AT&T (T)

AT&T is up against the odds. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think AT&T Will Underperform

Founded by Alexander Graham Bell, AT&T (NYSE:T) is a multinational telecomm conglomerate providing a range of communications and internet services.

- Sales were flat over the last five years, indicating it’s failed to expand its business

- Performance over the past five years shows each sale was less profitable, as its earnings per share fell by 7.9% annually

- Below-average returns on capital indicate management struggled to find compelling investment opportunities

AT&T doesn’t fulfill our quality requirements. You should search for better opportunities.

Why There Are Better Opportunities Than AT&T

At $29.08 per share, AT&T trades at 12.6x forward P/E. Yes, this valuation multiple is lower than that of other consumer discretionary peers, but we’ll remind you that you often get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. AT&T (T) Research Report: Q4 CY2025 Update

Telecommunications conglomerate AT&T (NYSE:T) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 3.6% year on year to $33.47 billion. Its GAAP profit of $0.53 per share was 14.3% above analysts’ consensus estimates.

AT&T (T) Q4 CY2025 Highlights:

- Revenue: $33.47 billion vs analyst estimates of $32.79 billion (3.6% year-on-year growth, 2.1% beat)

- EPS (GAAP): $0.53 vs analyst estimates of $0.46 (14.3% beat)

- Operating Margin: 17.3%, in line with the same quarter last year

- Free Cash Flow Margin: 13.6%, down from 15.6% in the same quarter last year

- Market Capitalization: $163.1 billion

Company Overview

Founded by Alexander Graham Bell, AT&T (NYSE:T) is a multinational telecomm conglomerate providing a range of communications and internet services.

Over the years, the company has evolved from a traditional telephone service provider into a modern communications leader, expanding its offerings to include wireless and services to keep consumers connected. In recent times, AT&T divested its media assets, such as WarnerMedia in 2022, to refocus on its core telecommunications business and invest in 5G and fiber network expansion. This is why you'll see a big drop in revenue in 2020 (the financials were restated for 2020 and 2021 as if the divestiture had happened so that investors could compare apples-to-apples financials).

AT&T's offerings range from wireless voice and data services to high-speed internet and entertainment products. For example, its flagship wireless service provides nationwide 5G coverage, allowing customers to enjoy fast data speeds and reliable connectivity on their smartphones. Another product, AT&T Fiber, offers ultra-fast internet service to homes and businesses, enabling high-definition streaming, online gaming, and efficient remote work capabilities.

AT&T generates revenue through three primary sources: wireless services, broadband internet, and business services. Under wireless services, its primary cash machine, the company earns income by providing mobile phone plans to consumers and businesses, charging based on data usage, plan features, or device financing. The broadband model involves offering high-speed internet access through fiber and DSL services to residential and commercial customers. AT&T's business products work by generating revenue when enterprises engage with its communications and networking services. For example, consider a corporation that uses AT&T's cloud networking to connect its various offices, AT&T earns fees for providing these essential services that enable the company's operations.

4. Wireless, Cable and Satellite

The massive physical footprints of cell phone towers, fiber in the ground, or satellites in space make it challenging for companies in this industry to adjust to shifting consumer habits. Over the last decade-plus, consumers have ‘cut the cord’ to their landlines and traditional cable subscriptions in favor of wireless communications and streaming video. These trends do mean that more households need cell phone plans and high-speed internet. Companies that successfully serve customers can enjoy high retention rates and pricing power since the options for mobile and internet connectivity in any geography are usually limited.

Competitors in the telecommunications industry include Verizon (NYSE:VZ), T-Mobile (NASDAQ:TMUS), and Comcast (NASDAQ:CMCSA).

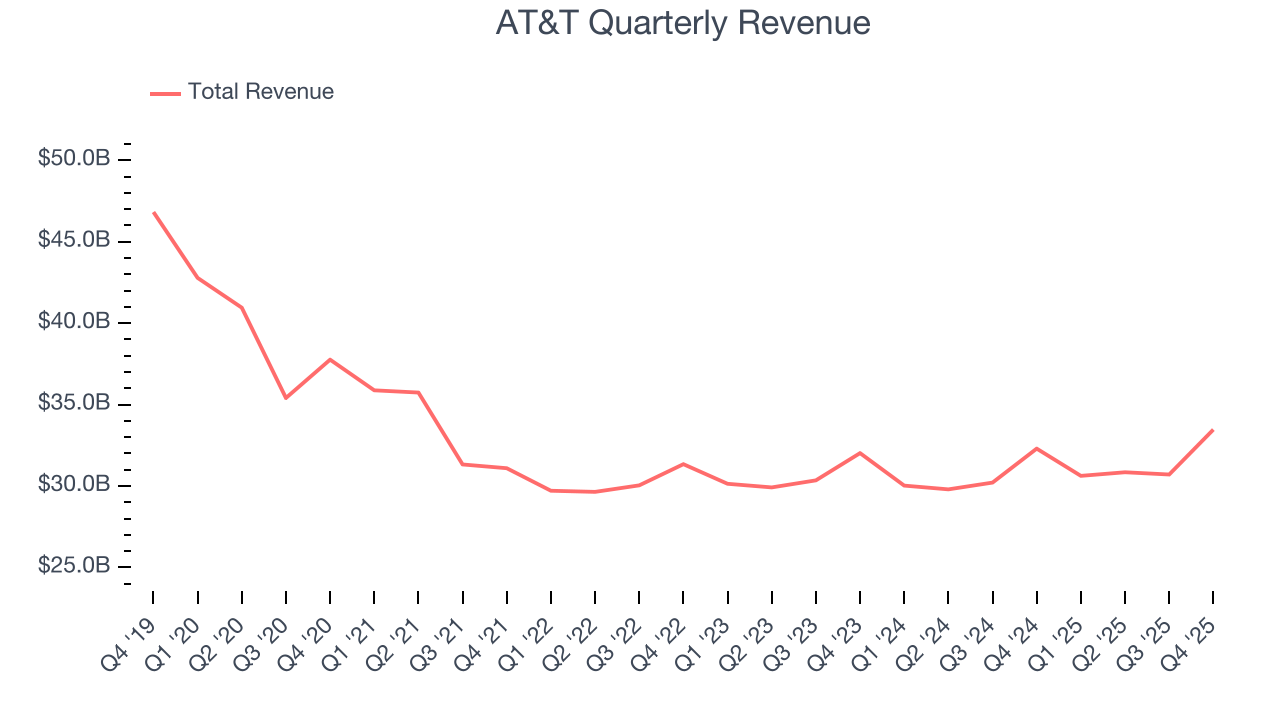

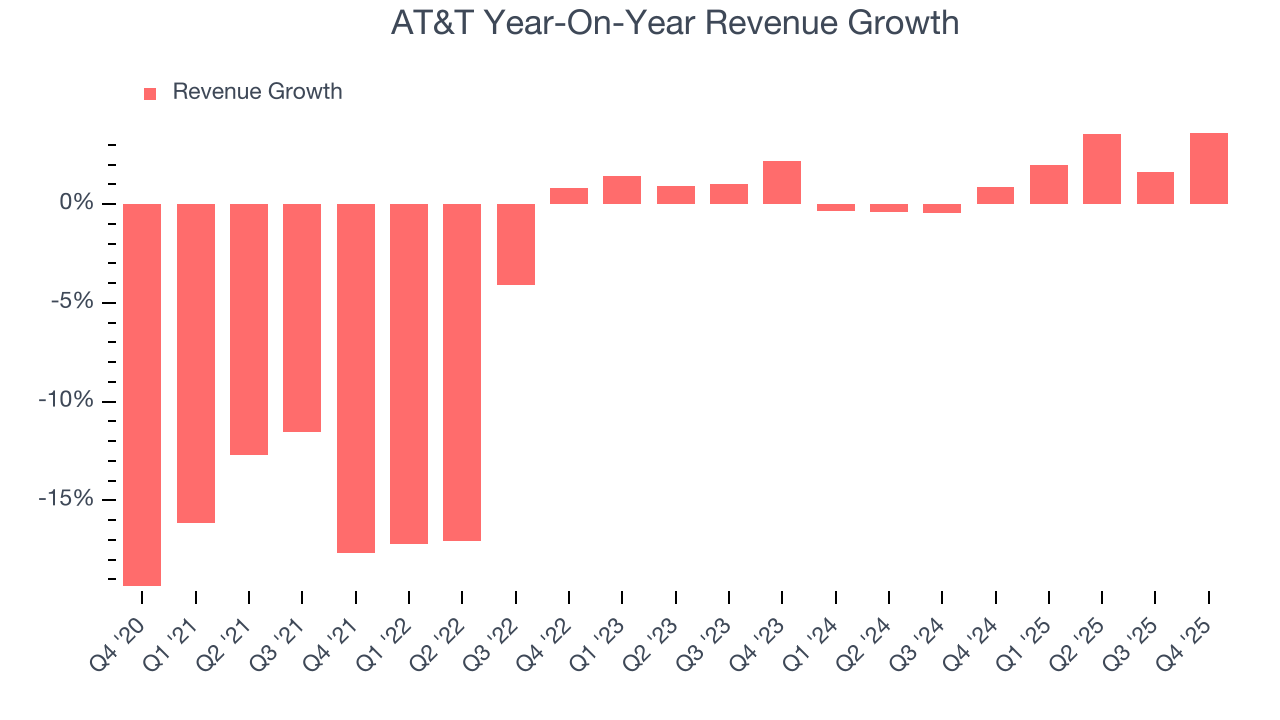

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. AT&T struggled to consistently generate demand over the last five years as its sales dropped at a 4.3% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. AT&T’s annualized revenue growth of 1.3% over the last two years is above its five-year trend, but we were still disappointed by the results.

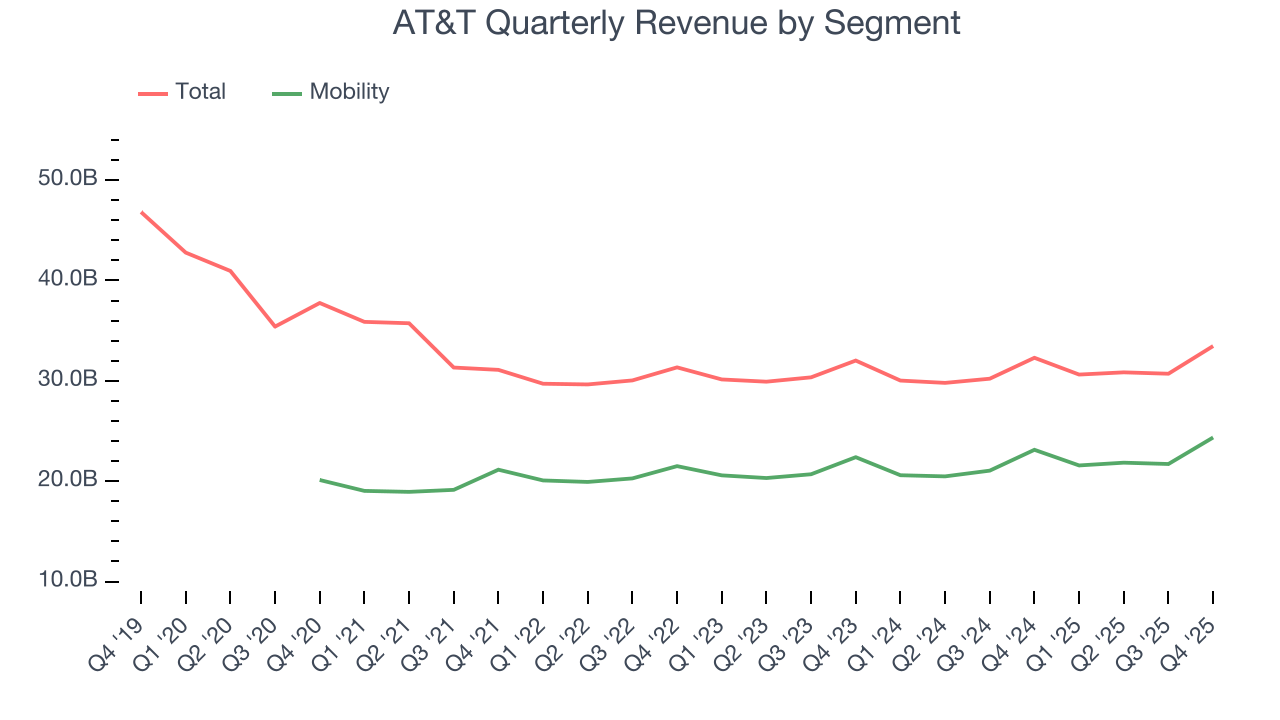

We can better understand the company’s revenue dynamics by analyzing its most important segment, Mobility. Over the last two years, AT&T’s Mobility revenue (wireless plans) averaged 3.2% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, AT&T reported modest year-on-year revenue growth of 3.6% but beat Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

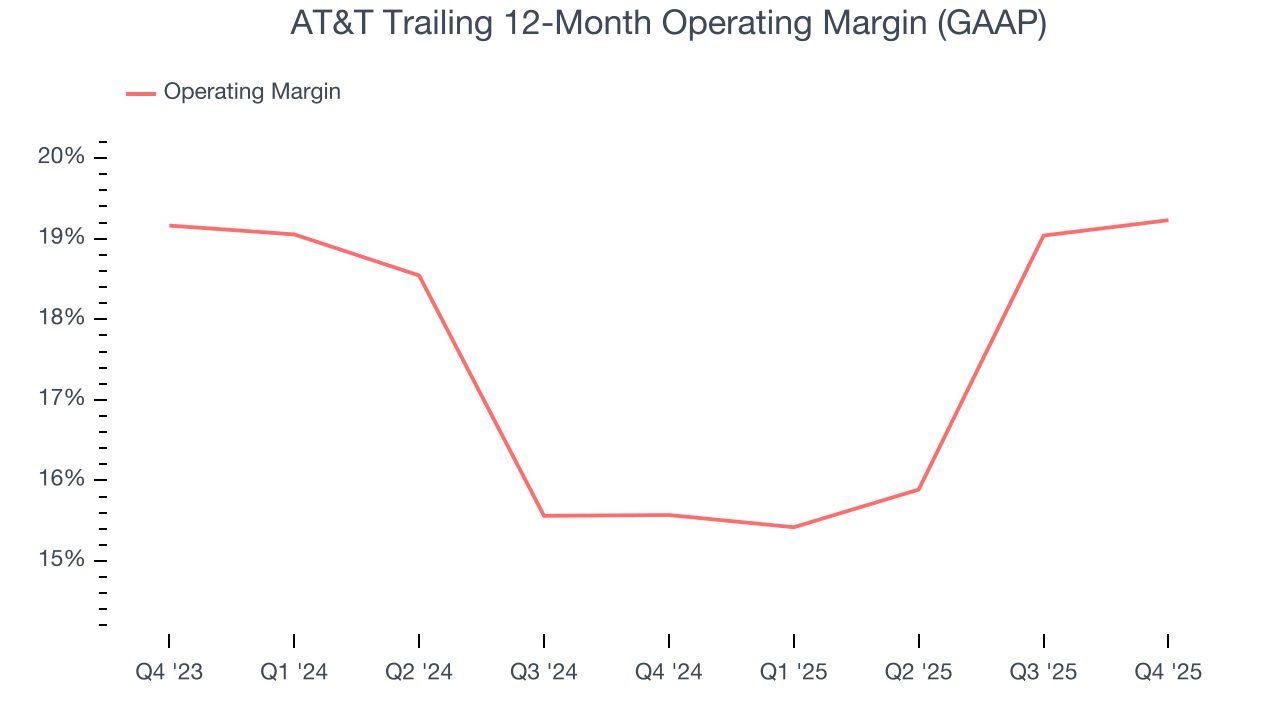

AT&T’s operating margin has been trending up over the last 12 months and averaged 17.4% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, AT&T generated an operating margin profit margin of 17.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

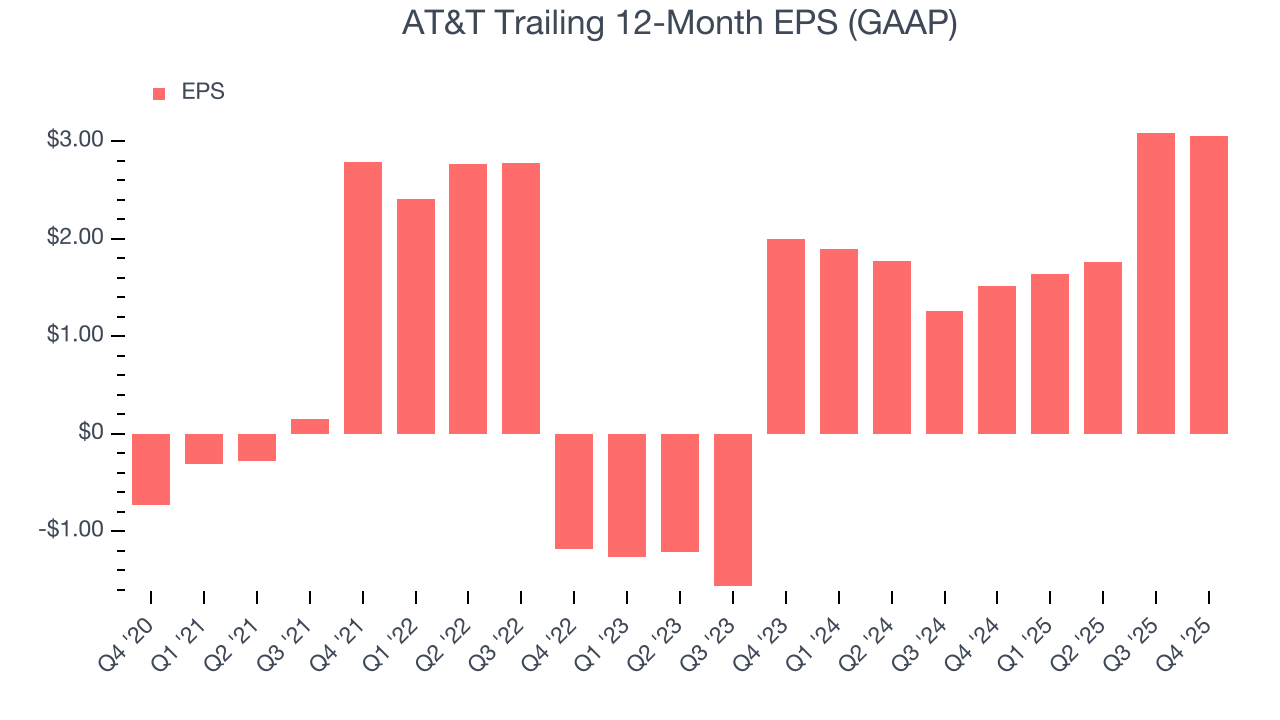

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

AT&T’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, AT&T reported EPS of $0.53, down from $0.57 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects AT&T’s full-year EPS of $3.05 to shrink by 27.8%.

8. Cash Is King

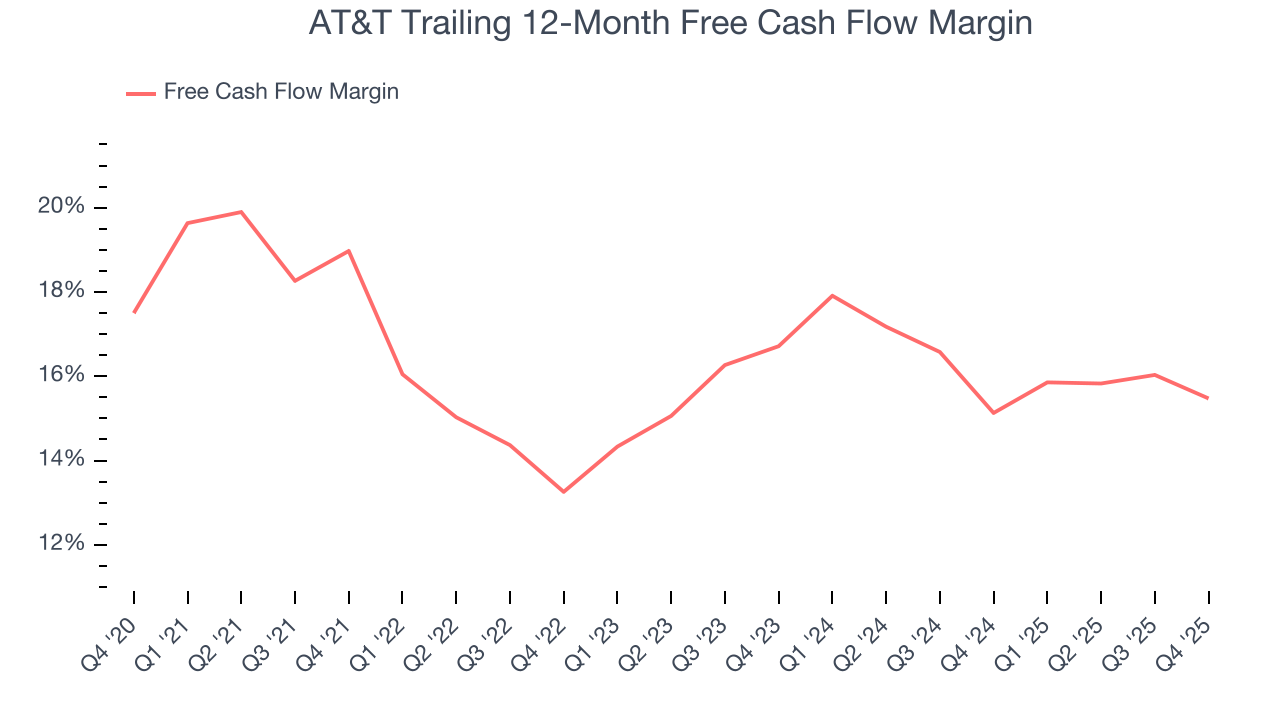

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

AT&T has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 15.3%, lousy for a consumer discretionary business.

AT&T’s free cash flow clocked in at $4.54 billion in Q4, equivalent to a 13.6% margin. The company’s cash profitability regressed as it was 2.1 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts’ consensus estimates show they’re expecting AT&T’s free cash flow margin of 15.5% for the last 12 months to remain the same.

9. Return on Invested Capital (ROIC)

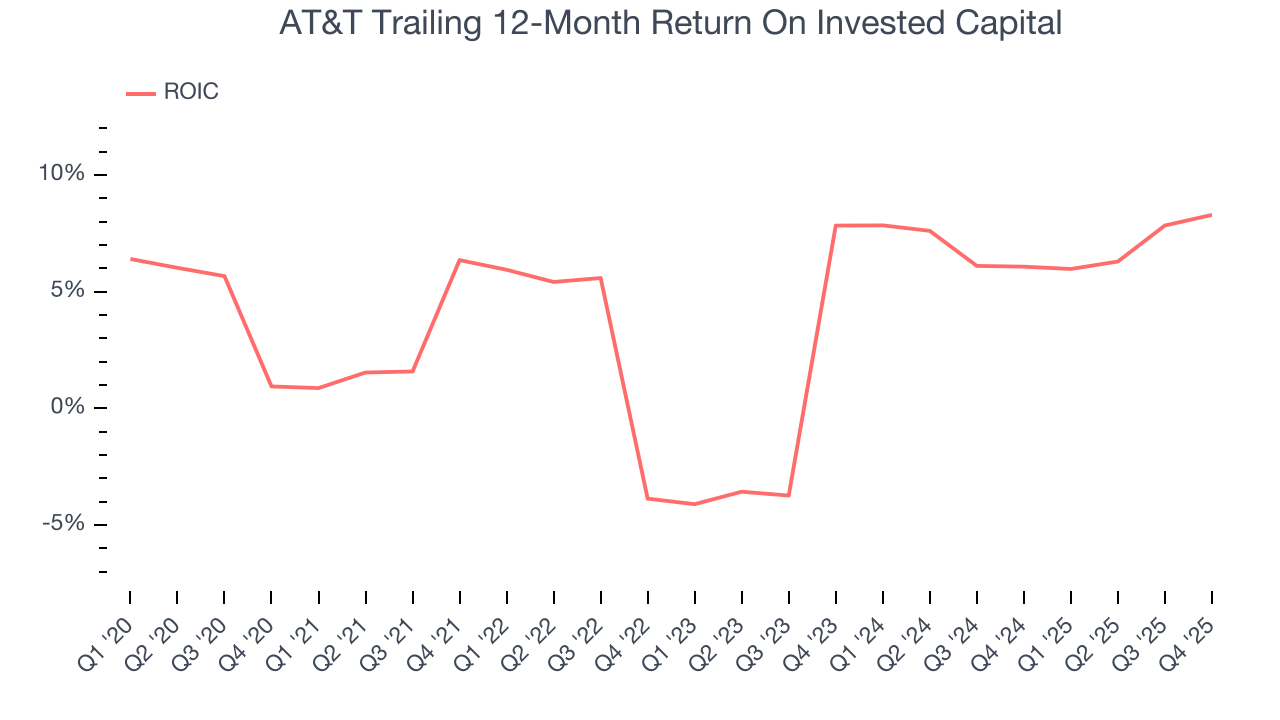

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

AT&T historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.9%, lower than the typical cost of capital (how much it costs to raise money) for consumer discretionary companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, AT&T’s has increased over the last few years. This is a good sign, and we hope the company can continue improving.

10. Balance Sheet Assessment

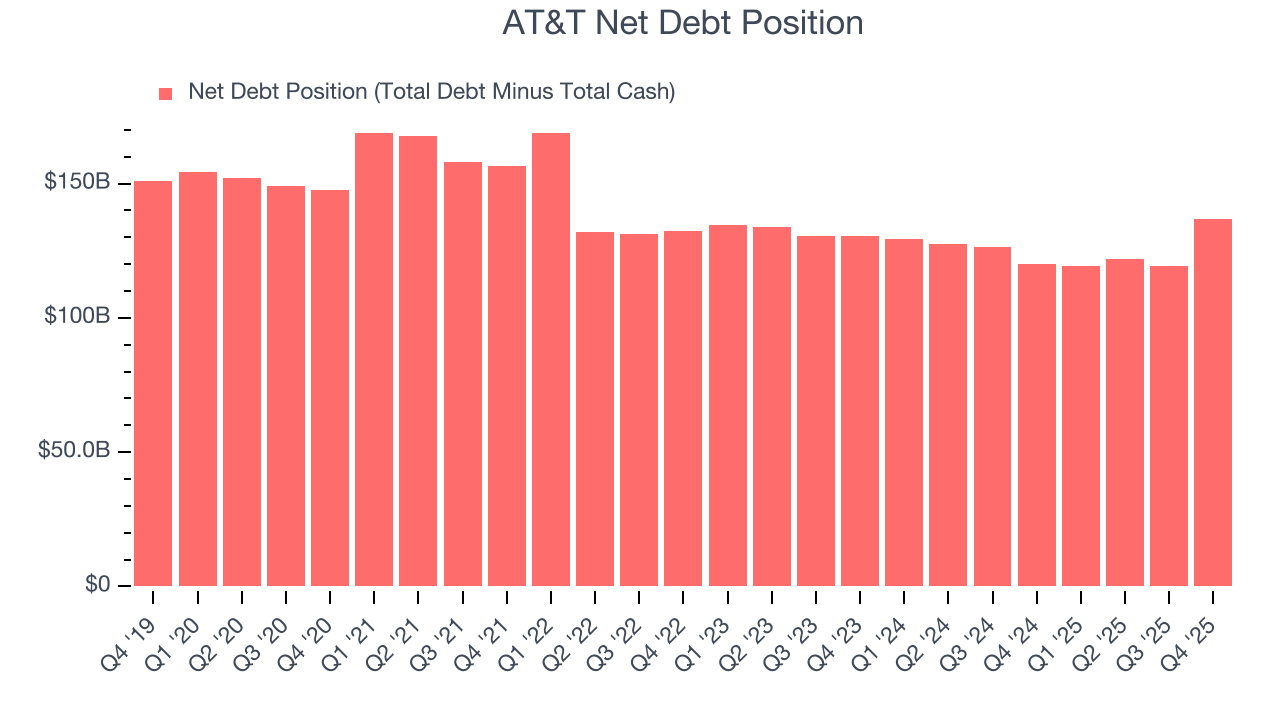

AT&T reported $18.23 billion of cash and $155 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $46.04 billion of EBITDA over the last 12 months, we view AT&T’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $3.22 billion of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from AT&T’s Q4 Results

It was good to see AT&T beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 3.7% to $23.87 immediately following the results.

12. Is Now The Time To Buy AT&T?

Updated: March 28, 2026 at 12:00 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

AT&T falls short of our quality standards. On top of that, AT&T’s Forecasted free cash flow margin suggests the company will ramp up its investments next year, and its declining EPS over the last five years makes it a less attractive asset to the public markets.

AT&T’s P/E ratio based on the next 12 months is 12.6x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $30.46 on the company (compared to the current share price of $29.08).