Columbia Sportswear (COLM)

Columbia Sportswear is in for a bumpy ride. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Columbia Sportswear Will Underperform

Originally founded as a hat store in 1938, Columbia Sportswear (NASDAQ:COLM) is a manufacturer of outerwear, sportswear, and footwear designed for outdoor enthusiasts.

- Annual revenue growth of 6.3% over the last five years was below our standards for the consumer discretionary sector

- Responsiveness to unforeseen market trends is restricted due to its substandard operating margin profitability

- Lacking free cash flow limits its freedom to invest in growth initiatives, execute share buybacks, or pay dividends

Columbia Sportswear’s quality doesn’t meet our expectations. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Columbia Sportswear

At $55.23 per share, Columbia Sportswear trades at 16.1x forward P/E. This multiple is cheaper than most consumer discretionary peers, but we think this is justified.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Columbia Sportswear (COLM) Research Report: Q4 CY2025 Update

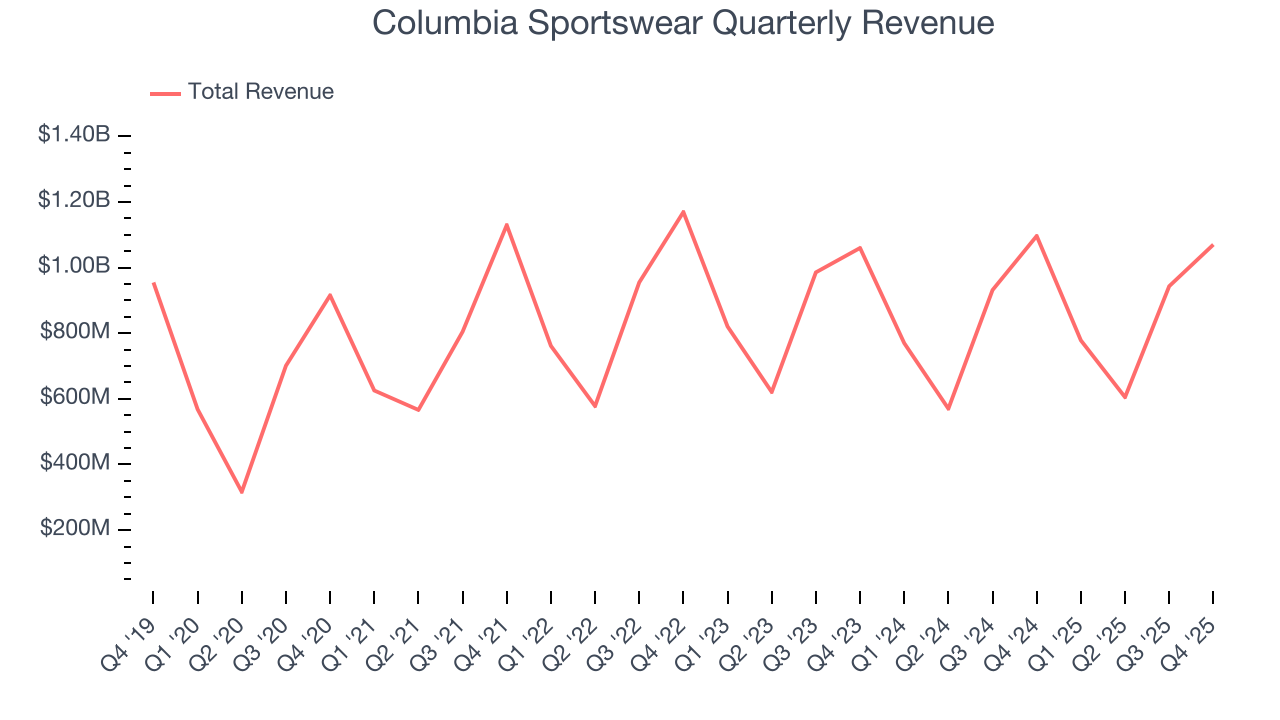

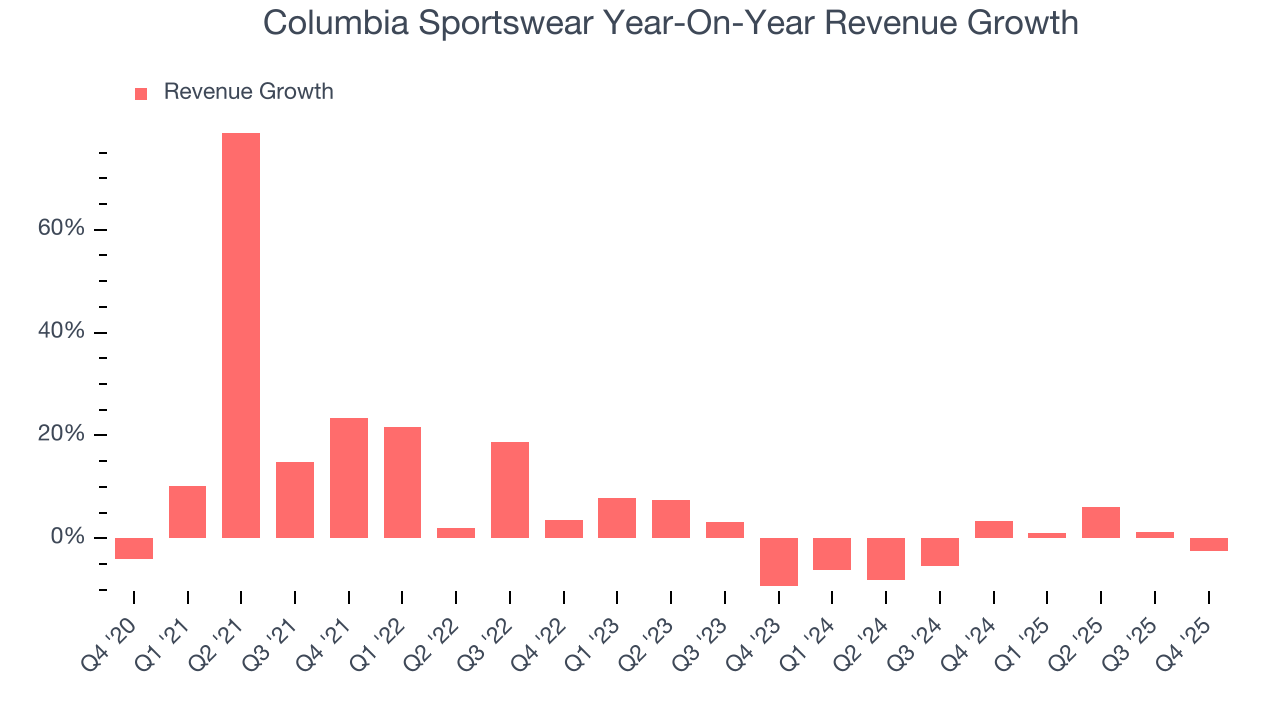

Outerwear manufacturer Columbia Sportswear (NASDAQ:COLM) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 2.4% year on year to $1.07 billion. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $753 million was less impressive, coming in 4% below expectations. Its GAAP profit of $1.73 per share was 43% above analysts’ consensus estimates.

Columbia Sportswear (COLM) Q4 CY2025 Highlights:

- Revenue: $1.07 billion vs analyst estimates of $1.03 billion (2.4% year-on-year decline, 3.6% beat)

- EPS (GAAP): $1.73 vs analyst estimates of $1.21 (43% beat)

- Adjusted EBITDA: $155.7 million vs analyst estimates of $109.9 million (14.5% margin, 41.7% beat)

- Revenue Guidance for Q1 CY2026 is $753 million at the midpoint, below analyst estimates of $784.6 million

- EPS (GAAP) guidance for the upcoming financial year 2026 is $3.43 at the midpoint, beating analyst estimates by 10.5%

- Operating Margin: 10.9%, down from 12.5% in the same quarter last year

- Free Cash Flow Margin: 61.9%, up from 50.1% in the same quarter last year

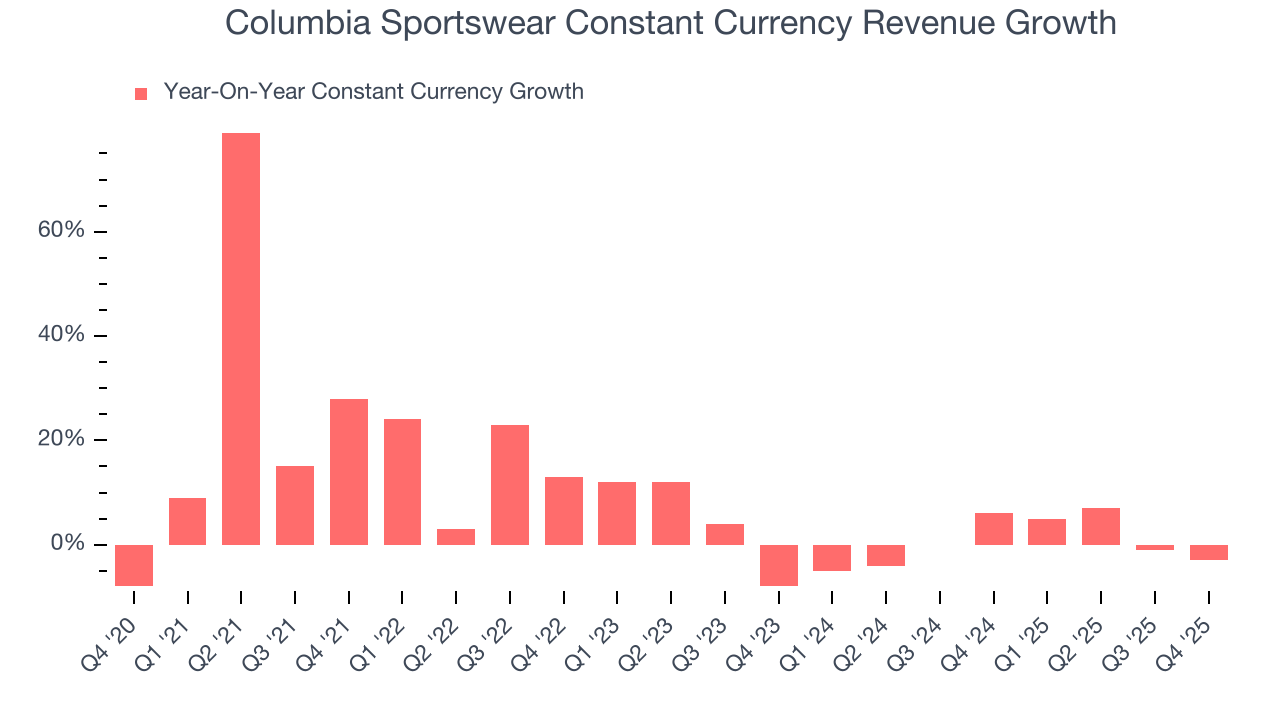

- Constant Currency Revenue fell 3% year on year (6% in the same quarter last year)

- Market Capitalization: $2.98 billion

Company Overview

Originally founded as a hat store in 1938, Columbia Sportswear (NASDAQ:COLM) is a manufacturer of outerwear, sportswear, and footwear designed for outdoor enthusiasts.

Columbia Sportswear’s 80-year-old brand represents the outdoors, and it has developed clothing technologies such as Omni-Heat Reflective, which reflects body heat while maintaining breathability, to stand out.

The company markets its products under several brands, including the flagship Columbia brand, Mountain Hardwear, Sorel, and prAna. Its products range from winter jackets, trail shoes, and waterproof boots to tents and sleeping bags, catering to a broad spectrum of outdoor activities including hiking, skiing, fishing, and trail running. This breadth appeals to a wide demographic, from casual hikers and families enjoying the outdoors to serious mountaineers and adventure sports enthusiasts.

Columbia Sportswear sells its products in over 90 countries through department stores, specialty stores, branded franchise stores, and corporate-owned online and brick-and-mortar stores.

4. Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Columbia Sportswear's primary competitors include The North Face (owned by VF Corporation NYSE:VFC), Jack Wolfskin (owned by Callaway Golf Company NYSE:ELY), Arc'teryx (owned by Amer Sports OTC:AGPDY), and private companies REI Co-op and Patagonia.

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Columbia Sportswear’s 6.3% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Columbia Sportswear’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.3% annually.

Columbia Sportswear also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales were flat. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Columbia Sportswear.

This quarter, Columbia Sportswear’s revenue fell by 2.4% year on year to $1.07 billion but beat Wall Street’s estimates by 3.6%. Company management is currently guiding for a 3.3% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

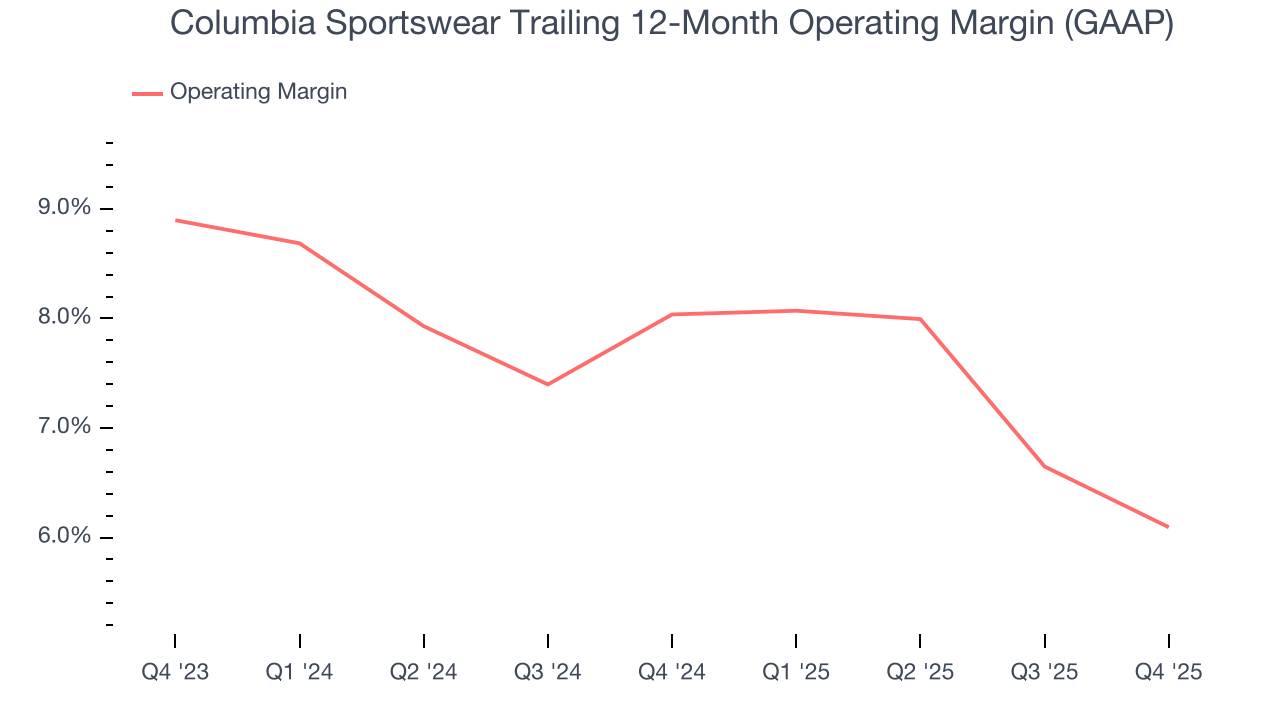

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Columbia Sportswear’s operating margin has been trending down over the last 12 months and averaged 7.1% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Columbia Sportswear generated an operating margin profit margin of 10.9%, down 1.6 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

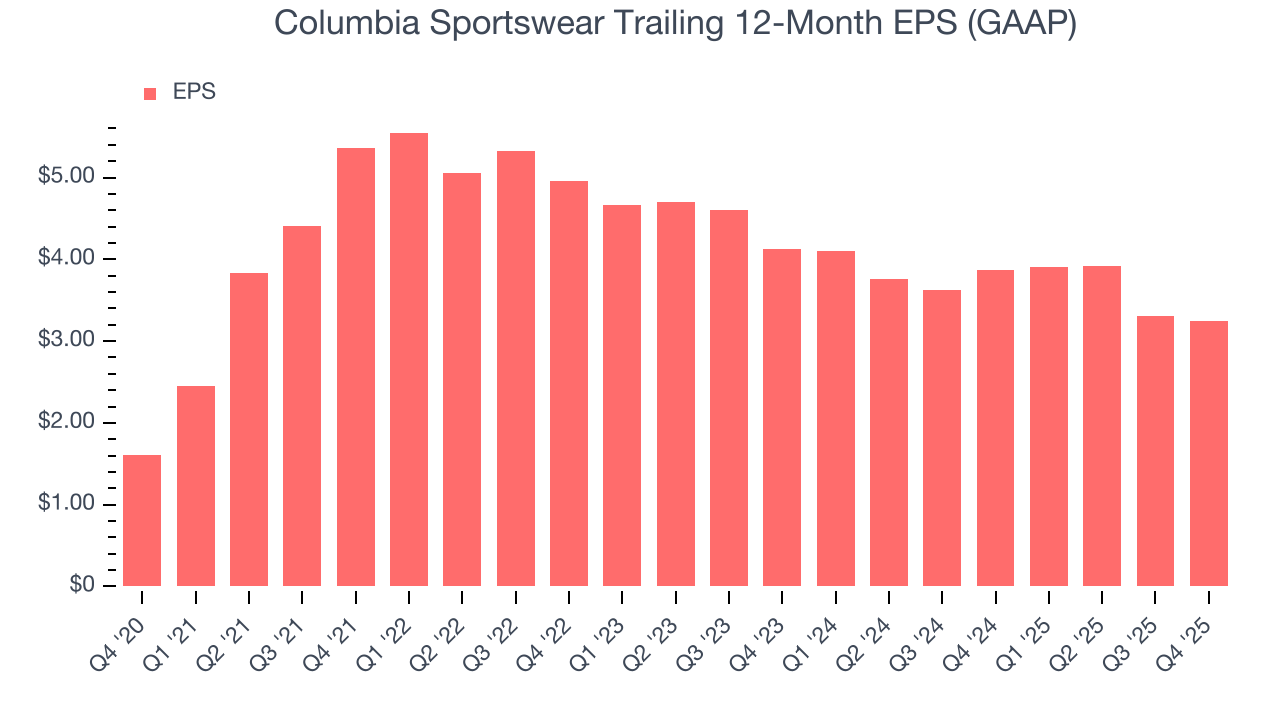

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Columbia Sportswear’s EPS grew at a weak 15% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q4, Columbia Sportswear reported EPS of $1.73, down from $1.80 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Columbia Sportswear’s full-year EPS of $3.24 to shrink by 5.6%.

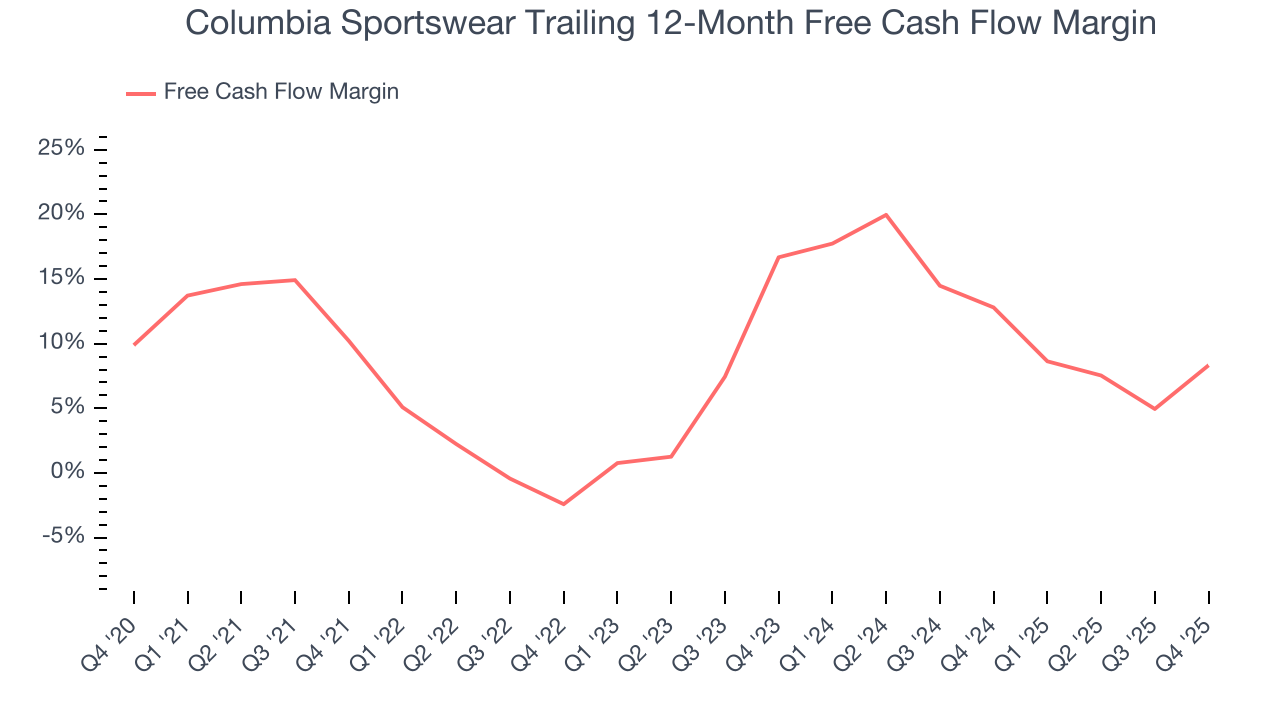

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Columbia Sportswear has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 10.6%, lousy for a consumer discretionary business.

Columbia Sportswear’s free cash flow clocked in at $663 million in Q4, equivalent to a 61.9% margin. This result was good as its margin was 11.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Columbia Sportswear historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 17.3%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Columbia Sportswear’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

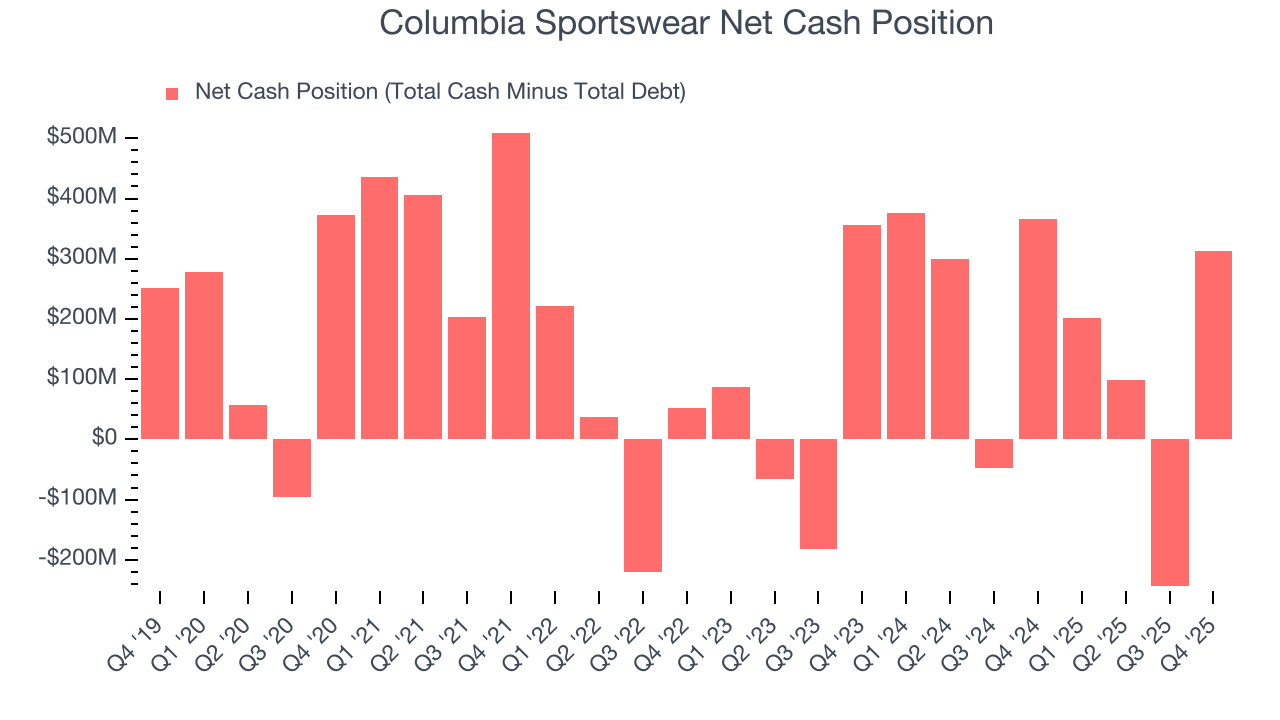

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Columbia Sportswear is a profitable, well-capitalized company with $790.8 million of cash and $477.7 million of debt on its balance sheet. This $313.1 million net cash position is 10.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Columbia Sportswear’s Q4 Results

It was good to see Columbia Sportswear beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS guidance for next quarter missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 5.3% to $60.50 immediately after reporting.

12. Is Now The Time To Buy Columbia Sportswear?

Updated: March 21, 2026 at 10:55 PM EDT

Are you wondering whether to buy Columbia Sportswear or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Columbia Sportswear falls short of our quality standards. On top of that, Columbia Sportswear’s Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion, and its projected EPS for the next year is lacking.

Columbia Sportswear’s P/E ratio based on the next 12 months is 16.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $64.50 on the company (compared to the current share price of $55.23).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.