Walker & Dunlop (WD)

We wouldn’t recommend Walker & Dunlop. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Walker & Dunlop Will Underperform

Originating as a small mortgage banking firm during the Great Depression in 1937, Walker & Dunlop (NYSE:WD) provides commercial real estate financing, property sales, appraisal, and investment management services with a focus on multifamily properties.

- Earnings per share fell by 14.6% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Loan losses and capital returns have eroded its tangible book value per share this cycle as its tangible book value per share declined by 6.8% annually over the last five years

- Annual net interest income declines of 40.1% for the past five years show its loan book struggled during this cycle

Walker & Dunlop doesn’t meet our quality criteria. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Walker & Dunlop

At $43.83 per share, Walker & Dunlop trades at 0.8x forward P/B. This multiple is lower than most banking companies, but for good reason.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Walker & Dunlop (WD) Research Report: Q4 CY2025 Update

Commercial real estate finance company Walker & Dunlop (NYSE:WD) missed Wall Street’s revenue expectations in Q4 CY2025, with sales flat year on year at $340 million. Its non-GAAP profit of $0.28 per share was 80.8% below analysts’ consensus estimates.

Walker & Dunlop (WD) Q4 CY2025 Highlights:

- Revenue: $340 million vs analyst estimates of $343.5 million (flat year on year, 1% miss)

- Adjusted EPS: $0.28 vs analyst expectations of $1.46 (80.8% miss)

- Market Capitalization: $2.01 billion

Company Overview

Originating as a small mortgage banking firm during the Great Depression in 1937, Walker & Dunlop (NYSE:WD) provides commercial real estate financing, property sales, appraisal, and investment management services with a focus on multifamily properties.

Walker & Dunlop operates at the intersection of real estate and finance, with a particular focus on multifamily properties. The company originates loans through government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac, as well as through the Federal Housing Administration (FHA). Under the Fannie Mae Delegated Underwriting and Servicing program, Walker & Dunlop shares a portion of the risk on loans it originates, with its maximum loss typically capped at 20% of the loan amount.

Beyond loan origination, Walker & Dunlop maintains a substantial servicing portfolio, generating steady fee income by managing loans throughout their lifecycle. The company retains servicing rights on most loans it originates, providing ongoing revenue streams long after the initial transaction. These services include collecting payments, managing escrow accounts, conducting property inspections, and reporting to investors.

Walker & Dunlop has expanded its offerings to include property sales brokerage, helping owners sell multifamily assets while often providing financing to the purchasers. Its investment management arm, Walker & Dunlop Investment Partners, manages debt and equity investments in commercial real estate funds with billions in assets under management. The company has also established a significant presence in affordable housing through tax credit syndication, forming partnerships with developers and investors to create and preserve affordable housing units nationwide.

Technology has become increasingly important to Walker & Dunlop's strategy, with investments in data analytics to support its small-balance lending platform and enhance its appraisal services. A client working with Walker & Dunlop might engage the company to secure financing for a multifamily property acquisition, later use its property sales team when selling the asset, and potentially invest in one of its real estate funds.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

Walker & Dunlop competes with major financial institutions and specialized commercial real estate service providers including CBRE Group, Jones Lang LaSalle, Wells Fargo, PNC Real Estate, Berkadia Commercial Mortgage, and Marcus & Millichap. In the affordable housing and tax credit syndication space, competitors include Boston Financial Investment Management, Raymond James, and Enterprise Community Partners.

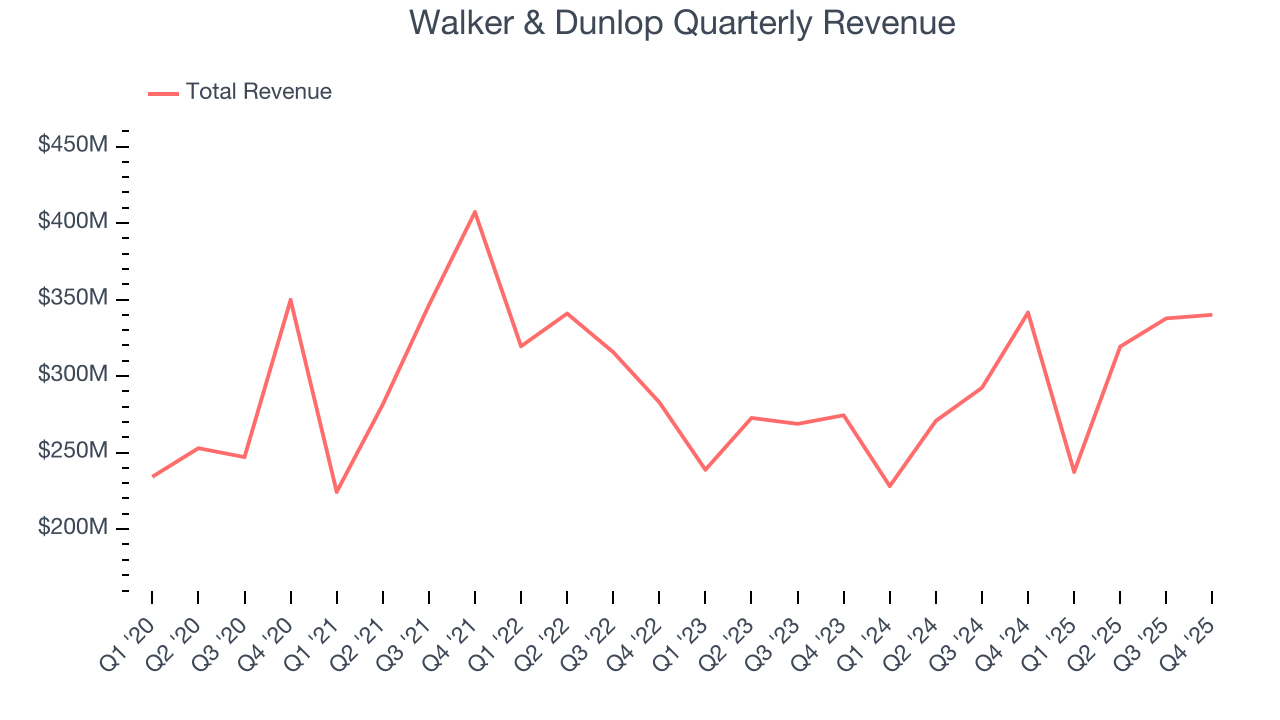

5. Sales Growth

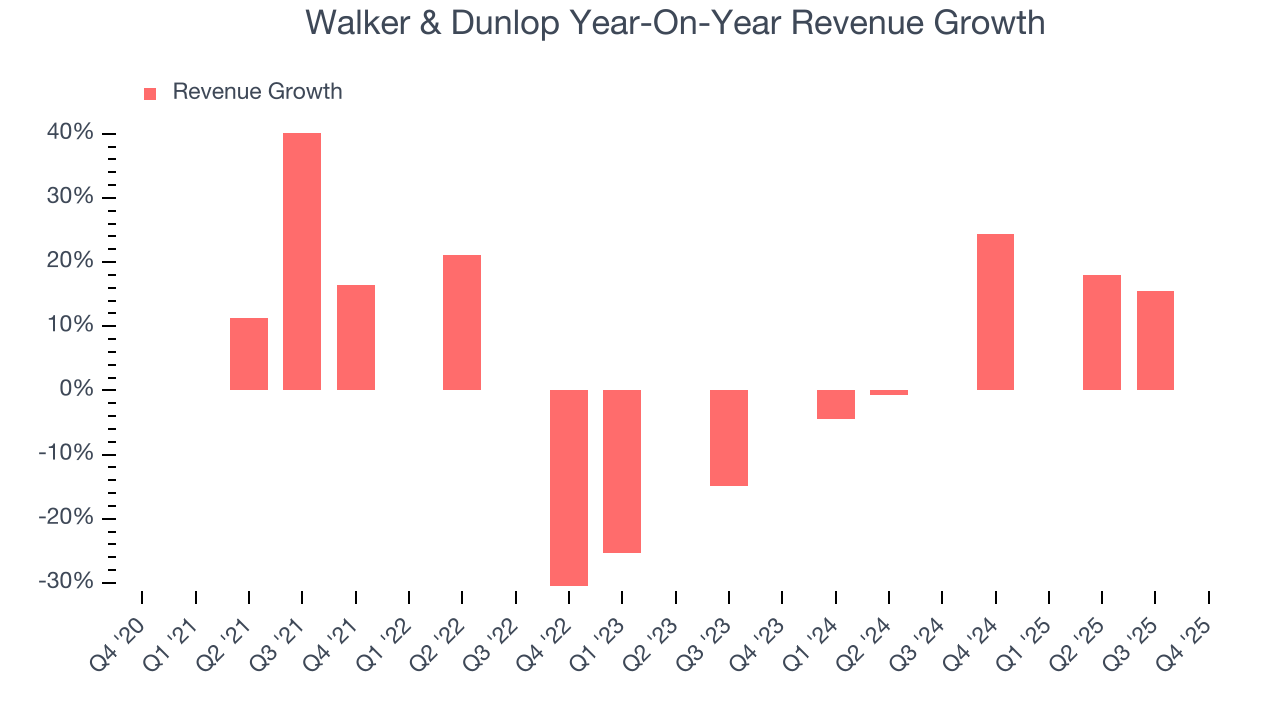

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. Unfortunately, Walker & Dunlop’s 2.6% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Walker & Dunlop’s annualized revenue growth of 8.2% over the last two years is above its five-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Walker & Dunlop missed Wall Street’s estimates and reported a rather uninspiring 0.4% year-on-year revenue decline, generating $340 million of revenue.

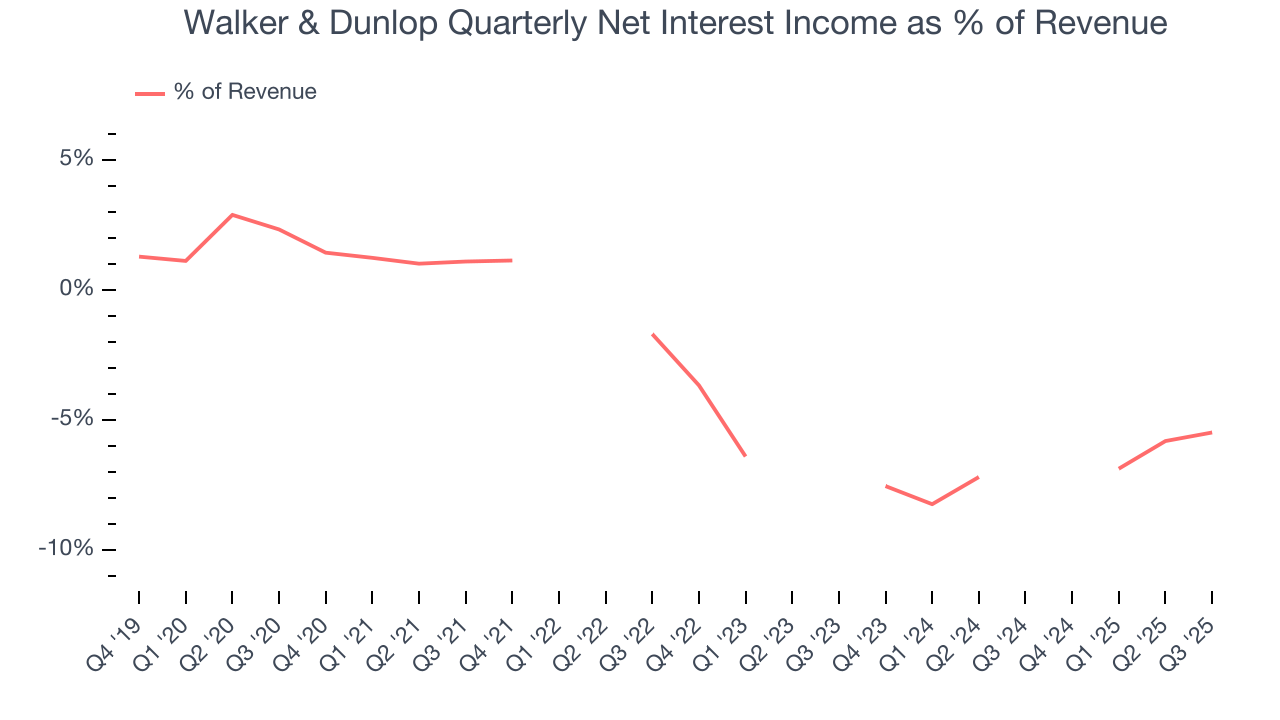

Net interest income made up -4% of the company’s total revenue during the last five years, meaning Walker & Dunlop is well diversified and has a variety of income streams driving its overall growth. Nevertheless, net interest income is critical to analyze for banks because they’re considered a higher-quality, more recurring revenue source by investors.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.6. Earnings Per Share

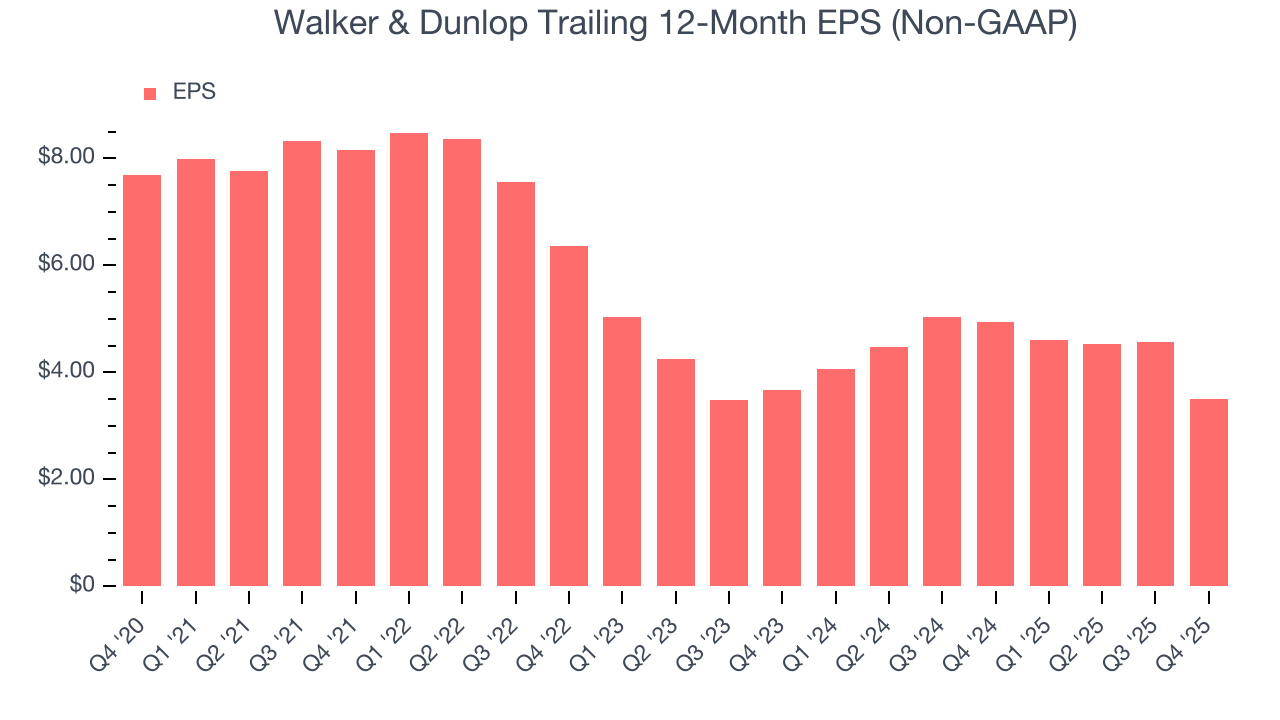

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Walker & Dunlop, its EPS declined by 14.6% annually over the last five years while its revenue grew by 2.6%. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Walker & Dunlop, its two-year annual EPS declines of 2.3% show it’s still underperforming. These results were bad no matter how you slice the data.

In Q4, Walker & Dunlop reported adjusted EPS of $0.28, down from $1.34 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Walker & Dunlop’s full-year EPS of $3.50 to grow 53%.

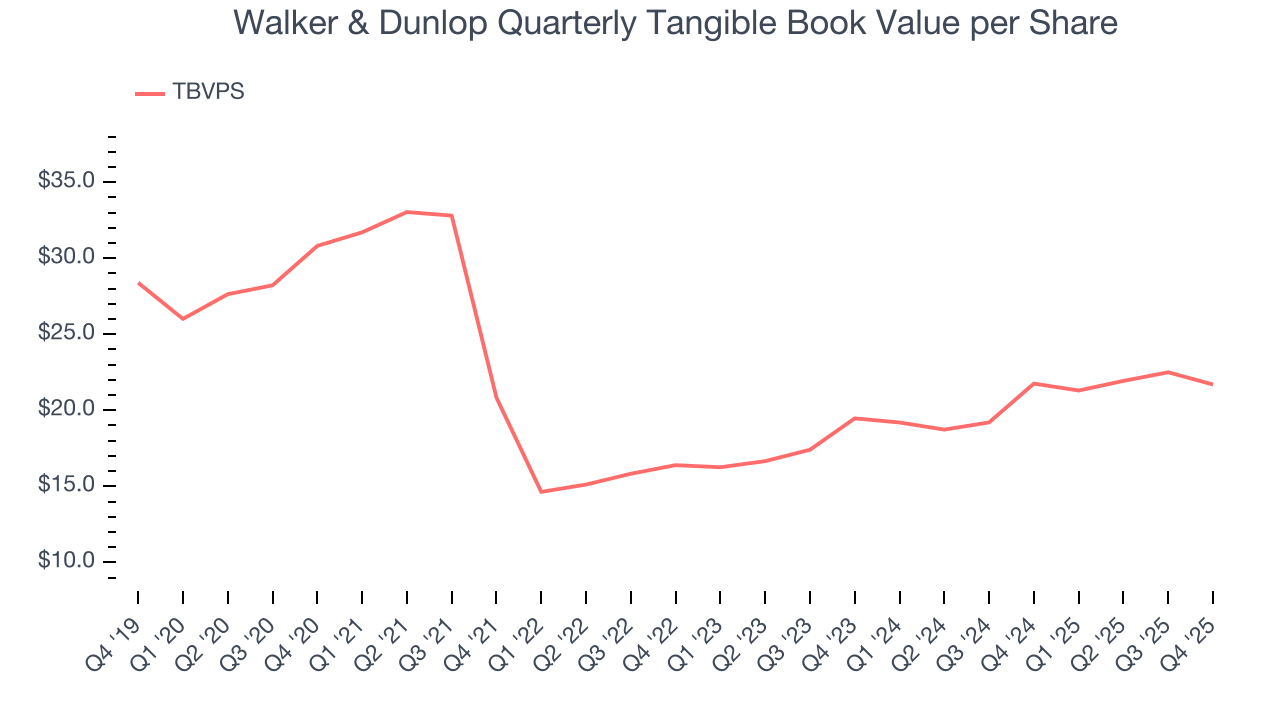

7. Tangible Book Value Per Share (TBVPS)

Banks operate as balance sheet businesses, with profits generated through borrowing and lending activities. Valuations reflect this reality, emphasizing balance sheet strength and long-term book value compounding ability.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

Walker & Dunlop’s TBVPS declined at a 6.8% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 5.6% annually over the last two years from $19.47 to $21.70 per share.

Over the next 12 months, Consensus estimates call for Walker & Dunlop’s TBVPS to grow by 16.6% to $25.31, solid growth rate.

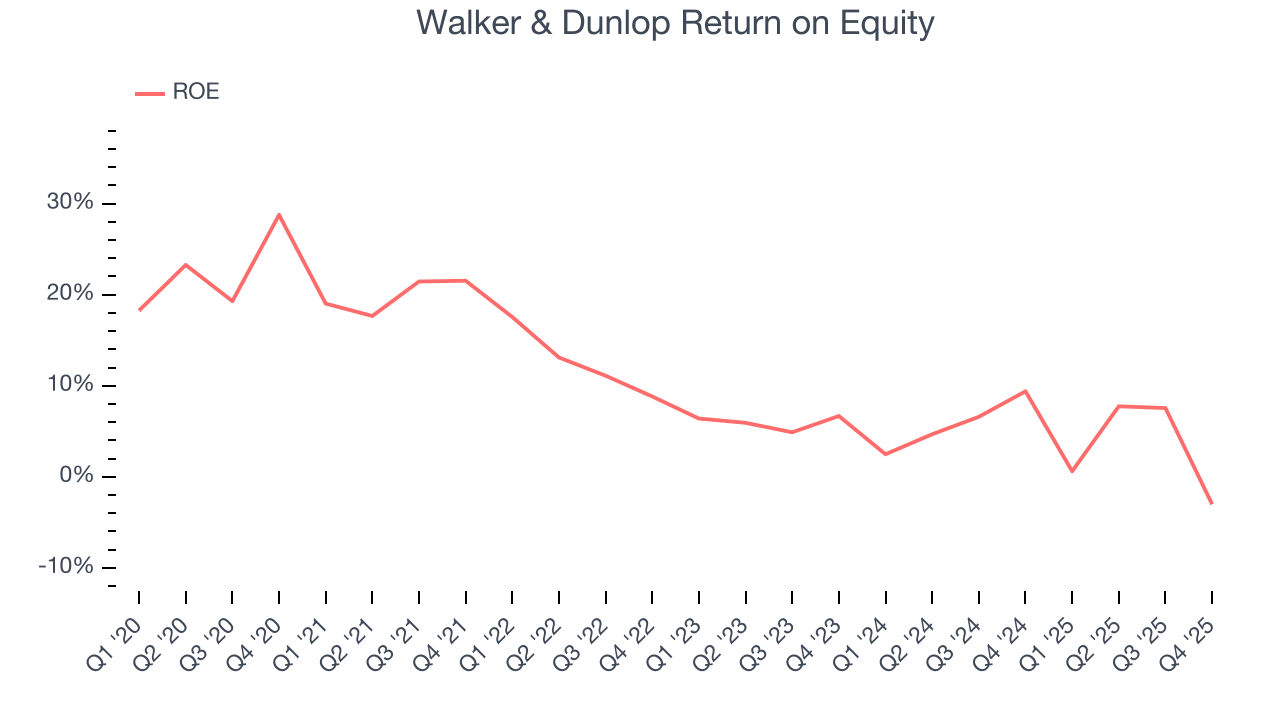

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Walker & Dunlop has averaged an ROE of 9.5%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

9. Key Takeaways from Walker & Dunlop’s Q4 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $58.91 immediately following the results.

10. Is Now The Time To Buy Walker & Dunlop?

Updated: March 22, 2026 at 12:47 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Walker & Dunlop.

We see the value of companies driving economic growth, but in the case of Walker & Dunlop, we’re out. First off, its revenue growth was weak over the last five years. While its estimated net interest income growth for the next 12 months is great, the downside is its TBVPS has declined over the last five years. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Walker & Dunlop’s P/B ratio based on the next 12 months is 0.8x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $67.50 on the company (compared to the current share price of $43.83).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.