GitLab (GTLB)

GitLab is a great business. Its impressive sales growth and unit economics give us a direct line of sight to robust future profits.― StockStory Analyst Team

1. News

2. Summary

Why We Like GitLab

With its all-remote workforce pioneering a new approach to software development, GitLab (NASDAQ:GTLB) provides a single-application DevSecOps platform that helps development, operations, and security teams collaborate to build, secure, and deploy software faster.

- Market share has increased as its 44.4% annual revenue growth over the last five years was exceptional

- Customers view its software as mission-critical to their operations as its ARR has averaged 26.4% growth over the last year

- Prominent and differentiated software culminates in a best-in-class gross margin of 87.4%

GitLab is a standout company. The price seems reasonable relative to its quality, so this could be a prudent time to buy some shares.

Why Is Now The Time To Buy GitLab?

At $22.72 per share, GitLab trades at 3.5x forward price-to-sales. The valuation sure appears attractive, and we suspect the stock is trading below its intrinsic value when factoring in its business quality.

We at StockStory love when high-quality companies go on sale because it enables investors to profit from earnings growth and a potential re-rating - the coveted “double play”.

3. GitLab (GTLB) Research Report: Q4 CY2025 Update

DevSecOps platform provider GitLab (NASDAQ:GTLB) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 23.2% year on year to $260.4 million. On the other hand, next quarter’s revenue guidance of $254 million was less impressive, coming in 0.8% below analysts’ estimates. Its non-GAAP profit of $0.30 per share was 30% above analysts’ consensus estimates.

GitLab (GTLB) Q4 CY2025 Highlights:

- Revenue: $260.4 million vs analyst estimates of $251.9 million (23.2% year-on-year growth, 3.4% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.23 (30% beat)

- Adjusted Operating Income: $53.39 million vs analyst estimates of $38.81 million (20.5% margin, 37.6% beat)

- Revenue Guidance for Q1 CY2026 is $254 million at the midpoint, below analyst estimates of $256 million

- Adjusted EPS guidance for the upcoming financial year 2027 is $0.78 at the midpoint, missing analyst estimates by 24%

- Operating Margin: -2%, up from -7.3% in the same quarter last year

- Free Cash Flow Margin: 16%, up from 11.1% in the previous quarter

- Net Revenue Retention Rate: 118%, down from 119% in the previous quarter

- Market Capitalization: $4.41 billion

Company Overview

With its all-remote workforce pioneering a new approach to software development, GitLab (NASDAQ:GTLB) provides a single-application DevSecOps platform that helps development, operations, and security teams collaborate to build, secure, and deploy software faster.

The company's platform eliminates the need for multiple disconnected tools by integrating the entire software development lifecycle into a unified application with a common interface and data model. This approach addresses the fragmentation challenges of traditional "DIY DevOps" environments where teams use separate tools for each development stage, creating integration complexities and inefficiencies.

GitLab's platform spans the complete DevSecOps lifecycle - from planning and coding to testing, security scanning, deployment, and monitoring. For example, a financial services company might use GitLab to develop a mobile banking application, with developers collaborating on code, security teams automatically scanning for vulnerabilities, and operations teams deploying the tested application to production - all within the same platform.

Operating on an open-core business model, GitLab allows its community of users to contribute improvements to the platform. Customers can choose between self-managed installations in their own environments or GitLab's Software-as-a-Service (SaaS) offering hosted in public or private clouds. The company monetizes through tiered subscription plans (Free, Premium, and Ultimate) with increasing functionality tailored to individual contributors, team managers, and enterprise-wide needs, respectively.

With over 30 million registered users and more than half of Fortune 100 companies as customers, GitLab serves organizations of all sizes across industries globally, helping them accelerate software delivery and innovation.

4. Developer Operations

As Marc Andreessen says, "software is eating the world" which means the volume of software produced is exploding. But building software is complex and difficult work which drives demand for software tools that help increase the speed, quality, and security of software deployment.

GitLab's primary competitor is Microsoft GitHub, following Microsoft's acquisition of GitHub. The company also competes with Atlassian's suite of development tools, as well as point solutions from companies like JFrog, Sonatype, and other DevOps tooling providers.

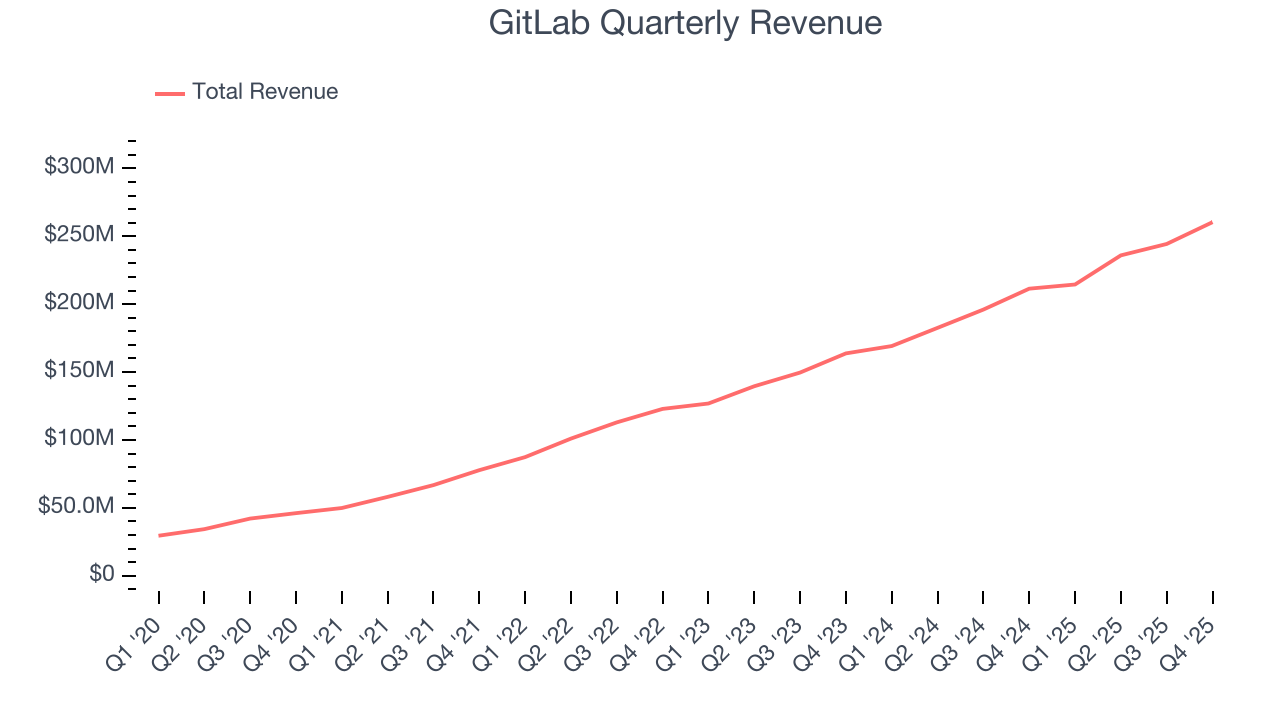

5. Revenue Growth

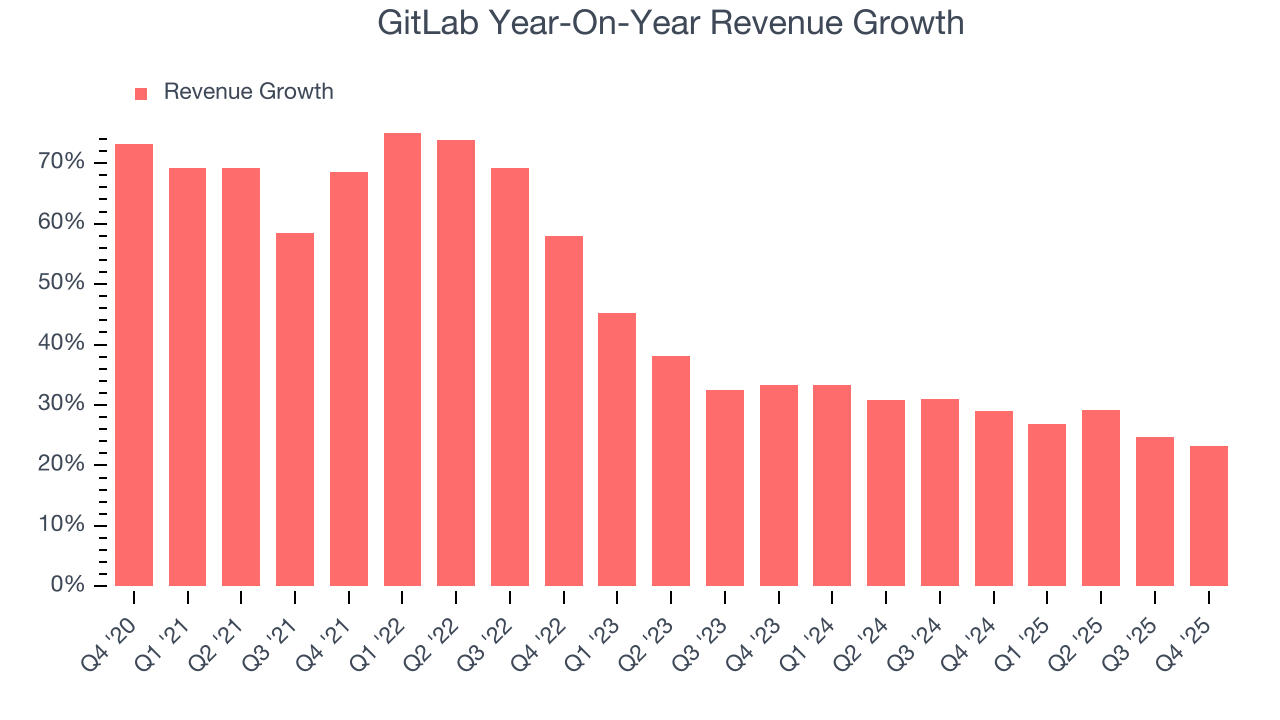

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, GitLab grew its sales at an incredible 44.4% compounded annual growth rate. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. GitLab’s annualized revenue growth of 28.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, GitLab reported robust year-on-year revenue growth of 23.2%, and its $260.4 million of revenue topped Wall Street estimates by 3.4%. Company management is currently guiding for a 18.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 17.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and indicates the market sees success for its products and services.

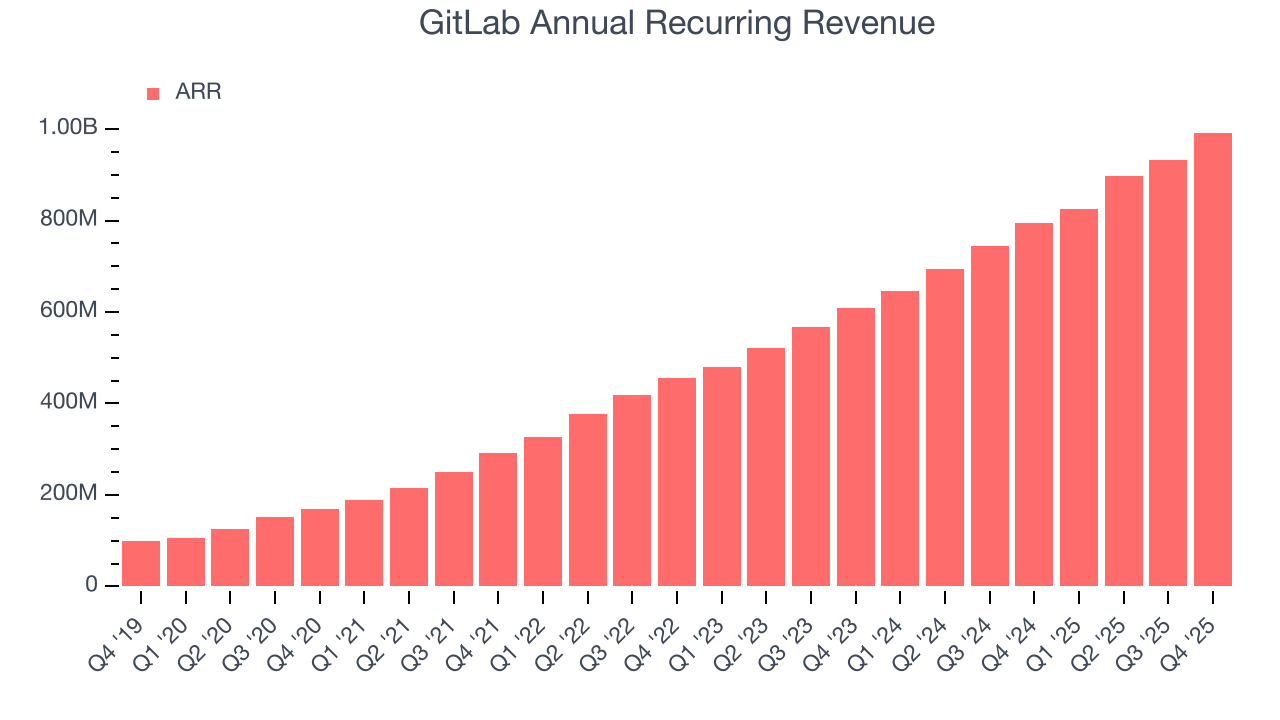

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

GitLab’s ARR punched in at $992.3 million in Q4, and over the last four quarters, its growth was fantastic as it averaged 26.8% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes GitLab a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

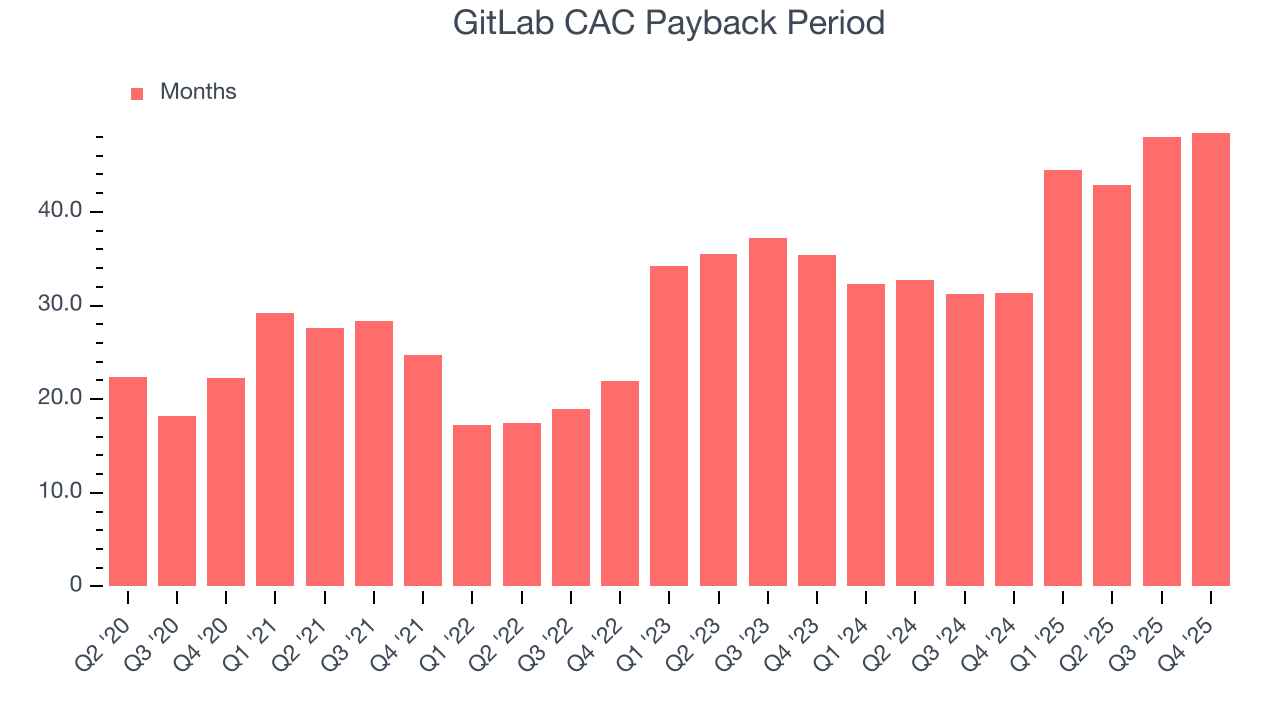

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

GitLab does a decent job acquiring new customers, and its CAC payback period checked in at 48.5 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

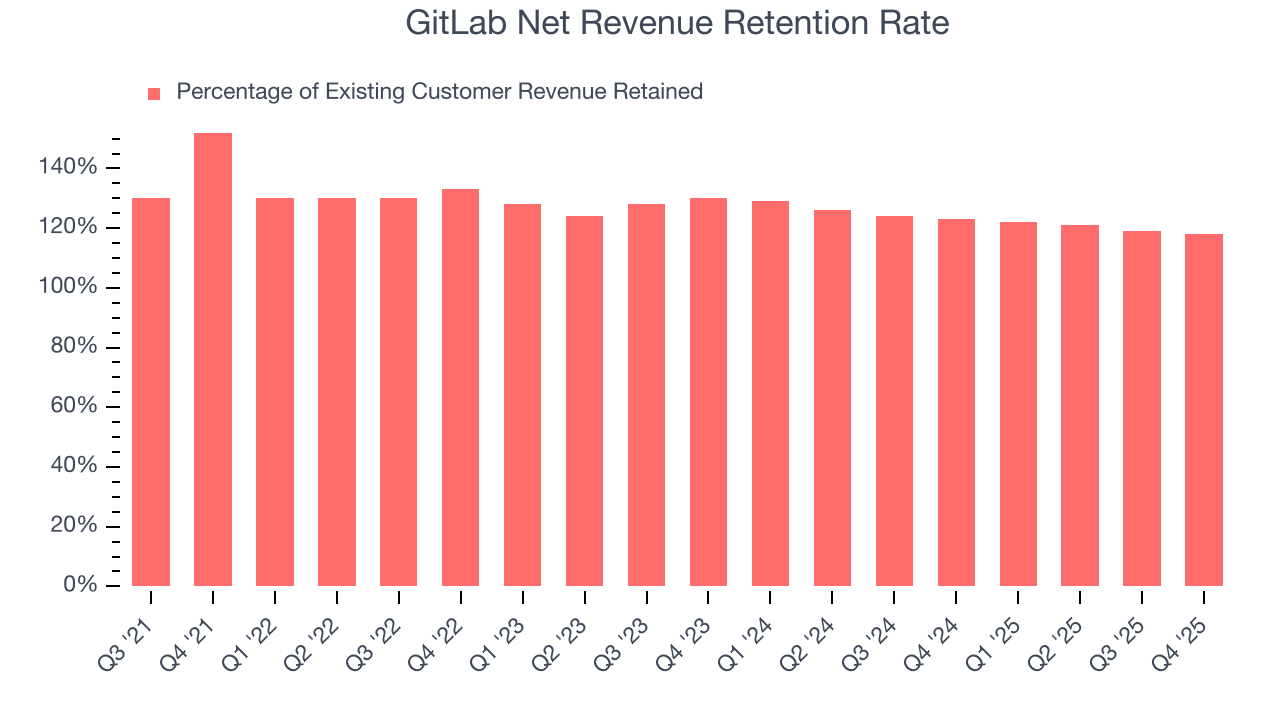

8. Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

GitLab’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 120% in Q4. This means GitLab would’ve grown its revenue by 20% even if it didn’t win any new customers over the last 12 months.

Despite falling over the last year, GitLab still has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

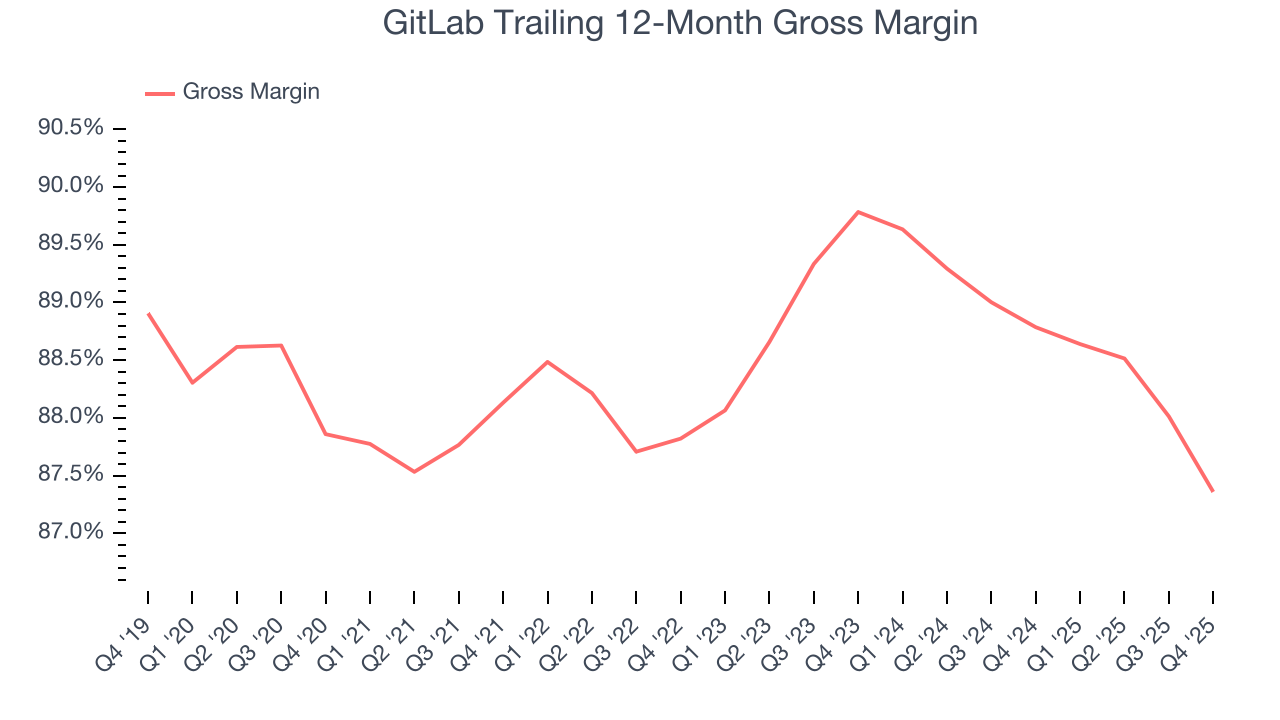

9. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

GitLab’s gross margin is one of the best in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 87.4% gross margin over the last year. Said differently, roughly $87.36 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. GitLab has seen gross margins decline by 2.4 percentage points over the last 2 year, which is among the worst in the software space.

GitLab produced a 86.6% gross profit margin in Q4, down 2.6 percentage points year on year. GitLab’s full-year margin has also been trending down over the past 12 months, decreasing by 1.4 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

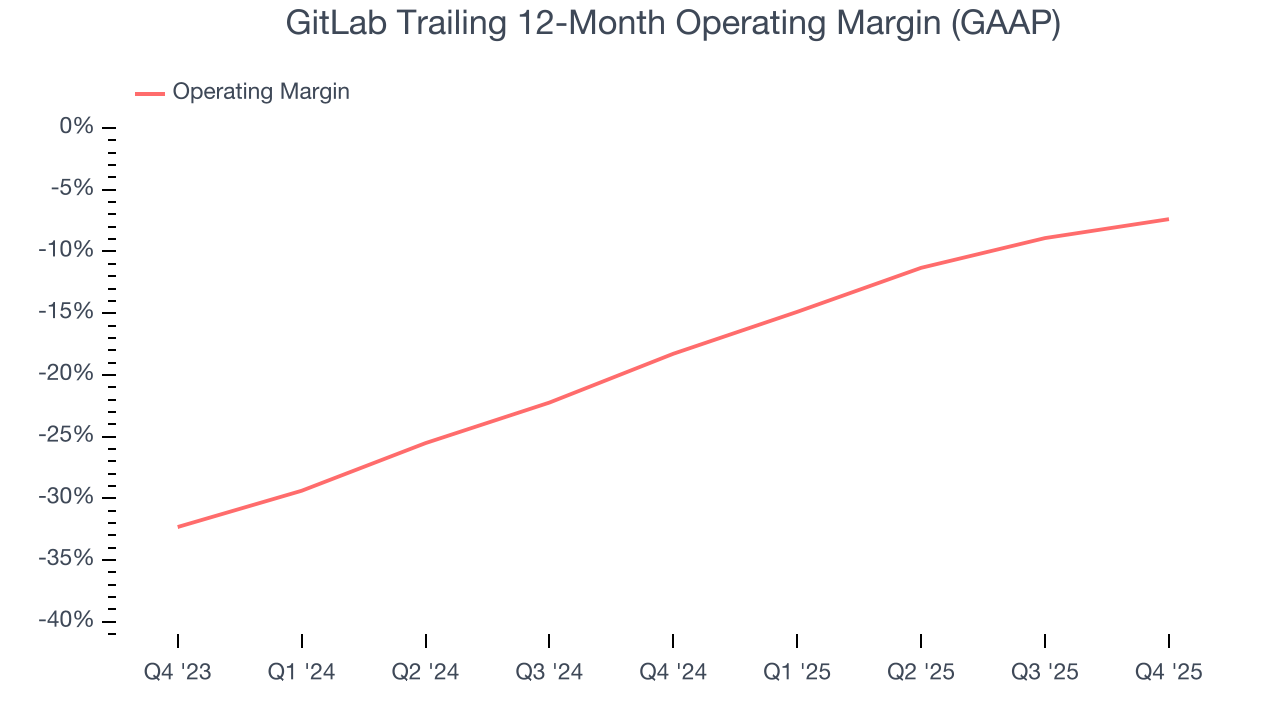

10. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

GitLab’s expensive cost structure has contributed to an average operating margin of negative 7.4% over the last year. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Over the last two years, GitLab’s expanding sales gave it operating leverage as its margin rose by 10.9 percentage points. Still, it will take much more for the company to reach long-term profitability.

This quarter, GitLab generated a negative 2% operating margin.

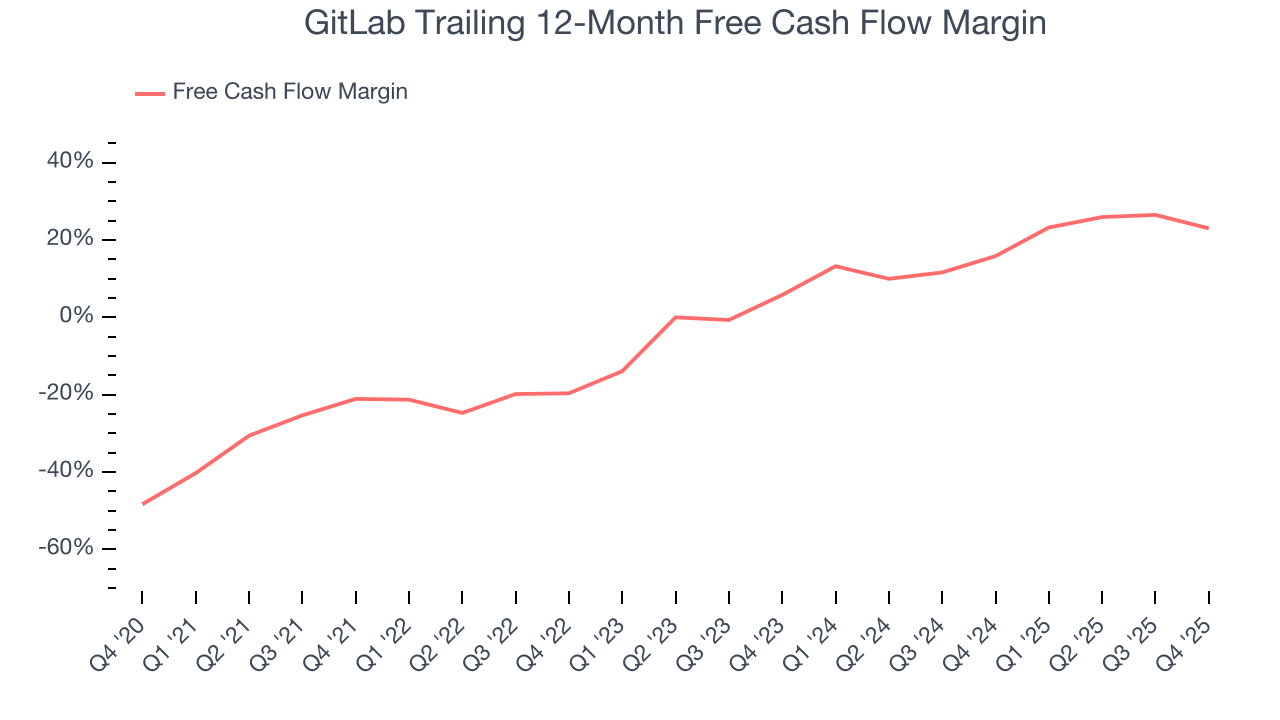

11. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

GitLab has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 23% over the last year, better than the broader software sector. GitLab has shown impressive cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

GitLab’s free cash flow clocked in at $41.78 million in Q4, equivalent to a 16% margin. The company’s cash profitability regressed as it was 13.3 percentage points lower than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts predict GitLab’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 23% for the last 12 months will decrease to 19.6%.

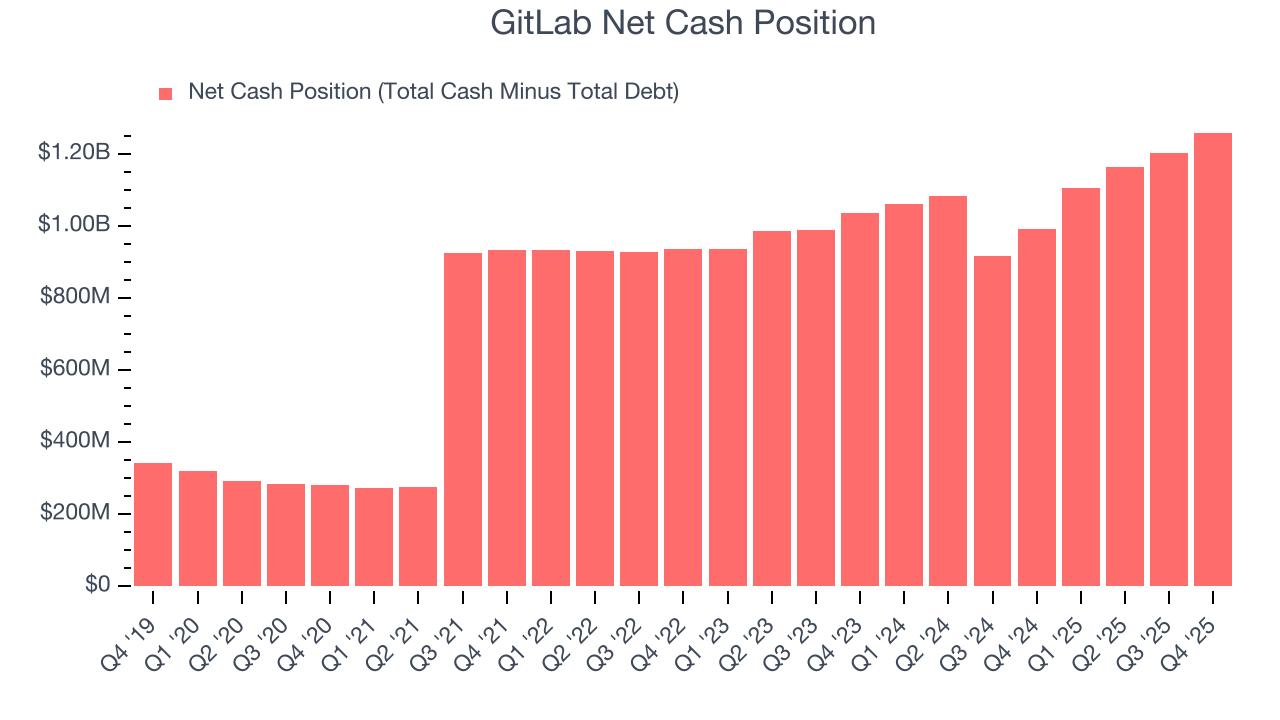

12. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

GitLab is a well-capitalized company with $1.26 billion of cash and no debt. This position is 28% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from GitLab’s Q4 Results

It was encouraging to see GitLab beat analysts’ revenue expectations this quarter. We were also glad its EPS guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.5% to $25.67 immediately after reporting.

14. Is Now The Time To Buy GitLab?

Updated: March 15, 2026 at 10:34 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

There are several reasons why we think GitLab is a great business. For starters, its revenue growth was exceptional over the last five years. And while its operating margins are low compared to other software companies, its admirable gross margin indicates excellent unit economics. On top of that, GitLab’s surging ARR shows its fundamentals and revenue predictability are improving.

GitLab’s price-to-sales ratio based on the next 12 months is 3.5x. Scanning the software space today, GitLab’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $34.20 on the company (compared to the current share price of $22.72), implying they see 50.6% upside in buying GitLab in the short term.