Enviri (NVRI)

Enviri is in for a bumpy ride. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Enviri Will Underperform

Cooling America’s first indoor ice rink in the 19th century, Enviri (NYSE:NVRI) offers steel and waste handling services.

- Annual sales declines of 2.7% for the past two years show its products and services struggled to connect with the market during this cycle

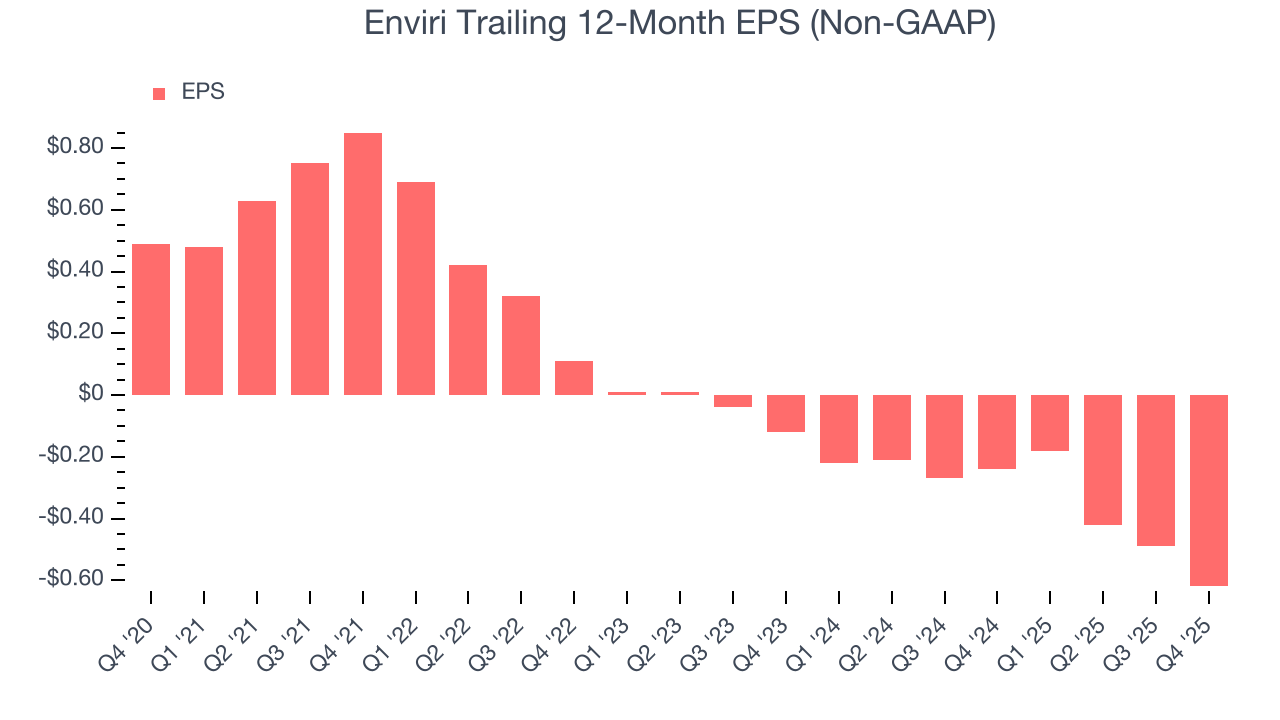

- Earnings per share have contracted by 26.7% annually over the last five years, a headwind for returns as stock prices often echo long-term EPS performance

- 5× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Enviri’s quality is lacking. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Enviri

Enviri’s stock price of $17.85 implies a valuation ratio of 14.1x forward EV-to-EBITDA. This multiple is high given its weaker fundamentals.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Enviri (NVRI) Research Report: Q4 CY2025 Update

Steel and waste handling company Enviri (NYSE:NVRI) announced better-than-expected revenue in Q4 CY2025, but sales were flat year on year at $556.4 million. Its non-GAAP loss of $0.17 per share was 25% above analysts’ consensus estimates.

Enviri (NVRI) Q4 CY2025 Highlights:

- Revenue: $556.4 million vs analyst estimates of $550.9 million (flat year on year, 1% beat)

- Adjusted EPS: -$0.17 vs analyst estimates of -$0.23 (25% beat)

- Adjusted EBITDA: $70.13 million vs analyst estimates of $65.13 million (12.6% margin, 7.7% beat)

- Operating Margin: -6%, in line with the same quarter last year

- Free Cash Flow was -$10.46 million, down from $1.8 million in the same quarter last year

- Market Capitalization: $1.54 billion

Company Overview

Cooling America’s first indoor ice rink in the 19th century, Enviri (NYSE:NVRI) offers steel and waste handling services.

Enviri, formerly known as Harsco, was established in 1853 as a car manufacturing company sparked by the growth of the U.S. railroad system. The company transitioned into the steel industry prior to World War II to forge iron and steel products, and through several acquisitions over the next few decades, propelled itself into the steel and waste handling industry. Two important deals in recent history were ALTEK in 2018 and Clean Earth in 2019, which enabled Enviri to offer metal recovery services and handling solutions for contaminated materials.

In the steel industry, Enviri provides services to recover valuable metals from slag, a leftover material from making steel. This process not only helps reduce waste but also makes steel production more efficient. Additionally, Enviri inspects, repairs, and renews tracks which is crucial for both passenger and freight trains to run smoothly without delays.

Enviri also helps industries like construction and energy with managing waste in an environmentally friendly way. It treats and recycles industrial waste, helping companies follow environmental laws and reduce impact on the planet. These services can handle many different types of waste, making it easier for companies to manage waste responsibly.

4. Waste Management

Waste management companies can possess licenses permitting them to handle hazardous materials. Furthermore, many services are performed through contracts and statutorily mandated, non-discretionary, or recurring, leading to more predictable revenue streams. However, regulation can be a headwind, rendering existing services obsolete or forcing companies to invest precious capital to comply with new, more environmentally-friendly rules. Lastly, waste management companies are at the whim of economic cycles. Interest rates, for example, can greatly impact industrial production or commercial projects that create waste and byproducts.

Competitors offering similar products include Waste Management (NYSE:WM), Clean Harbors (NYSE:CLH), and Schnitzer Steel (NASDAQ:SCHN).

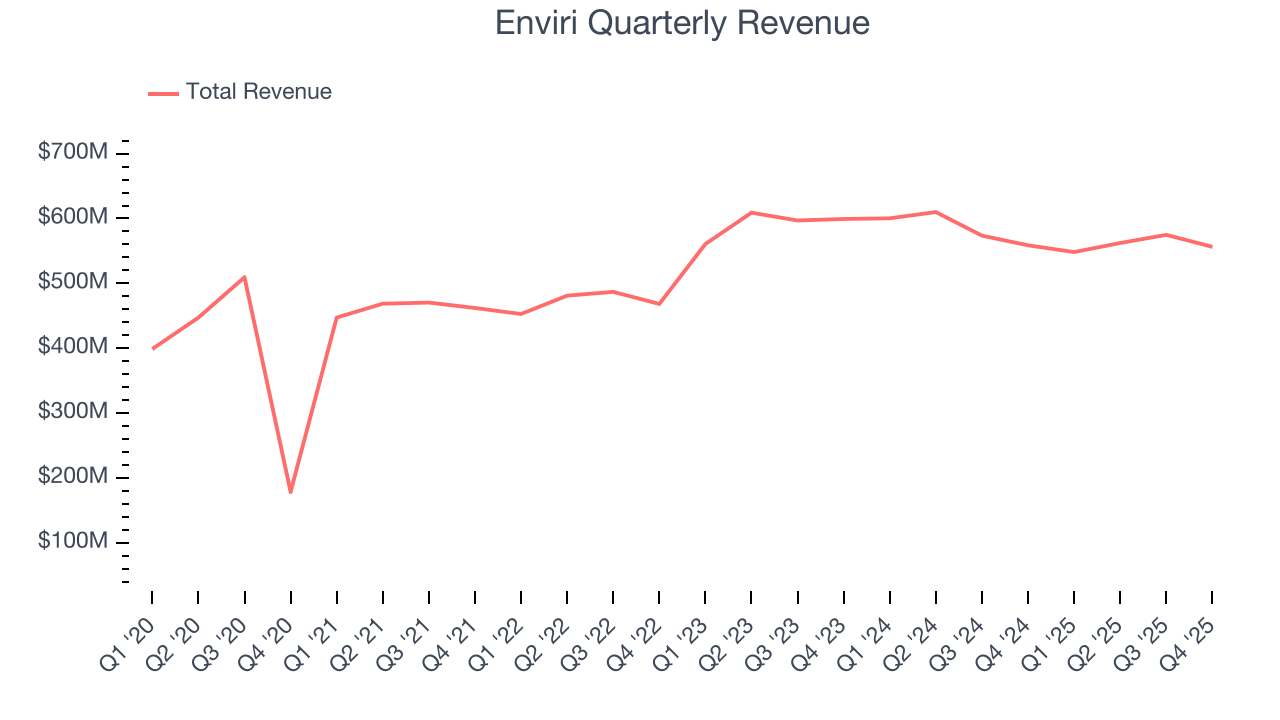

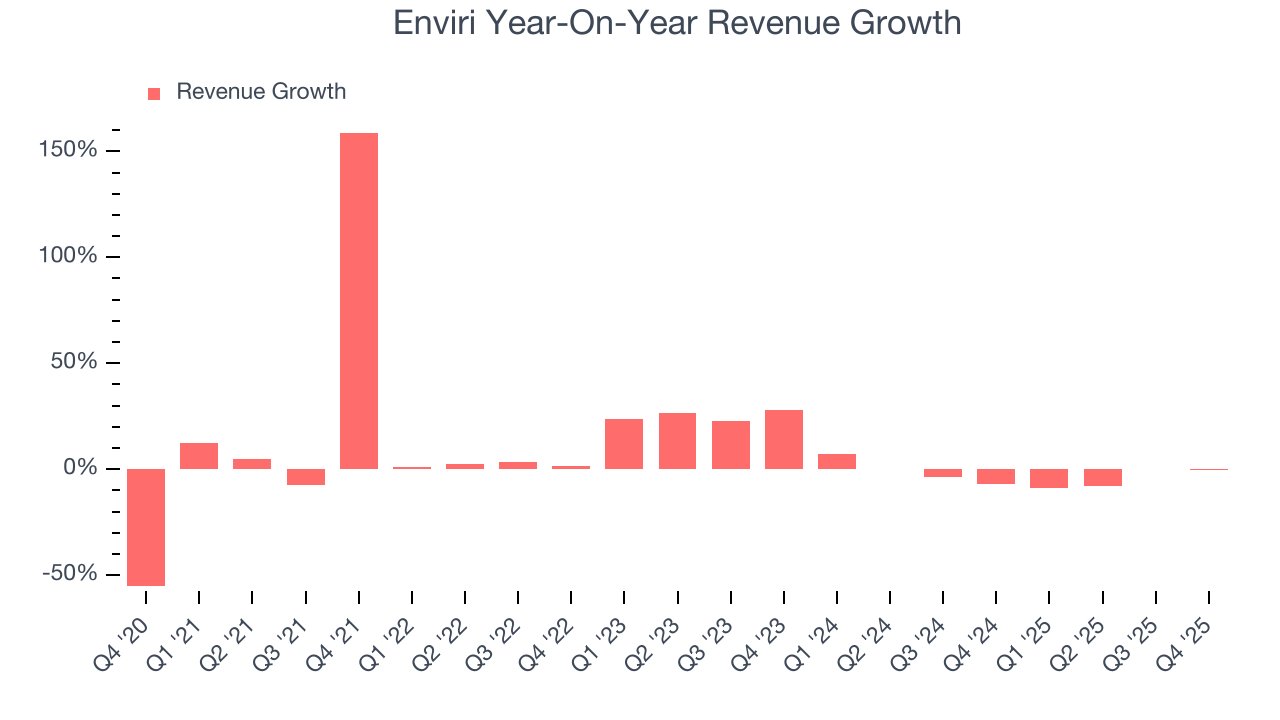

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Enviri’s sales grew at a decent 7.9% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Enviri’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2.7% over the last two years.

This quarter, Enviri’s $556.4 million of revenue was flat year on year but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

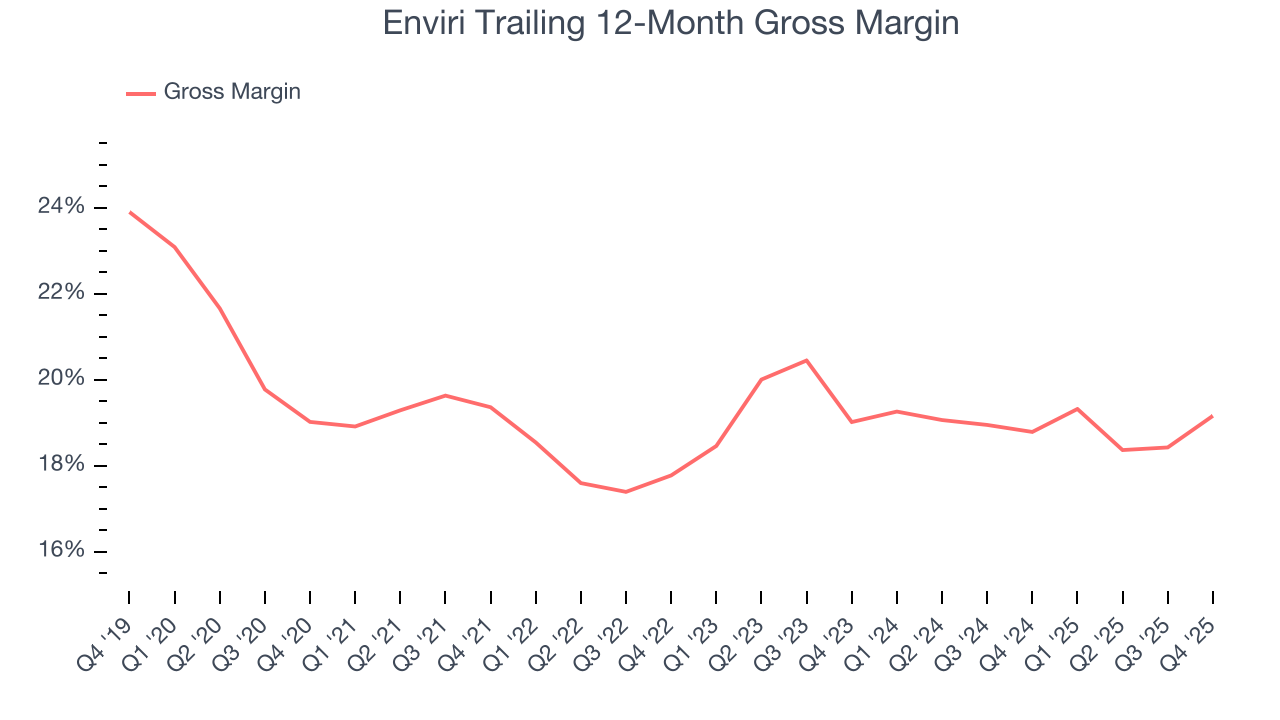

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Enviri has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 18.8% gross margin over the last five years. That means Enviri paid its suppliers a lot of money ($81.17 for every $100 in revenue) to run its business.

Enviri produced a 15.3% gross profit margin in Q4 , marking a 2.9 percentage point increase from 12.4% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

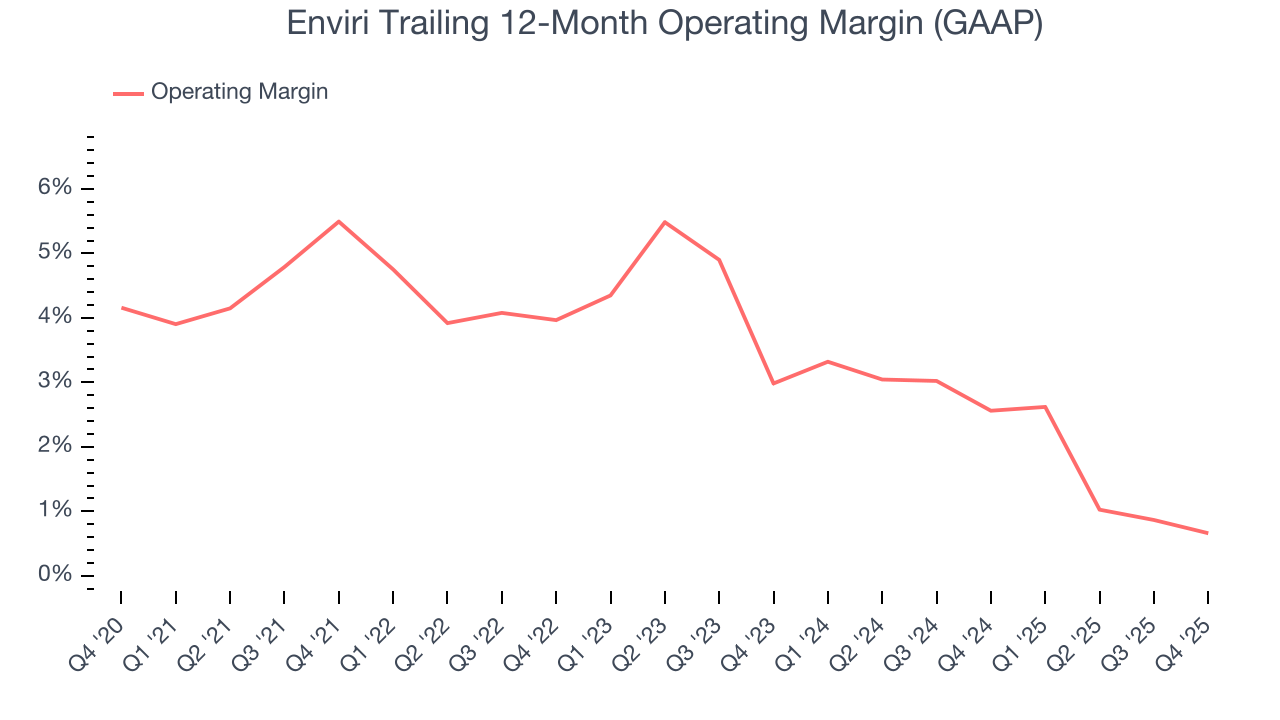

7. Operating Margin

Enviri was profitable over the last five years but held back by its large cost base. Its average operating margin of 3% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Enviri’s operating margin decreased by 4.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Enviri’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Enviri generated an operating margin profit margin of negative 6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Enviri, its EPS declined by 26.7% annually over the last five years while its revenue grew by 7.9%. This tells us the company became less profitable on a per-share basis as it expanded.

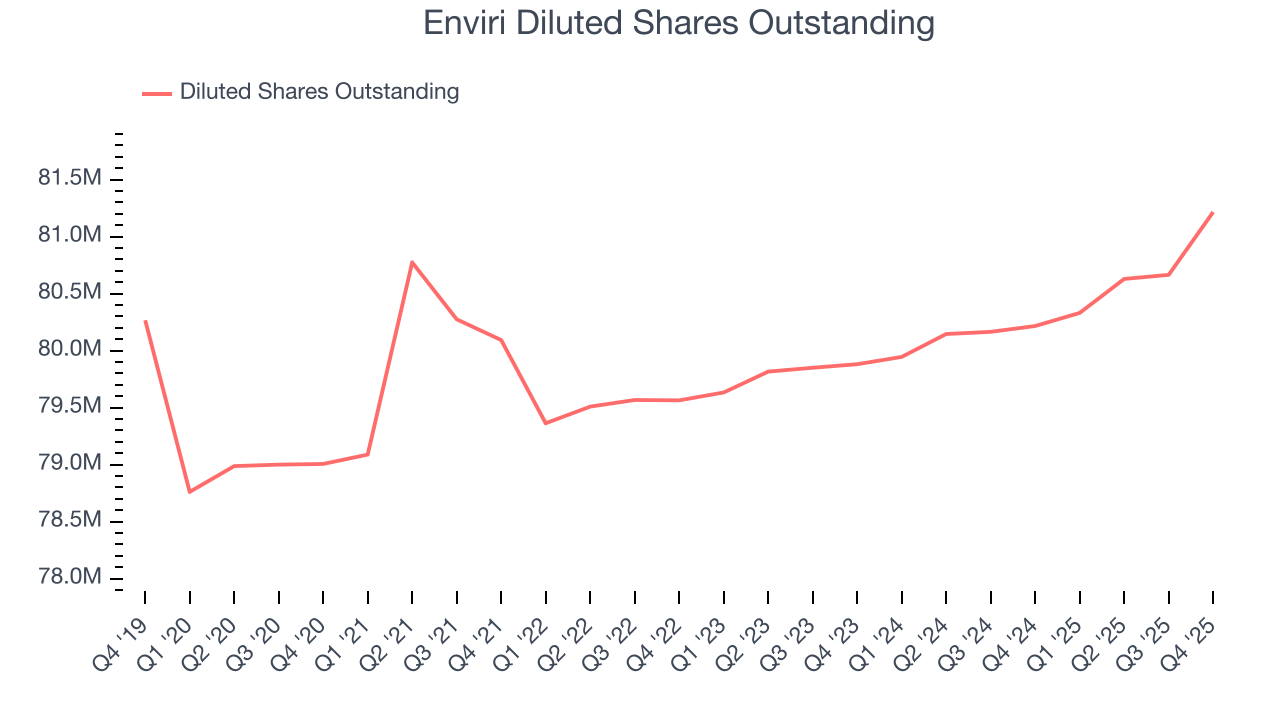

We can take a deeper look into Enviri’s earnings to better understand the drivers of its performance. As we mentioned earlier, Enviri’s operating margin was flat this quarter but declined by 4.8 percentage points over the last five years. Its share count also grew by 2.8%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Enviri, its two-year annual EPS declines of 127% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Enviri reported adjusted EPS of negative $0.17, down from negative $0.04 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Enviri to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.62 will advance to negative $0.29.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

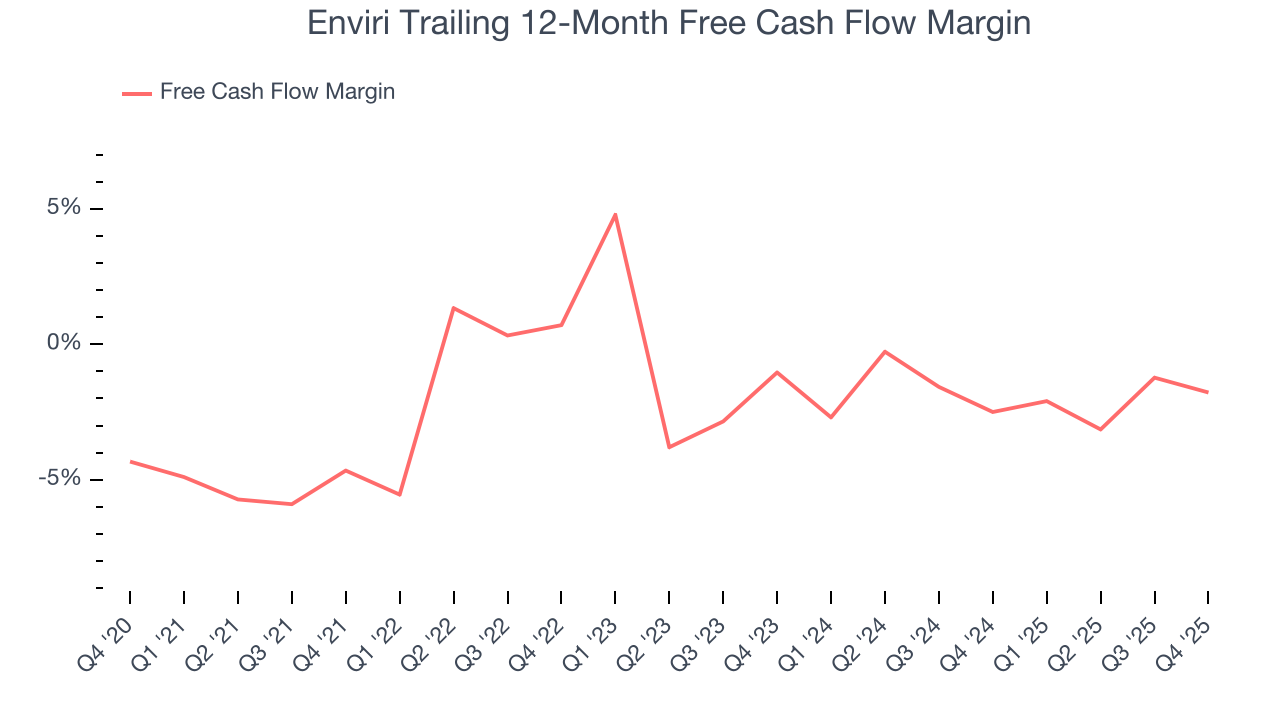

Enviri’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.8%, meaning it lit $1.83 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Enviri’s margin expanded by 2.9 percentage points during that time. We have no doubt shareholders would like to continue seeing its cash conversion rise.

Enviri burned through $10.46 million of cash in Q4, equivalent to a negative 1.9% margin. The company’s cash burn increased meaningfully year on year while its cash conversion fell 2.2 percentage points. This relationship shows Enviri’s management team spent more cash this quarter but was less efficient at generating sales with that cash.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

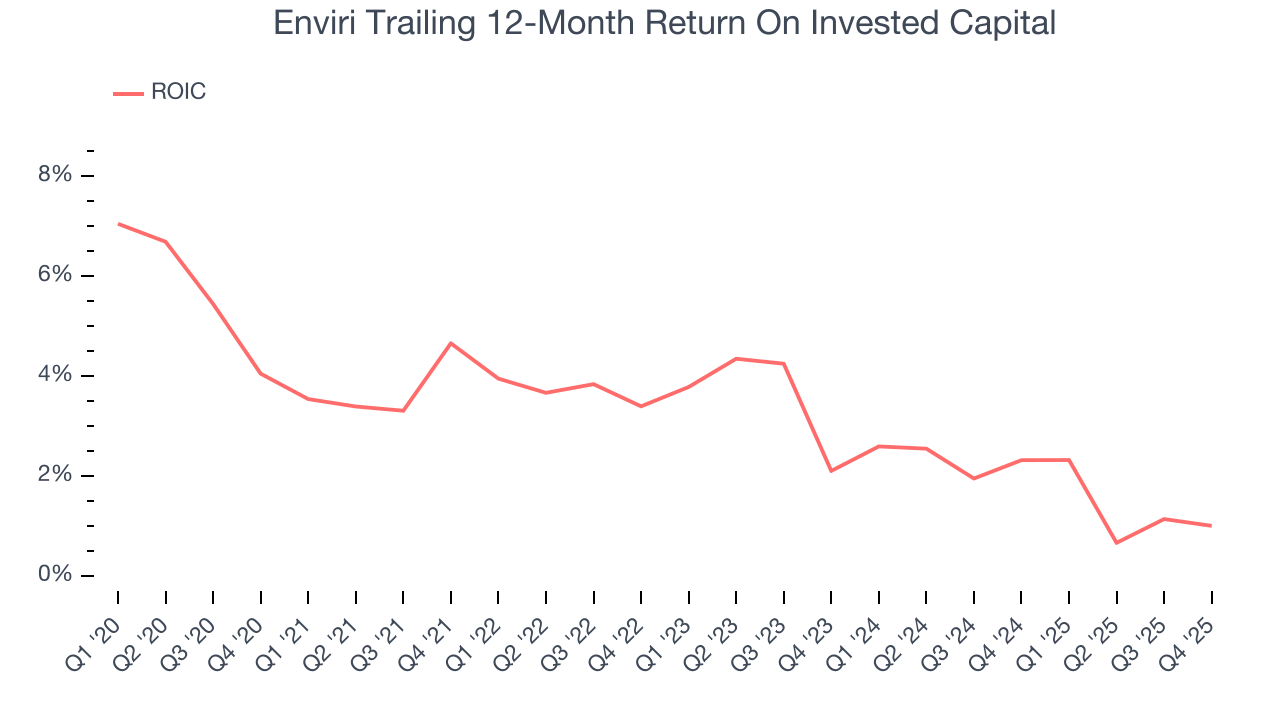

Enviri historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.7%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Enviri’s ROIC averaged 2.4 percentage point decreases each year. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

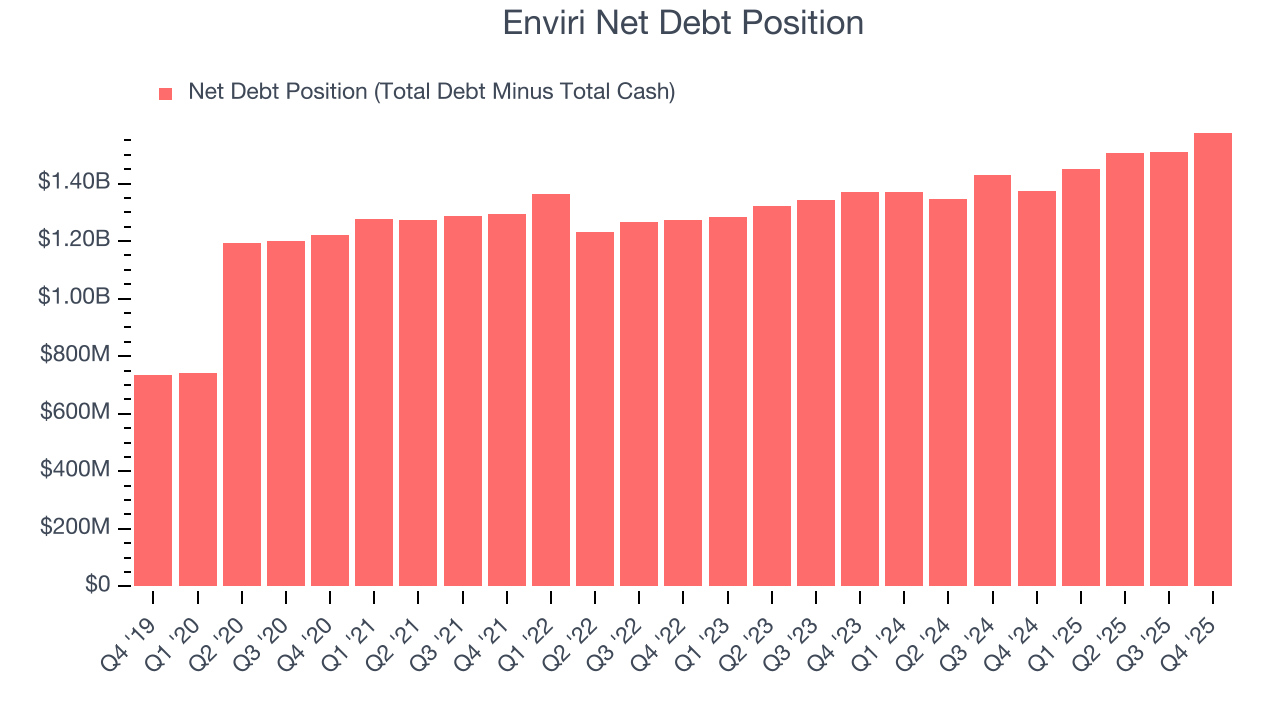

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Enviri’s $1.7 billion of debt exceeds the $125.3 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $276.1 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Enviri could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Enviri can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Enviri’s Q4 Results

It was good to see Enviri beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $19.11 immediately following the results.

13. Is Now The Time To Buy Enviri?

Updated: March 13, 2026 at 11:46 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Enviri.

We see the value of companies helping their customers, but in the case of Enviri, we’re out. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s rising cash profitability gives it more optionality, the downside is its projected EPS for the next year is lacking.

Enviri’s EV-to-EBITDA ratio based on the next 12 months is 14.1x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $21.67 on the company (compared to the current share price of $17.85).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.