Amneal (AMRX)

We aren’t fans of Amneal. Its weak returns on capital indicate management was inefficient with its resources and missed opportunities.― StockStory Analyst Team

1. News

2. Summary

Why Amneal Is Not Exciting

Founded in 2002 and growing into one of America's largest generic drug producers, Amneal Pharmaceuticals (NASDAQ:AMRX) develops, manufactures, and distributes generic medicines, specialty branded drugs, biosimilars, and injectable products for the U.S. healthcare market.

- Low returns on capital reflect management’s struggle to allocate funds effectively

- The good news is that its excellent adjusted operating margin highlights the strength of its business model

Amneal falls short of our quality standards. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Amneal

Amneal’s stock price of $14.65 implies a valuation ratio of 17.2x forward P/E. This multiple is lower than most healthcare companies, but for good reason.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Amneal (AMRX) Research Report: Q4 CY2025 Update

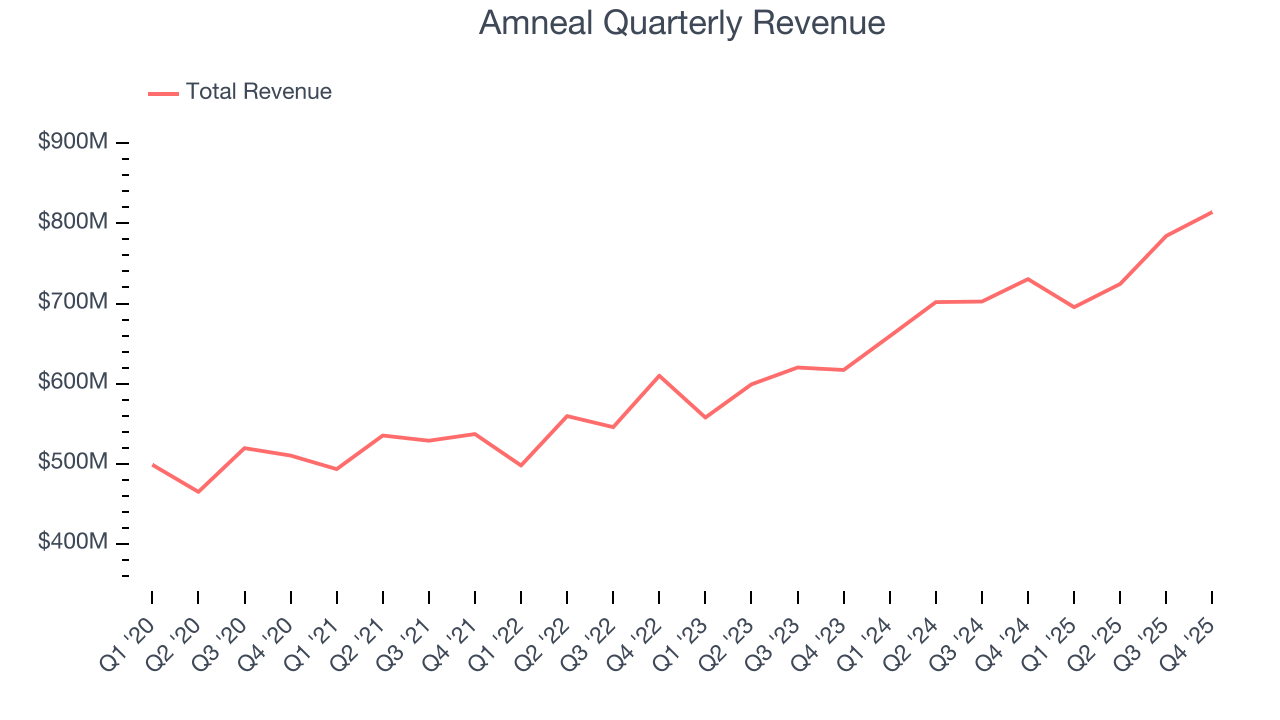

Pharmaceutical company Amneal Pharmaceuticals (NASDAQ:AMRX) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 11.5% year on year to $814.3 million. On the other hand, the company’s full-year revenue guidance of $3.1 billion at the midpoint came in 3.4% below analysts’ estimates. Its non-GAAP profit of $0.21 per share was 14.1% above analysts’ consensus estimates.

Amneal (AMRX) Q4 CY2025 Highlights:

- Revenue: $814.3 million vs analyst estimates of $807.1 million (11.5% year-on-year growth, 0.9% beat)

- Adjusted EPS: $0.21 vs analyst estimates of $0.18 (14.1% beat)

- Adjusted EBITDA: $175.2 million vs analyst estimates of $169.8 million (21.5% margin, 3.2% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.98 at the midpoint, beating analyst estimates by 4.3%

- EBITDA guidance for the upcoming financial year 2026 is $740 million at the midpoint, above analyst estimates of $731.8 million

- Operating Margin: 13.8%, up from 10.4% in the same quarter last year

- Free Cash Flow Margin: 13.3%, similar to the same quarter last year

- Market Capitalization: $4.56 billion

Company Overview

Founded in 2002 and growing into one of America's largest generic drug producers, Amneal Pharmaceuticals (NASDAQ:AMRX) develops, manufactures, and distributes generic medicines, specialty branded drugs, biosimilars, and injectable products for the U.S. healthcare market.

Amneal operates through three main business segments: Generics, Specialty, and AvKARE. The Generics segment forms the backbone of the company with over 260 product families spanning oral solids, liquids, injectables, nasal sprays, and topicals. Amneal focuses on developing complex generics with high barriers to entry, giving it opportunities to be first-to-file or first-to-market with products that can command higher margins.

The company has significantly expanded its injectable portfolio for hospitals, launching products like esmolol hydrochloride in large volume bags. In 2022, Amneal entered the biosimilar market with Alymsys (referencing Avastin), followed by Releuko and Flynetra, biosimilars for cancer supportive care.

Amneal's Specialty segment focuses on branded medications for central nervous system disorders and endocrine conditions. Key products include RYTARY for Parkinson's disease, UNITHROID for hypothyroidism, and recently acquired ONGENTYS, an add-on treatment for Parkinson's patients experiencing "off" episodes.

The AvKARE segment primarily serves U.S. government agencies, particularly the Department of Defense and Veterans Affairs. This division repackages pharmaceuticals and distributes medical supplies to institutional customers, with a focus on 340b-qualified entities that receive discounted pricing.

When patients fill prescriptions at their local pharmacy, they might receive Amneal's generic version of a common medication without realizing it. For example, a patient with high blood pressure might be prescribed Amneal's generic lisinopril, while a hospital might use Amneal's injectable antibiotics for post-surgical care.

Amneal generates revenue by selling its products through major wholesalers and distributors who then supply retail pharmacies, hospitals, and government institutions. The company maintains manufacturing facilities in the United States, India, and Ireland, with a global supply chain that supports its diverse product portfolio.

4. Generic Pharmaceuticals

The generic pharmaceutical industry operates on a volume-driven, low-cost business model, producing bioequivalent versions of branded drugs once their patents expire. These companies benefit from consistent demand for affordable medications, as they are critical to reducing healthcare costs. Generics typically face lower R&D expenses and shorter regulatory approval timelines compared to branded drug makers, enabling cost efficiencies. However, the industry is highly competitive, with intense pricing pressures, thin margins, and frequent legal challenges from branded pharmaceutical companies over patent disputes. Looking ahead, the industry is supported by tailwinds such as the role of AI in streamlining drug development (reverse engineering complex formulations) and manufacturing efficiency (optimize processes and remove inefficiencies). Governments and insurers' focus on reducing drug costs can also boost generics' adoption. However, headwinds include escalating pricing pressure from large buyers like pharmacy chains and healthcare distributors as well as evolving regulatory hurdles.

Amneal's primary competitors in the generic pharmaceutical market include Teva Pharmaceutical Industries, Viatris (formerly Mylan), Sandoz Group, and Sun Pharmaceutical Industries. In the specialty pharmaceutical segment, Amneal competes with companies like Supernus Pharmaceuticals and Alkermes, while its AvKARE division faces competition from major pharmaceutical wholesalers such as Cardinal Health, McKesson, and Cencora (formerly AmerisourceBergen).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.02 billion in revenue over the past 12 months, Amneal has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

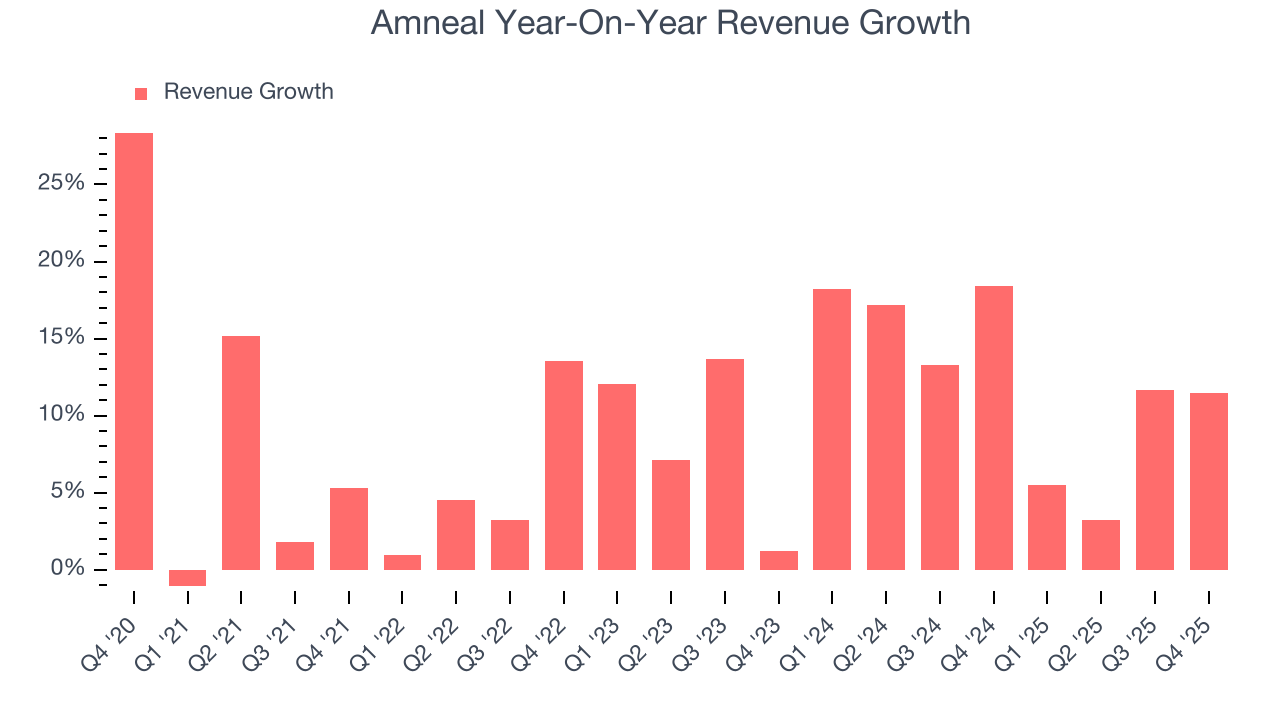

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Amneal’s sales grew at a decent 8.7% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Amneal’s annualized revenue growth of 12.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Amneal reported year-on-year revenue growth of 11.5%, and its $814.3 million of revenue exceeded Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and implies the market is baking in some success for its newer products and services.

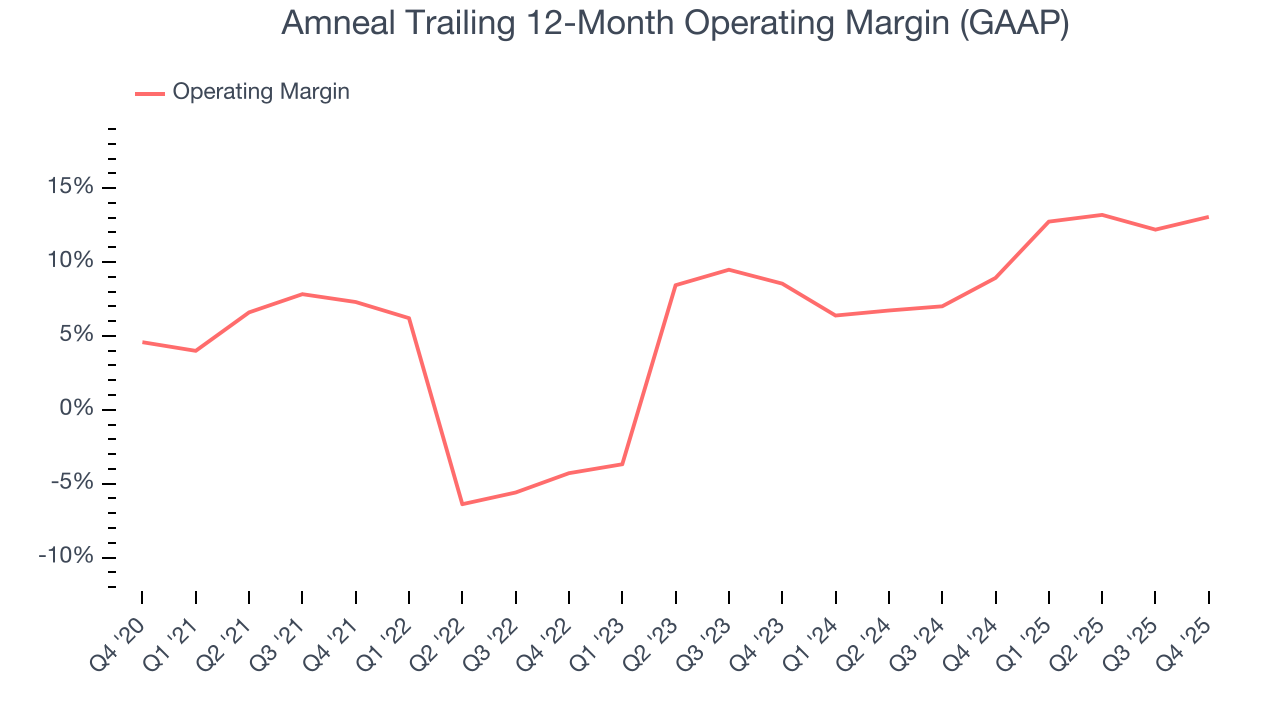

7. Operating Margin

Amneal was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.2% was weak for a healthcare business.

On the plus side, Amneal’s operating margin rose by 5.8 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 4.5 percentage points on a two-year basis.

In Q4, Amneal generated an operating margin profit margin of 13.8%, up 3.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

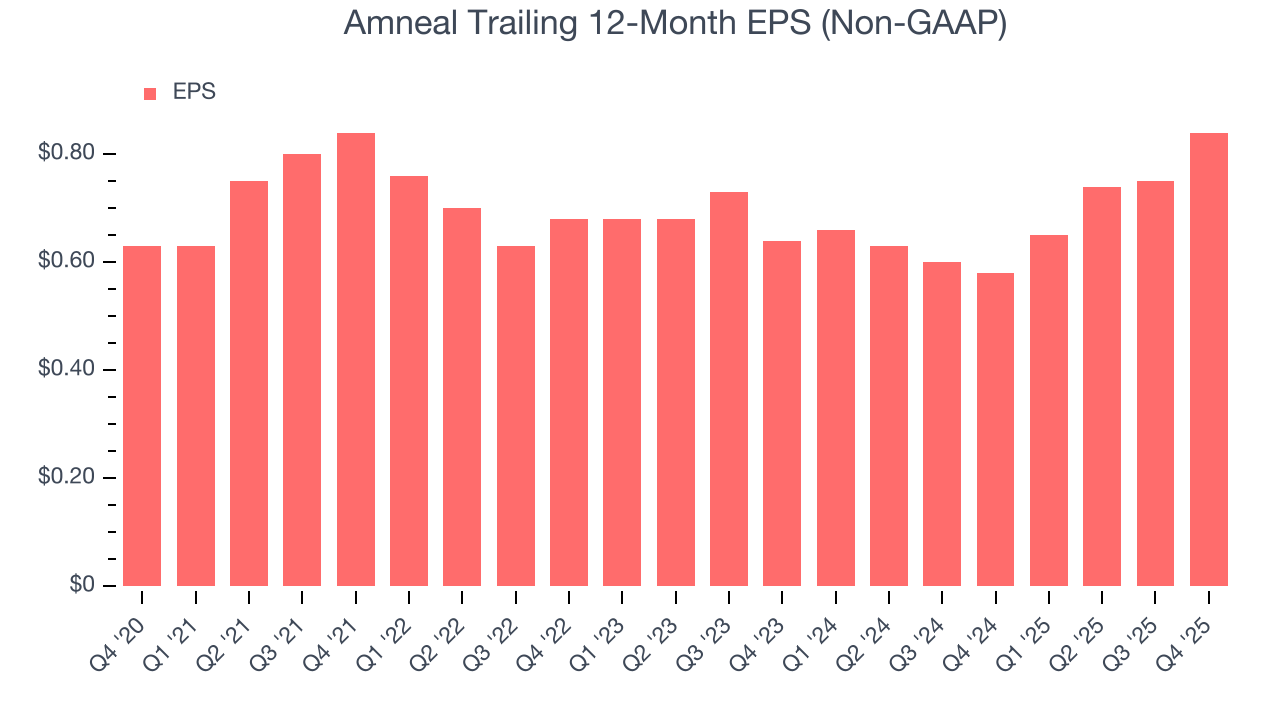

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Amneal’s EPS grew at a decent 5.9% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 8.7% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

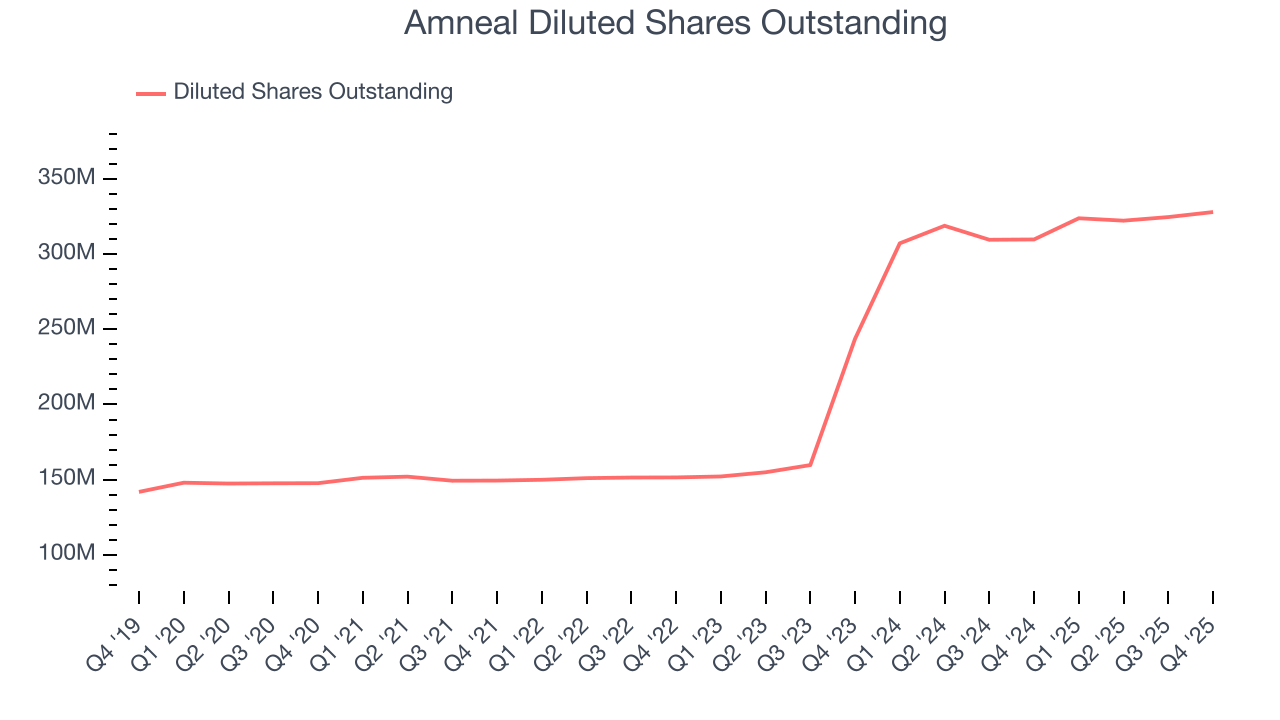

Diving into Amneal’s quality of earnings can give us a better understanding of its performance. A five-year view shows Amneal has diluted its shareholders, growing its share count by 122%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Amneal reported adjusted EPS of $0.21, up from $0.12 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Amneal’s full-year EPS of $0.84 to grow 13.1%.

9. Cash Is King

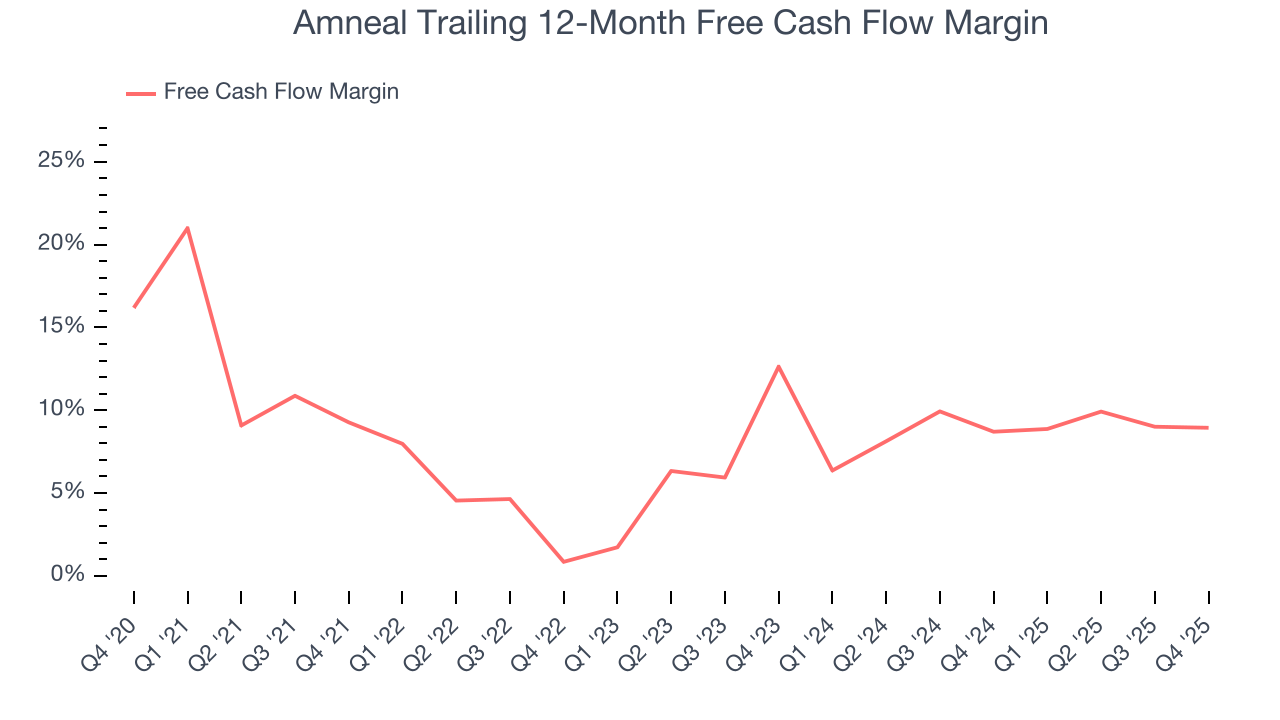

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Amneal has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.2% over the last five years, slightly better than the broader healthcare sector.

Amneal’s free cash flow clocked in at $108.5 million in Q4, equivalent to a 13.3% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

10. Return on Invested Capital (ROIC)

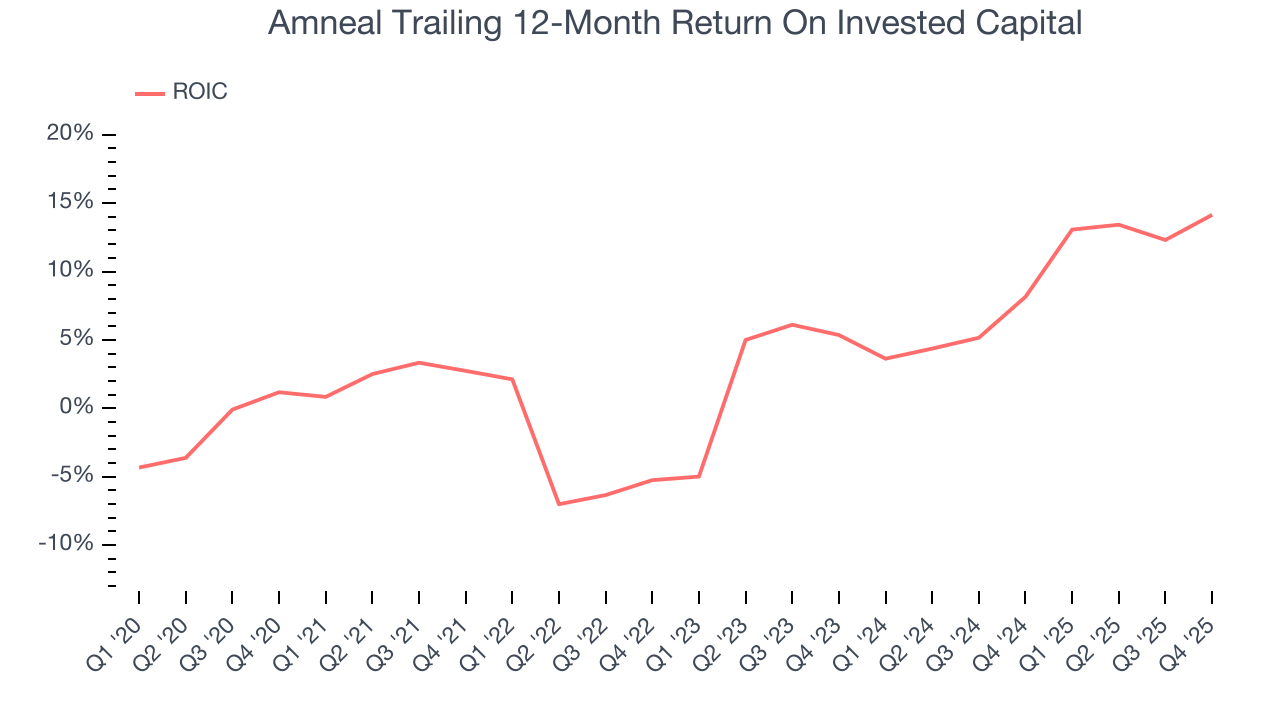

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Amneal historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Amneal’s ROIC has increased significantly over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

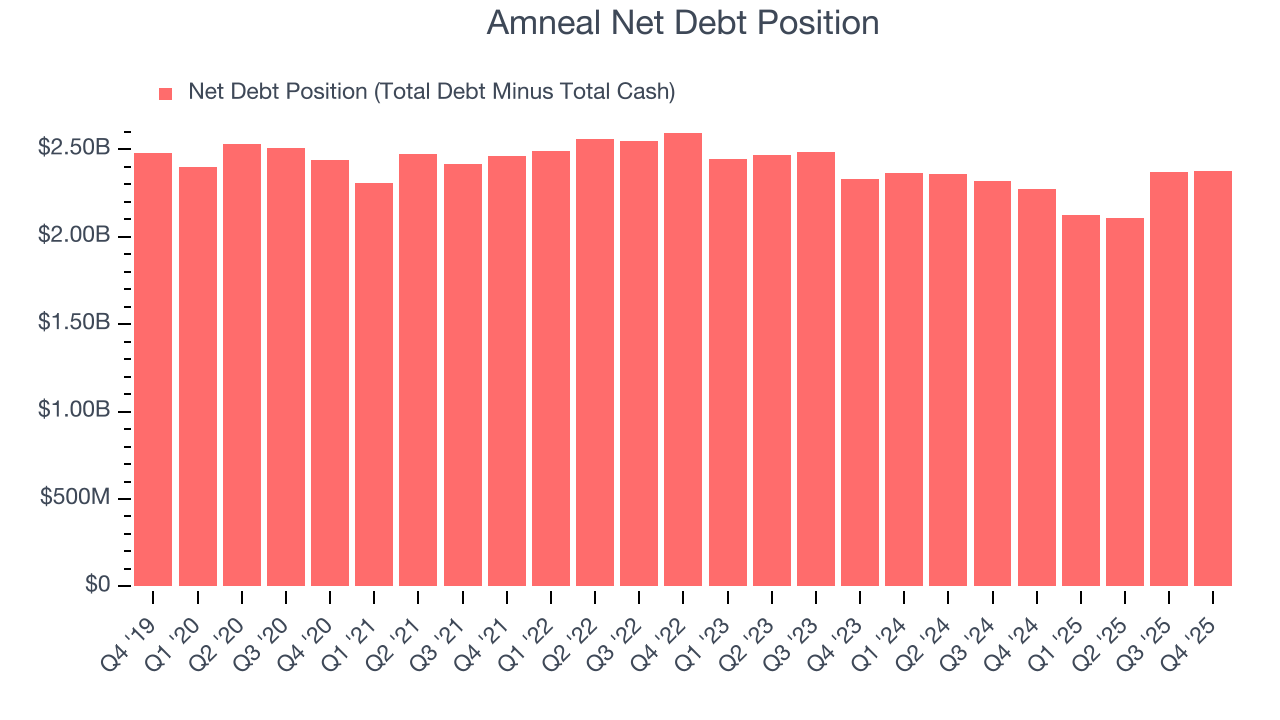

11. Balance Sheet Assessment

Amneal reported $310.9 million of cash and $2.69 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $688.4 million of EBITDA over the last 12 months, we view Amneal’s 3.5× net-debt-to-EBITDA ratio as safe. We also see its $128.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Amneal’s Q4 Results

We enjoyed seeing Amneal beat analysts’ full-year EPS guidance expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $14.35 immediately following the results.

13. Is Now The Time To Buy Amneal?

Before deciding whether to buy Amneal or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Amneal isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its mediocre ROIC lags the market and is a headwind for its stock price. And while the company’s rising returns show management's prior bets are at least better than before, the downside is its operating margins are low compared to other healthcare companies.

Amneal’s P/E ratio based on the next 12 months is 15.3x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $15.20 on the company (compared to the current share price of $14.35).