Freshworks (FRSH)

Freshworks piques our interest. It’s not only rapidly winning market share but also boasts impressive unit economics, a winning formula.― StockStory Analyst Team

1. News

2. Summary

Why Freshworks Is Interesting

Starting as a customer service solution before expanding into a comprehensive software suite, Freshworks (NASDAQ:FRSH) provides AI-powered software-as-a-service solutions that help companies manage customer service, IT support, sales, and marketing functions.

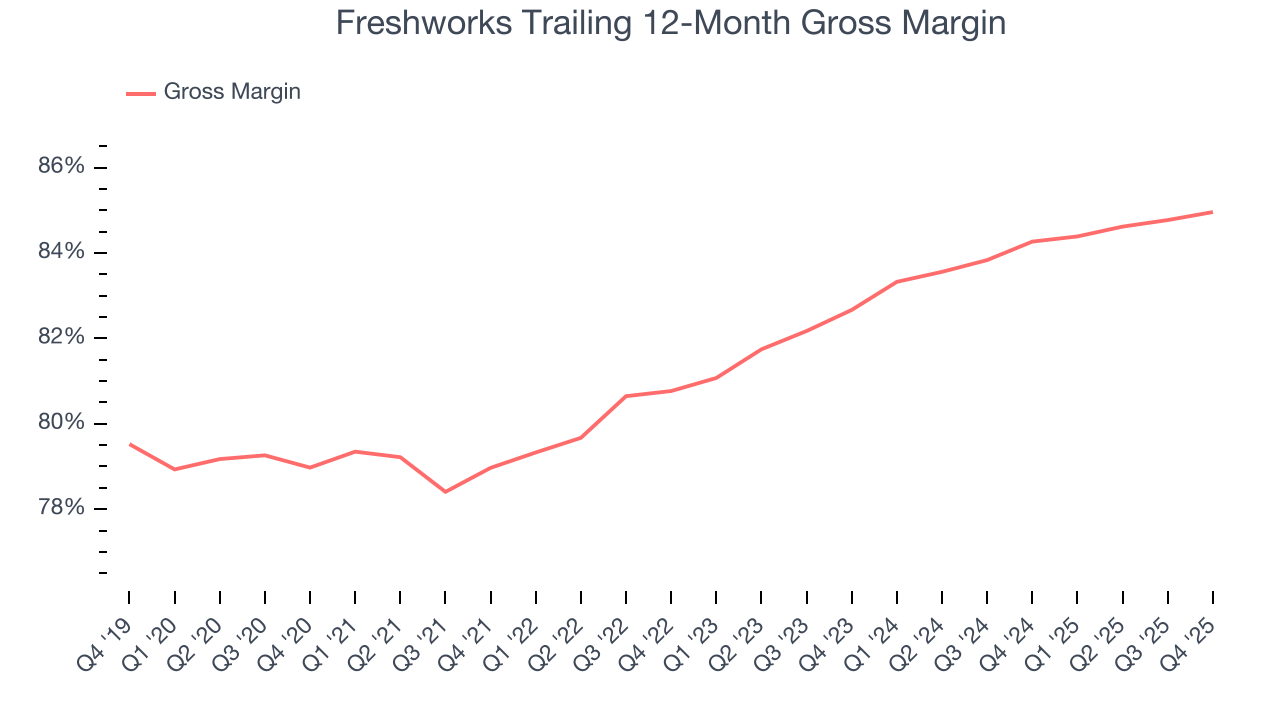

- Software is difficult to replicate at scale and results in a premier gross margin of 85%

- Operating margin improvement of 20.8 percentage points over the last year demonstrates its ability to scale efficiently

- A blemish is its customers generally do not adopt complementary products as its 105% net revenue retention rate lags behind the industry standard

Freshworks shows some potential. If you like the story, the price seems reasonable.

Why Is Now The Time To Buy Freshworks?

Freshworks is trading at $8.12 per share, or 2.4x forward price-to-sales. When viewed through the lens of revenue growth, the current valuation seems quite attractive.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Freshworks (FRSH) Research Report: Q4 CY2025 Update

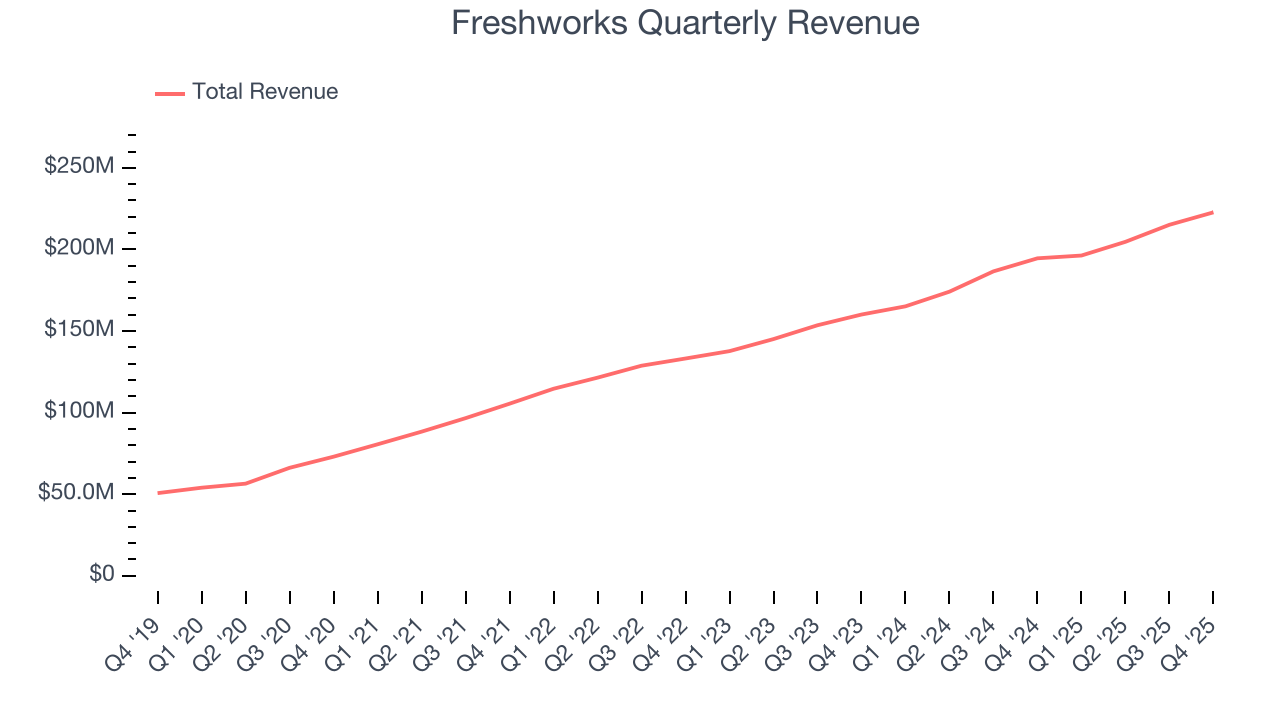

Business software provider Freshworks (NASDAQ:FRSH) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 14.5% year on year to $222.7 million. Guidance for next quarter’s revenue was better than expected at $223.5 million at the midpoint, 1.3% above analysts’ estimates. Its non-GAAP profit of $0.14 per share was 23.8% above analysts’ consensus estimates.

Freshworks (FRSH) Q4 CY2025 Highlights:

- Revenue: $222.7 million vs analyst estimates of $218.7 million (14.5% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.14 vs analyst estimates of $0.11 (23.8% beat)

- Adjusted Operating Income: $41.62 million vs analyst estimates of $32.15 million (18.7% margin, 29.4% beat)

- Revenue Guidance for Q1 CY2026 is $223.5 million at the midpoint, above analyst estimates of $220.7 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.56 at the midpoint, missing analyst estimates by 19%

- Operating Margin: 17.8%, up from -12.2% in the same quarter last year

- Free Cash Flow Margin: 25.2%, down from 26.6% in the previous quarter

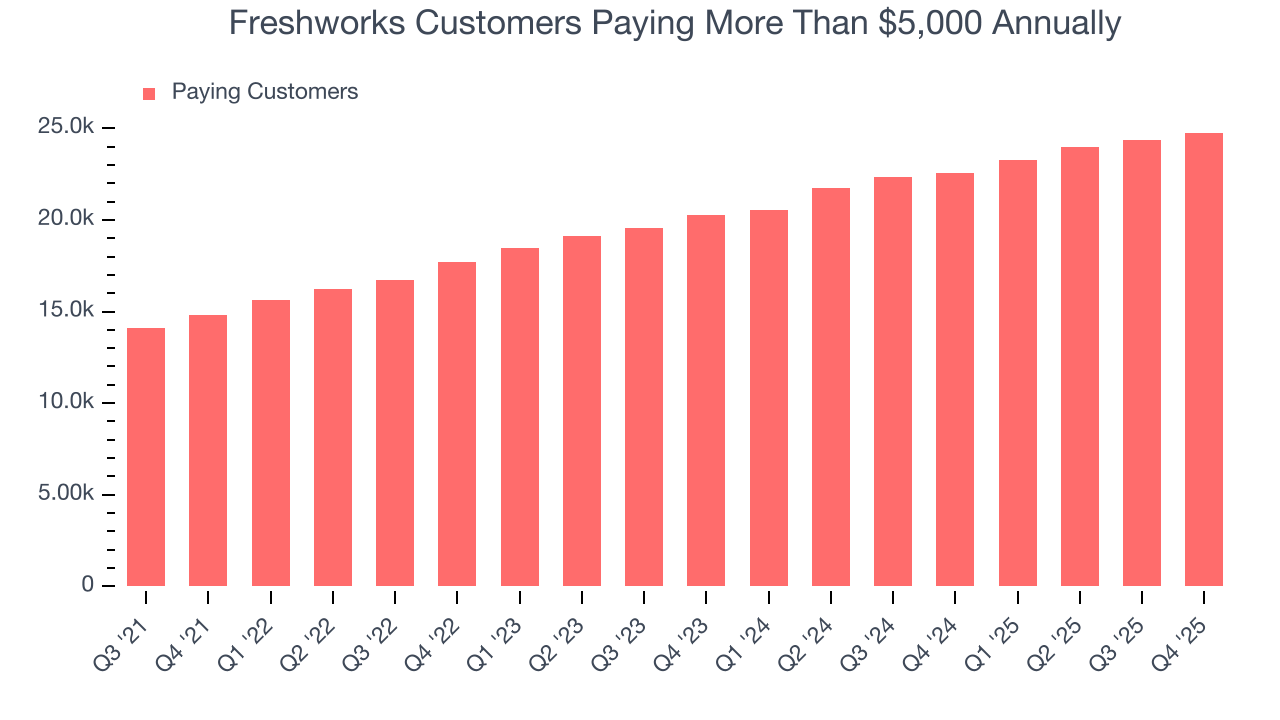

- Customers: 24,762 customers paying more than $5,000 annually

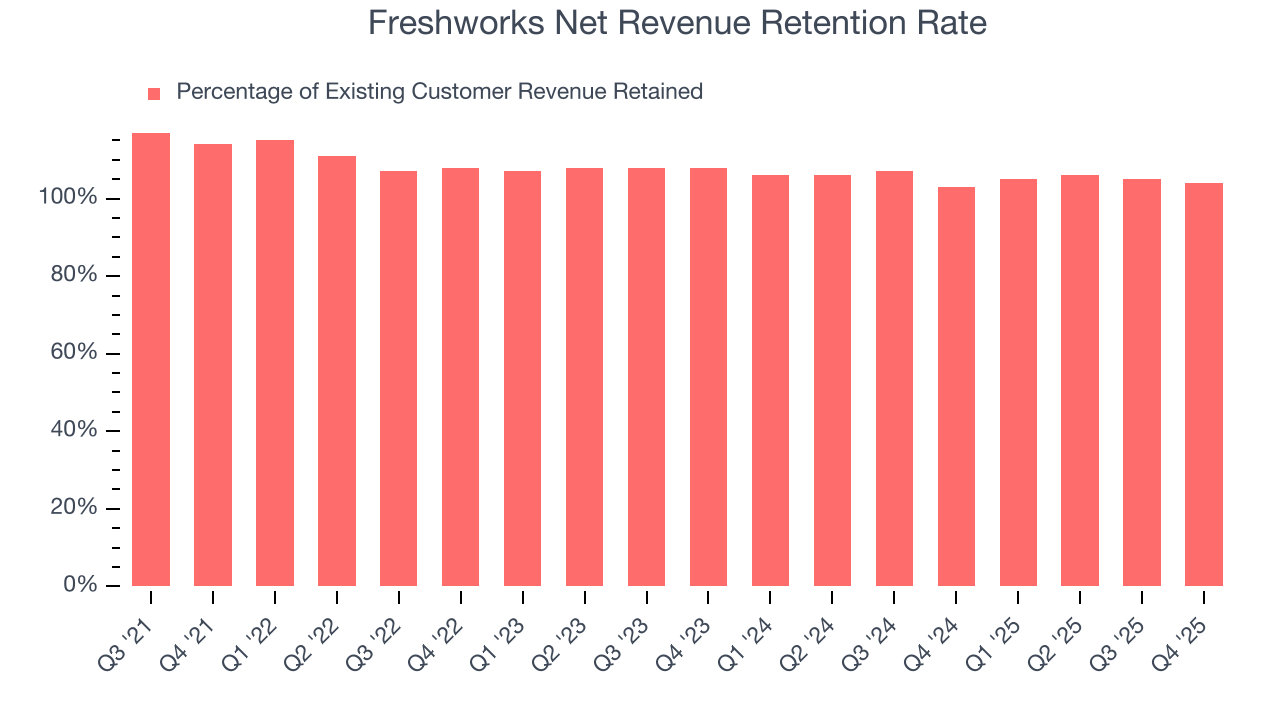

- Net Revenue Retention Rate: 104%, down from 105% in the previous quarter

- Billings: $259.6 million at quarter end, up 16.7% year on year

- Market Capitalization: $2.43 billion

Company Overview

Starting as a customer service solution before expanding into a comprehensive software suite, Freshworks (NASDAQ:FRSH) provides AI-powered software-as-a-service solutions that help companies manage customer service, IT support, sales, and marketing functions.

Freshworks' product ecosystem addresses three core business needs: customer relationship management, IT service management, and sales and marketing automation. Its flagship offerings include Freshdesk for customer service ticketing, Freshservice for IT support, and Freshsales for sales force automation. All products are built on the company's Neo platform, which features Freddy AI, a generative AI engine that provides self-service capabilities, contextual assistance, and actionable insights across all applications.

The company employs a product-led growth strategy with a multi-pronged go-to-market approach. Freshworks offers free trials and subscription plans that range from free to premium tiers, making their solutions accessible to businesses of all sizes—from small startups to large enterprises. This approach removes adoption barriers and accelerates customer acquisition.

A business using Freshworks might deploy Freshdesk to manage customer inquiries across multiple channels, implement Freshservice to streamline their IT department's operations, and utilize Freshsales to track sales opportunities—all while benefiting from the AI-powered automation and insights provided by the Freddy AI engine.

Freshworks monetizes through subscription-based pricing models, with higher tiers offering advanced features and capabilities. The company primarily competes with established enterprise software providers like Salesforce, ServiceNow, and Zendesk, as well as specialized players in each segment and legacy vendors such as Oracle, SAP, and Microsoft.

4. Sales Software

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

Freshworks competes with Salesforce (NYSE:CRM), Zendesk (acquired by private equity), and ServiceNow (NYSE:NOW) in various segments, along with legacy vendors like Oracle (NYSE:ORCL), SAP (NYSE:SAP), and Microsoft (NASDAQ:MSFT). The company also faces competition from specialized providers like HubSpot (NYSE:HUBS) in marketing and Atlassian (NASDAQ:TEAM) in IT service management.

5. Revenue Growth

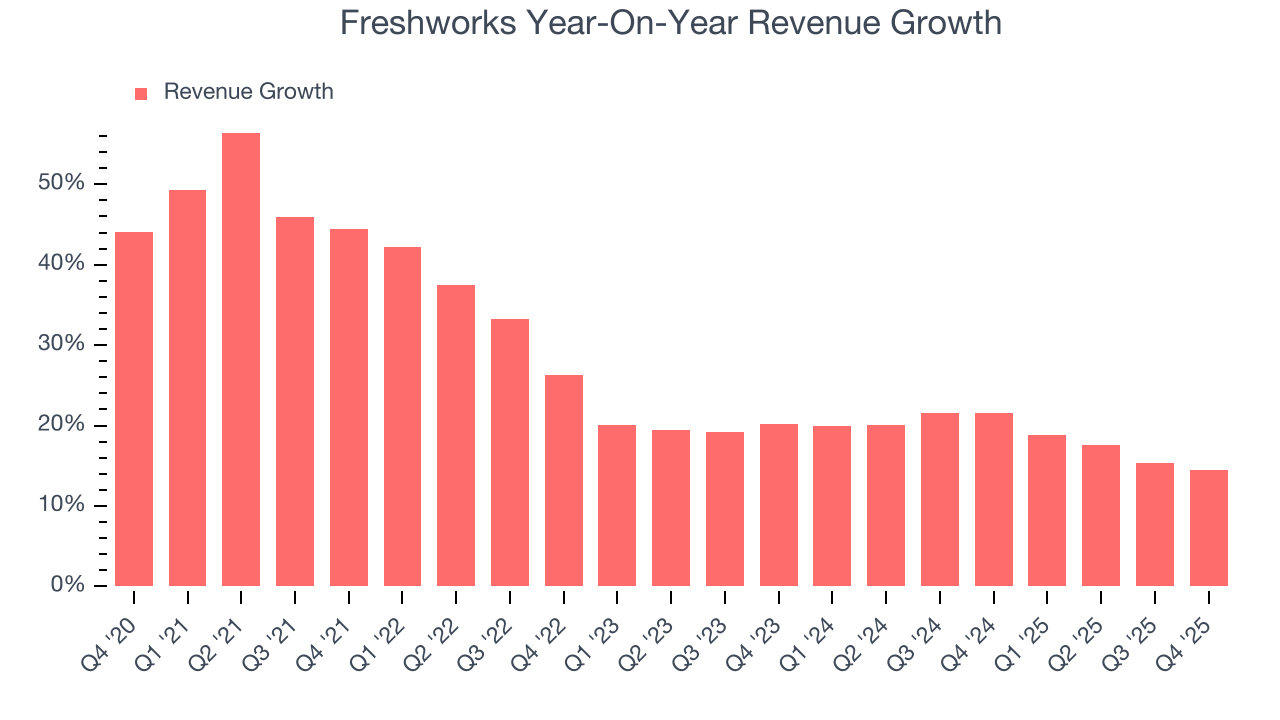

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Freshworks grew its sales at an impressive 27.4% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Freshworks’s annualized revenue growth of 18.6% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Freshworks reported year-on-year revenue growth of 14.5%, and its $222.7 million of revenue exceeded Wall Street’s estimates by 1.8%. Company management is currently guiding for a 13.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

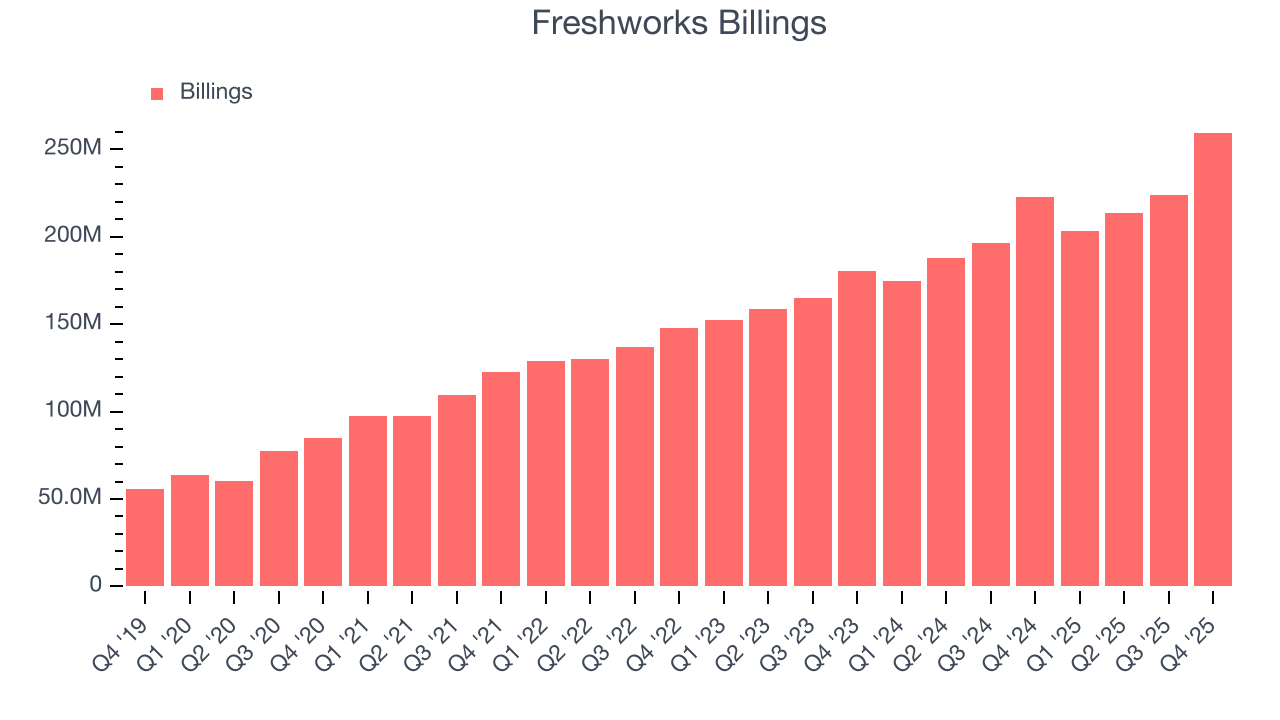

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Freshworks’s billings punched in at $259.6 million in Q4, and over the last four quarters, its growth slightly outpaced the sector as it averaged 15.2% year-on-year increases. This performance aligned with its total sales growth and shows the company is successfully converting sales into cash. Its growth also enhances liquidity and provides a solid foundation for future investments.

7. Enterprise Customer Base

This quarter, Freshworks reported 24,762 enterprise customers paying more than $5,000 annually, an increase of 385 from the previous quarter. That’s in line with the number of contract wins in the last quarter but quite a bit below what we’ve observed over the previous year, suggesting that the slowdown we observed in the last quarter could continue. It also implies that Freshworks will likely need to upsell its existing large customers or move down market to maintain its top-line growth.

8. Customer Acquisition Efficiency

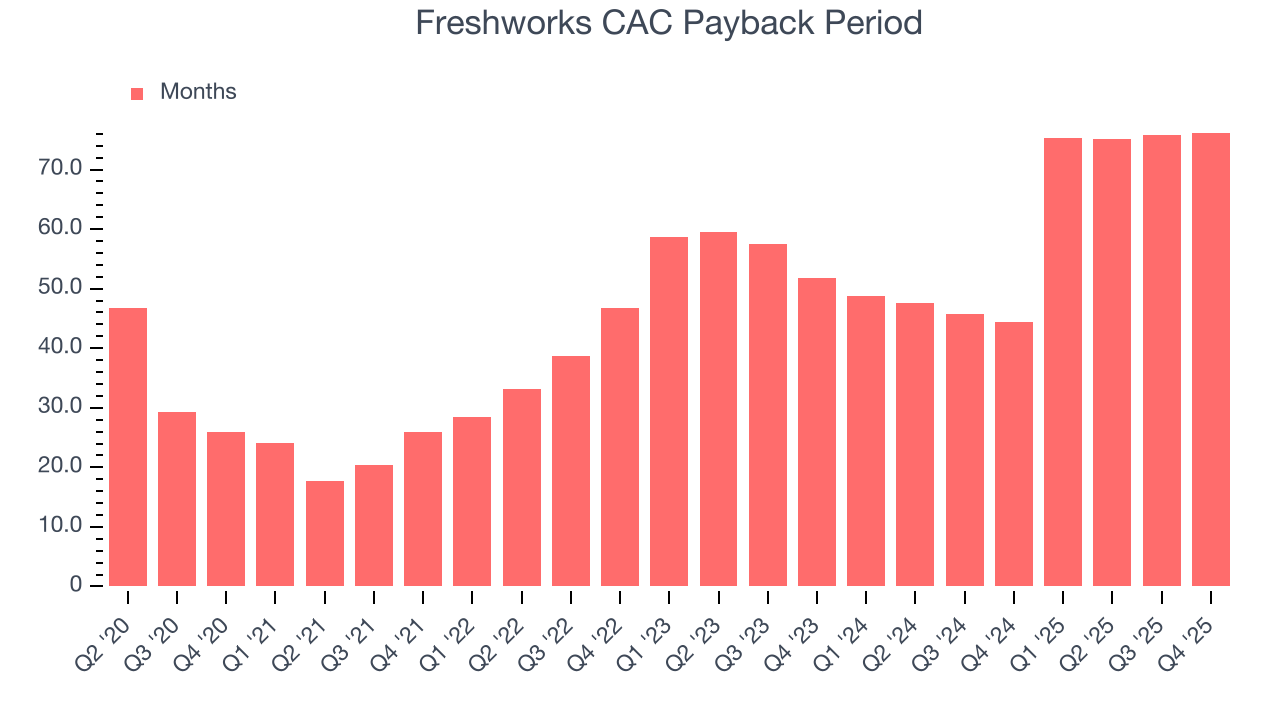

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Freshworks to acquire new customers as its CAC payback period checked in at 76.2 months this quarter. The company’s drawn-out sales cycles partly stem from its focus on enterprise clients who require some degree of customization, resulting in long onboarding periods. The complex integrations are a double-edged sword - while Freshworks may not see immediate returns from its sales and marketing investments, it is rewarded with higher switching costs and lifetime value if it can continue meeting its customer’s needs.

9. Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Freshworks’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 105% in Q4. This means Freshworks would’ve grown its revenue by 5% even if it didn’t win any new customers over the last 12 months.

Freshworks has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

10. Gross Margin & Pricing Power

What makes the software-as-a-service model so attractive is that once the software is developed, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Freshworks’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 85% gross margin over the last year. That means Freshworks only paid its providers $15.04 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Freshworks has seen gross margins improve by 2.3 percentage points over the last 2 year, which is solid in the software space.

This quarter, Freshworks’s gross profit margin was 85.6%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

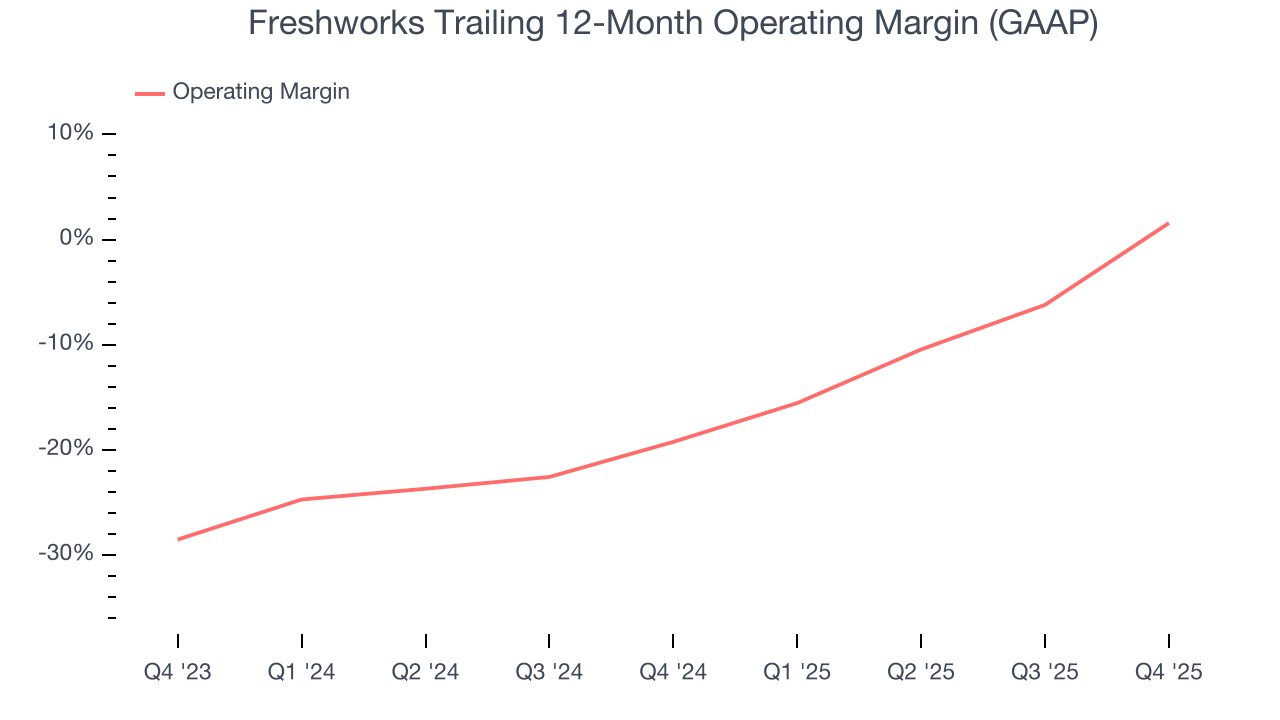

11. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Freshworks has done a decent job managing its cost base over the last year. The company has produced an average operating margin of 1.6%, higher than the broader software sector.

Analyzing the trend in its profitability, Freshworks’s operating margin rose by 20.8 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Freshworks generated an operating margin profit margin of 17.8%, up 30.1 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

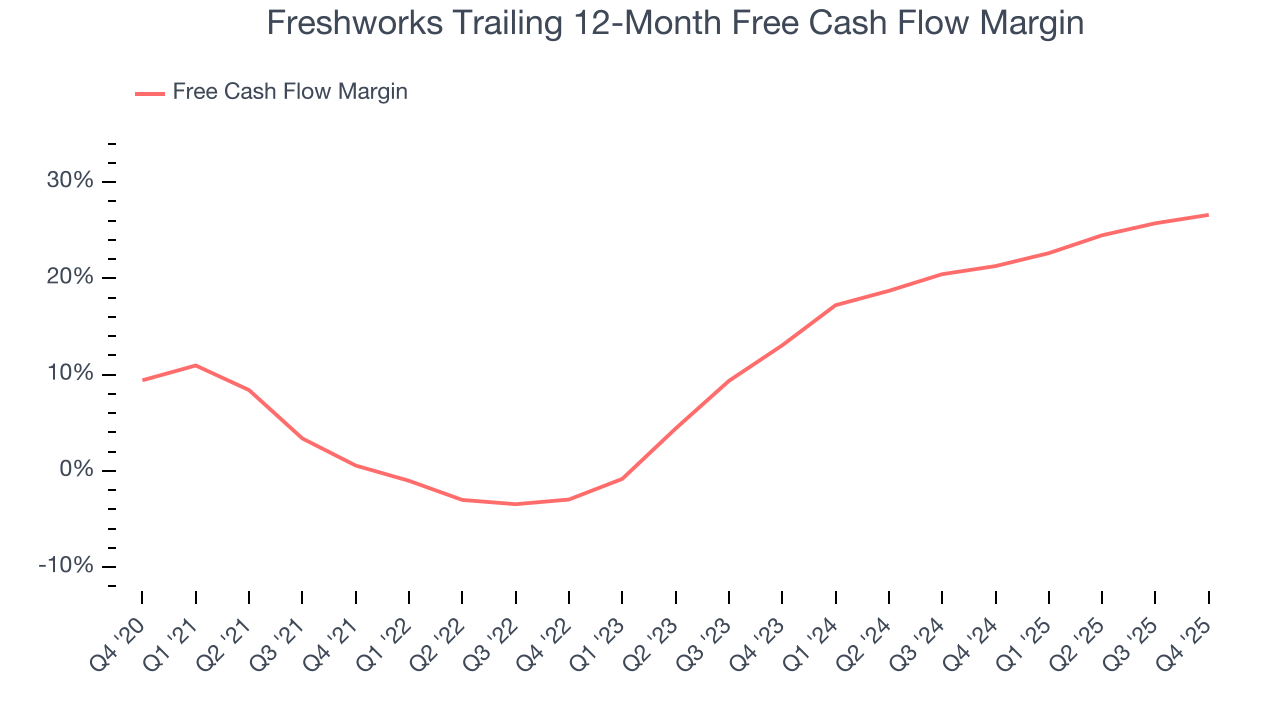

12. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Freshworks has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors while maintaining a cash cushion. The company’s free cash flow margin averaged 26.6% over the last year, quite impressive for a software business.

Freshworks’s free cash flow clocked in at $56.23 million in Q4, equivalent to a 25.2% margin. This result was good as its margin was 3.8 percentage points higher than in the same quarter last year, but we note it was lower than its one-year cash profitability. Nevertheless, we wouldn’t put too much weight on a single quarter because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

Over the next year, analysts’ consensus estimates show they’re expecting Freshworks’s free cash flow margin of 26.6% for the last 12 months to remain the same.

13. Balance Sheet Assessment

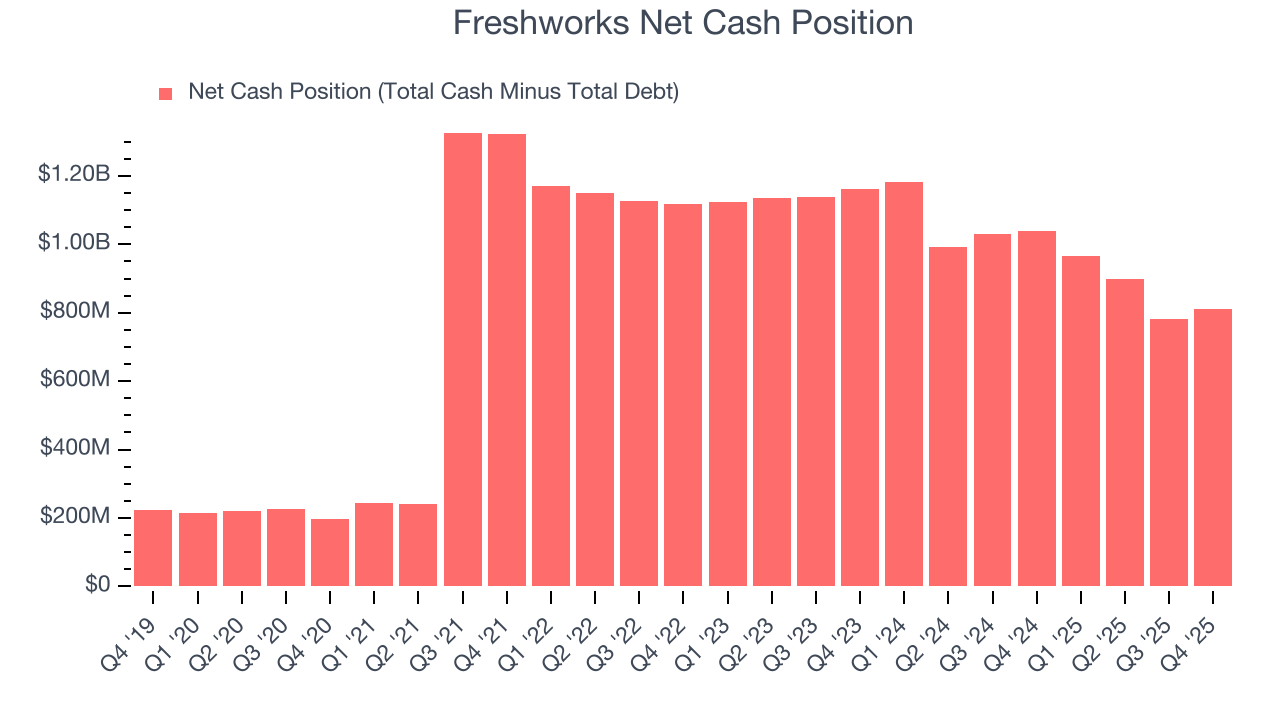

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Freshworks is a profitable, well-capitalized company with $843.7 million of cash and $33.28 million of debt on its balance sheet. This $810.5 million net cash position is 39.4% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

14. Key Takeaways from Freshworks’s Q4 Results

It was good to see Freshworks provide revenue guidance for next quarter that slightly beat analysts’ expectations. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.7% to $8.41 immediately after reporting.

15. Is Now The Time To Buy Freshworks?

Updated: March 15, 2026 at 10:36 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Freshworks, you should also grasp the company’s longer-term business quality and valuation.

There are a lot of things to like about Freshworks. First off, its revenue growth was strong over the last five years. And while its customers generally do not adopt its complementary products, its admirable gross margin indicates excellent unit economics. On top of that, its expanding operating margin shows it’s becoming more efficient at building and selling its software.

Freshworks’s price-to-sales ratio based on the next 12 months is 2.4x. Looking at the software landscape right now, Freshworks trades at a pretty interesting price. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $12.57 on the company (compared to the current share price of $8.12), implying they see 54.8% upside in buying Freshworks in the short term.