Tapestry (TPR)

We wouldn’t recommend Tapestry. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Tapestry Will Underperform

Originally founded as Coach, Tapestry (NYSE:TPR) is an American fashion conglomerate with a portfolio of luxury brands offering high-quality accessories and fashion products.

- Sales trends were unexciting over the last five years as its 8.6% annual growth was below the typical consumer discretionary company

- Responsiveness to unforeseen market trends is restricted due to its substandard operating margin profitability

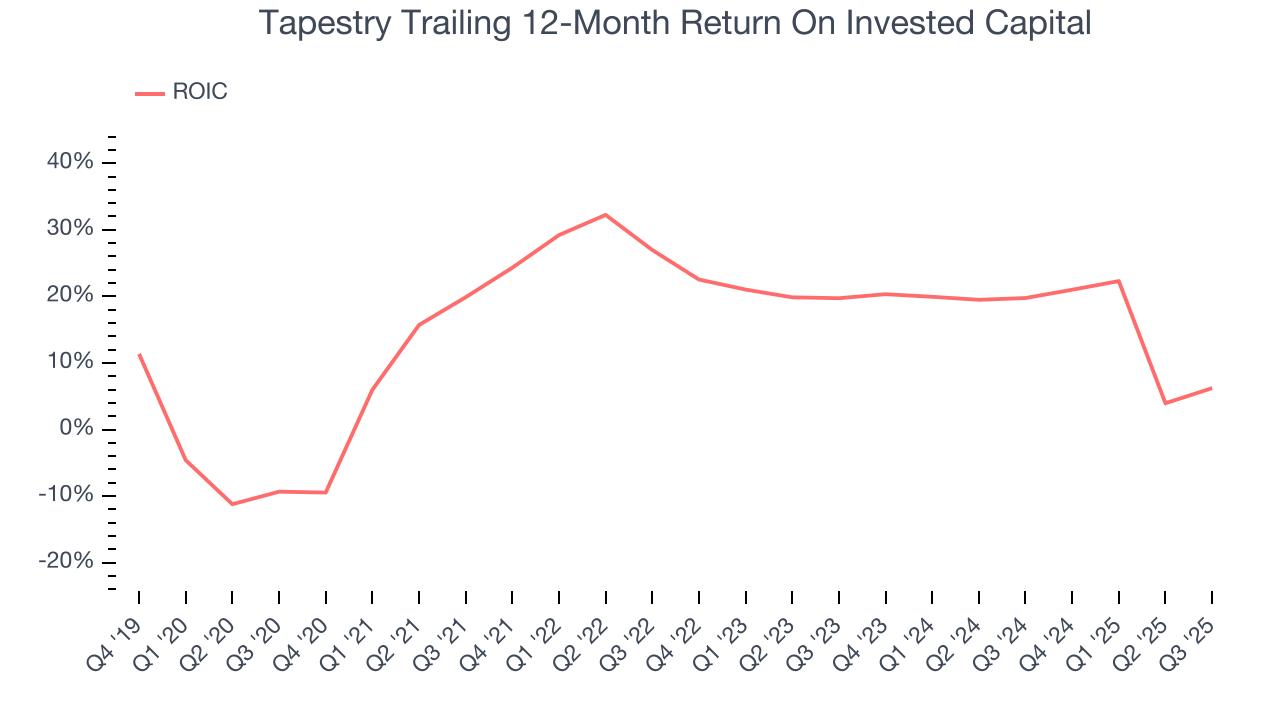

- ROIC of 18.5% reflects management’s challenges in identifying attractive investment opportunities, and its shrinking returns suggest its past profit sources are losing steam

Tapestry’s quality is insufficient. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Tapestry

Tapestry’s stock price of $130.29 implies a valuation ratio of 23x forward P/E. Not only does Tapestry trade at a premium to companies in the consumer discretionary space, but this multiple is also high for its top-line growth.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Tapestry (TPR) Research Report: Q3 CY2025 Update

Luxury fashion conglomerate Tapestry (NYSE:TPR) reported Q3 CY2025 results beating Wall Street’s revenue expectations, with sales up 13.1% year on year to $1.70 billion. The company’s full-year revenue guidance of $7.3 billion at the midpoint came in 0.9% above analysts’ estimates. Its GAAP profit of $1.28 per share was 2.6% above analysts’ consensus estimates.

Tapestry (TPR) Q3 CY2025 Highlights:

- Revenue: $1.70 billion vs analyst estimates of $1.64 billion (13.1% year-on-year growth, 4.1% beat)

- EPS (GAAP): $1.28 vs analyst estimates of $1.25 (2.6% beat)

- Adjusted EBITDA: $431.2 million vs analyst estimates of $379.1 million (25.3% margin, 13.7% beat)

- The company lifted its revenue guidance for the full year to $7.3 billion at the midpoint from $7.2 billion, a 1.4% increase

- EPS (GAAP) guidance for the full year is $5.53 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 19.3%, up from 16.7% in the same quarter last year

- Free Cash Flow Margin: 4.7%, down from 6.2% in the same quarter last year

- Constant Currency Revenue rose 21% year on year (0% in the same quarter last year)

- Market Capitalization: $22.63 billion

Company Overview

Originally founded as Coach, Tapestry (NYSE:TPR) is an American fashion conglomerate with a portfolio of luxury brands offering high-quality accessories and fashion products.

Coach, the cornerstone brand of the company that was founded in 1941, became a leader in the luxury leather goods market, offering iconic high-quality handbags. With an expanding vision, the company evolved to encompass other notable brands in the luxury market such as Kate Spade New York and Stuart Weitzman.

In 2017, Coach rebranded to Tapestry to better mirror its multi-brand identity. The company allows each brand to retain its uniqueness while leveraging Tapestry's vast resources, creating synergies.

In late 2024, the proposed Tapestry-Capri merger was called off after a US judge blocked the deal due to antitrust concerns.

4. Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Tapestry’s main competitors are PVH Corp (NYSE:PVH) who owns Calvin Klein and Tommy Hilfiger; Kering (OTCMKTS:PPRUY) who owns Gucci, Yves Saint Laurent, and Bottega Veneta; LVMH Moët Hennessy Louis Vuitton (OTCMKTS:LVMUY) who owns Louis Vuitton, Dior, Givenchy; Ralph Lauren (NYSE:RL)

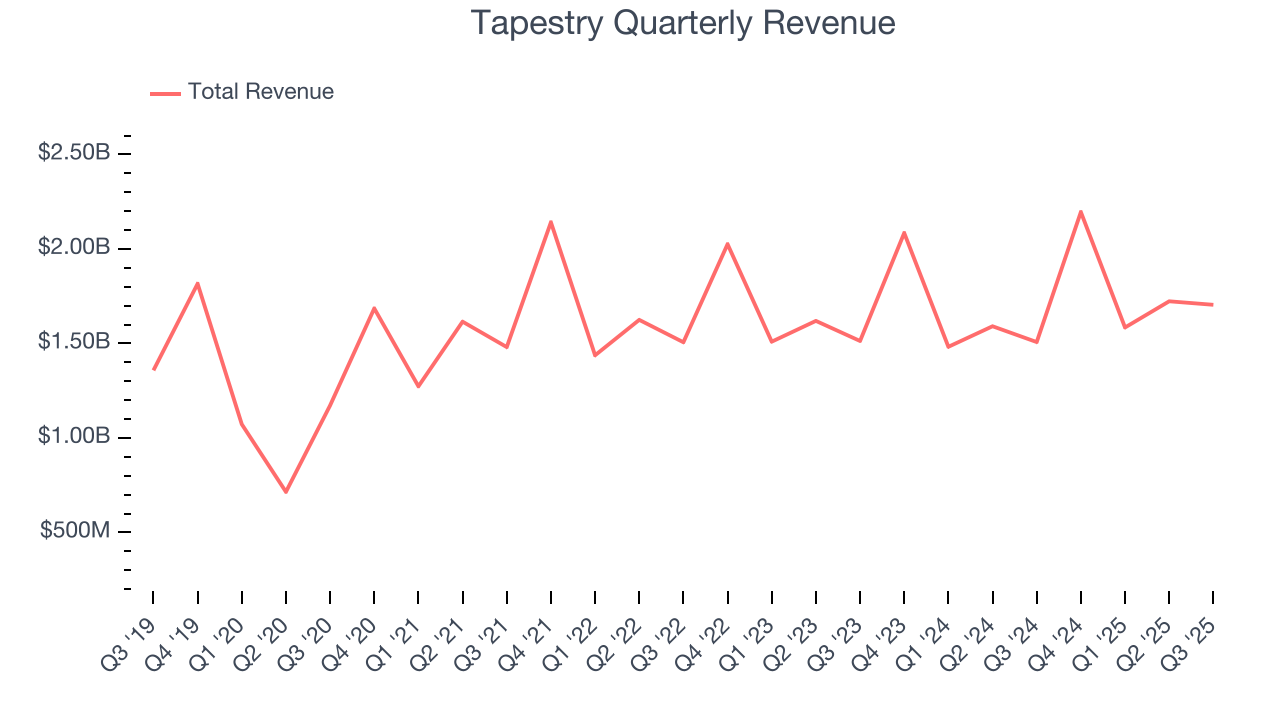

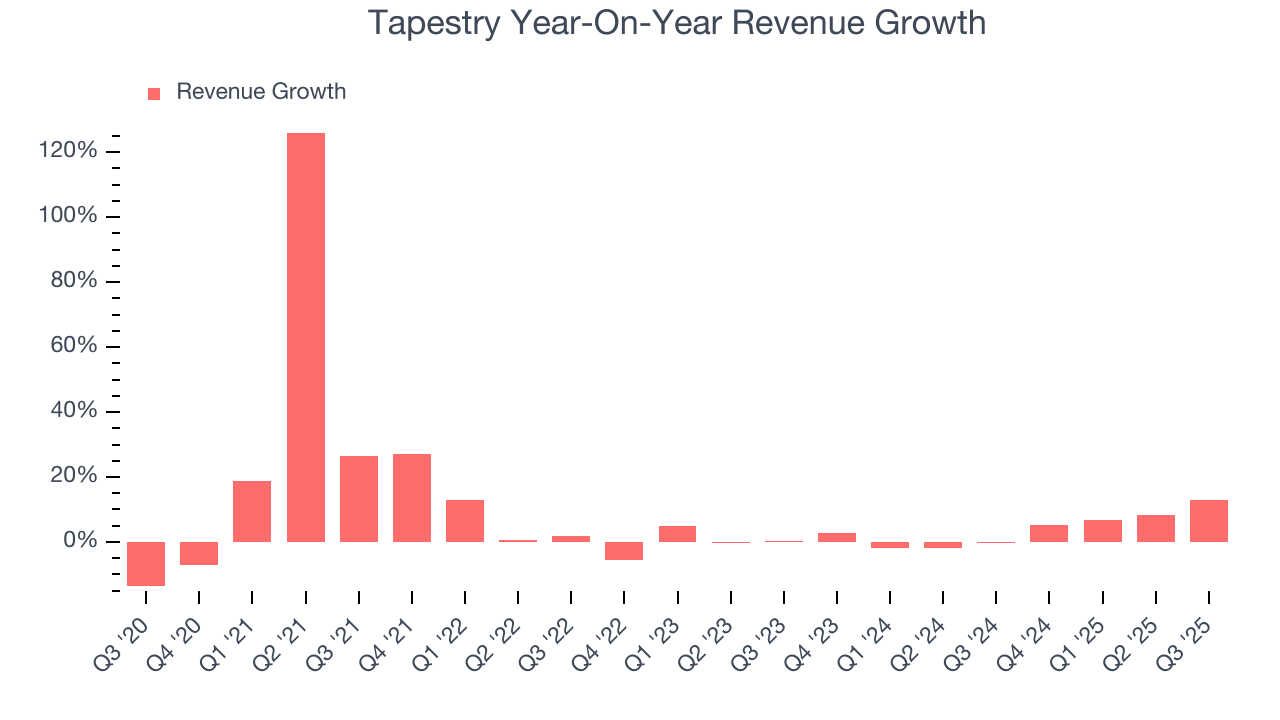

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Tapestry’s 8.6% annualized revenue growth over the last five years was sluggish. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Tapestry’s recent performance shows its demand has slowed as its annualized revenue growth of 4% over the last two years was below its five-year trend.

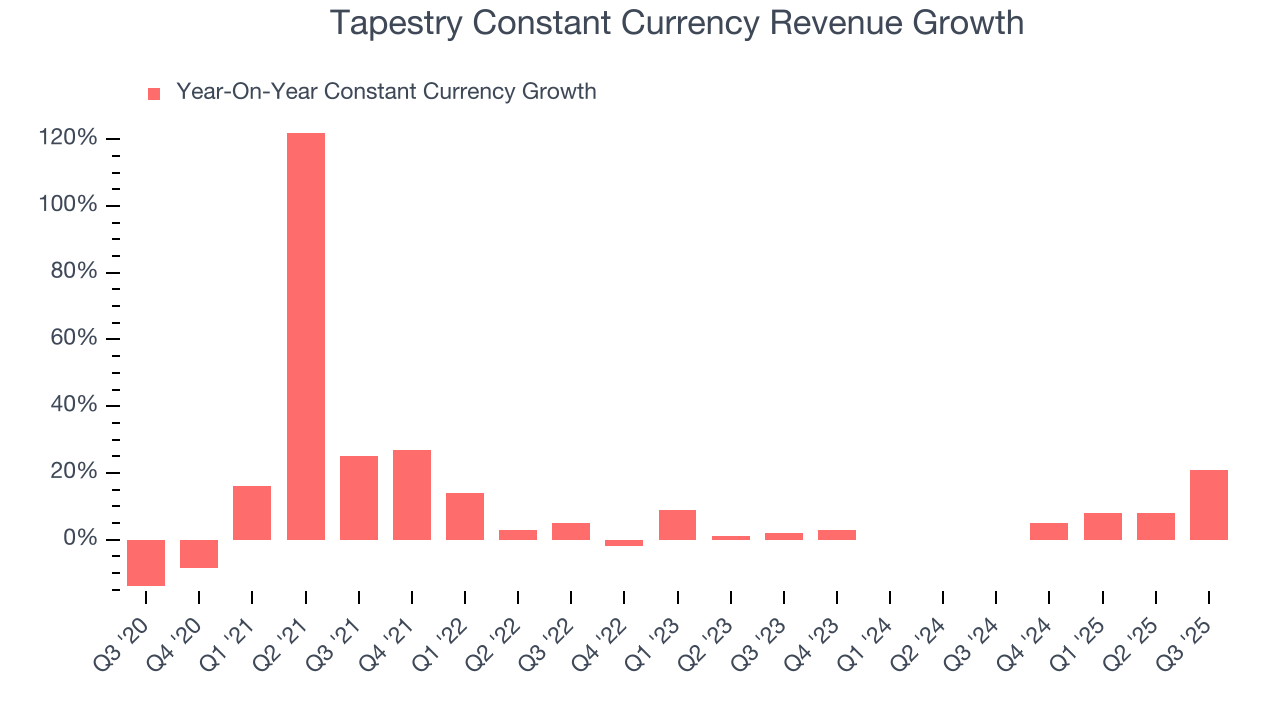

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.6% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Tapestry.

This quarter, Tapestry reported year-on-year revenue growth of 13.1%, and its $1.70 billion of revenue exceeded Wall Street’s estimates by 4.1%.

Looking ahead, sell-side analysts expect revenue to grow 1.2% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

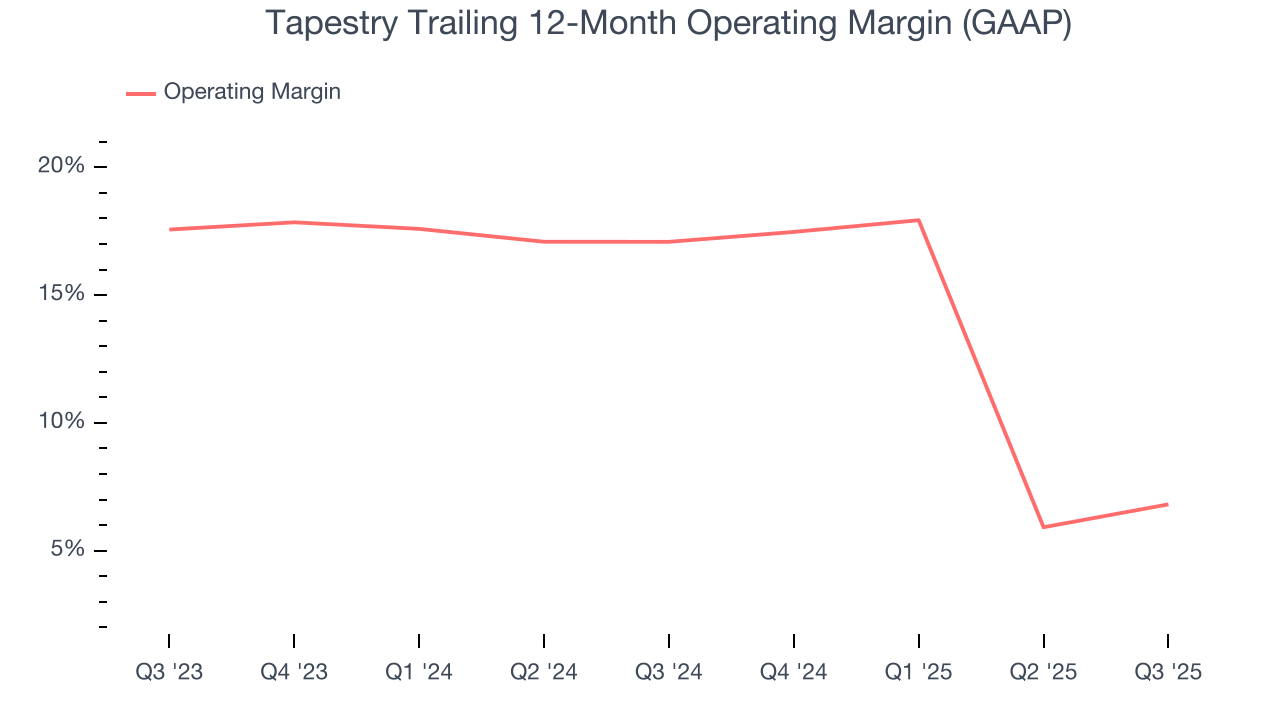

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Tapestry’s operating margin has shrunk over the last 12 months, but it still averaged 11.7% over the last two years, decent for a consumer discretionary business. This shows it generally does a decent job managing its expenses.

This quarter, Tapestry generated an operating margin profit margin of 19.3%, up 2.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

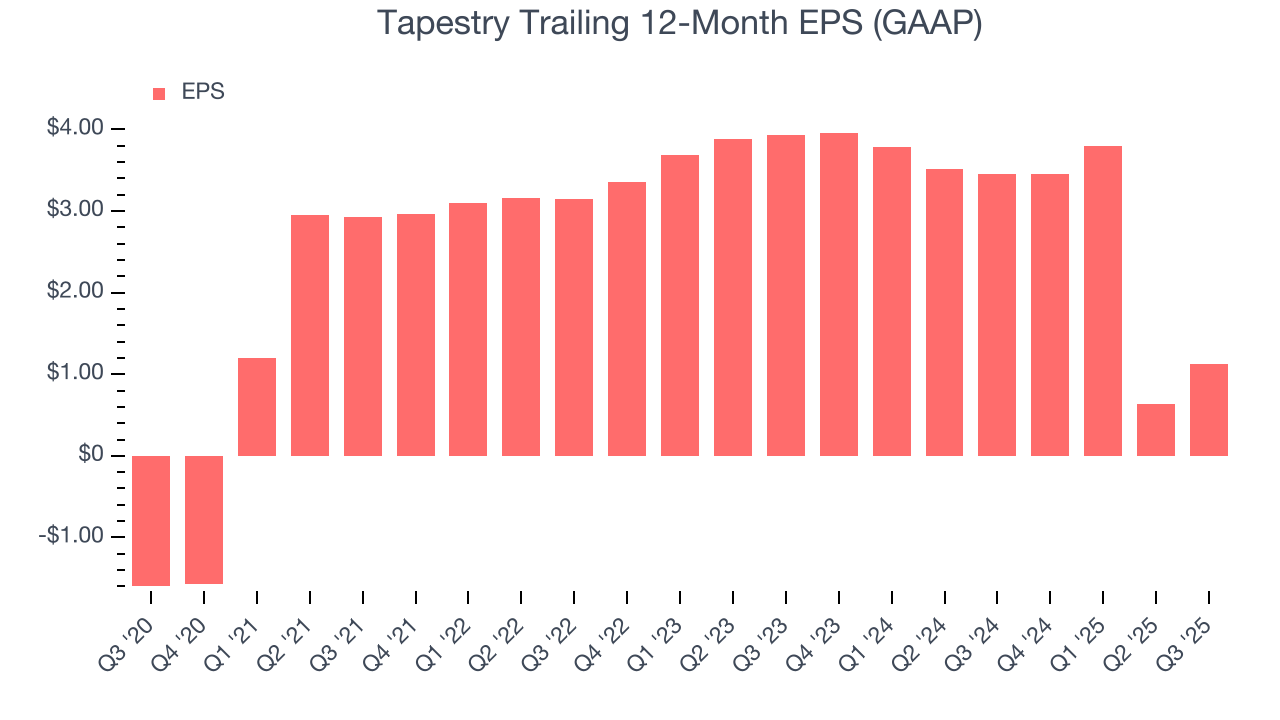

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tapestry’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Tapestry reported EPS of $1.28, up from $0.79 in the same quarter last year. This print beat analysts’ estimates by 2.6%. Over the next 12 months, Wall Street expects Tapestry’s full-year EPS of $1.12 to grow 386%.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

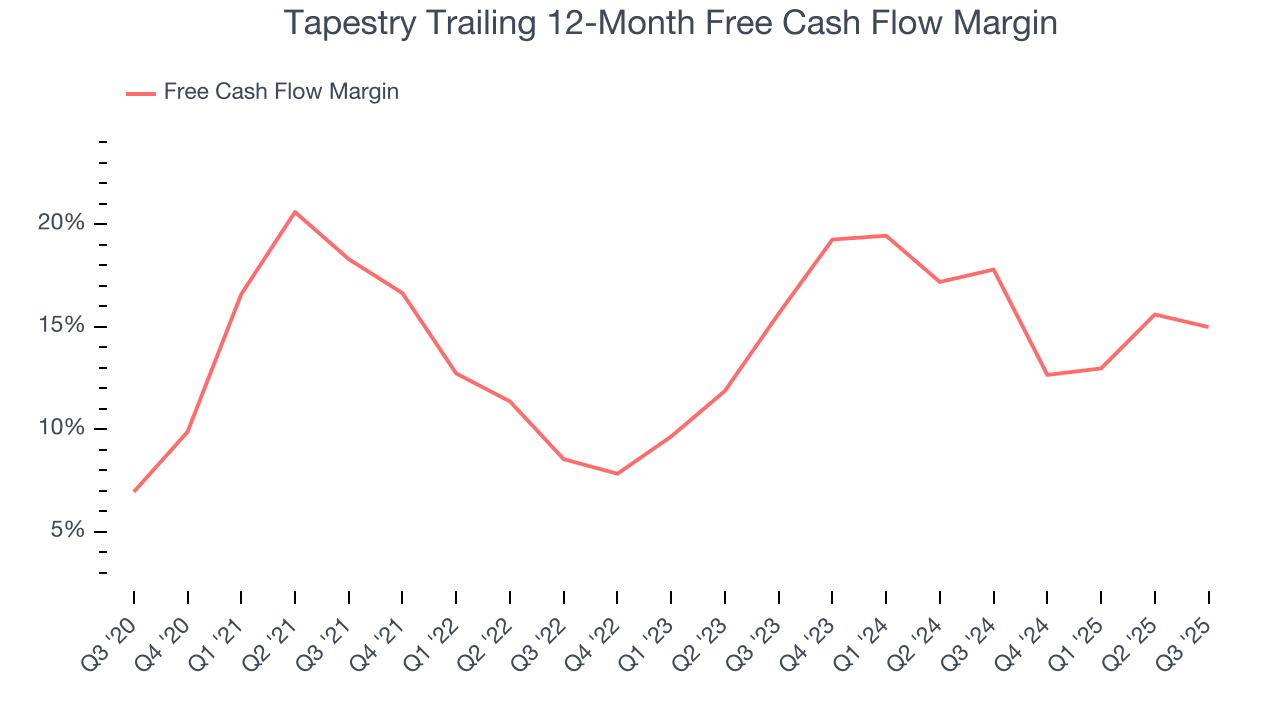

Tapestry has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 16.3% over the last two years, quite impressive for a consumer discretionary business.

Tapestry’s free cash flow clocked in at $80.2 million in Q3, equivalent to a 4.7% margin. The company’s cash profitability regressed as it was 1.5 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Tapestry hasn’t been the highest-quality company lately because of its poor top-line performance, it historically found a few growth initiatives that worked. Its five-year average ROIC was 18.5%, higher than most consumer discretionary businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Tapestry’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

10. Balance Sheet Assessment

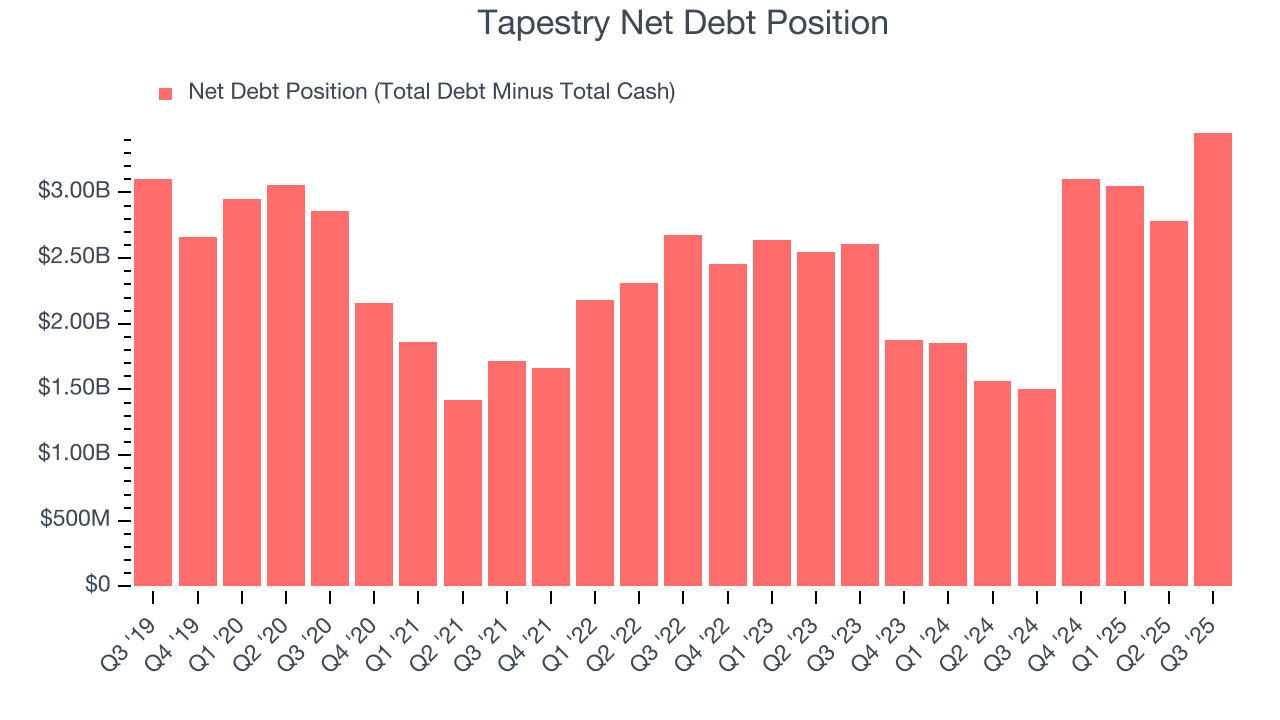

Tapestry reported $743.2 million of cash and $4.20 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.67 billion of EBITDA over the last 12 months, we view Tapestry’s 2.1× net-debt-to-EBITDA ratio as safe. We also see its $65.8 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Tapestry’s Q3 Results

We were impressed by how significantly Tapestry blew past analysts’ constant currency revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 13.7% to $94.28 immediately after reporting.

12. Is Now The Time To Buy Tapestry?

Updated: January 24, 2026 at 9:46 PM EST

Are you wondering whether to buy Tapestry or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Tapestry falls short of our quality standards. To begin with, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its constant currency sales performance has disappointed. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Tapestry’s P/E ratio based on the next 12 months is 23x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $133.61 on the company (compared to the current share price of $130.29).