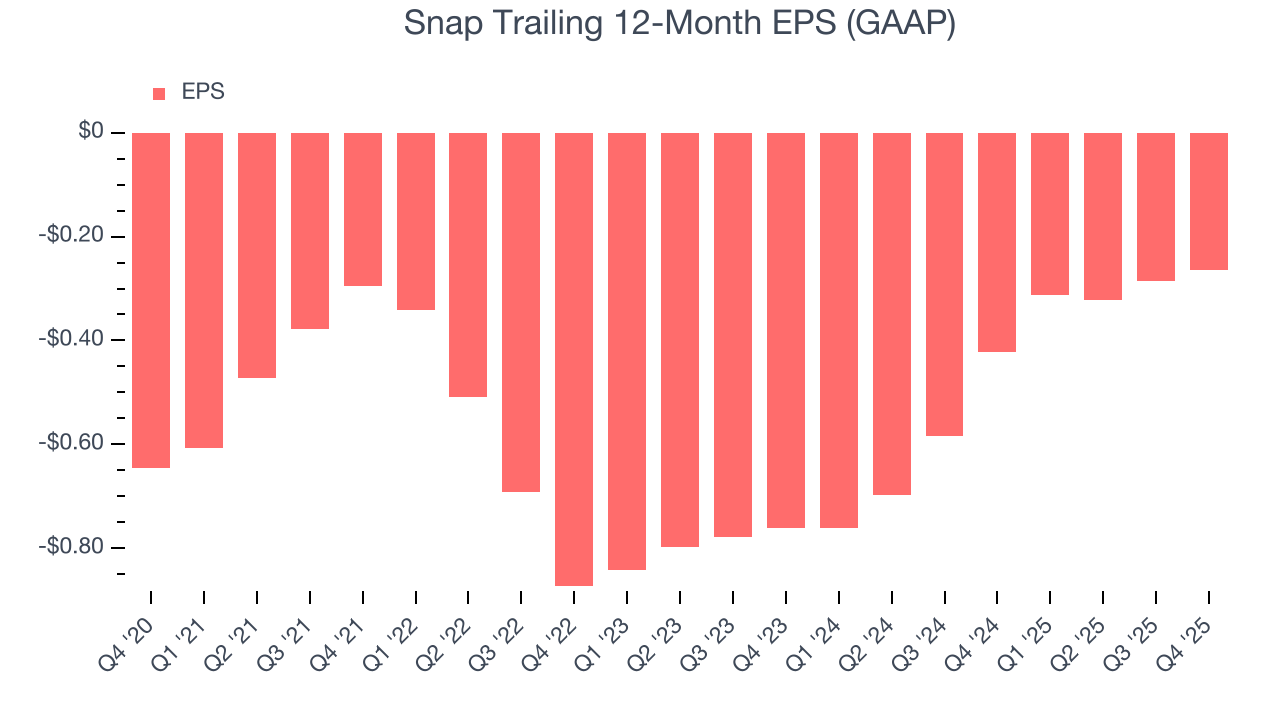

10. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Snap’s full-year earnings are still negative, it reduced its losses and improved its EPS by 32.8% annually over the last three years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

In Q4, Snap reported EPS of $0.03, up from $0.01 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Snap to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.27 will advance to negative $0.15.

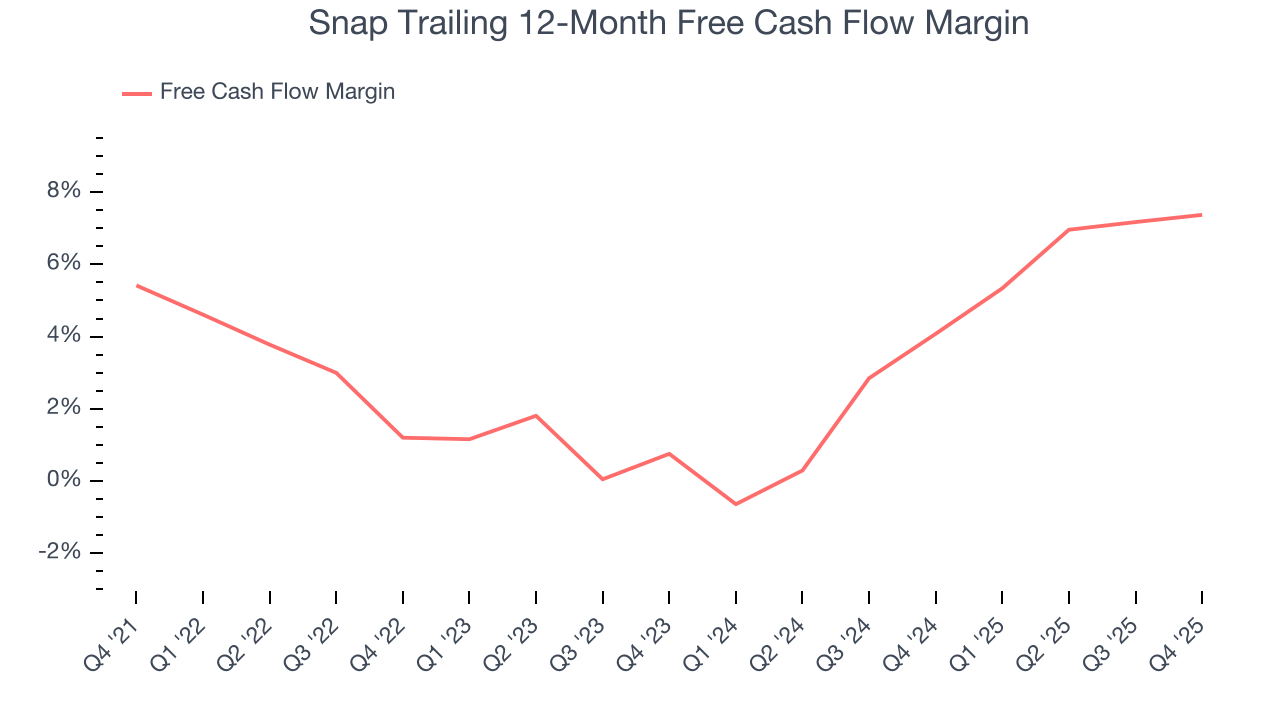

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Snap has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.8% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that Snap’s margin expanded by 6.2 percentage points over the last few years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Snap’s free cash flow clocked in at $205.6 million in Q4, equivalent to a 12% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

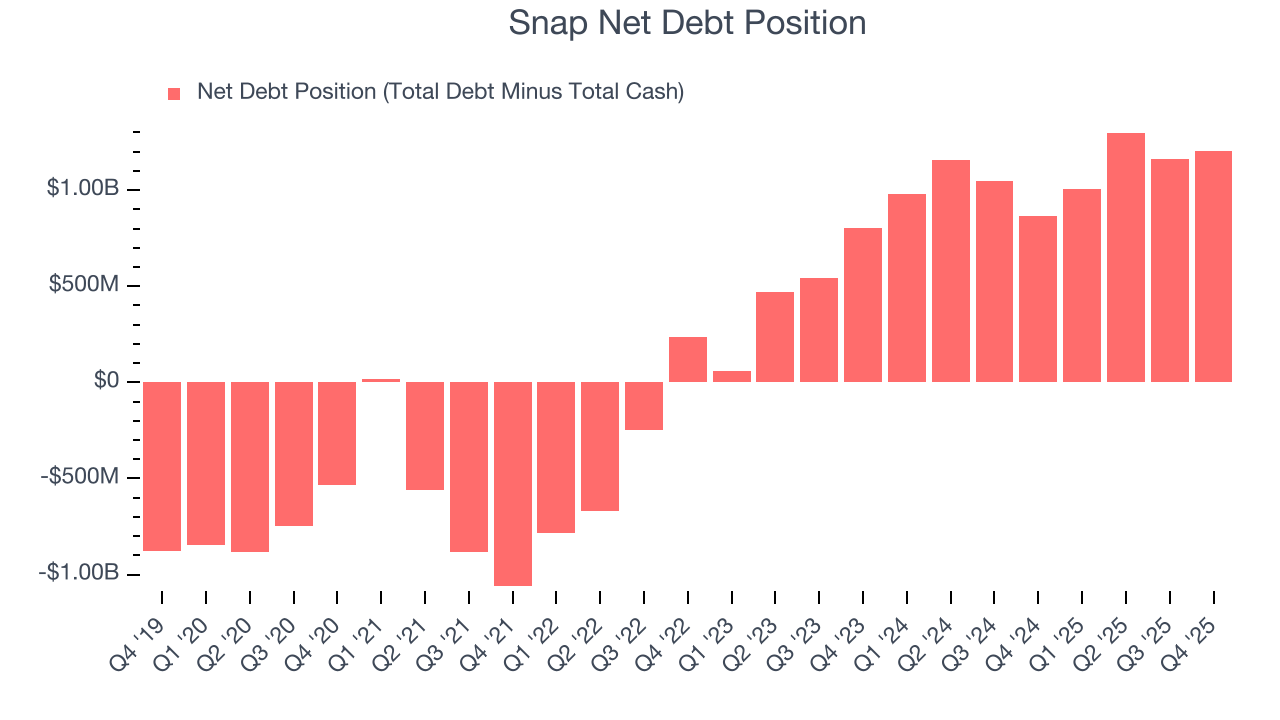

12. Balance Sheet Assessment

Snap reported $2.94 billion of cash and $4.14 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $689.5 million of EBITDA over the last 12 months, we view Snap’s 1.7× net-debt-to-EBITDA ratio as safe. We also see its $12.16 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Snap’s Q4 Results

We were impressed by how significantly Snap blew past analysts’ EBITDA expectations this quarter on a slight revenue beat. On the other hand, its number of daily active users slightly missed. Overall, this print had some key positives. The stock traded up 5.1% to $6.24 immediately following the results.

14. Is Now The Time To Buy Snap?

Updated: March 29, 2026 at 10:15 PM EDT

Before investing in or passing on Snap, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There’s plenty to admire about Snap. Although its revenue growth was mediocre over the last three years, its growth over the next 12 months is expected to be higher. On top of that, Snap’s EPS growth over the last three years has been fantastic, and the company’s projected EPS for the next year implies the company’s fundamentals will improve.

Snap’s EV/EBITDA ratio based on the next 12 months is 7.8x. Looking at the consumer internet landscape right now, Snap trades at a pretty interesting price. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $7.97 on the company (compared to the current share price of $3.95), implying they see 102% upside in buying Snap in the short term.