Pure Storage (PSTG)

Pure Storage is in a league of its own. Its fusion of growth, outstanding profitability, and encouraging prospects makes it a beloved asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like Pure Storage

Founded in 2009 as a pioneer in enterprise all-flash storage technology, Pure Storage (NYSE:PSTG) provides all-flash data storage hardware and software that helps organizations manage their data more efficiently across on-premises and cloud environments.

- Impressive 16.8% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 61.7% outpaced its revenue gains

- Exciting sales outlook for the upcoming 12 months calls for 19.5% growth, an acceleration from its two-year trend

We expect great things from Pure Storage. The price looks reasonable relative to its quality, and we believe now is a favorable time to buy.

Why Is Now The Time To Buy Pure Storage?

Pure Storage is trading at $61.27 per share, or 26.4x forward P/E. Many business services names may carry a lower valuation multiple, but Pure Storage’s price is fair given its business quality.

Our analysis and backtests consistently tell us that buying high-quality companies and holding them for many years leads to market outperformance. Over the long term, entry price doesn’t matter nearly as much as business fundamentals.

3. Pure Storage (PSTG) Research Report: Q4 CY2025 Update

Data storage solutions provider Pure Storage (NYSE:PSTG) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 20.4% year on year to $1.06 billion. On top of that, next quarter’s revenue guidance ($1 billion at the midpoint) was surprisingly good and 8.1% above what analysts were expecting. Its non-GAAP profit of $0.69 per share was 7% above analysts’ consensus estimates.

Pure Storage (PSTG) Q4 CY2025 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $1.03 billion (20.4% year-on-year growth, 2.5% beat)

- Adjusted EPS: $0.69 vs analyst estimates of $0.64 (7% beat)

- Revenue Guidance for Q1 CY2026 is $1 billion at the midpoint, above analyst estimates of $925.1 million

- Operating Margin: 8.2%, up from 4.8% in the same quarter last year

- Free Cash Flow Margin: 19%, up from 17.3% in the same quarter last year

- Market Capitalization: $22.36 billion

Company Overview

Founded in 2009 as a pioneer in enterprise all-flash storage technology, Pure Storage (NYSE:PSTG) provides all-flash data storage hardware and software that helps organizations manage their data more efficiently across on-premises and cloud environments.

Pure Storage's business revolves around its integrated data storage platform that combines specialized hardware systems with proprietary software. The company's product lineup includes FlashArray for block storage needs and FlashBlade for unstructured data workloads, both powered by its Purity operating software and DirectFlash hardware technology that's designed to work directly with NAND flash memory chips rather than traditional solid-state drives (SSDs).

What sets Pure Storage apart is its "Evergreen" architecture, which allows customers to upgrade their storage systems without disruptive migrations or complete replacements. This approach enables continuous improvement through non-disruptive hardware and software updates, extending the useful life of storage investments.

The company serves organizations across various industries that need to store and process large amounts of data efficiently. For example, a hospital might use Pure Storage's FlashArray to run its electronic health record system and medical imaging applications, benefiting from faster data access and reduced power consumption compared to traditional disk-based storage.

Pure Storage has evolved its business model to include subscription-based offerings. Its Evergreen//One service provides storage as a service with consumption-based pricing, while Evergreen//Flex offers a hybrid approach with hardware ownership but flexible capacity scaling. The company also offers Portworx, a platform for managing data in Kubernetes environments, addressing the needs of organizations developing cloud-native applications.

Revenue comes from both hardware sales and recurring subscription services. Pure Storage has expanded its focus to include artificial intelligence workloads, which require high-performance storage to process massive datasets efficiently. The company's global operations serve over 12,500 customers, including approximately 60% of Fortune 500 companies.

4. Hardware & Infrastructure

The Hardware & Infrastructure sector will be buoyed by demand related to AI adoption, cloud computing expansion, and the need for more efficient data storage and processing solutions. Companies with tech offerings such as servers, switches, and storage solutions are well-positioned in our new hybrid working and IT world. On the other hand, headwinds include ongoing supply chain disruptions, rising component costs, and intensifying competition from cloud-native and hyperscale providers reducing reliance on traditional hardware. Additionally, regulatory scrutiny over data sovereignty, cybersecurity standards, and environmental sustainability in hardware manufacturing could increase compliance costs.

Pure Storage competes primarily with legacy data storage vendors including Dell EMC, NetApp, Hitachi Vantara, IBM, and HPE. The company also faces competition from cloud storage services offered by major public cloud providers like AWS, Microsoft Azure, and Google Cloud.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

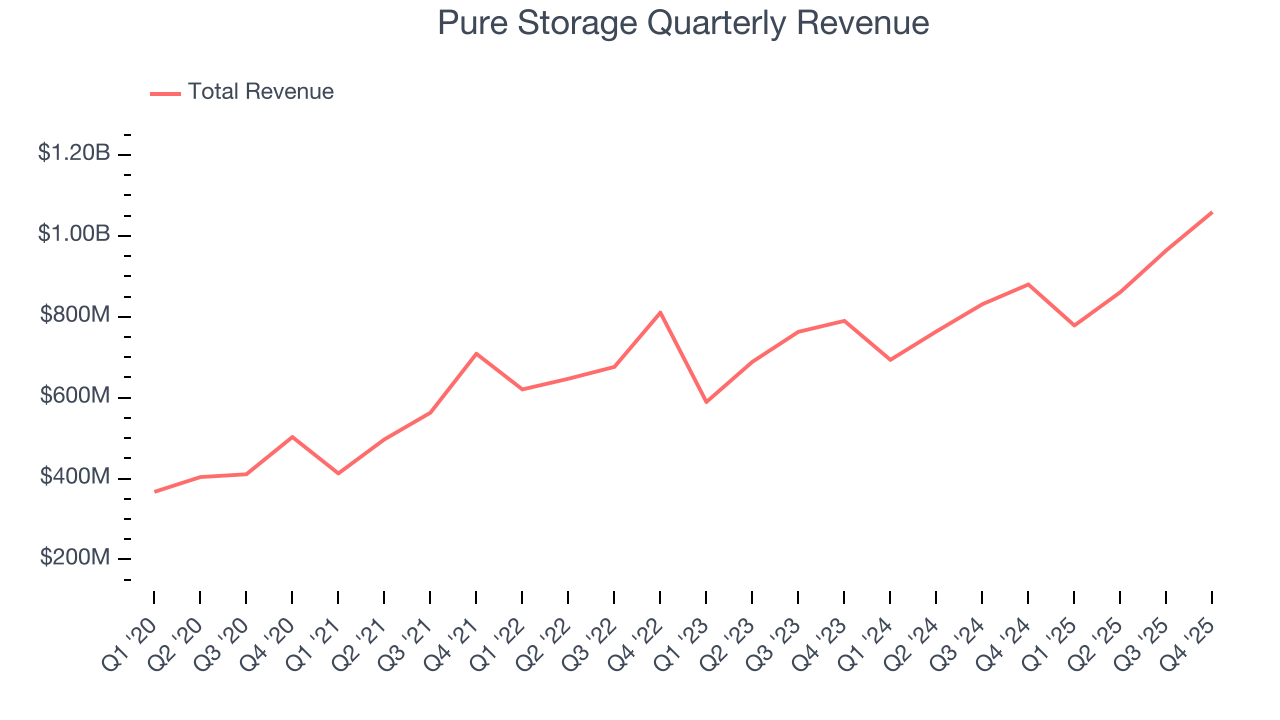

With $3.66 billion in revenue over the past 12 months, Pure Storage is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

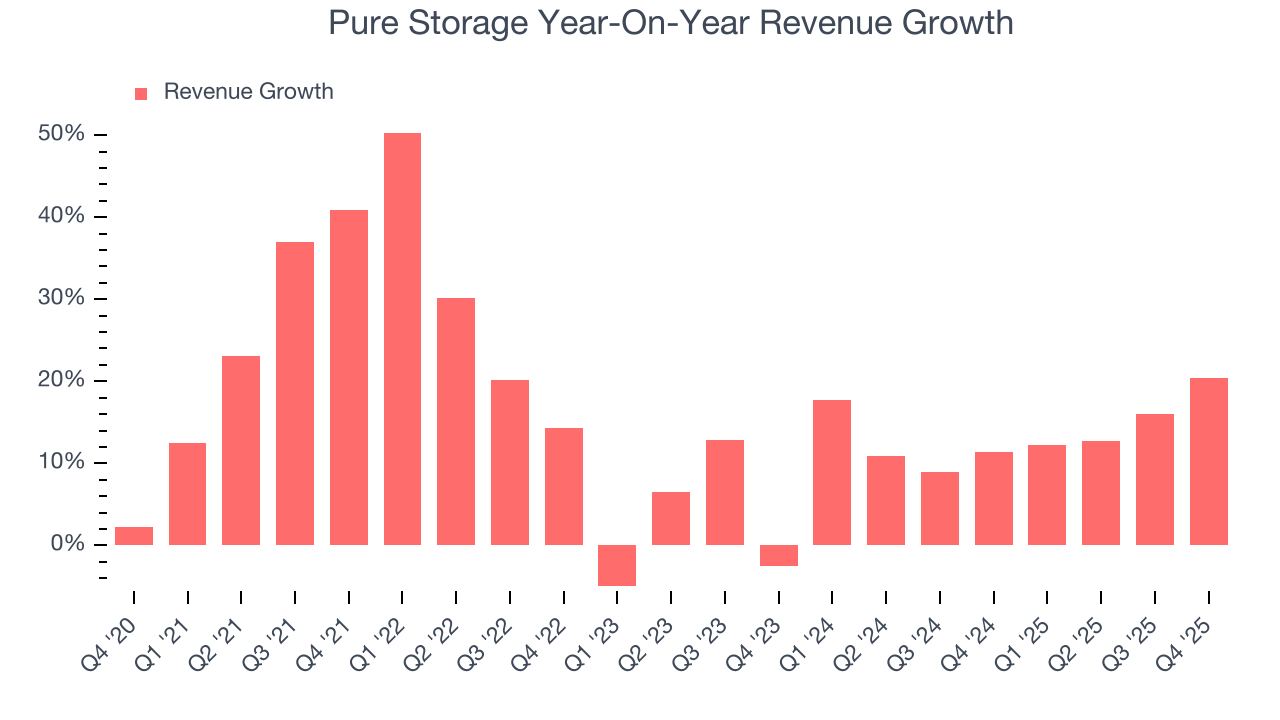

As you can see below, Pure Storage’s sales grew at an incredible 16.8% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Pure Storage’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Pure Storage’s annualized revenue growth of 13.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Pure Storage reported robust year-on-year revenue growth of 20.4%, and its $1.06 billion of revenue topped Wall Street estimates by 2.5%. Company management is currently guiding for a 28.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16.4% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will fuel better top-line performance.

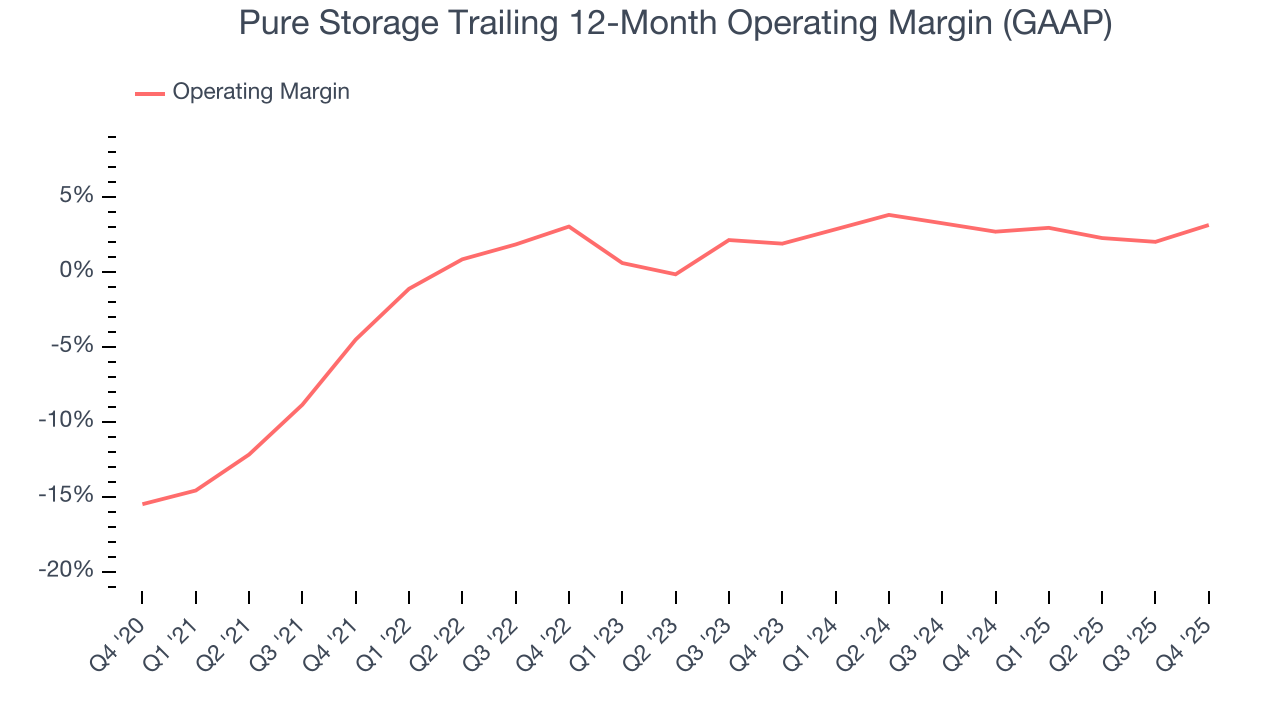

6. Operating Margin

Pure Storage was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.6% was weak for a business services business.

On the plus side, Pure Storage’s operating margin rose by 7.6 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, Pure Storage generated an operating margin profit margin of 8.2%, up 3.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

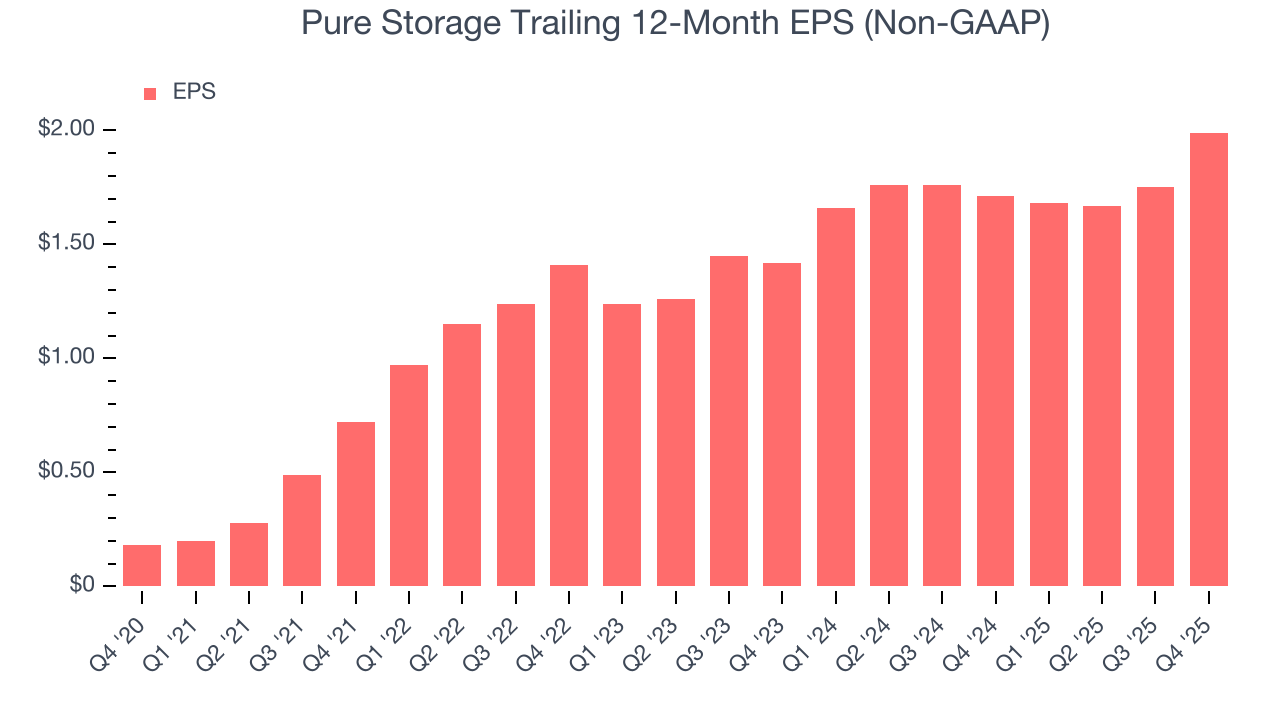

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Pure Storage’s EPS grew at an astounding 61.7% compounded annual growth rate over the last five years, higher than its 16.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Pure Storage’s earnings can give us a better understanding of its performance. As we mentioned earlier, Pure Storage’s operating margin expanded by 7.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Pure Storage, its two-year annual EPS growth of 18.4% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Pure Storage reported adjusted EPS of $0.69, up from $0.45 in the same quarter last year. This print beat analysts’ estimates by 7%. Over the next 12 months, Wall Street expects Pure Storage’s full-year EPS of $1.99 to grow 12.4%.

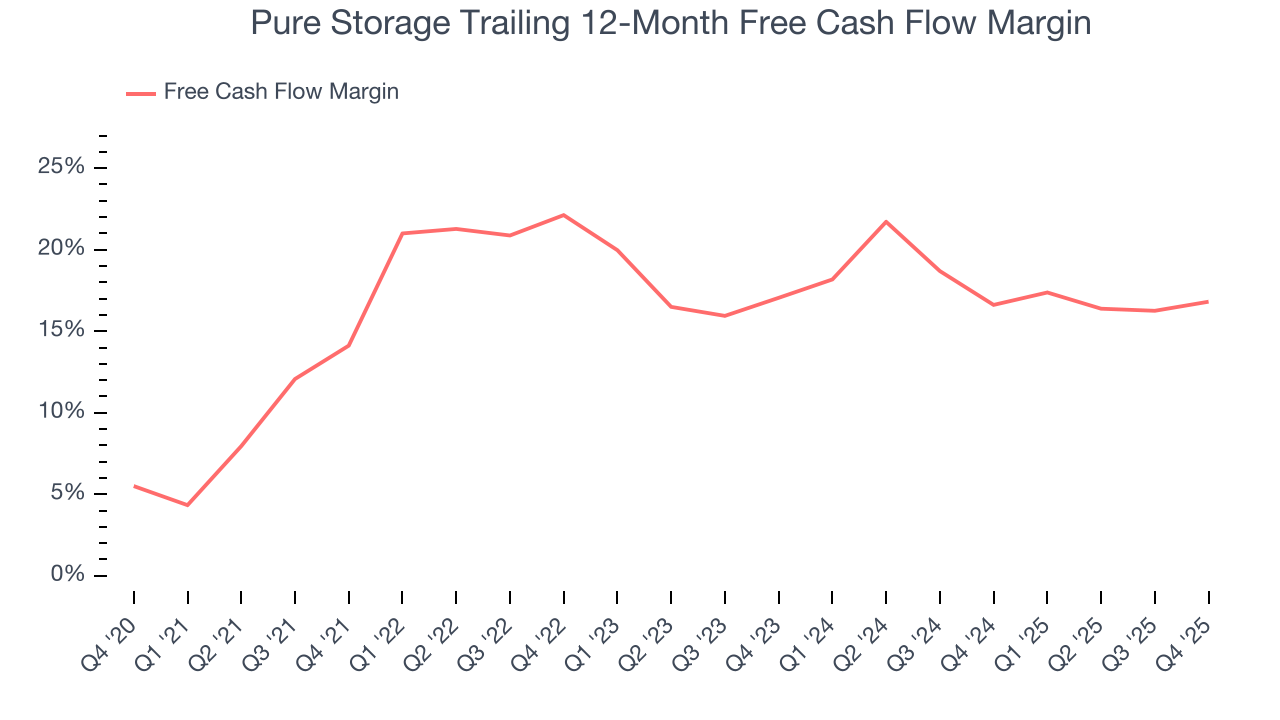

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Pure Storage has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging 17.4% over the last five years. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Pure Storage’s margin expanded by 2.7 percentage points during that time. This is encouraging because it gives the company more optionality.

Pure Storage’s free cash flow clocked in at $201.4 million in Q4, equivalent to a 19% margin. This result was good as its margin was 1.8 percentage points higher than in the same quarter last year, building on its favorable historical trend.

9. Balance Sheet Assessment

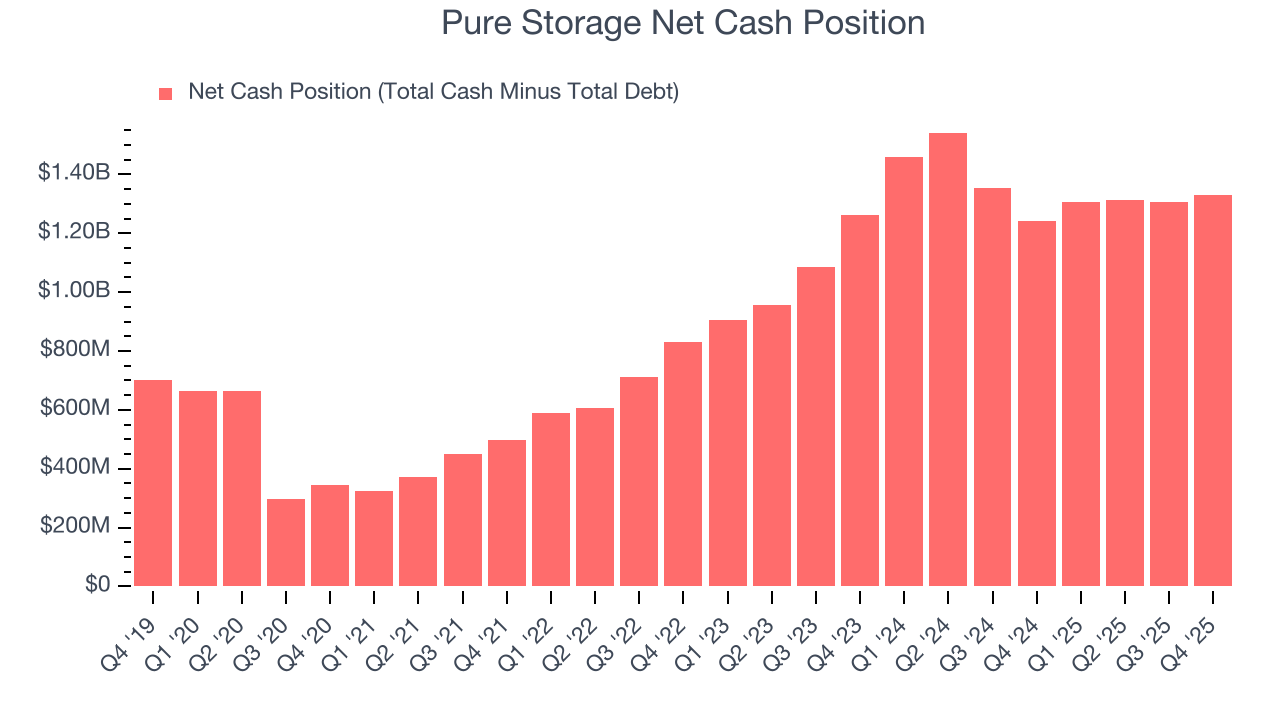

Companies with more cash than debt have lower bankruptcy risk.

Pure Storage is a profitable, well-capitalized company with $1.55 billion of cash and $216.1 million of debt on its balance sheet. This $1.33 billion net cash position is 5.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

10. Key Takeaways from Pure Storage’s Q4 Results

We were impressed by Pure Storage’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 4.1% to $76.87 immediately following the results.

11. Is Now The Time To Buy Pure Storage?

Updated: March 16, 2026 at 12:24 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Pure Storage, you should also grasp the company’s longer-term business quality and valuation.

There are multiple reasons why we think Pure Storage is an elite business services company. For starters, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. On top of that, its ARR growth has been marvelous, and its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Pure Storage’s P/E ratio based on the next 12 months is 26.4x. Looking across the spectrum of business services businesses, Pure Storage’s fundamentals clearly illustrate it’s a special business. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $91.21 on the company (compared to the current share price of $61.27), implying they see 48.9% upside in buying Pure Storage in the short term.