Wolverine Worldwide (WWW)

We wouldn’t buy Wolverine Worldwide. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Wolverine Worldwide Will Underperform

Founded in 1883, Wolverine Worldwide (NYSE:WWW) is a global footwear company with a diverse portfolio of brands including Merrell, Hush Puppies, and Saucony.

- Products and services fail to spark excitement with consumers, as seen in its flat sales over the last five years

- Earnings per share lagged its peers over the last five years as they only grew by 7.8% annually

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

Wolverine Worldwide doesn’t meet our quality criteria. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Wolverine Worldwide

Wolverine Worldwide is trading at $15.89 per share, or 11.4x forward P/E. Wolverine Worldwide’s valuation may seem like a bargain, especially when stacked up against other consumer discretionary companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Wolverine Worldwide (WWW) Research Report: Q4 CY2025 Update

Footwear conglomerate Wolverine Worldwide (NYSE:WWW) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 4.6% year on year to $517.5 million. The company’s full-year revenue guidance of $1.97 billion at the midpoint came in 0.6% above analysts’ estimates. Its non-GAAP profit of $0.45 per share was 3.1% above analysts’ consensus estimates.

Wolverine Worldwide (WWW) Q4 CY2025 Highlights:

- Revenue: $517.5 million vs analyst estimates of $512.9 million (4.6% year-on-year growth, 0.9% beat)

- Adjusted EPS: $0.45 vs analyst estimates of $0.44 (3.1% beat)

- Adjusted EBITDA: $54.5 million vs analyst estimates of $61.65 million (10.5% margin, 11.6% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.43 at the midpoint, beating analyst estimates by 5.1%

- Operating Margin: 9.4%, up from 8% in the same quarter last year

- Free Cash Flow Margin: 28.1%, up from 15% in the same quarter last year

- Market Capitalization: $1.48 billion

Company Overview

Founded in 1883, Wolverine Worldwide (NYSE:WWW) is a global footwear company with a diverse portfolio of brands including Merrell, Hush Puppies, and Saucony.

Each brand in Wolverine Worldwide's lineup has its unique identity and market segment, ranging from outdoor and work footwear to fashion and casual wear. For example, Merrell is known for its high-performance outdoor footwear, appealing to adventure enthusiasts, while Hush Puppies offers relaxed, casual shoes that resonate with a lifestyle-oriented consumer base.

To improve its products, the company attempts to develop new materials and technologies to enhance comfort, durability, and performance. Some of Wolverine Worldwide's designs include Contour Welt and Durashocks, which are geared toward work footwear.

The company's global reach is supported by its extensive distribution network. Wolverine products are available in more than 200 countries and territories through a combination of wholesale, retail, e-commerce, and licensing channels. This ensures that Wolverine's brands are accessible to a vast consumer base worldwide.

4. Consumer Discretionary - Footwear

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Footwear companies design, manufacture, and market shoes across athletic, casual, and luxury segments. Tailwinds include the global athleisure trend, growing health and fitness awareness driving sneaker demand, and expanding direct-to-consumer digital channels that improve brand control and margins. However, headwinds are notable: the industry faces intense competition and brand-switching behavior, heavy marketing spend requirements to maintain relevance, and exposure to volatile raw material and freight costs. Tariff risk from concentrated overseas manufacturing, primarily in Asia, remains a persistent concern. Additionally, inventory management is challenging given seasonal and trend-driven demand, with markdowns eroding profitability when styles miss consumer expectations.

Wolverine Worldwide's primary competitors include Nike (NYSE:NKE), Adidas (ETR:ADS), VF Corp (NYSE:VFC), who owns The North Face and Vans, Deckers Outdoor (NYSE:DECK), who owns UGG and Hoka, and Columbia Sportswear (NASDAQ:COLM).

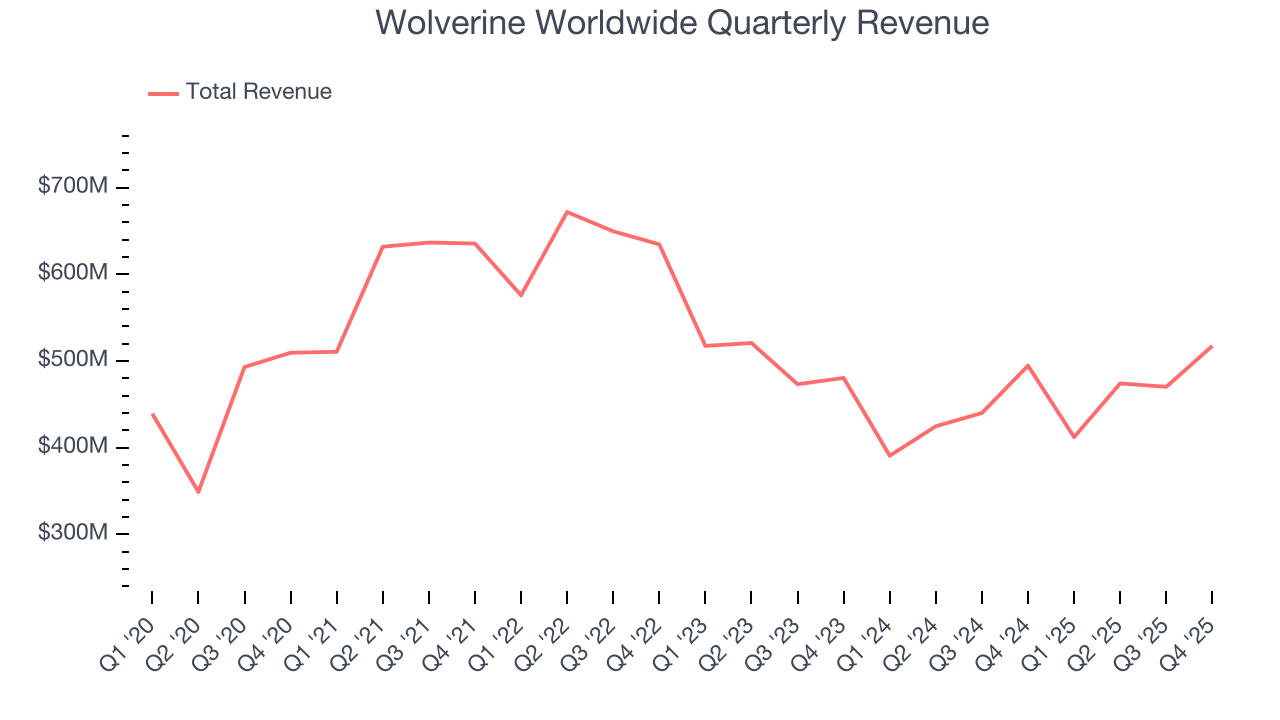

5. Revenue Growth

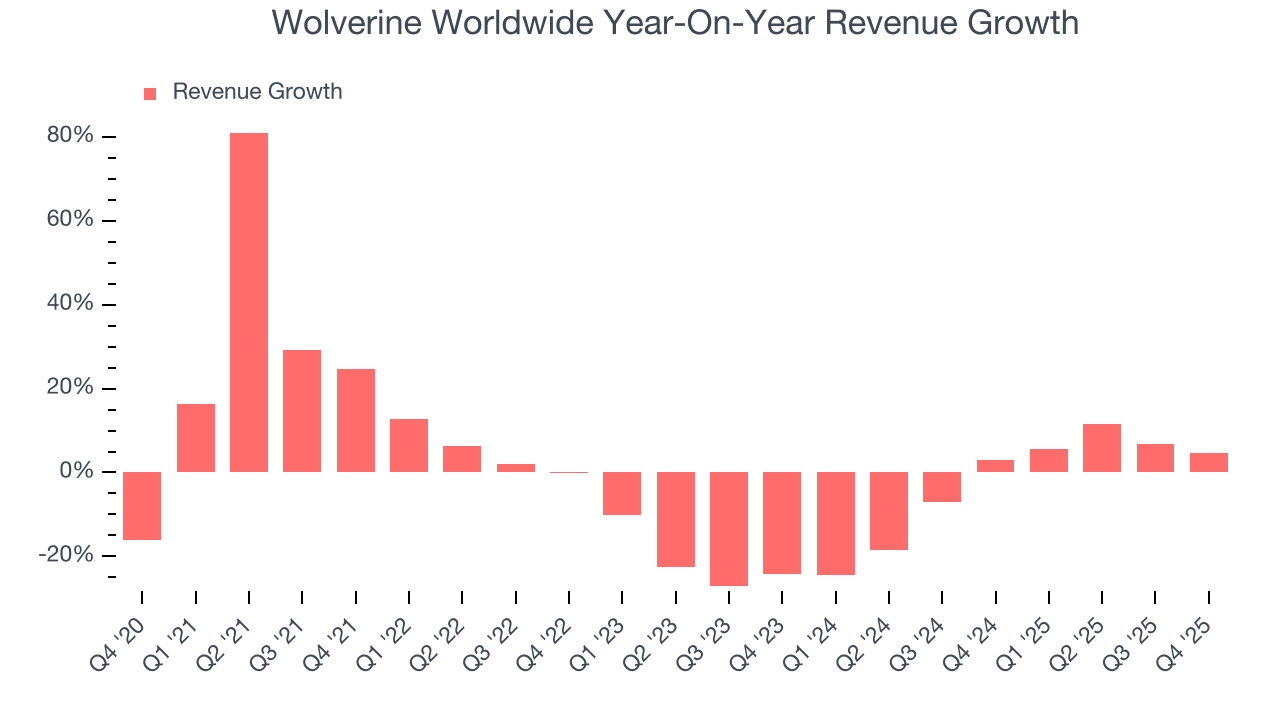

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Wolverine Worldwide struggled to consistently increase demand as its $1.87 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Wolverine Worldwide’s recent performance shows its demand remained suppressed as its revenue has declined by 3% annually over the last two years.

This quarter, Wolverine Worldwide reported modest year-on-year revenue growth of 4.6% but beat Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

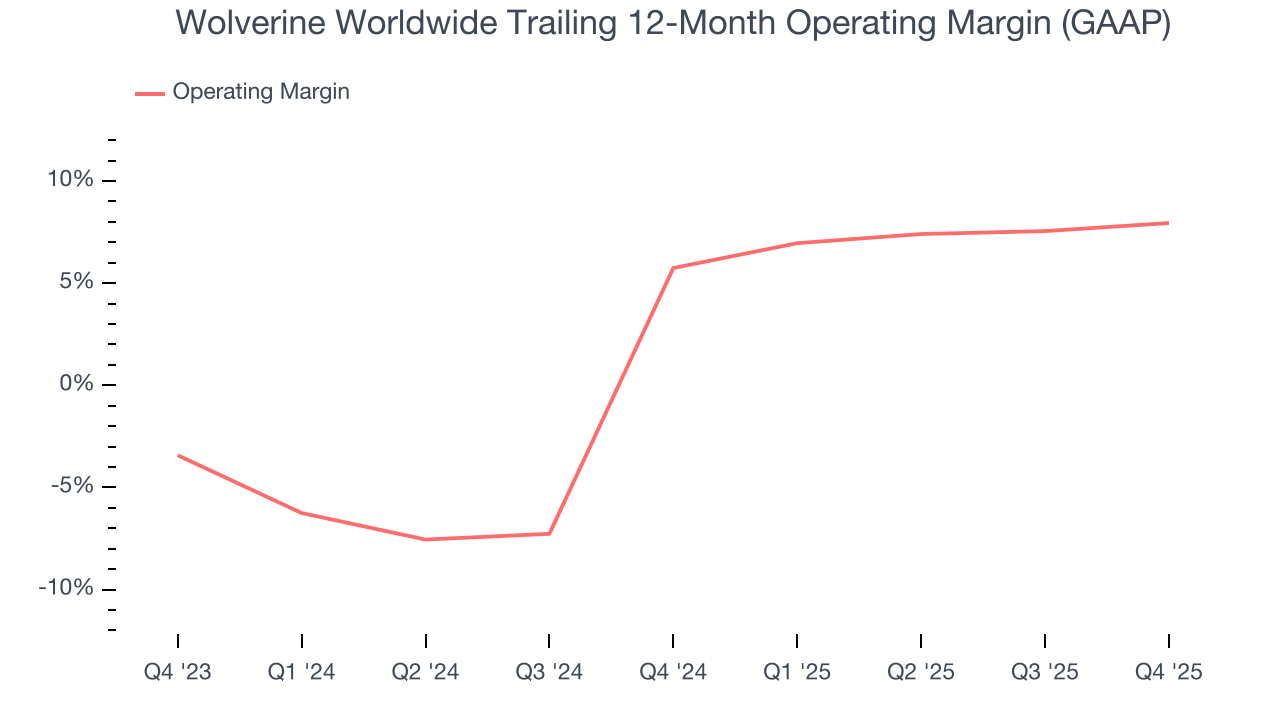

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Wolverine Worldwide’s operating margin has risen over the last 12 months and averaged 6.9% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, Wolverine Worldwide generated an operating margin profit margin of 9.4%, up 1.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

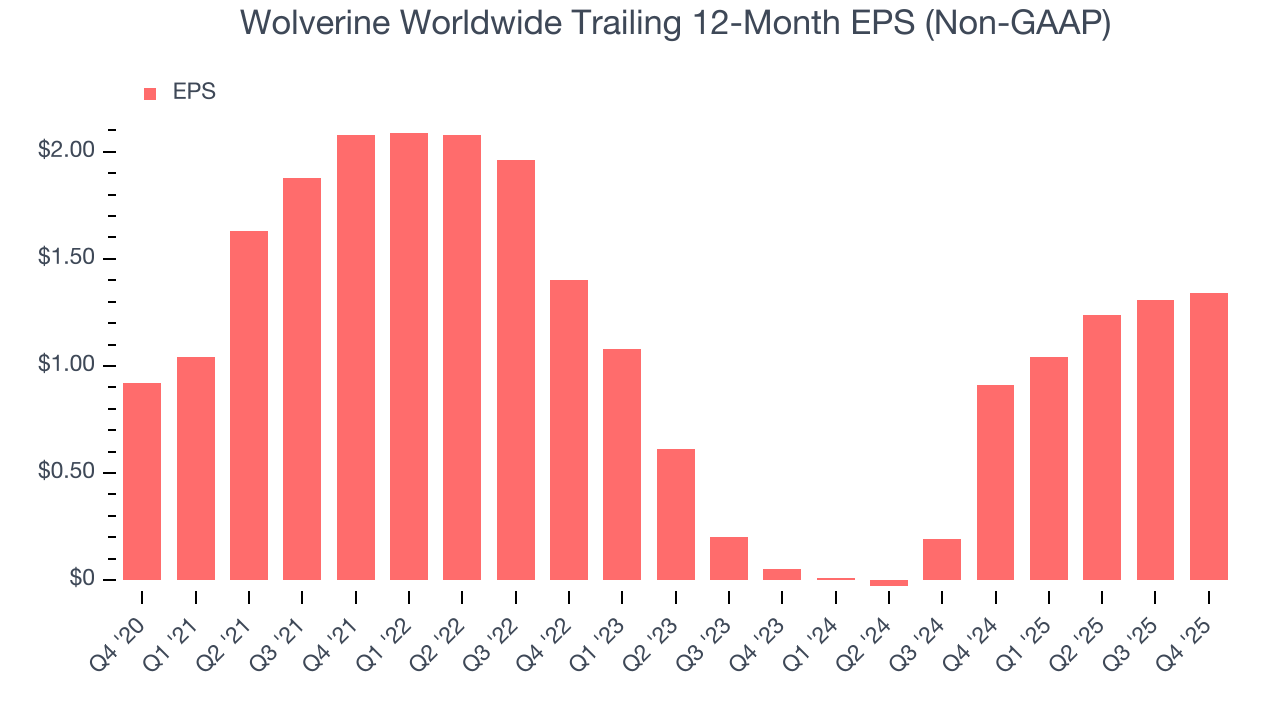

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Wolverine Worldwide’s EPS grew at a weak 7.8% compounded annual growth rate over the last five years. On the bright side, this performance was better than its flat revenue and tells us management responded to softer demand by adapting its cost structure.

In Q4, Wolverine Worldwide reported adjusted EPS of $0.45, up from $0.42 in the same quarter last year. This print beat analysts’ estimates by 3.1%. Over the next 12 months, Wall Street expects Wolverine Worldwide’s full-year EPS of $1.34 to stay about the same.

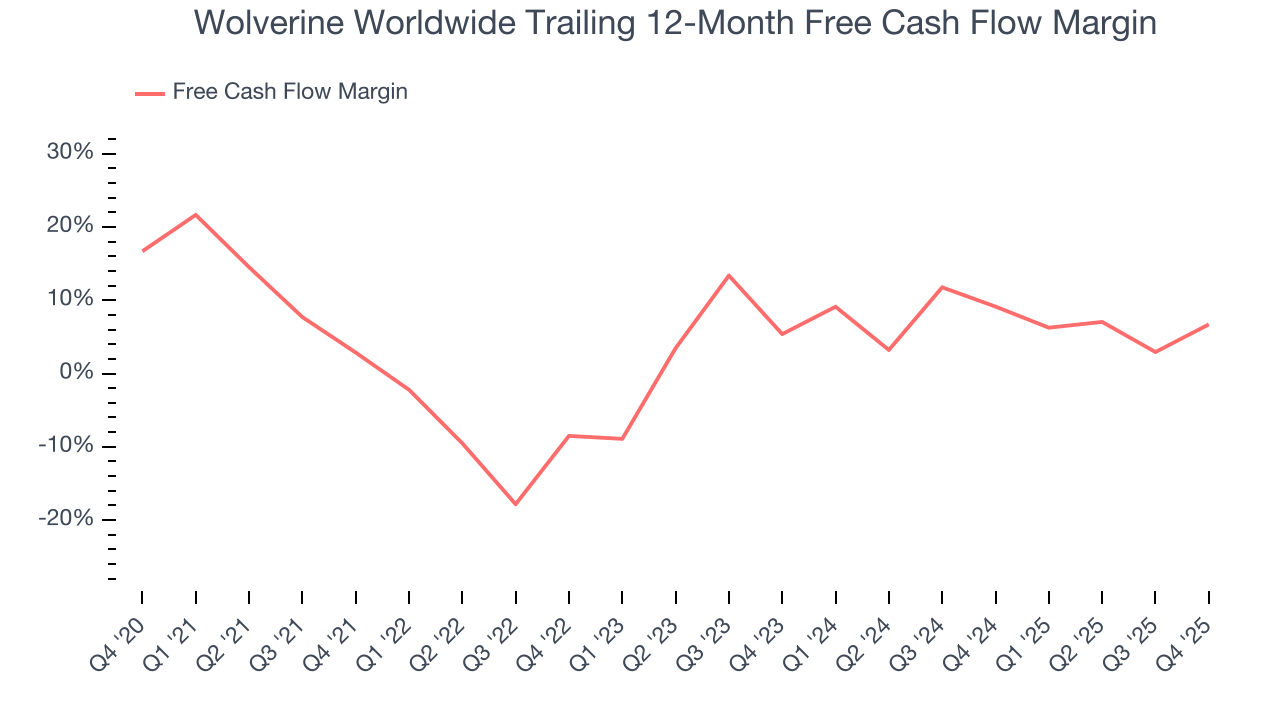

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Wolverine Worldwide has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.9%, lousy for a consumer discretionary business.

Wolverine Worldwide’s free cash flow clocked in at $145.6 million in Q4, equivalent to a 28.1% margin. This result was good as its margin was 13.1 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

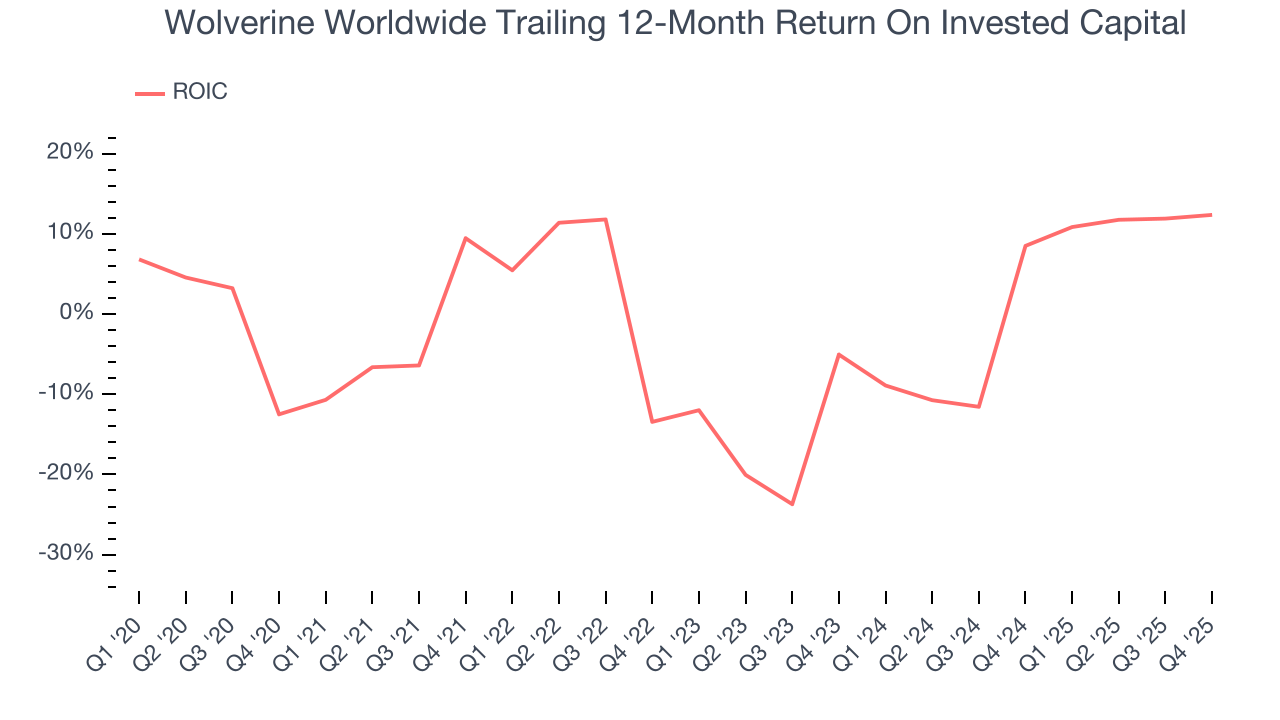

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Wolverine Worldwide historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.4%, lower than the typical cost of capital (how much it costs to raise money) for consumer discretionary companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Wolverine Worldwide’s ROIC has increased significantly. This is a good sign, and we hope the company can continue improving.

10. Balance Sheet Assessment

Wolverine Worldwide reported $206.3 million of cash and $762 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $185.8 million of EBITDA over the last 12 months, we view Wolverine Worldwide’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $16.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Wolverine Worldwide’s Q4 Results

It was great to see Wolverine Worldwide’s full-year EPS guidance top analysts’ expectations. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its EBITDA missed. Overall, this print had some key positives. The stock traded up 6.5% to $19.21 immediately following the results.

12. Is Now The Time To Buy Wolverine Worldwide?

Updated: March 22, 2026 at 10:54 PM EDT

Before making an investment decision, investors should account for Wolverine Worldwide’s business fundamentals and valuation in addition to what happened in the latest quarter.

Wolverine Worldwide falls short of our quality standards. On top of that, Wolverine Worldwide’s Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion, and its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders.

Wolverine Worldwide’s P/E ratio based on the next 12 months is 11.4x. This valuation multiple is fair, but we don’t have much confidence in the company. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $23.44 on the company (compared to the current share price of $15.89).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.