B&G Foods (BGS)

B&G Foods faces an uphill battle. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think B&G Foods Will Underperform

Started as a small grocery store in New York City, B&G Foods (NYSE:BGS) is an American packaged foods company with a diverse portfolio of more than 50 brands.

- Products have few die-hard fans as sales have declined by 5.4% annually over the last three years

- Projected sales decline of 8.9% over the next 12 months indicates demand will continue deteriorating

- 7× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

B&G Foods falls short of our expectations. We see more attractive opportunities in the market.

Why There Are Better Opportunities Than B&G Foods

B&G Foods’s stock price of $5.25 implies a valuation ratio of 9x forward P/E. B&G Foods’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. B&G Foods (BGS) Research Report: Q4 CY2025 Update

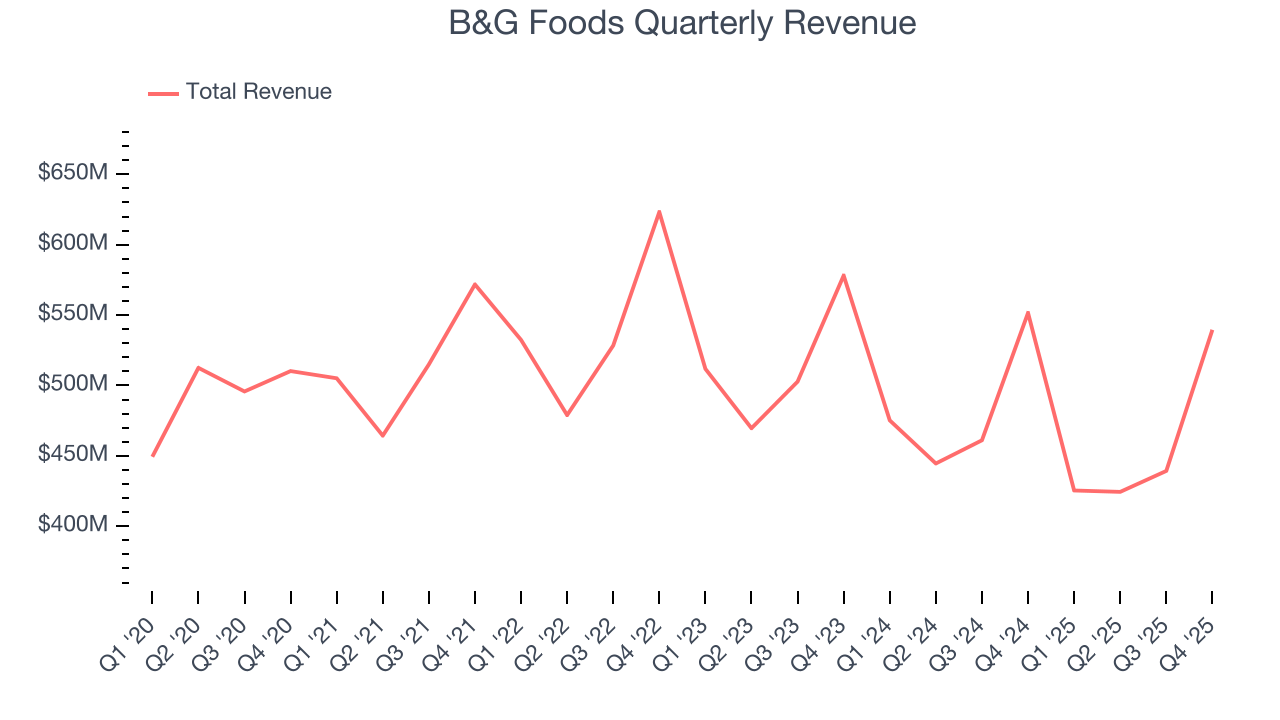

Packaged foods company B&G Foods (NYSE:BGS) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 2.2% year on year to $539.6 million. On the other hand, the company’s full-year revenue guidance of $1.68 billion at the midpoint came in 5.6% below analysts’ estimates. Its non-GAAP profit of $0.28 per share was 7.1% below analysts’ consensus estimates.

B&G Foods (BGS) Q4 CY2025 Highlights:

- Revenue: $539.6 million vs analyst estimates of $536.1 million (2.2% year-on-year decline, 0.6% beat)

- Adjusted EPS: $0.28 vs analyst expectations of $0.30 (7.1% miss)

- Adjusted EBITDA: $84.68 million vs analyst estimates of $87.2 million (15.7% margin, 2.9% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.60 at the midpoint, beating analyst estimates by 17.5%

- EBITDA guidance for the upcoming financial year 2026 is $270 million at the midpoint, above analyst estimates of $265.3 million

- Operating Margin: 5.2%, up from -46.6% in the same quarter last year

- Sales Volumes were flat year on year (2.2% in the same quarter last year)

- Market Capitalization: $414.3 million

Company Overview

Started as a small grocery store in New York City, B&G Foods (NYSE:BGS) is an American packaged foods company with a diverse portfolio of more than 50 brands.

The company was founded in 1889 by brothers Ralph and George Burns, along with their business partner George Brinkman. Their humble grocery store quickly gained popularity on the East Coast for its creamed horseradish, and the rest is history.

Over the next century, B&G Foods would enter the packaged foods business, acquiring several well-known brands such as Ortega, Green Giant, and Cream of Wheat, among others. These acquisitions allowed the company to expand its product offerings and introduce a wide range of beloved food products to consumers. Today, B&G Foods sells everything from canned vegetables to hot sauces, spices, snacks, and breakfast favorites.

The company continuously explores new flavors, packaging innovations, and product formulations to meet changing consumer demands and preferences. For example, it’s collaborated with Cinnamon Toast Crunch, Einstein Bros Bagels, Girl Scouts, and Snickers to manufacture and distribute branded seasoning blends.

While deeply rooted in the United States, B&G Foods has a global reach, and its products are available in various countries. It reaches consumers mostly through retail partnerships with grocery stores and retailers such as Walmart, Kroger, Publix, and Safeway.

4. Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors in the packaged foods industry include Conagra (NYSE:CAG), General Mills (NYSE:GIS), Hormel Foods (NYSE:HRL), Kraft Heinz (NASDAQ:KHC), and McCormick (NYSE:MKC).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.83 billion in revenue over the past 12 months, B&G Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, B&G Foods’s revenue declined by 5.4% per year over the last three years despite selling a similar number of units each year. We’ll explore what this means in the "Volume Growth" section.

This quarter, B&G Foods’s revenue fell by 2.2% year on year to $539.6 million but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to decline by 4.2% over the next 12 months, similar to its three-year rate. it’s tough to feel optimistic about a company facing demand difficulties.

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

B&G Foods’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

In B&G Foods’s Q4 2025, year on year sales volumes were flat. This result was more or less in line with its historical levels.

7. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

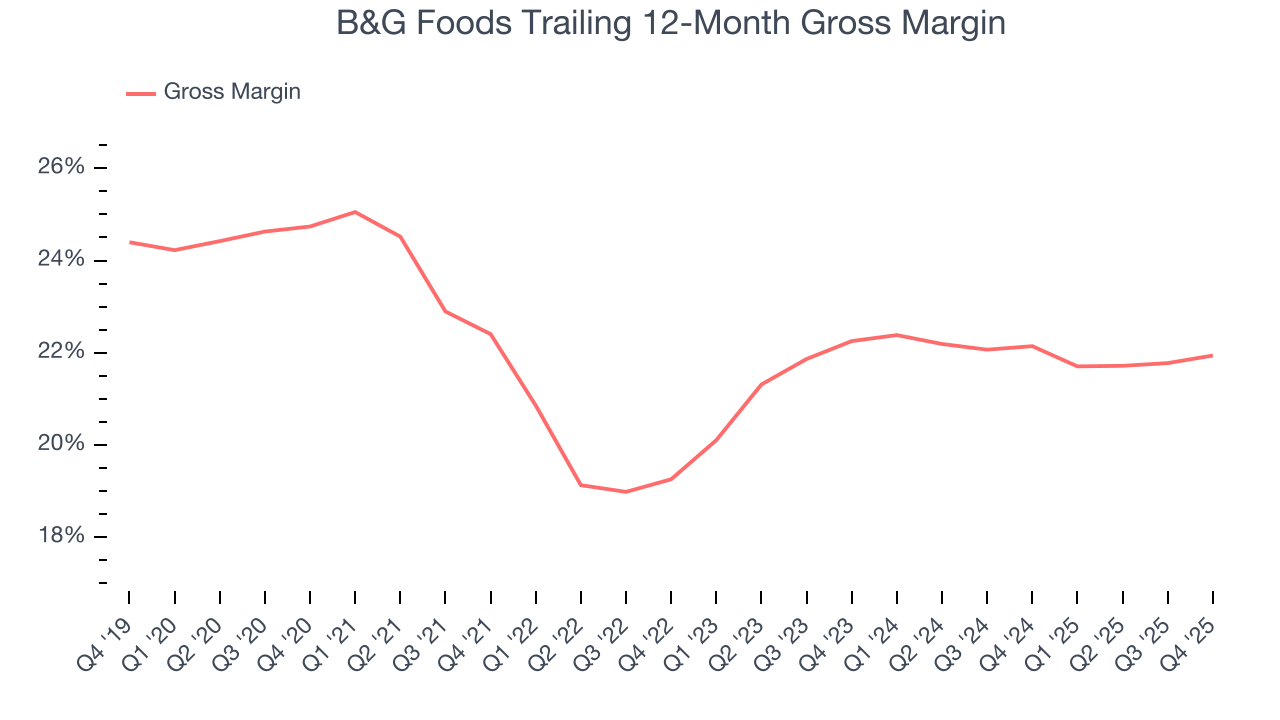

B&G Foods has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 22% gross margin over the last two years. That means B&G Foods paid its suppliers a lot of money ($77.95 for every $100 in revenue) to run its business.

This quarter, B&G Foods’s gross profit margin was 22.7%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

8. Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

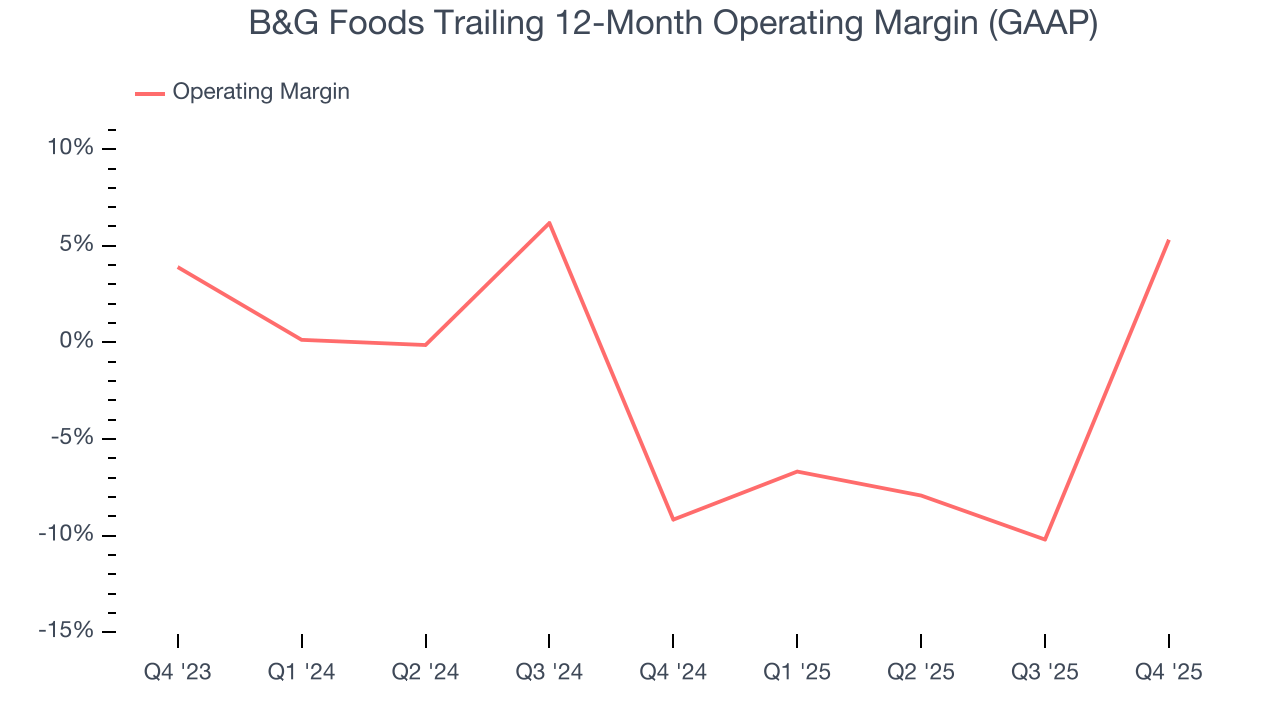

Although B&G Foods was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 2.1% over the last two years. Unprofitable public companies are rare in the defensive consumer staples industry, so this performance certainly caught our eye.

On the plus side, B&G Foods’s operating margin rose by 14.5 percentage points over the last year. Still, it will take much more for the company to show consistent profitability.

In Q4, B&G Foods generated an operating margin profit margin of 5.2%, up 51.8 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

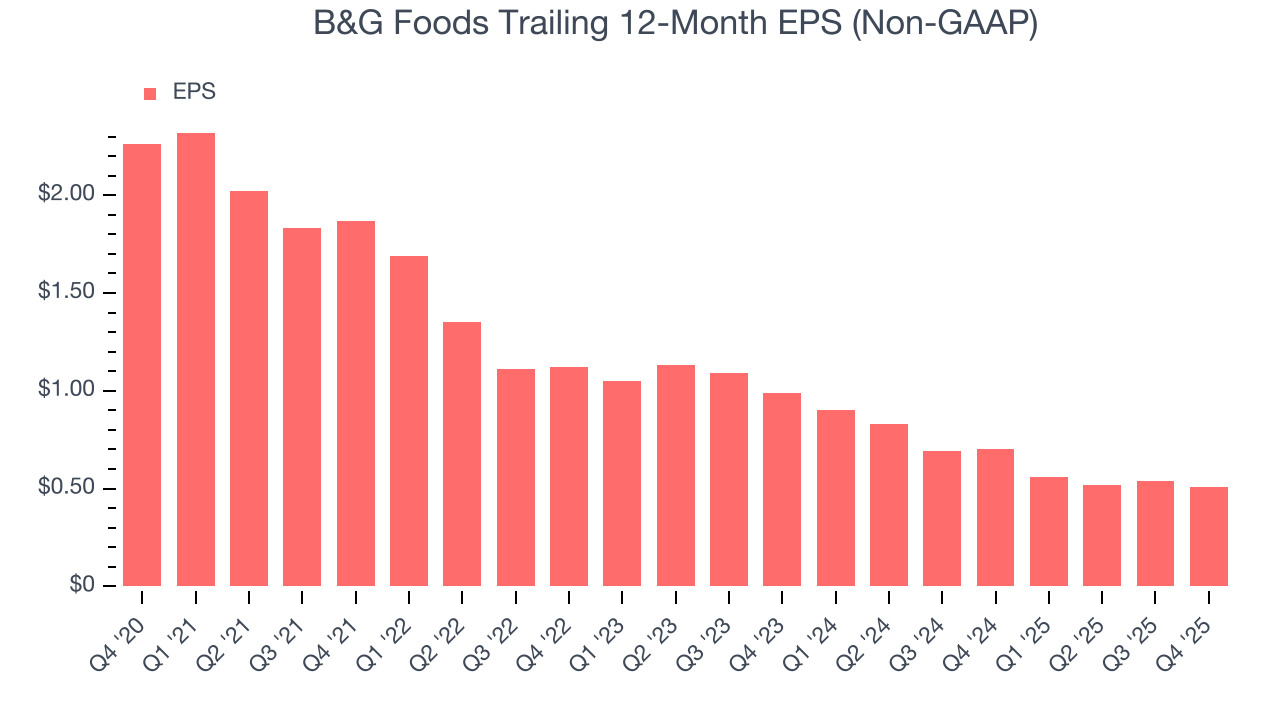

Sadly for B&G Foods, its EPS declined by 23.1% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, B&G Foods reported adjusted EPS of $0.28, down from $0.31 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects B&G Foods’s full-year EPS of $0.51 to stay about the same.

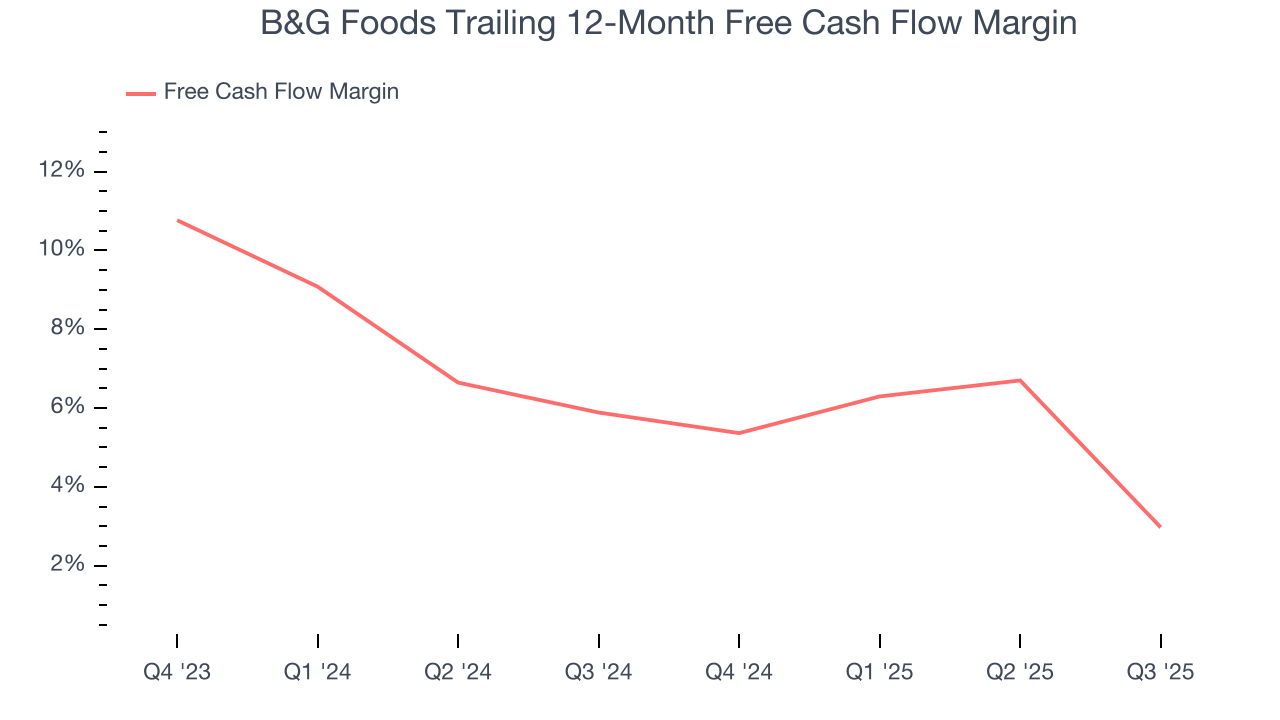

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

B&G Foods has shown weak cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, below what we’d expect for a consumer staples business.

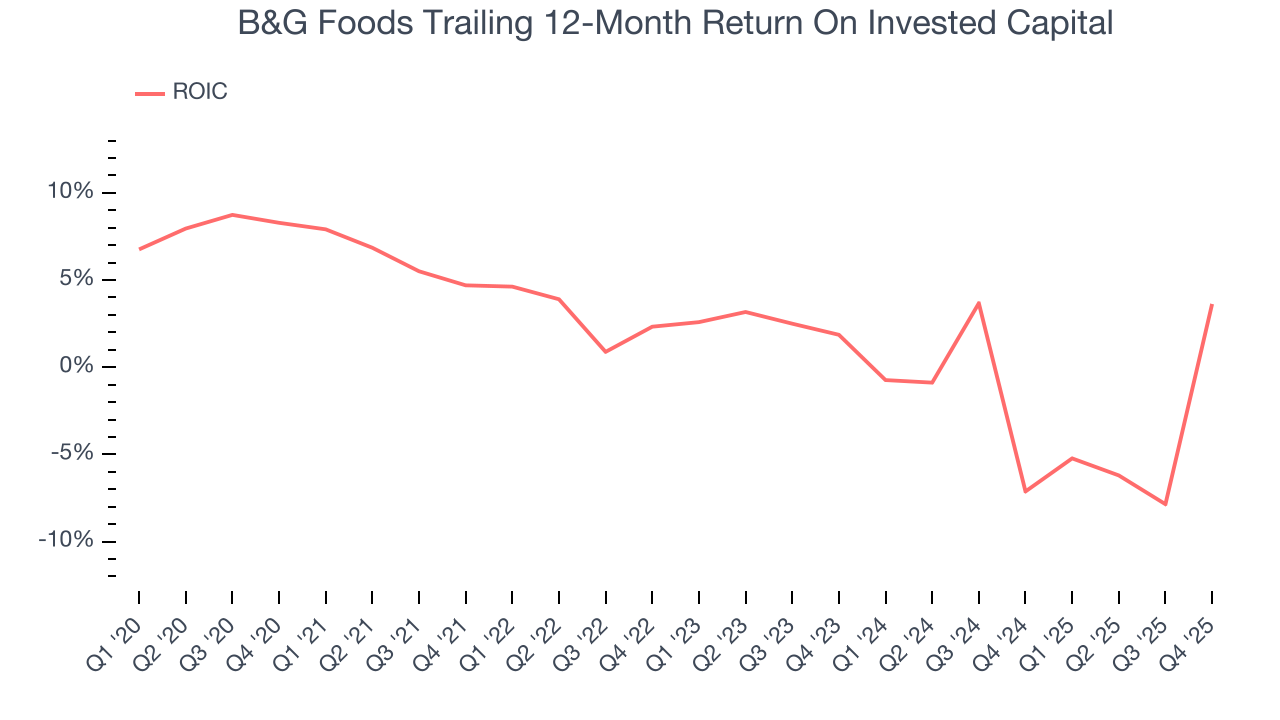

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

B&G Foods historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 1.1%, lower than the typical cost of capital (how much it costs to raise money) for consumer staples companies.

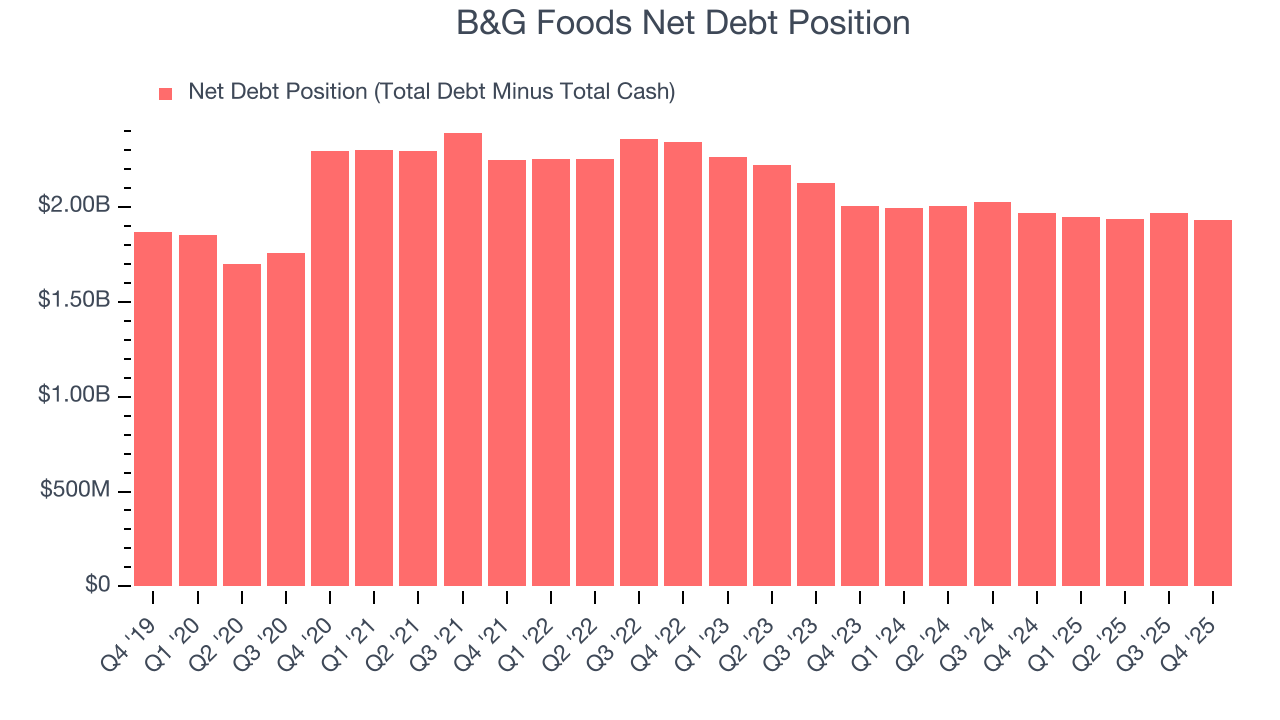

12. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

B&G Foods’s $1.98 billion of debt exceeds the $56.29 million of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $272.2 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. B&G Foods could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope B&G Foods can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

13. Key Takeaways from B&G Foods’s Q4 Results

It was encouraging to see B&G Foods beat analysts’ gross margin expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded up 11.2% to $5.63 immediately after reporting.

14. Is Now The Time To Buy B&G Foods?

Updated: March 14, 2026 at 10:54 PM EDT

Before making an investment decision, investors should account for B&G Foods’s business fundamentals and valuation in addition to what happened in the latest quarter.

We cheer for all companies serving everyday consumers, but in the case of B&G Foods, we’ll be cheering from the sidelines. To kick things off, its revenue has declined over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its expanding operating margin shows the business has become more efficient, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

B&G Foods’s P/E ratio based on the next 12 months is 9x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $5 on the company (compared to the current share price of $5.25).