Teladoc (TDOC)

Teladoc doesn’t excite us. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Teladoc Is Not Exciting

Founded to help people in rural areas get online medical consultations, Teladoc Health (NYSE:TDOC) is a telemedicine platform that facilitates remote doctor’s visits.

- Focus on expanding its platform came at the expense of monetization as its average revenue per user fell by 8.5% annually

- Muted 1.7% annual revenue growth over the last three years shows its demand lagged behind its consumer internet peers

- The good news is that its earnings per share grew by 76.2% annually over the last three years, outpacing its peers

Teladoc is in the penalty box. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Teladoc

Teladoc’s stock price of $5.55 implies a valuation ratio of 4.2x forward EV/EBITDA. This sure is a cheap multiple, but you get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Teladoc (TDOC) Research Report: Q4 CY2025 Update

Digital medical services platform Teladoc Health (NYSE:TDOC) announced better-than-expected revenue in Q4 CY2025, but sales were flat year on year at $642.3 million. On the other hand, next quarter’s revenue guidance of $609 million was less impressive, coming in 3.8% below analysts’ estimates. Its GAAP loss of $0.14 per share was 24% above analysts’ consensus estimates.

Teladoc (TDOC) Q4 CY2025 Highlights:

- Revenue: $642.3 million vs analyst estimates of $635.9 million (flat year on year, 1% beat)

- EPS (GAAP): -$0.14 vs analyst estimates of -$0.18 (24% beat)

- Adjusted EBITDA: $83.78 million vs analyst estimates of $80.61 million (13% margin, 3.9% beat)

- Revenue Guidance for Q1 CY2026 is $609 million at the midpoint, below analyst estimates of $633.2 million

- EPS (GAAP) guidance for the upcoming financial year 2026 is -$0.90 at the midpoint, missing analyst estimates by 16.6%

- EBITDA guidance for the upcoming financial year 2026 is $287 million at the midpoint, below analyst estimates of $294.8 million

- Operating Margin: -5.6%, up from -7.5% in the same quarter last year

- Free Cash Flow Margin: 8.3%, down from 15.5% in the previous quarter

- U.S. Integrated Care Members: 101.8 million, up 8 million year on year

- Market Capitalization: $805.7 million

Company Overview

Founded to help people in rural areas get online medical consultations, Teladoc Health (NYSE:TDOC) is a telemedicine platform that facilitates remote doctor’s visits.

The company's key product is their virtual care platform, which allows patients to connect with licensed healthcare providers through a secure online portal or mobile app. Patients can get virtual consultations for a range of medical issues such as mental health, dermatology, and respiratory health.

The customer problem that Teladoc's product solves is access to proper healthcare. Many people, especially those in rural areas, have limited access to doctors or specialists. These individuals may be elderly or in poor health, making it difficult to travel long distances for medical care. Teladoc's platform enables medical consultations from home. Over time, though, a broader population has adopted the platform due to convenience and time saved.

Teladoc generates revenue by charging a fee for each virtual consultation, which varies depending on the type of service provided. A virtual consultation with a primary care physician may cost $75, while a therapy session may cost $150. The healthcare providers who partner with Teladoc are paid by the company for each virtual consultation, and fees also vary by service and specialty. Teladoc also generates revenue by partnering with insurance companies and employers to provide telemedicine services to their members or employees.

4. Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors offering online legal or document services include Doximity (NYSE:DOCS) and private companies Sesame Health and MDLive.

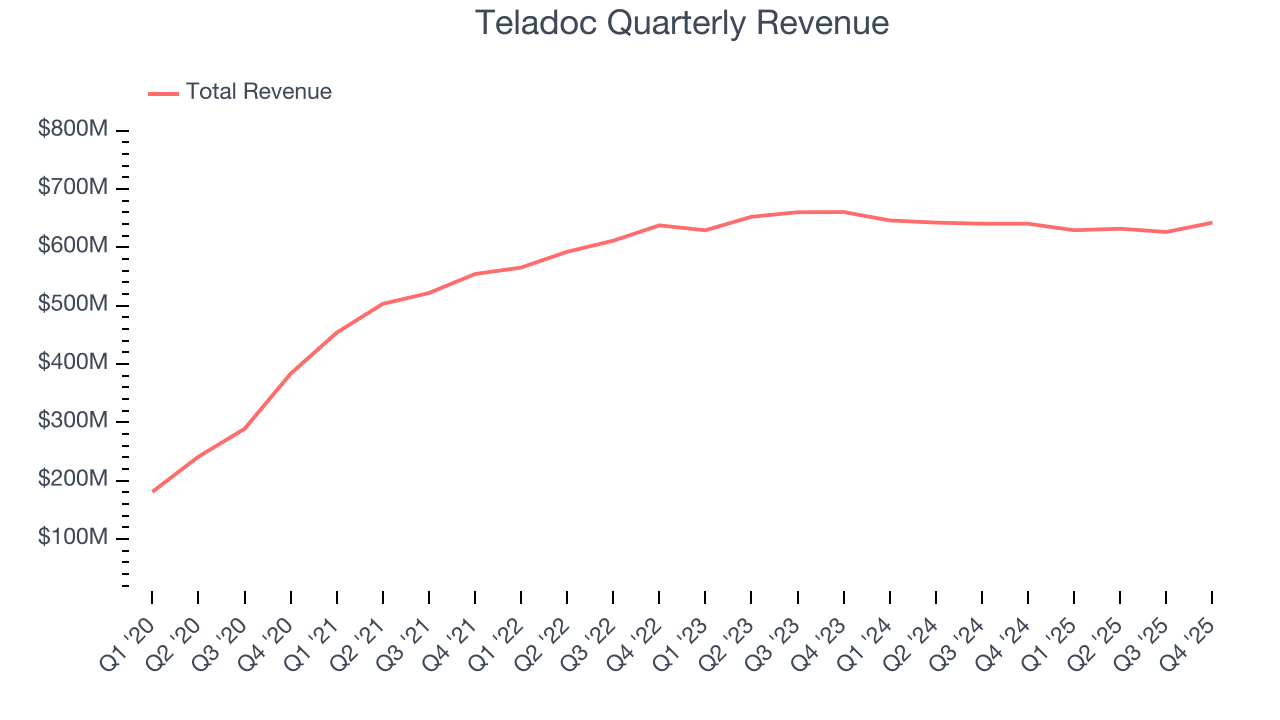

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Teladoc’s sales grew at a weak 1.7% compounded annual growth rate over the last three years. This fell short of our benchmarks and is a poor baseline for our analysis.

This quarter, Teladoc’s $642.3 million of revenue was flat year on year but beat Wall Street’s estimates by 1%. Company management is currently guiding for a 3.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and suggests its newer products and services will not accelerate its top-line performance yet.

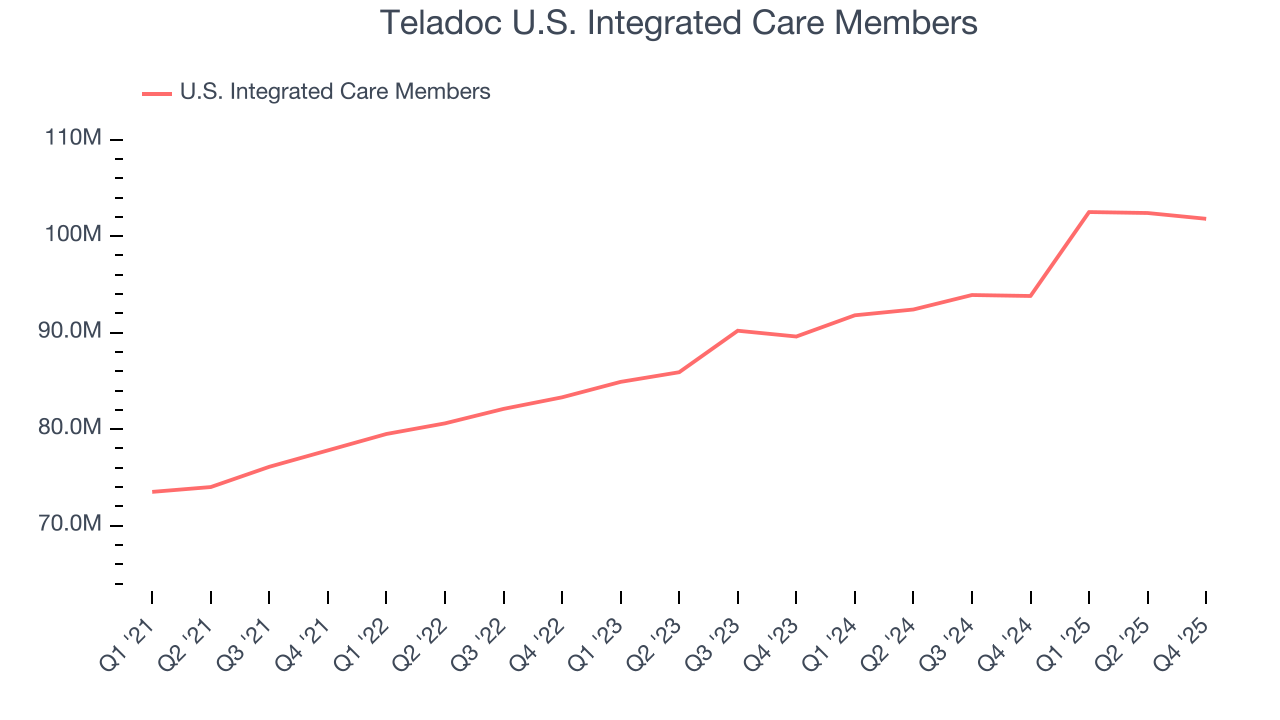

6. U.S. Integrated Care Members

User Growth

As an online marketplace, Teladoc generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, Teladoc’s u.s. integrated care members, a key performance metric for the company, increased by 7.9% annually to 101.8 million in the latest quarter. This growth rate is decent for a consumer internet business and indicates people enjoy using its offerings.

In Q4, Teladoc added 8 million u.s. integrated care members, leading to 8.5% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

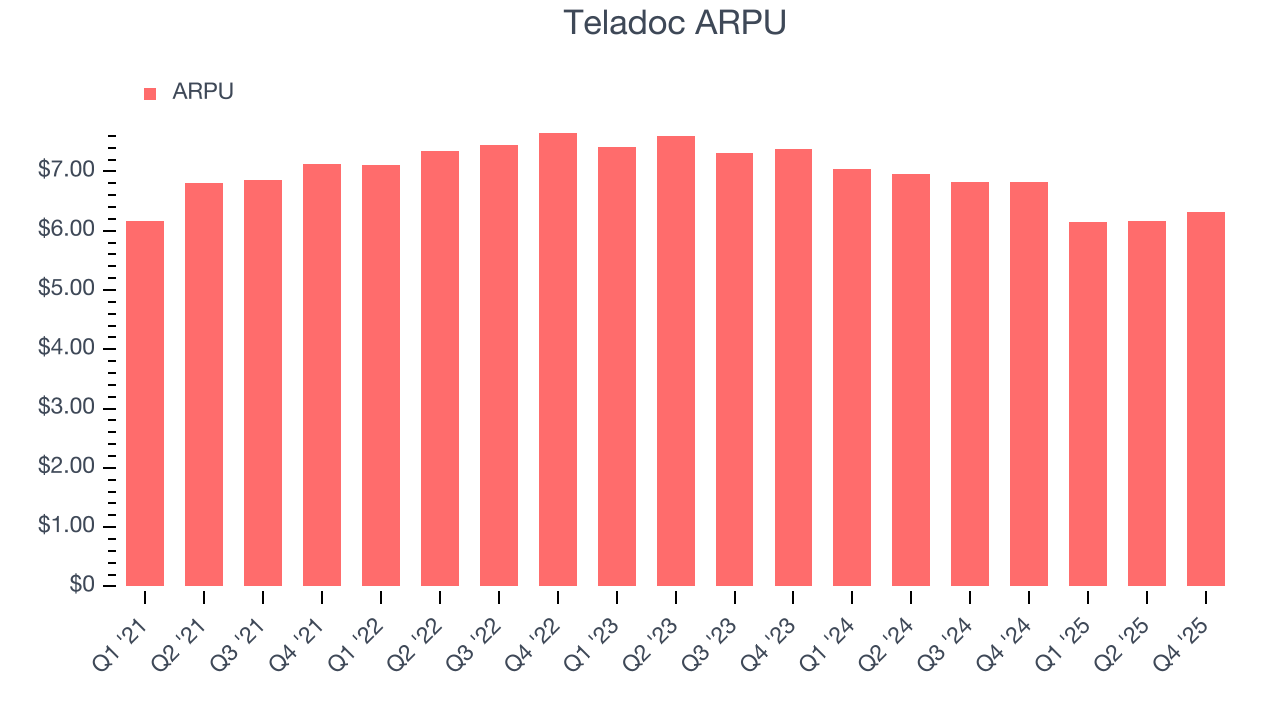

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and Teladoc’s take rate, or "cut", on each order.

Teladoc’s ARPU fell over the last two years, averaging 8.5% annual declines. This isn’t great, but the increase in u.s. integrated care members is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Teladoc tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, Teladoc’s ARPU clocked in at $6.31. It declined 7.6% year on year, worse than the change in its u.s. integrated care members.

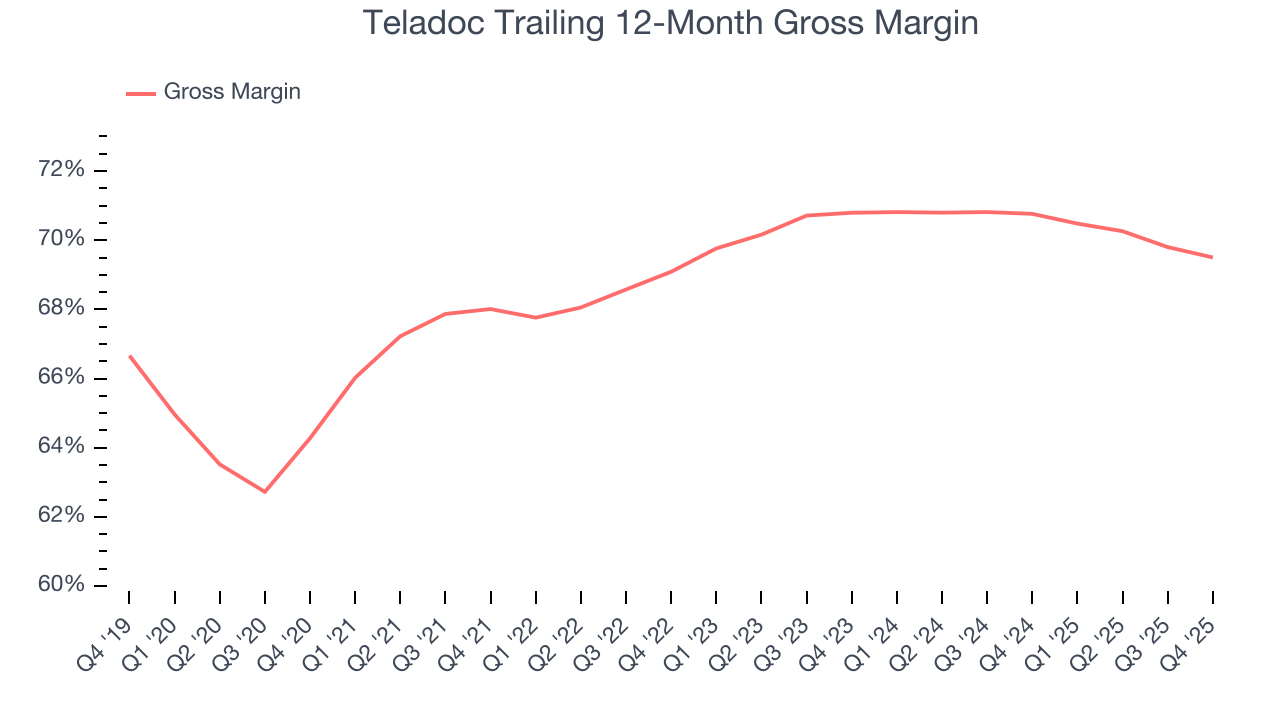

7. Gross Margin & Pricing Power

For online marketplaces like Teladoc, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

Teladoc has robust unit economics, an output of its asset-lite business model and pricing power. Its margin is better than the broader consumer internet industry and enables the company to fund large investments in new products and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 70.1% gross margin over the last two years. That means Teladoc only paid its providers $29.86 for every $100 in revenue.

In Q4, Teladoc produced a 69.3% gross profit margin, down 1.2 percentage points year on year. Teladoc’s full-year margin has also been trending down over the past 12 months, decreasing by 1.3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

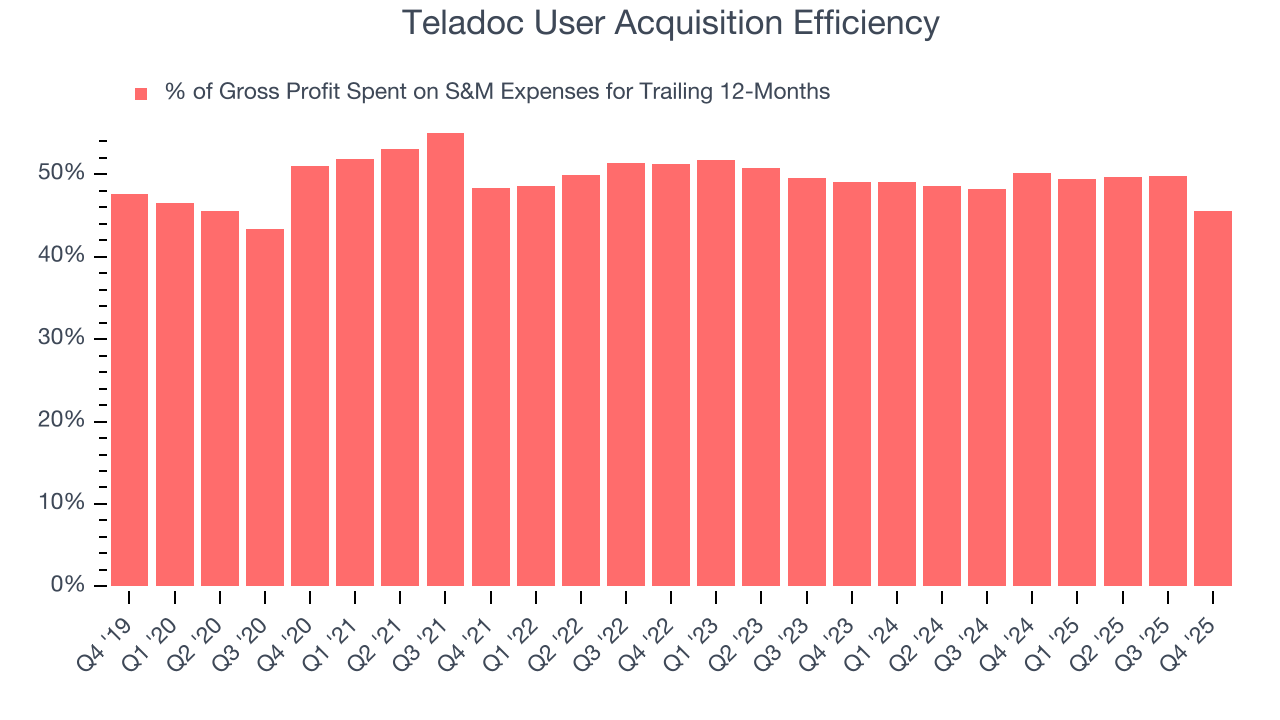

8. User Acquisition Efficiency

Consumer internet businesses like Teladoc grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s relatively expensive for Teladoc to acquire new users as the company has spent 45.6% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates that Teladoc operates in a competitive market and must continue investing to maintain an acceptable growth trajectory.

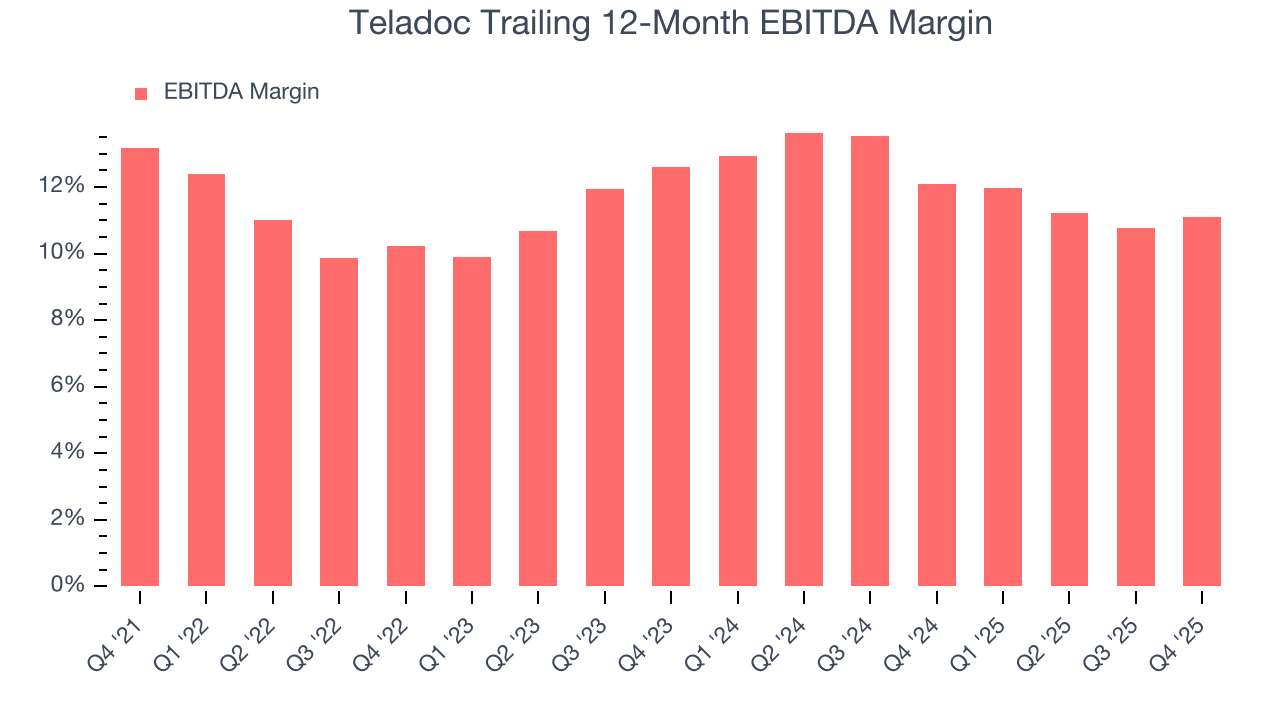

9. EBITDA

Teladoc’s EBITDA margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 11.6% over the last two years. This profitability was top-notch for a consumer internet business, showing it’s an well-run company with an efficient cost structure. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Teladoc’s EBITDA margin might fluctuated slightly but has generally stayed the same over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Teladoc generated an EBITDA margin profit margin of 13%, up 1.4 percentage points year on year. The increase was encouraging, and because its gross margin actually decreased, we can assume it was more efficient because its operating expenses like marketing, R&D, and administrative overhead grew slower than its revenue.

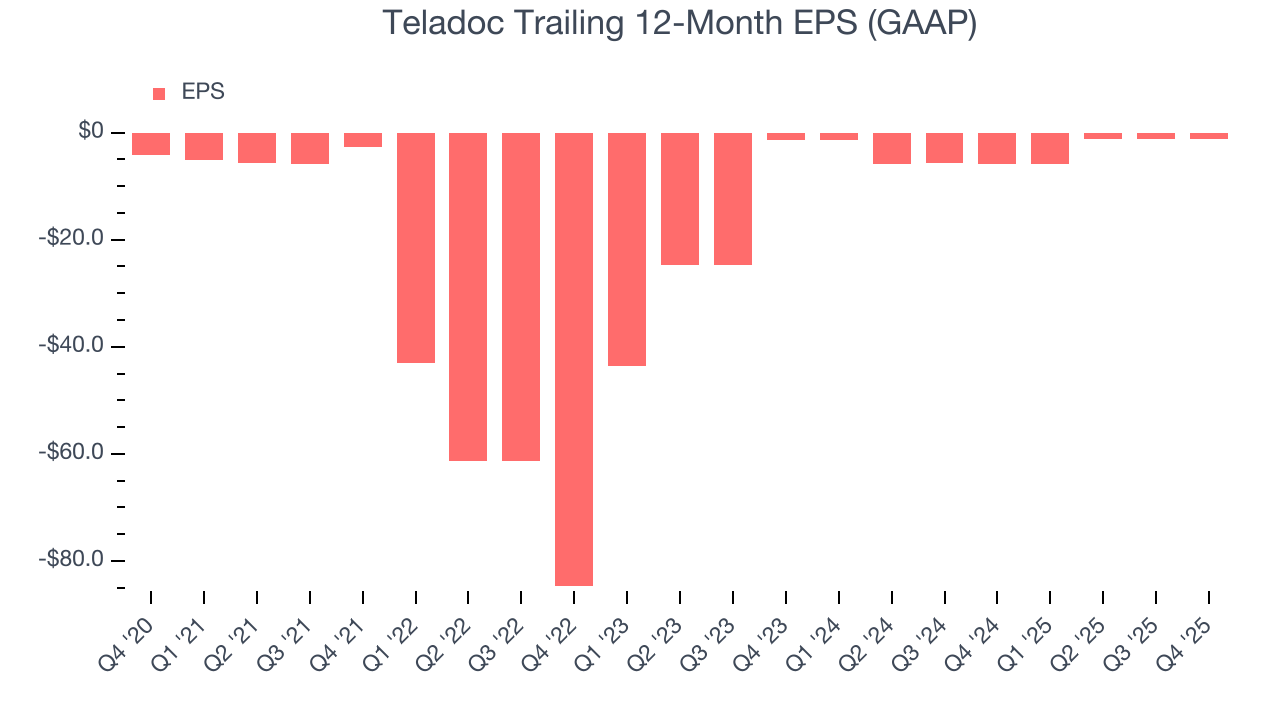

10. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Teladoc’s full-year earnings are still negative, it reduced its losses and improved its EPS by 76.2% annually over the last three years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, Teladoc reported EPS of negative $0.14, up from negative $0.28 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Teladoc to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.14 will advance to negative $0.74.

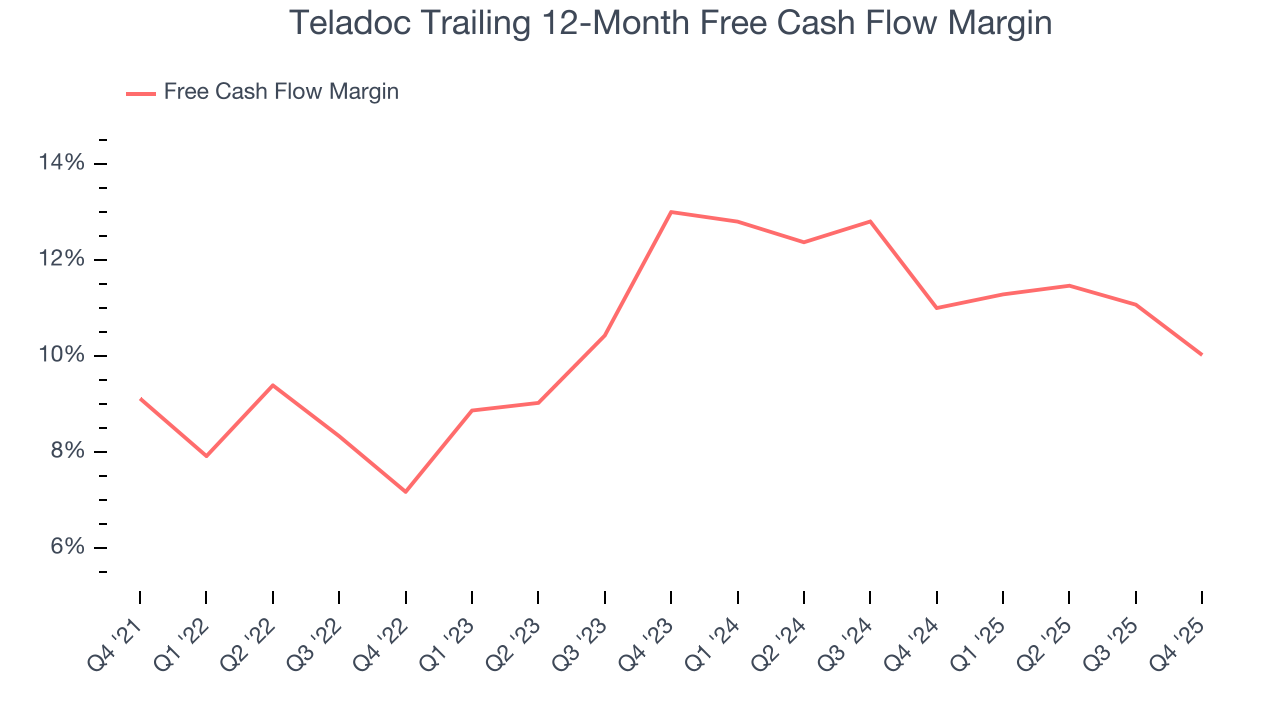

11. Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Teladoc has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.5% over the last two years, better than the broader consumer internet sector.

Taking a step back, we can see that Teladoc’s margin expanded by 2.9 percentage points over the last few years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Teladoc’s free cash flow clocked in at $53.42 million in Q4, equivalent to a 8.3% margin. The company’s cash profitability regressed as it was 4.1 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

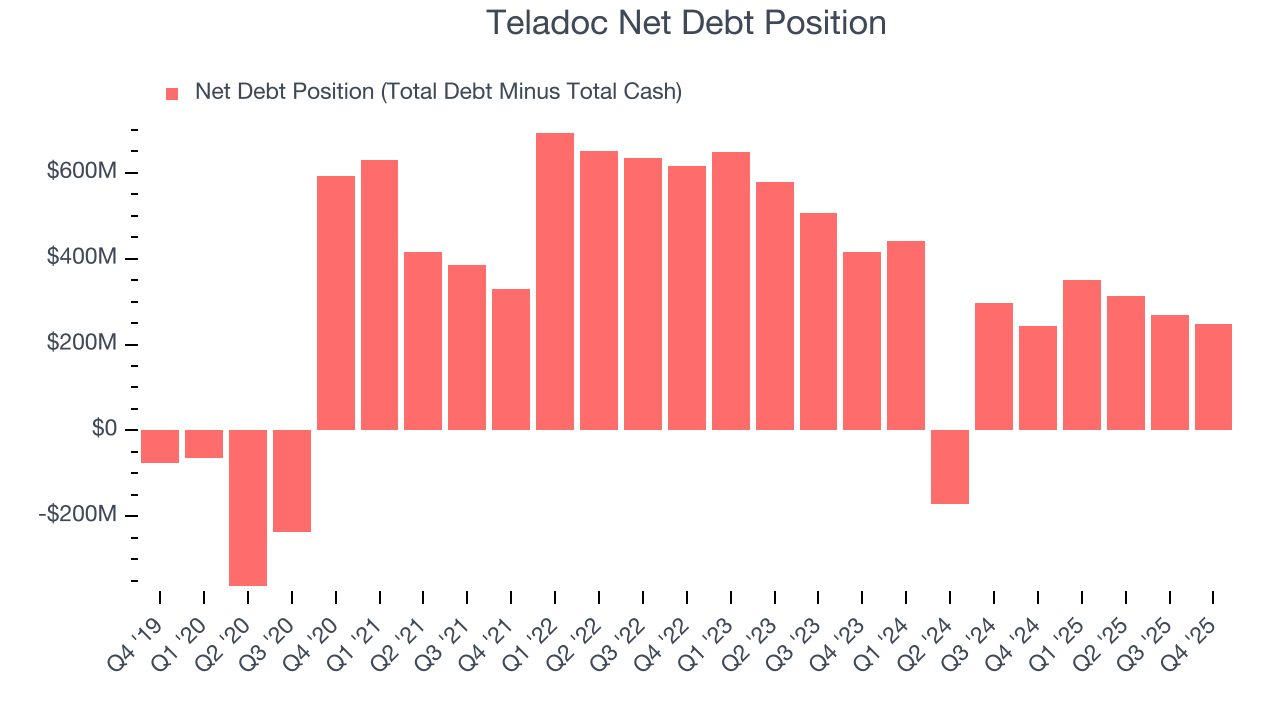

12. Balance Sheet Assessment

Teladoc reported $781.1 million of cash and $1.03 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $281.1 million of EBITDA over the last 12 months, we view Teladoc’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $17.06 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Teladoc’s Q4 Results

We enjoyed seeing Teladoc beat analysts’ EBITDA expectations this quarter. We were also glad it expanded its number of users. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $4.64 immediately following the results.

14. Is Now The Time To Buy Teladoc?

Updated: March 17, 2026 at 10:38 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Teladoc, you should also grasp the company’s longer-term business quality and valuation.

Teladoc isn’t a terrible business, but it isn’t one of our picks. For starters, its revenue growth was weak over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its EPS growth over the last three years has been fantastic, the downside is its ARPU has declined over the last two years. On top of that, its sales and marketing efficiency is mediocre.

Teladoc’s EV/EBITDA ratio based on the next 12 months is 4.2x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $7.12 on the company (compared to the current share price of $5.55).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.