PagerDuty (PD)

PagerDuty is in for a bumpy ride. Its decelerating revenue growth and expected decline in cash profitability will make it tough to beat the market.― StockStory Analyst Team

1. News

2. Summary

Why We Think PagerDuty Will Underperform

Born from the frustration of developers being woken up by unprioritized alerts, PagerDuty (NYSE:PD) is a digital operations management platform that helps organizations detect and respond to IT incidents, outages, and other critical issues in real-time.

- Customers were hesitant to make long-term commitments to its software as its 4.1% average ARR growth over the last year was sluggish

- Sales are projected to remain flat over the next 12 months as demand decelerates from its two-year trend

- Sales trends were unexciting over the last two years as its 6.9% annual growth was well below the typical software company

PagerDuty doesn’t meet our quality standards. There are better opportunities in the market.

Why There Are Better Opportunities Than PagerDuty

At $7.13 per share, PagerDuty trades at 1.3x forward price-to-sales. PagerDuty’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. PagerDuty (PD) Research Report: Q4 CY2025 Update

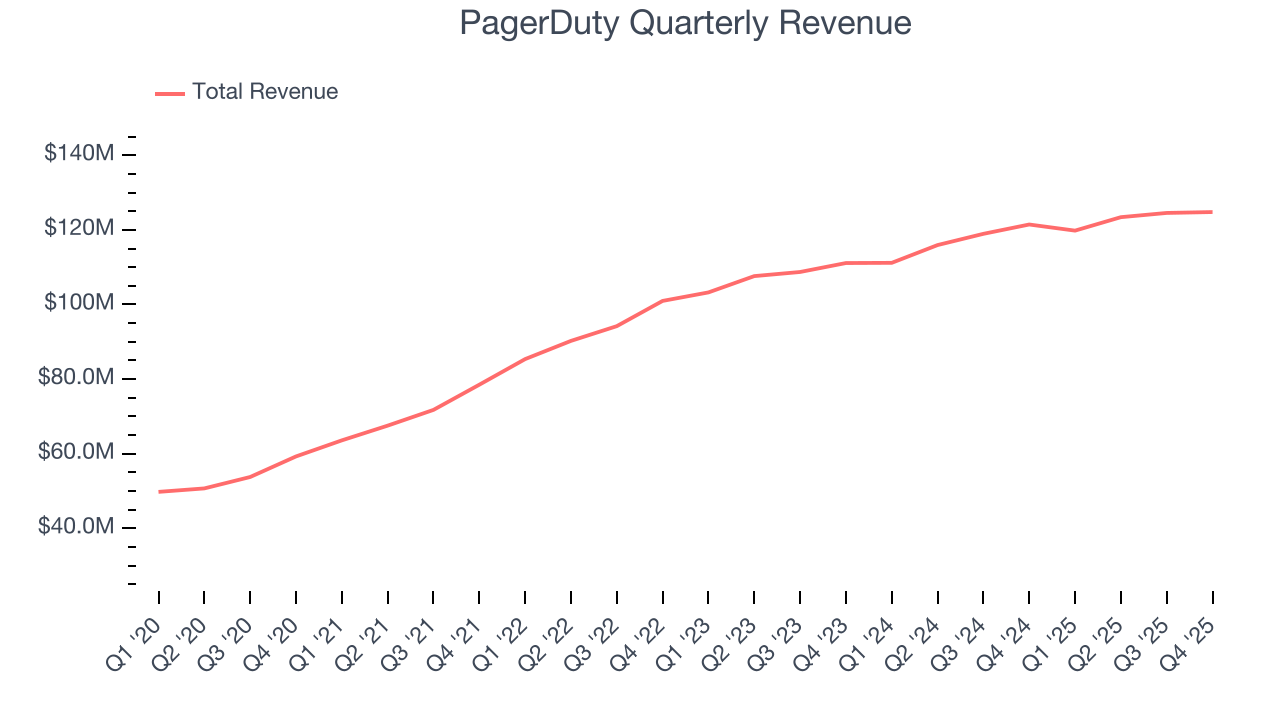

Digital operations platform PagerDuty (NYSE:PD) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 2.7% year on year to $124.8 million. On the other hand, next quarter’s revenue guidance of $119 million was less impressive, coming in 3.9% below analysts’ estimates. Its non-GAAP profit of $0.29 per share was 16.5% above analysts’ consensus estimates.

PagerDuty (PD) Q4 CY2025 Highlights:

- Revenue: $124.8 million vs analyst estimates of $123.2 million (2.7% year-on-year growth, 1.3% beat)

- Adjusted EPS: $0.29 vs analyst estimates of $0.25 (16.5% beat)

- Adjusted Operating Income: $29.83 million vs analyst estimates of $25.52 million (23.9% margin, 16.8% beat)

- Revenue Guidance for Q1 CY2026 is $119 million at the midpoint, below analyst estimates of $123.8 million

- Adjusted EPS guidance for the upcoming financial year 2027 is $1.26 at the midpoint, beating analyst estimates by 5.1%

- Operating Margin: 3.6%, up from -9.6% in the same quarter last year

- Free Cash Flow Margin: 18.1%, up from 16.8% in the previous quarter

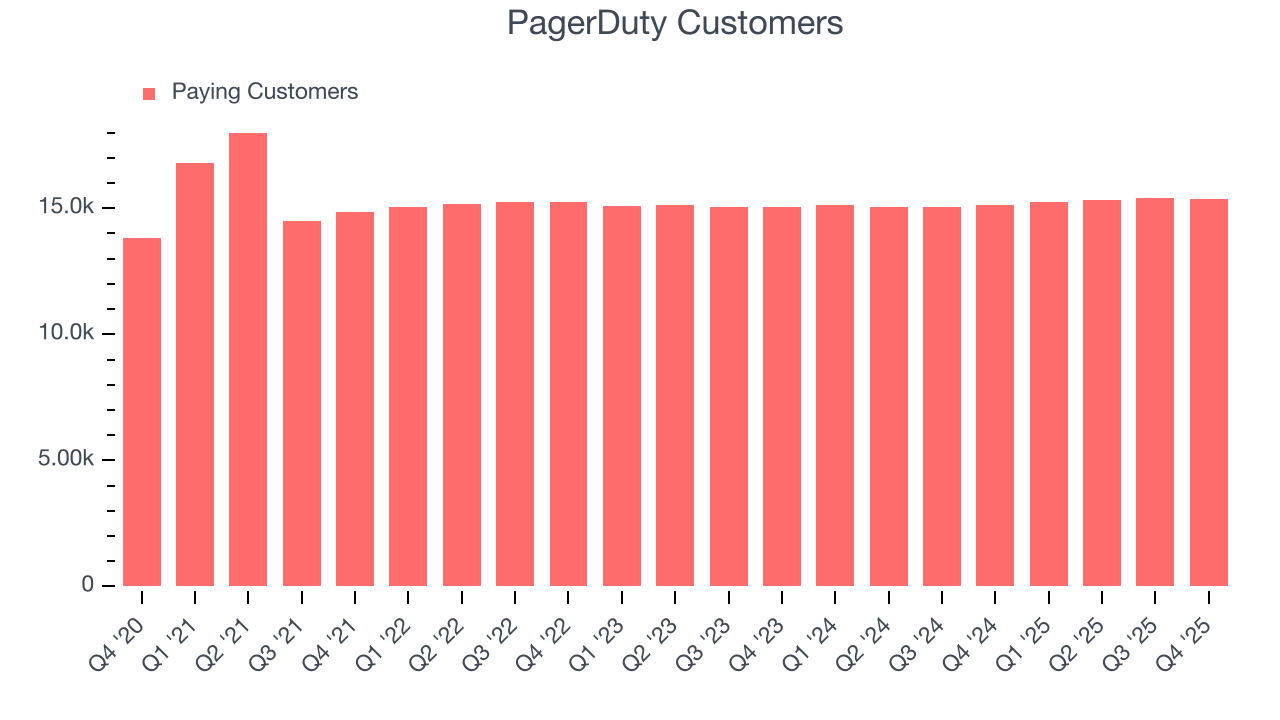

- Customers: 15,351, down from 15,398 in the previous quarter

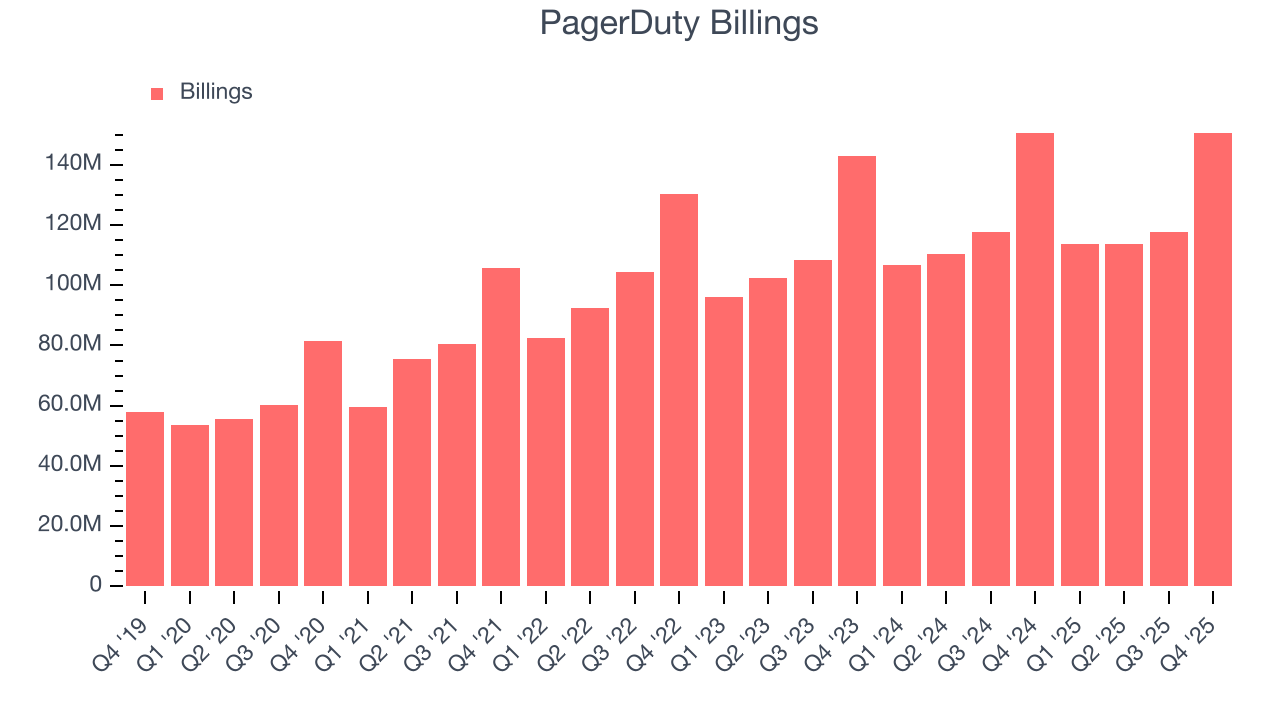

- Billings: $150.7 million at quarter end, in line with the same quarter last year

- Market Capitalization: $674.5 million

Company Overview

Born from the frustration of developers being woken up by unprioritized alerts, PagerDuty (NYSE:PD) is a digital operations management platform that helps organizations detect and respond to IT incidents, outages, and other critical issues in real-time.

The company's Operations Cloud platform combines several key capabilities: artificial intelligence for operations (AIOps), automation, incident management, and customer service operations. This integration enables teams to quickly identify problems, mobilize the right responders, and resolve issues before they significantly impact customers or the business.

PagerDuty's system ingests signals from across an organization's technology stack, using machine learning to filter out noise and correlate related issues. When critical incidents occur, the platform automatically routes alerts to the appropriate teams based on predetermined schedules and escalation policies. This ensures that the right experts are engaged without unnecessary disruption to others.

A healthcare company might use PagerDuty to monitor its patient portal, automatically alerting on-call engineers when response times slow down. Financial institutions rely on it to coordinate rapid responses to potential security breaches. E-commerce businesses deploy it to minimize downtime during high-traffic shopping events.

The company monetizes through a subscription model with tiered pricing based on features and scale. Its platform integrates with over 700 popular tools and services, making it a central hub in many companies' technology ecosystems. PagerDuty has expanded beyond its core developer audience to serve IT teams, security operations, customer service departments, and business stakeholders across organizations of all sizes.

4. Cloud Monitoring

Software is eating the world, increasing organizations’ reliance on digital-only solutions. As more workloads and applications move to the cloud, the reliability of the underlying cloud infrastructure becomes ever more critical and ever more complex. To solve this challenge, companies and their engineering teams have turned to a range of cloud monitoring tools that provide them with the visibility to troubleshoot issues in real-time.

PagerDuty competes with incident management and IT operations platforms including Atlassian's Opsgenie (NASDAQ:TEAM), Splunk (NASDAQ:SPLK), ServiceNow (NYSE:NOW), and Everbridge (NASDAQ:EVBG), as well as offerings from companies like Red Hat (part of IBM) and xMatters (acquired by Everbridge).

5. Revenue Growth

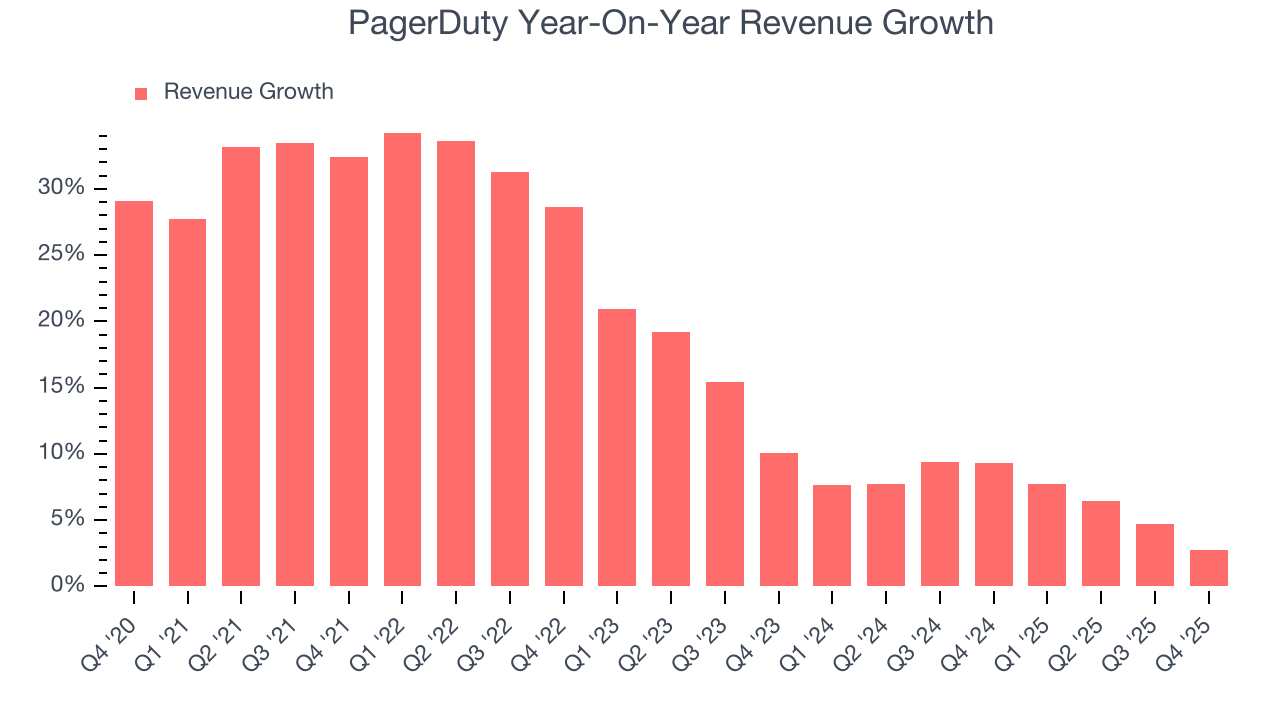

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, PagerDuty’s 18.2% annualized revenue growth over the last five years was decent. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. PagerDuty’s recent performance shows its demand has slowed as its annualized revenue growth of 6.9% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, PagerDuty reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 1.3%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

PagerDuty’s billings came in at $150.7 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 2.5% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

7. Customer Base

PagerDuty reported 15,351 customers at the end of the quarter, a sequential decrease of 47. That’s worse than what we’ve observed previously, and we’ve no doubt shareholders would like to see the company accelerate its sales momentum.

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for PagerDuty to acquire new customers as its CAC payback period checked in at 179.1 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

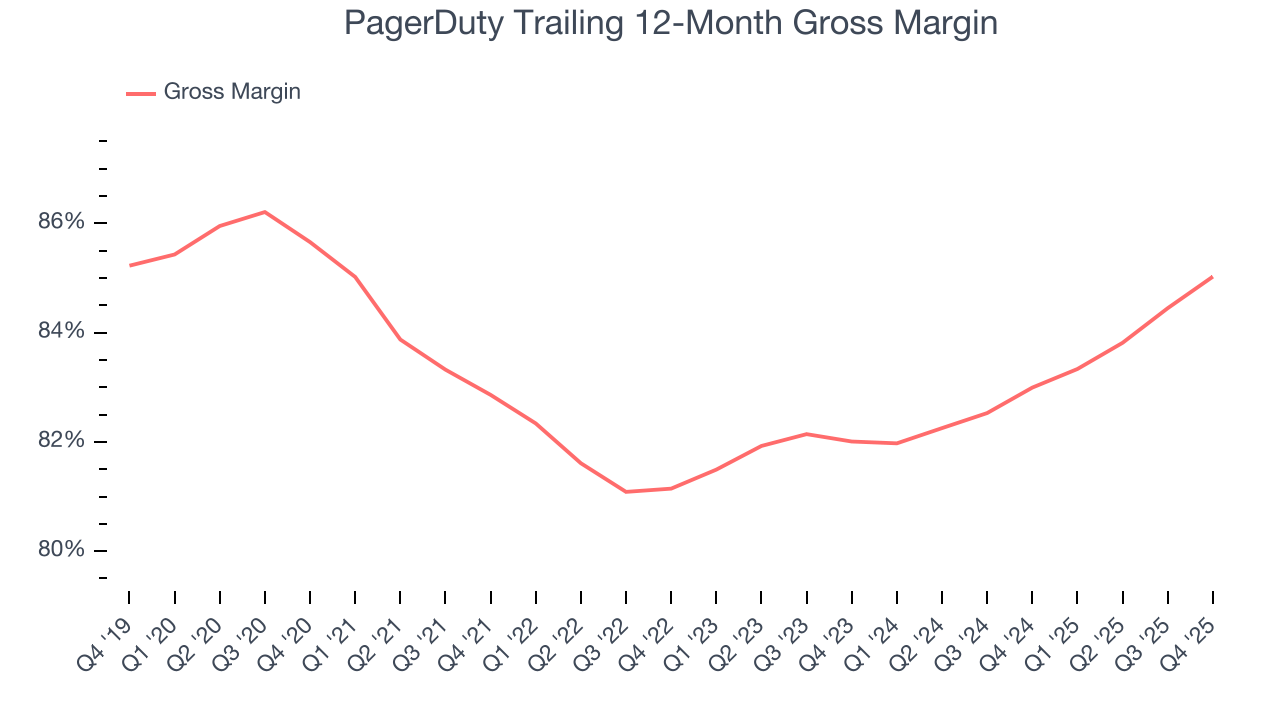

9. Gross Margin & Pricing Power

For software companies like PagerDuty, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

PagerDuty’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 85% gross margin over the last year. Said differently, roughly $85.02 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. PagerDuty has seen gross margins improve by 3 percentage points over the last 2 year, which is very good in the software space.

In Q4, PagerDuty produced a 85.9% gross profit margin, up 2.3 percentage points year on year. PagerDuty’s full-year margin has also been trending up over the past 12 months, increasing by 2 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

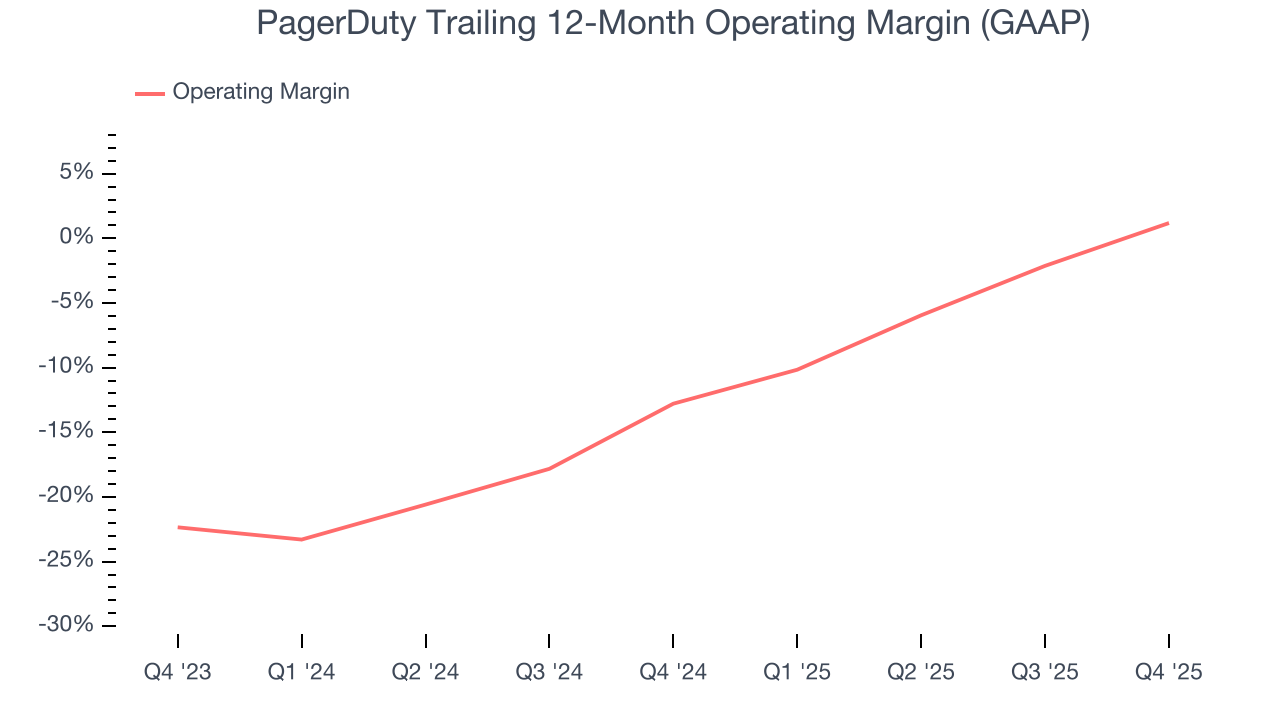

10. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

PagerDuty has done a decent job managing its cost base over the last year. The company has produced an average operating margin of 1.2%, higher than the broader software sector.

Looking at the trend in its profitability, PagerDuty’s operating margin rose by 14 percentage points over the last two years, as its sales growth gave it operating leverage.

This quarter, PagerDuty generated an operating margin profit margin of 3.6%, up 13.3 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

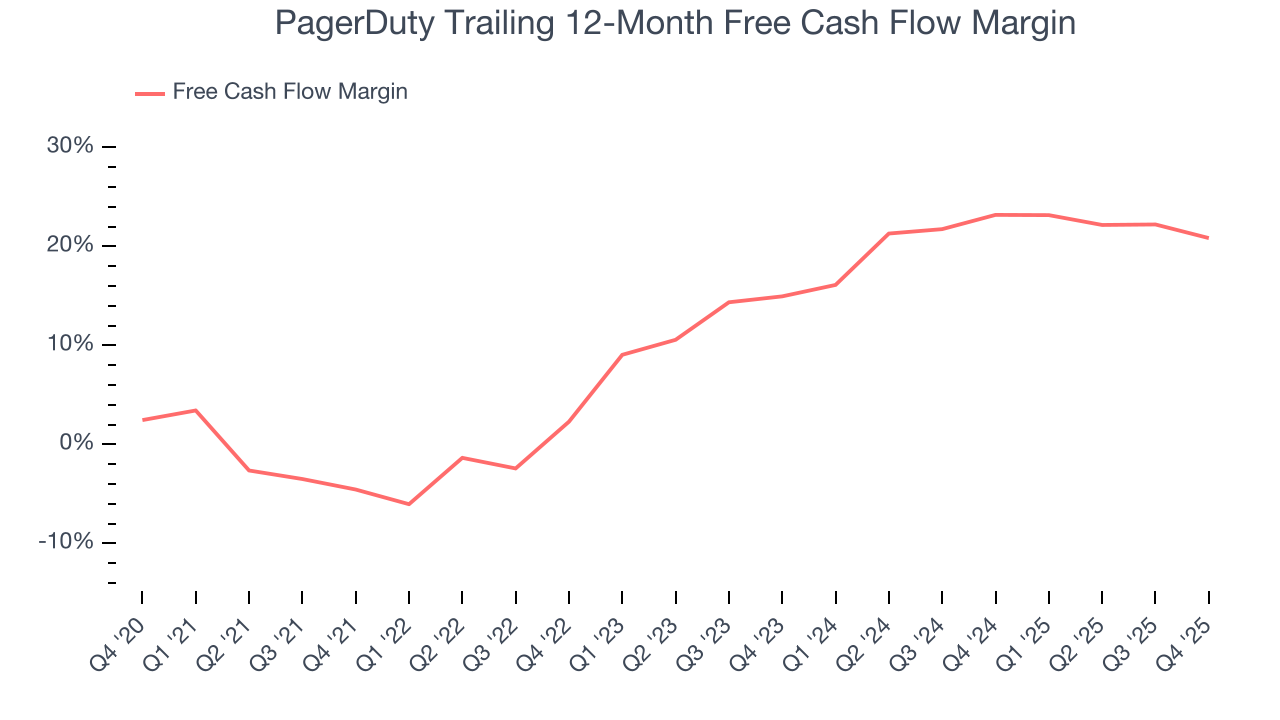

11. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

PagerDuty has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 20.8% over the last year, better than the broader software sector.

PagerDuty’s free cash flow clocked in at $22.56 million in Q4, equivalent to a 18.1% margin. The company’s cash profitability regressed as it was 5.5 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict PagerDuty’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 20.8% for the last 12 months will increase to 25.4%, it options for capital deployment (investments, share buybacks, etc.).

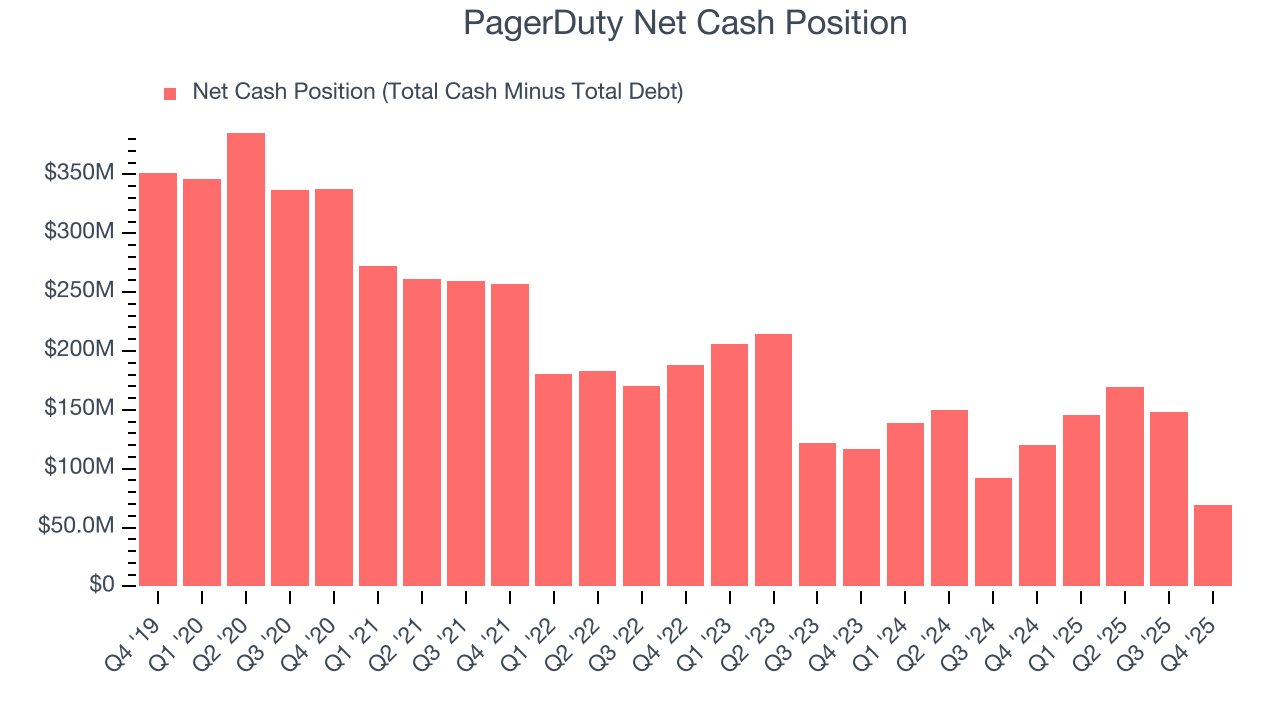

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

PagerDuty is a profitable, well-capitalized company with $469.8 million of cash and $400.7 million of debt on its balance sheet. This $69.11 million net cash position is 11.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from PagerDuty’s Q4 Results

We were impressed by PagerDuty’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also happy its billings narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 14.9% to $6.24 immediately following the results.

14. Is Now The Time To Buy PagerDuty?

Updated: March 14, 2026 at 10:14 PM EDT

Are you wondering whether to buy PagerDuty or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

We see the value of companies addressing major business pain points, but in the case of PagerDuty, we’re out. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its ARR has disappointed and shows the company is having difficulty retaining customers and their spending.

PagerDuty’s price-to-sales ratio based on the next 12 months is 1.3x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $8 on the company (compared to the current share price of $7.13).