Astec (ASTE)

Astec doesn’t excite us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why Astec Is Not Exciting

Inventing the first ever double-barrel hot-mix asphalt plant, Astec (NASDAQ:ASTE) provides machines and equipment for building roads, processing raw materials, and producing concrete.

- Cash-burning tendencies make us wonder if it can sustainably generate shareholder value

- Product roadmap and go-to-market strategy need to be reconsidered as its backlog has averaged 13.1% declines over the past two years

- A positive is that its estimated revenue growth of 12.8% for the next 12 months implies demand will accelerate from its two-year trend

Astec is in the penalty box. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Astec

At $52.61 per share, Astec trades at 14.1x forward P/E. This multiple is cheaper than most industrials peers, but we think this is justified.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Astec (ASTE) Research Report: Q4 CY2025 Update

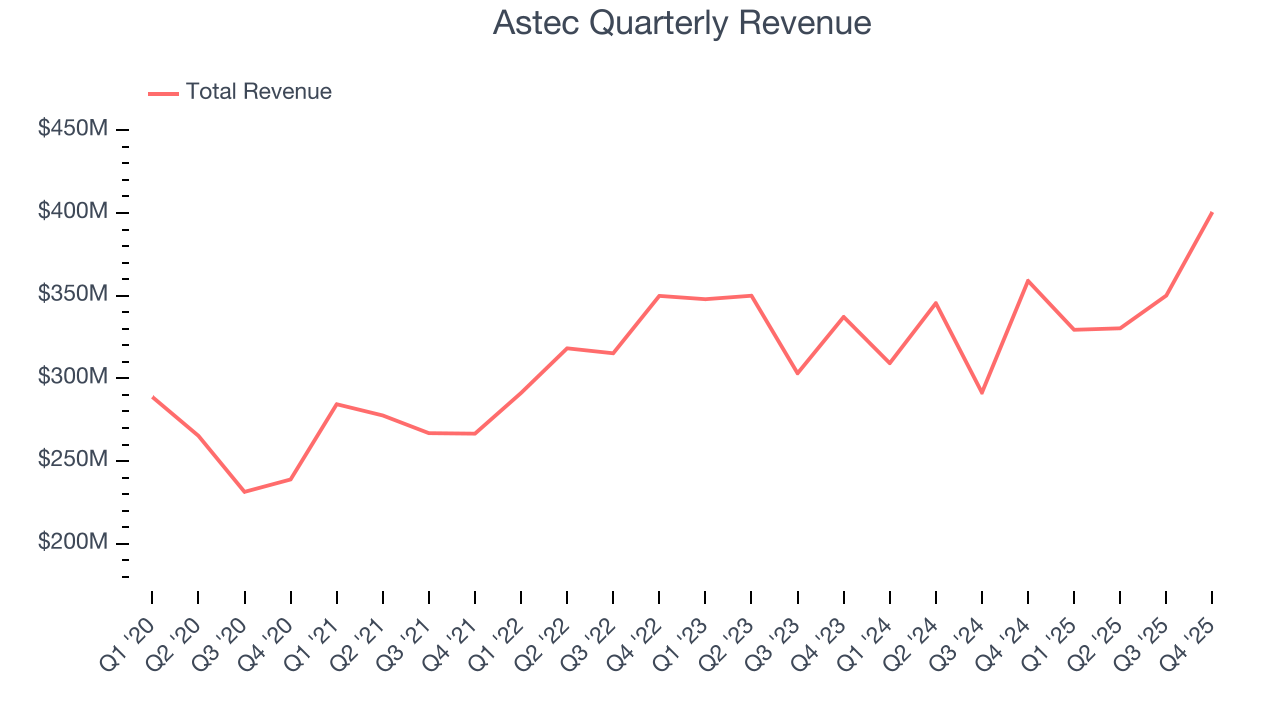

Construction equipment company Astec (NASDAQ:ASTE) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 11.6% year on year to $400.6 million. Its non-GAAP profit of $1.06 per share was 27.7% above analysts’ consensus estimates.

Astec (ASTE) Q4 CY2025 Highlights:

- Revenue: $400.6 million vs analyst estimates of $374.2 million (11.6% year-on-year growth, 7.1% beat)

- Adjusted EPS: $1.06 vs analyst estimates of $0.83 (27.7% beat)

- Adjusted EBITDA: $44.7 million vs analyst estimates of $37.5 million (11.2% margin, 19.2% beat)

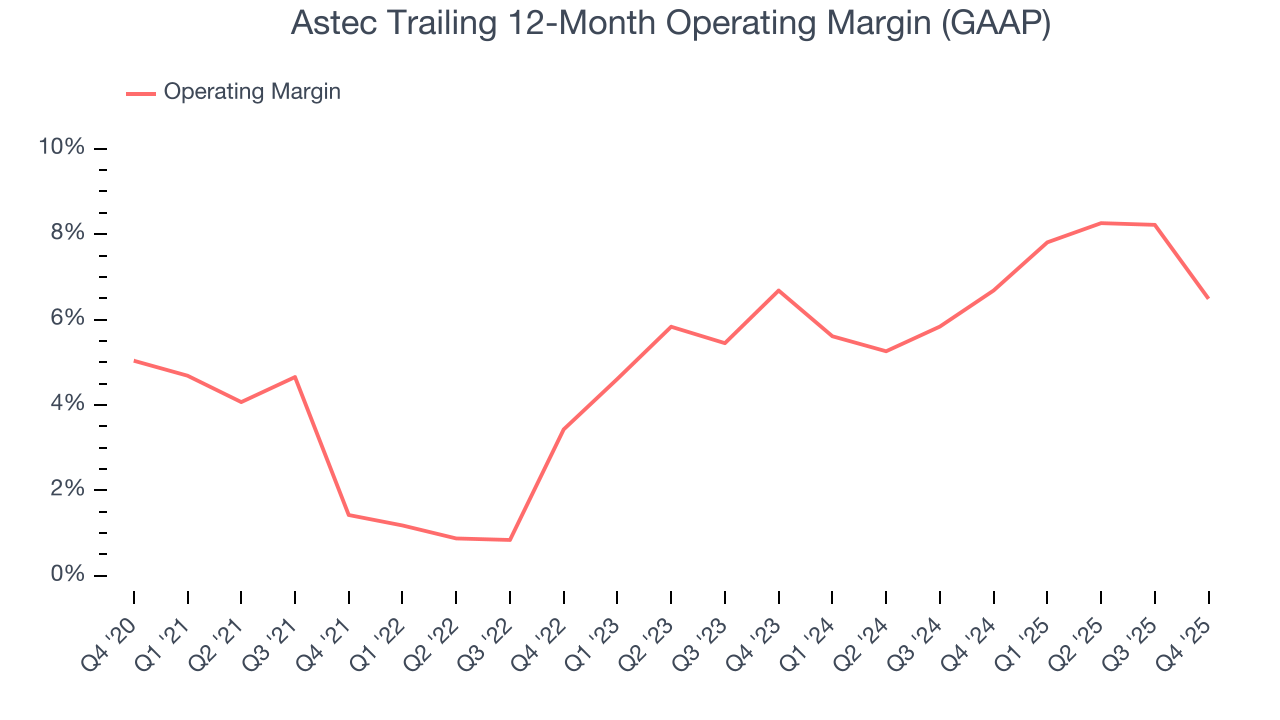

- Operating Margin: 5.7%, down from 12.2% in the same quarter last year

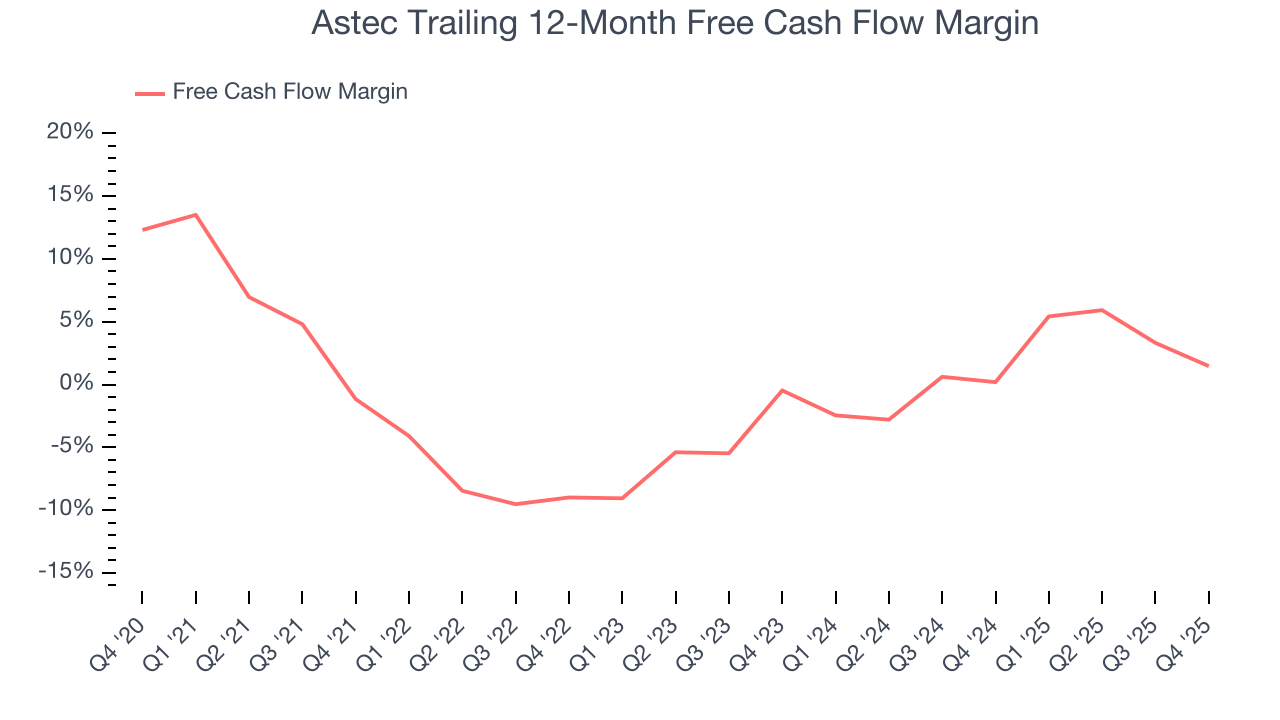

- Free Cash Flow Margin: 1.8%, down from 8.9% in the same quarter last year

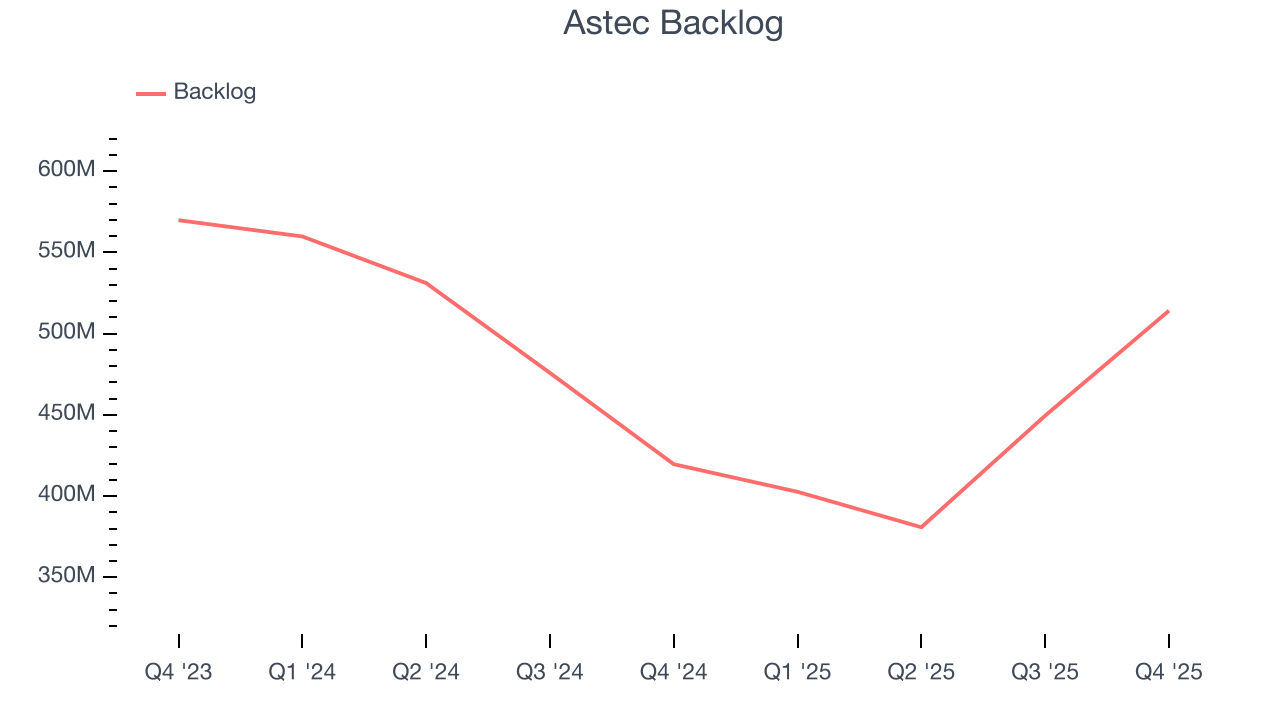

- Backlog: $514.1 million at quarter end, up 22.5% year on year

- Market Capitalization: $1.34 billion

Company Overview

Inventing the first ever double-barrel hot-mix asphalt plant, Astec (NASDAQ:ASTE) provides machines and equipment for building roads, processing raw materials, and producing concrete.

Astec was founded in 1972 with a vision to combine new technology with traditionally low-tech industries like road construction. The company quickly grew by acquiring various companies and notably acquired Power Flame for $43 million in 2016, enhancing its industrial heating systems capabilities.

Astec makes machines and equipment for building roads, processing raw materials, and producing concrete. Its offerings span from asphalt and concrete plants that mix ingredients to make asphalt or concrete, respectively, to crushers and screeners that crush large rocks into smaller pieces and separate these pieces into different sizes for use in construction.

Astec offers equipment for each stage of construction to construction companies, developers, and mining companies. For example, its asphalt plants create the material needed to pave roads while its crushing and screening equipment processes raw materials like rocks into usable forms for building.

It primarily engages in direct transactions where customers purchase the equipment outright to use. Customers can also engage in service agreements and the duration of the contract depends on the type of equipment, ranging from several years to over a decade.

4. Construction Machinery

Automation that increases efficiencies and connected equipment that collects analyzable data have been trending, creating new sales opportunities for construction machinery companies. On the other hand, construction machinery companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the commercial and residential construction that drives demand for these companies’ offerings.

Competitors offering similar products include Caterpillar (NYSE:CAT), Terex (NYSE:TEX), and Gencor (NASDAQ:GENC).

5. Revenue Growth

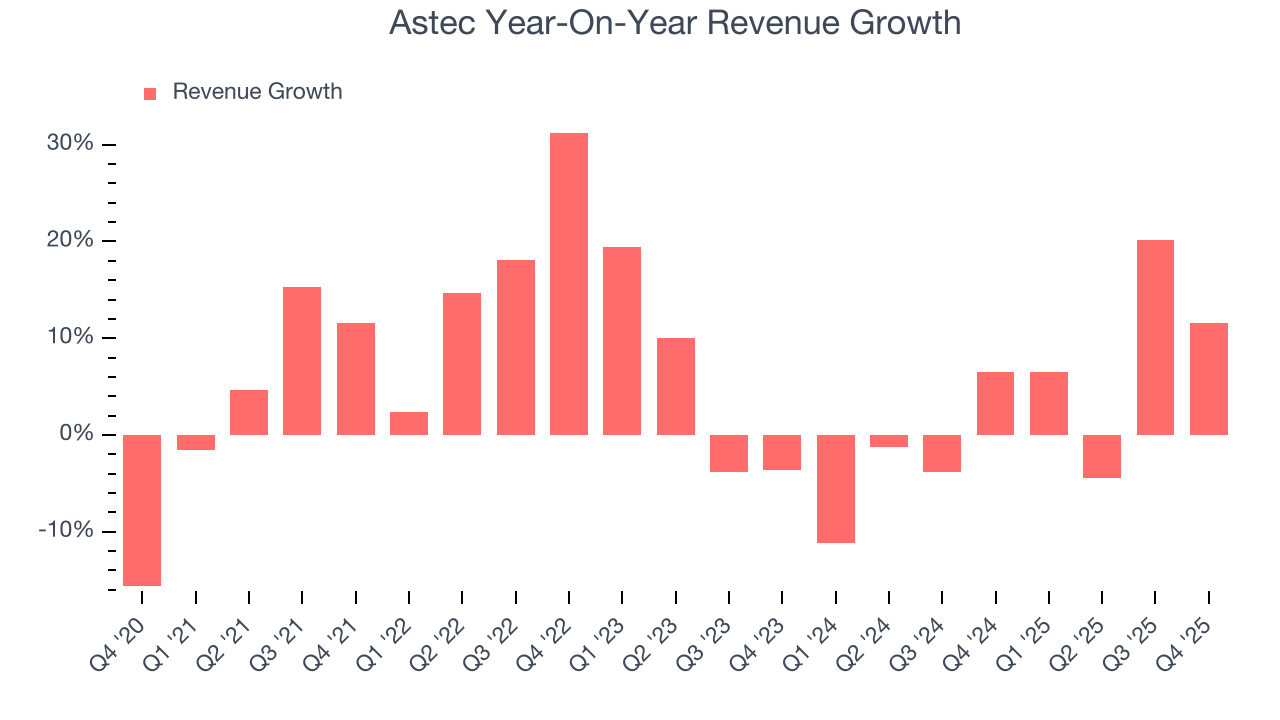

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Astec’s sales grew at a mediocre 6.6% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Astec’s recent performance shows its demand has slowed as its annualized revenue growth of 2.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs. We also note many other Construction Machinery businesses have faced declining sales because of cyclical headwinds. While Astec grew slower than we’d like, it did do better than its peers.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Astec’s backlog reached $514.1 million in the latest quarter and averaged 13.1% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Astec reported year-on-year revenue growth of 11.6%, and its $400.6 million of revenue exceeded Wall Street’s estimates by 7.1%.

Looking ahead, sell-side analysts expect revenue to grow 3.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

6. Gross Margin & Pricing Power

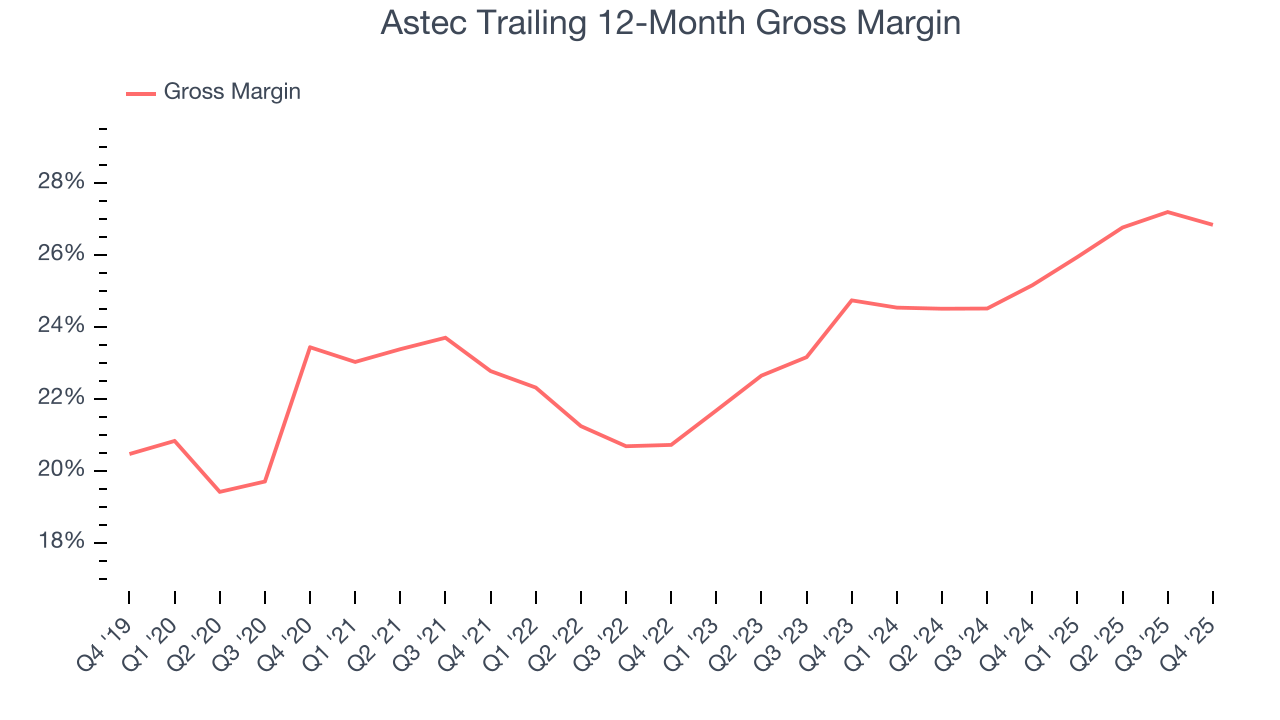

Astec has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 24.2% gross margin over the last five years. That means Astec paid its suppliers a lot of money ($75.84 for every $100 in revenue) to run its business.

This quarter, Astec’s gross profit margin was 27.3%, down 1.4 percentage points year on year. Zooming out, however, Astec’s full-year margin has been trending up over the past 12 months, increasing by 1.7 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

7. Operating Margin

Astec was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.1% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Astec’s operating margin rose by 5.1 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Astec generated an operating margin profit margin of 5.7%, down 6.5 percentage points year on year. Since Astec’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

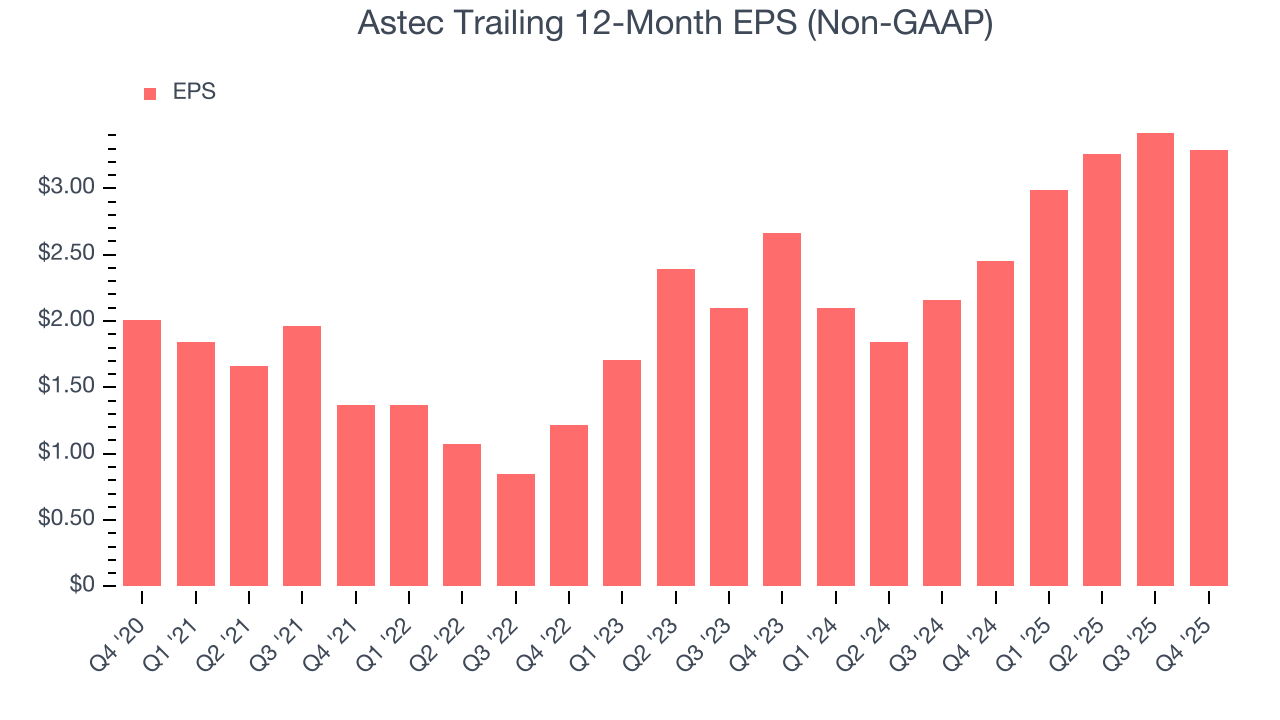

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Astec’s EPS grew at a solid 10.4% compounded annual growth rate over the last five years, higher than its 6.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Astec’s earnings can give us a better understanding of its performance. As we mentioned earlier, Astec’s operating margin declined this quarter but expanded by 5.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Astec, its two-year annual EPS growth of 11.2% is similar to its five-year trend, implying strong and stable earnings power.

In Q4, Astec reported adjusted EPS of $1.06, down from $1.19 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Astec’s full-year EPS of $3.29 to stay about the same.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

While Astec posted positive free cash flow this quarter, the broader story hasn’t been so clean. Astec’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.7%, meaning it lit $1.72 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Astec’s margin expanded by 2.6 percentage points during that time. Despite its improvement and recent free cash flow generation, we’d like to see more quarters of positive cash flow before recommending the stock.

Astec’s free cash flow clocked in at $7.4 million in Q4, equivalent to a 1.8% margin. The company’s cash profitability regressed as it was 7.1 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

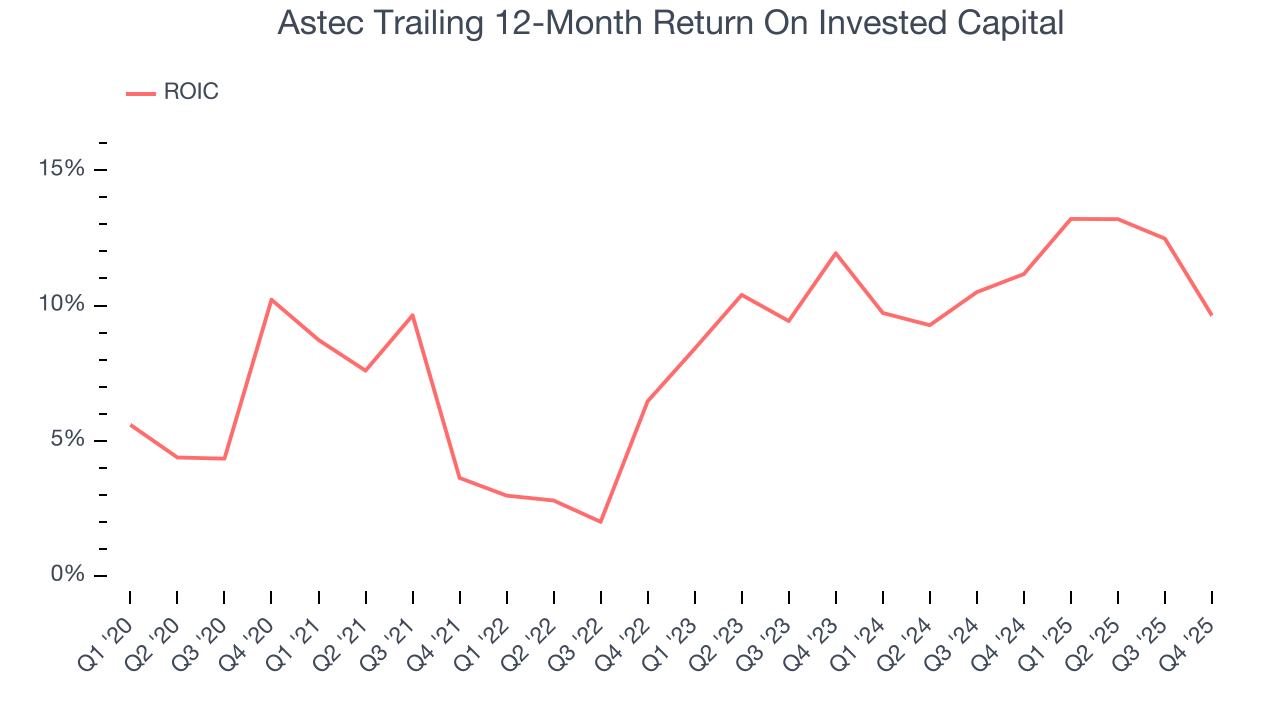

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Astec historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.6%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Astec’s has increased over the last few years. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Assessment

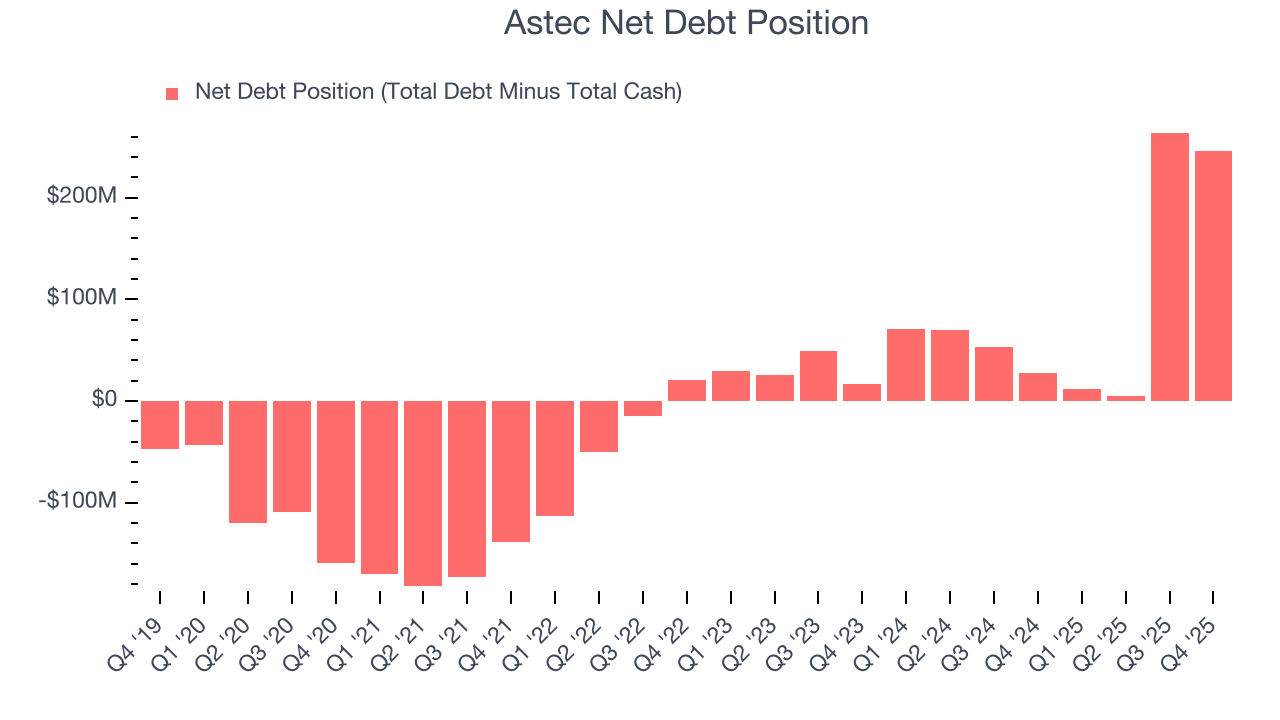

Astec reported $74.1 million of cash and $319.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $134.2 million of EBITDA over the last 12 months, we view Astec’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $15.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Astec’s Q4 Results

It was good to see Astec beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 1% to $59.09 immediately following the results.

13. Is Now The Time To Buy Astec?

Updated: March 15, 2026 at 11:14 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Astec.

Astec isn’t a terrible business, but it doesn’t pass our bar. For starters, its revenue growth was mediocre over the last five years. While its expanding operating margin shows the business has become more efficient, the downside is its cash burn raises the question of whether it can sustainably maintain growth. On top of that, its backlog declined.

Astec’s P/E ratio based on the next 12 months is 14.2x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $75.50 on the company (compared to the current share price of $52.87).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.