VF Corp (VFC)

VF Corp is up against the odds. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think VF Corp Will Underperform

Owner of The North Face, Vans, and Supreme, VF Corp (NYSE:VFC) is a clothing conglomerate specializing in branded lifestyle apparel, footwear, and accessories.

- Sales stagnated over the last five years and signal the need for new growth strategies

- Earnings per share fell by 11.6% annually over the last five years while its revenue was flat, showing each sale was less profitable

- High net-debt-to-EBITDA ratio of 6× increases the risk of forced asset sales or dilutive financing if operational performance weakens

VF Corp doesn’t live up to our standards. There are better opportunities in the market.

Why There Are Better Opportunities Than VF Corp

VF Corp is trading at $20.12 per share, or 25.1x forward P/E. Not only is VF Corp’s multiple richer than most consumer discretionary peers, but it’s also expensive for its revenue characteristics.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. VF Corp (VFC) Research Report: Q4 CY2025 Update

Lifestyle clothing conglomerate VF Corp (NYSE:VFC) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 4.9% year on year to $2.83 billion. On the other hand, next quarter’s revenue guidance of $2.02 billion was less impressive, coming in 2.5% below analysts’ estimates. Its non-GAAP profit of $0.61 per share was 37.9% above analysts’ consensus estimates.

VF Corp (VFC) Q4 CY2025 Highlights:

- Revenue: $2.83 billion vs analyst estimates of $2.75 billion (4.9% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0.61 vs analyst estimates of $0.44 (37.9% beat)

- Revenue Guidance for Q1 CY2026 is $2.02 billion at the midpoint, below analyst estimates of $2.08 billion

- Operating Margin: 8%, in line with the same quarter last year

- Market Capitalization: $7.92 billion

Company Overview

Owner of The North Face, Vans, and Supreme, VF Corp (NYSE:VFC) is a clothing conglomerate specializing in branded lifestyle apparel, footwear, and accessories.

Its brands cater to different lifestyles and consumer segments, and some notable names under the VF Corp umbrella include The North Face, a top brand for outdoor apparel, gear, and footwear; Vans, a leading brand known for its skate-culture-inspired shoes and apparel; Supreme, a well-known streetwear brand; Timberland, which specializes in durable outdoor wear and is famous for its waterproof leather boots; Dickies, a brand that delivers performance-oriented workwear and apparel for workers in various industries including construction and service; JanSport, a popular backpack and collegiate gear brand among students and young adults; and Smartwool, a company known for high-quality Merino wool socks, apparel, and accessories.

VF Corp's target consumer base is as diverse as its brand portfolio, ranging from outdoor enthusiasts and athletes to fashion-conscious individuals and professionals needing workwear. Its products can be found at various retailers, department stores, and e-commerce websites.

4. Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

VF Corp's primary competitors include Nike, Inc. (NYSE:NKE), Adidas (OTCMKTS:ADDYY), Columbia Sportswear (NASDAQ:COLM), Lululemon (NASDAQ:LULU), and Levi (NYSE:LEVI).

5. Revenue Growth

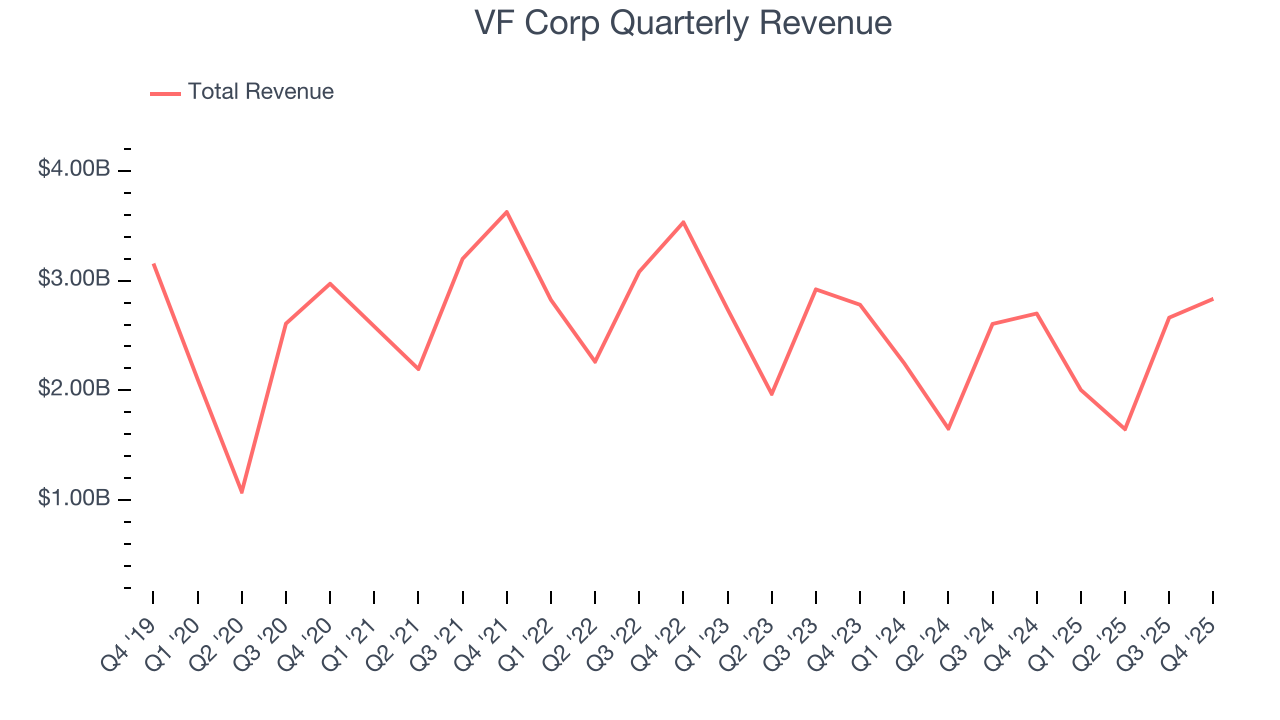

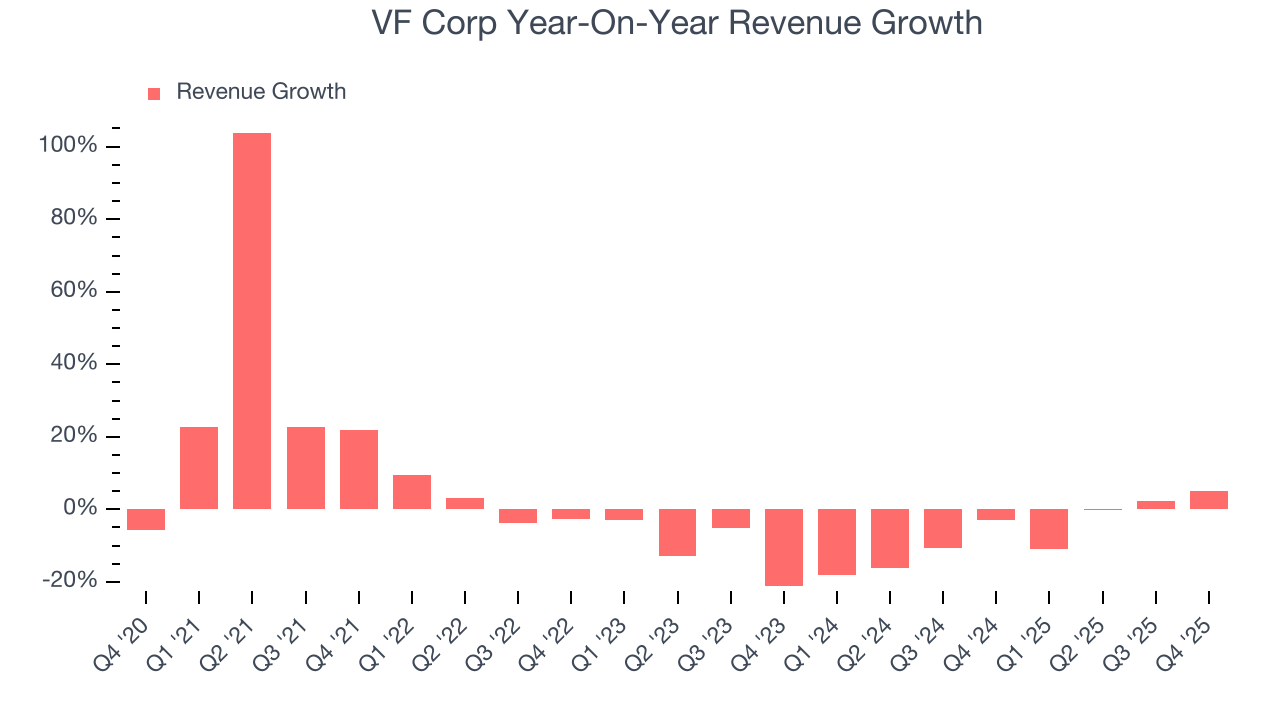

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, VF Corp struggled to consistently increase demand as its $9.15 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. VF Corp’s recent performance shows its demand remained suppressed as its revenue has declined by 6.2% annually over the last two years.

This quarter, VF Corp reported modest year-on-year revenue growth of 4.9% but beat Wall Street’s estimates by 3.1%. Company management is currently guiding for a 1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

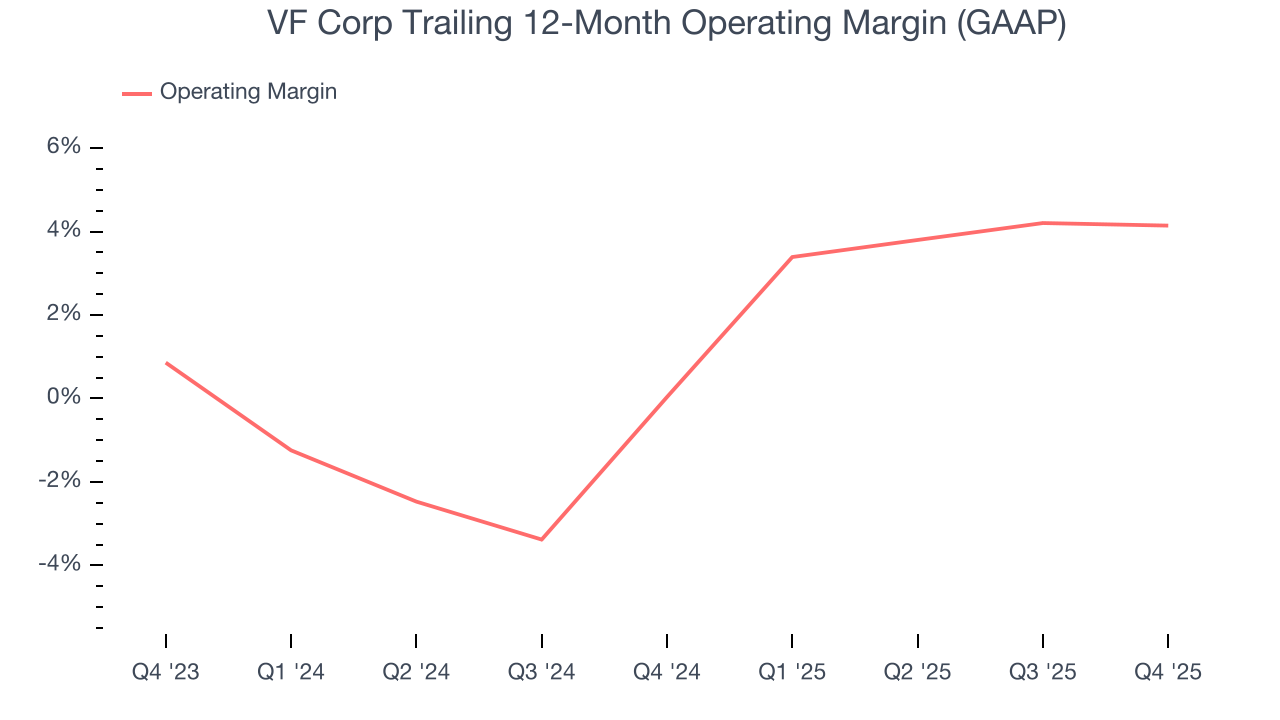

6. Operating Margin

VF Corp’s operating margin has been trending up over the last 12 months and averaged 2.1% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, VF Corp generated an operating margin profit margin of 8%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

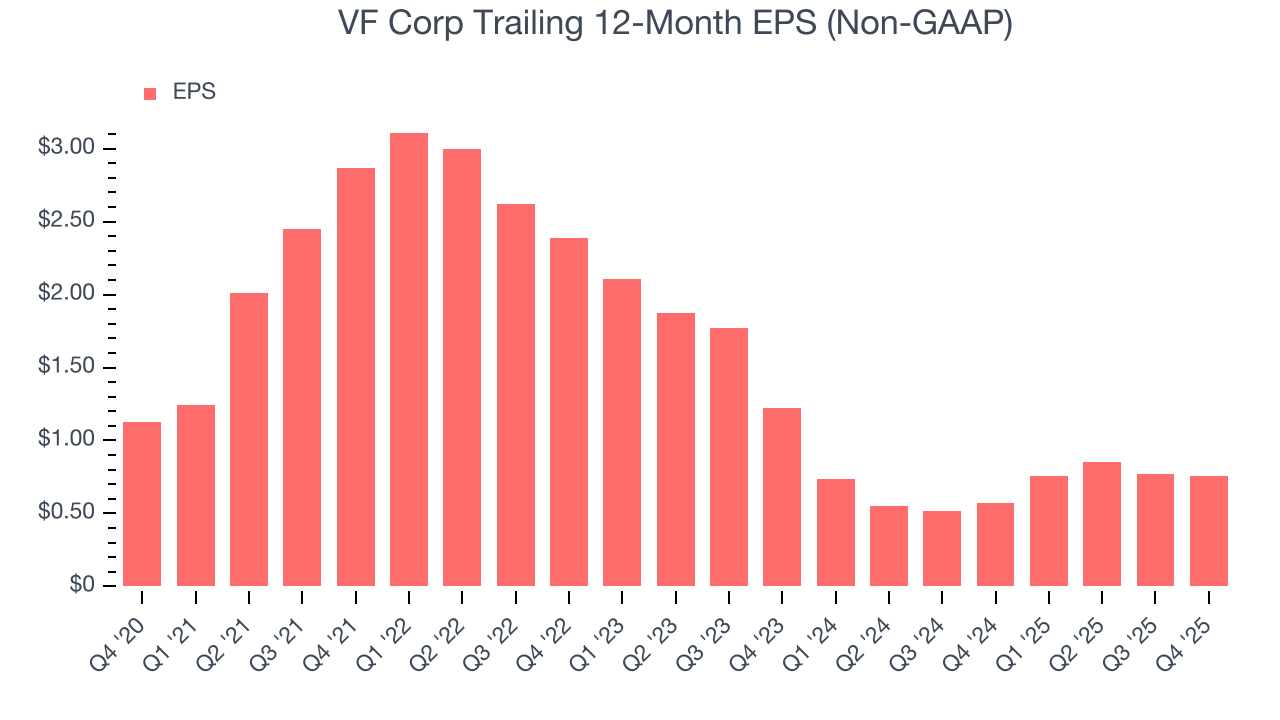

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for VF Corp, its EPS declined by 7.6% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

In Q4, VF Corp reported adjusted EPS of $0.61, down from $0.62 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects VF Corp’s full-year EPS of $0.76 to grow 21.8%.

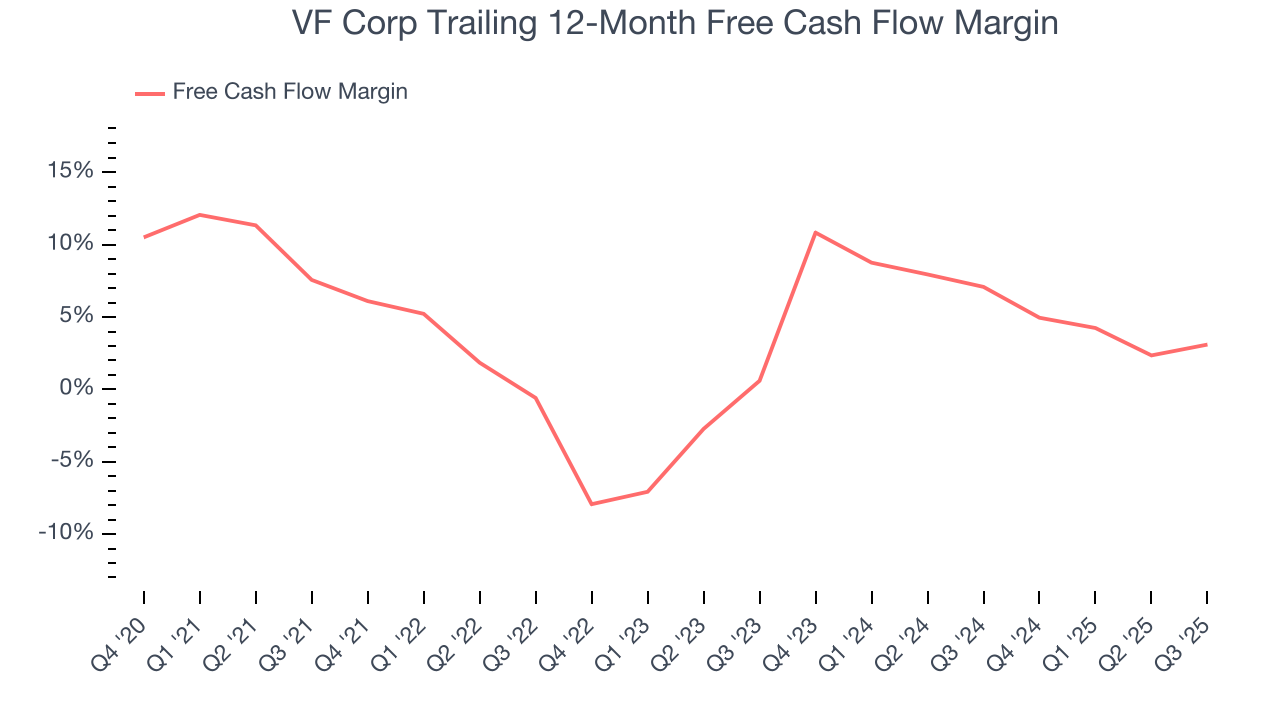

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the last two years, VF Corp’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.1%, meaning it lit $1.06 of cash on fire for every $100 in revenue.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

VF Corp historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.2%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, VF Corp’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Key Takeaways from VF Corp’s Q4 Results

It was good to see VF Corp beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed. Overall, this print had some key positives. The stock traded up 5.8% to $21.45 immediately following the results.

11. Is Now The Time To Buy VF Corp?

Updated: January 28, 2026 at 6:19 AM EST

Before investing in or passing on VF Corp, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

We see the value of companies helping consumers, but in the case of VF Corp, we’re out. First off, its revenue growth was weak over the last five years. On top of that, VF Corp’s constant currency sales performance has disappointed, and its declining EPS over the last five years makes it a less attractive asset to the public markets.

VF Corp’s P/E ratio based on the next 12 months is 21.9x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $17.19 on the company (compared to the current share price of $21.45), implying they don’t see much short-term potential in VF Corp.