CECO Environmental (CECO)

We’re firm believers in CECO Environmental. Its sales and EPS are anticipated to grow nicely over the next 12 months, a welcome sign for investors.― StockStory Analyst Team

1. News

2. Summary

Why We Like CECO Environmental

With roots dating back to 1869 and a focus on creating cleaner industrial operations, CECO Environmental (NASDAQ:CECO) provides technology and expertise that helps industrial companies reduce emissions, treat water, and improve energy efficiency across various sectors.

- Market share has increased this cycle as its 19.6% annual revenue growth over the last five years was exceptional

- Demand for the next 12 months is expected to accelerate above its two-year trend as Wall Street forecasts robust revenue growth of 23.2%

- Earnings per share have outperformed the peer group average over the last five years, increasing by 10% annually

CECO Environmental is a market leader. No coincidence the stock is up 518% over the last five years.

Is Now The Time To Buy CECO Environmental?

At $53.54 per share, CECO Environmental trades at 35.4x forward P/E. There are high expectations given this pricey multiple; we can’t deny that.

If you’re a fan of the company and its story, we suggest a small position as the long-term outlook seems solid. Be aware that CECO Environmental’s premium valuation could result in choppy short-term stock performance.

3. CECO Environmental (CECO) Research Report: Q4 CY2025 Update

Environmental solutions provider CECO Environmental (NASDAQ:CECO) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 35.4% year on year to $214.7 million. The company’s full-year revenue guidance of $950 million at the midpoint came in 8.1% above analysts’ estimates. Its GAAP profit of $0.08 per share was 73.9% below analysts’ consensus estimates.

CECO Environmental (CECO) Q4 CY2025 Highlights:

- Revenue: $214.7 million vs analyst estimates of $208.2 million (35.4% year-on-year growth, 3.1% beat)

- EPS (GAAP): $0.08 vs analyst expectations of $0.31 (73.9% miss)

- Adjusted EBITDA: $29.8 million vs analyst estimates of $30.7 million (13.9% margin, 2.9% miss)

- EBITDA guidance for the upcoming financial year 2026 is $125 million at the midpoint, above analyst estimates of $117.7 million

- Operating Margin: 7.7%, in line with the same quarter last year

- Free Cash Flow was $7.29 million, up from -$4.4 million in the same quarter last year

- Market Capitalization: $2.77 billion

Company Overview

With roots dating back to 1869 and a focus on creating cleaner industrial operations, CECO Environmental (NASDAQ:CECO) provides technology and expertise that helps industrial companies reduce emissions, treat water, and improve energy efficiency across various sectors.

CECO Environmental operates at the intersection of industrial productivity and environmental protection, offering engineered solutions that address air pollution, water treatment, and energy efficiency challenges. The company's product portfolio includes specialized equipment such as dampers, scrubbers, filtration systems, thermal oxidizers, and water treatment packages that help industrial facilities meet regulatory requirements while optimizing their operations.

The company serves a diverse range of industries through two main segments: Engineered Systems and Industrial Process Solutions. The Engineered Systems segment focuses on emissions management, separation technologies, and acoustic control for sectors like power generation, hydrocarbon processing, and midstream oil and gas. The Industrial Process Solutions segment provides air pollution control, fluid handling, and filtration systems for industries ranging from semiconductor fabrication to food processing and automotive manufacturing.

A typical CECO customer might be a refinery seeking to reduce harmful emissions from its operations. CECO would design and install specialized scrubber systems that capture pollutants before they enter the atmosphere, helping the facility comply with environmental regulations while maintaining operational efficiency.

Rather than selling standardized products, CECO typically customizes its solutions to meet specific customer requirements. The company generates revenue through the design, manufacture, installation, and servicing of these engineered systems. CECO maintains a global presence with direct sales operations in key regions including the United States, Europe, the Middle East, and Asia, allowing it to serve multinational industrial clients worldwide.

4. Industrial & Environmental Services

Growing regulatory pressure on environmental compliance and increasing corporate ESG commitments should buoy the sector for years to come. On the other hand, environmental regulations continue to evolve, and this may require costly upgrades, volatility in commodity waste and recycling markets, and labor shortages in industrial services. As for digitization, a theme that is impacting nearly every industry, the increasing use of data, analytics, and automation will give rise to improved efficiency of operations. Conversely, though, the benefits of digitization also come with challenges of integrating new technologies into legacy systems.

CECO Environmental competes with other environmental technology and industrial solutions providers including Donaldson Company (NYSE:DCI), Evoqua Water Technologies (now part of Xylem, NYSE:XYL), Fuel Tech (NASDAQ:FTEK), and privately-held companies like Dürr Environmental and Babcock & Wilcox Environmental.

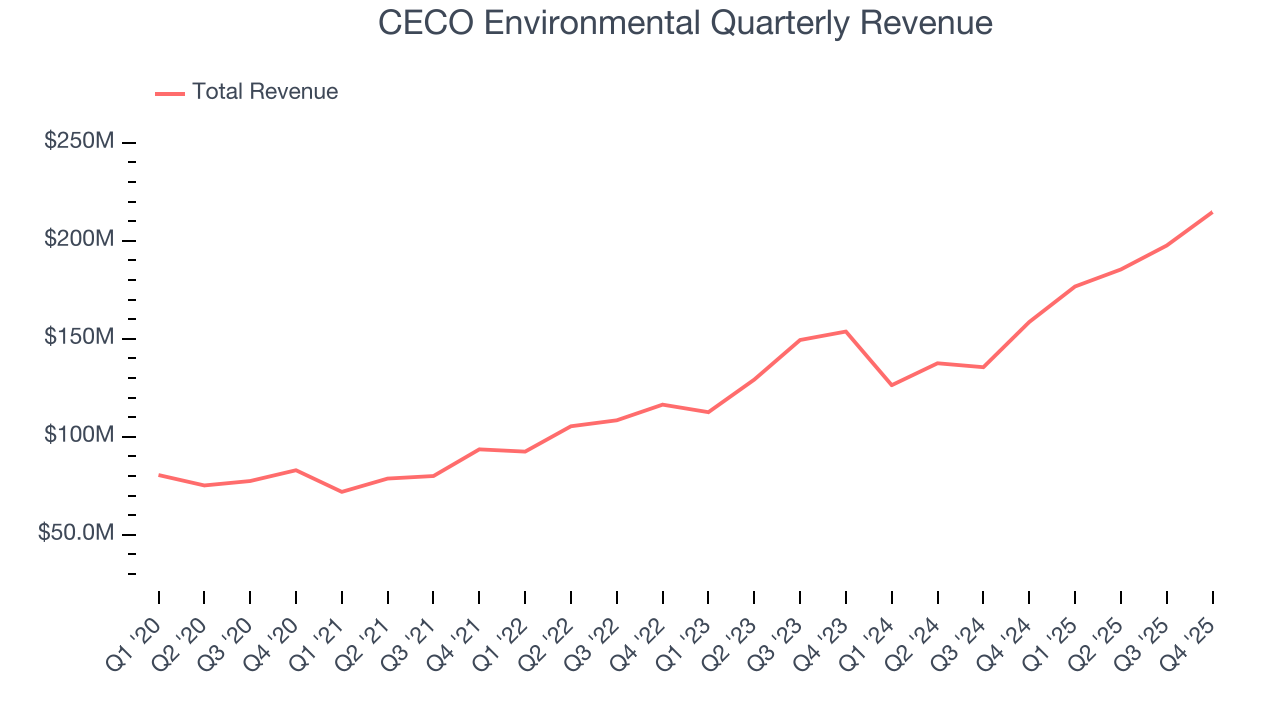

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $774.4 million in revenue over the past 12 months, CECO Environmental is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

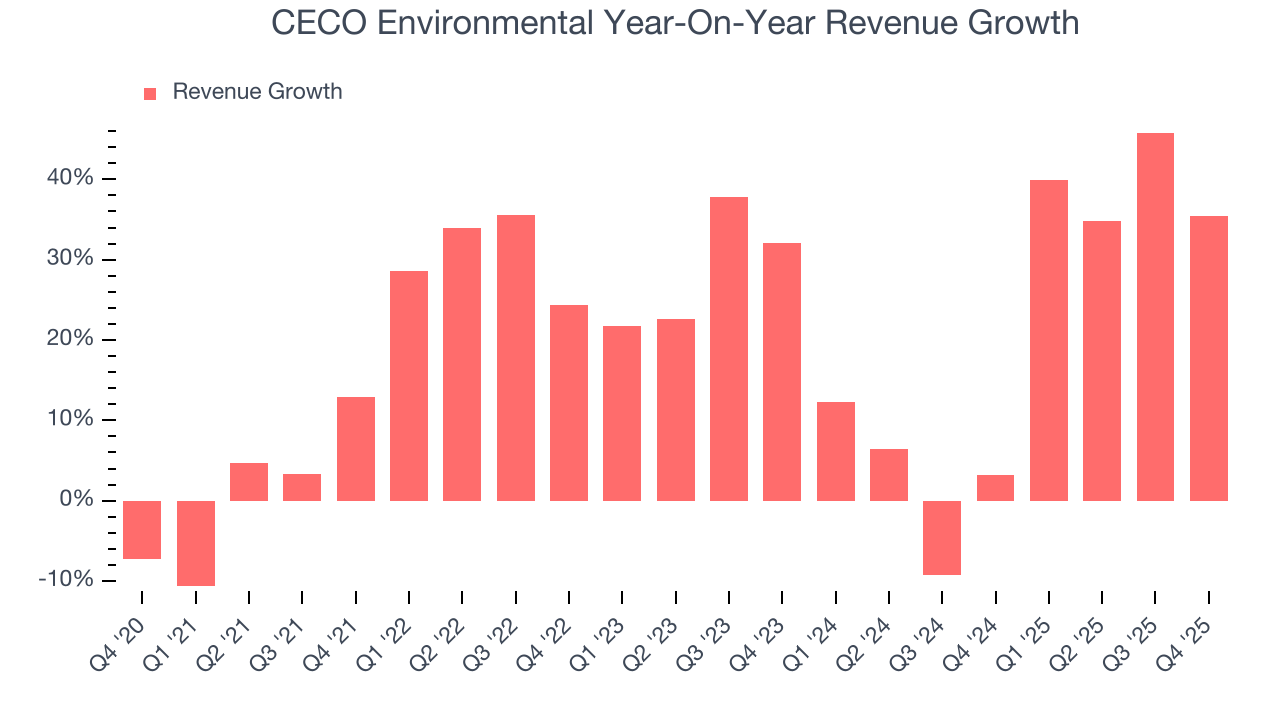

As you can see below, CECO Environmental’s sales grew at an incredible 19.6% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows CECO Environmental’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. CECO Environmental’s annualized revenue growth of 19.2% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, CECO Environmental reported wonderful year-on-year revenue growth of 35.4%, and its $214.7 million of revenue exceeded Wall Street’s estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 14.4% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and suggests the market is forecasting success for its products and services.

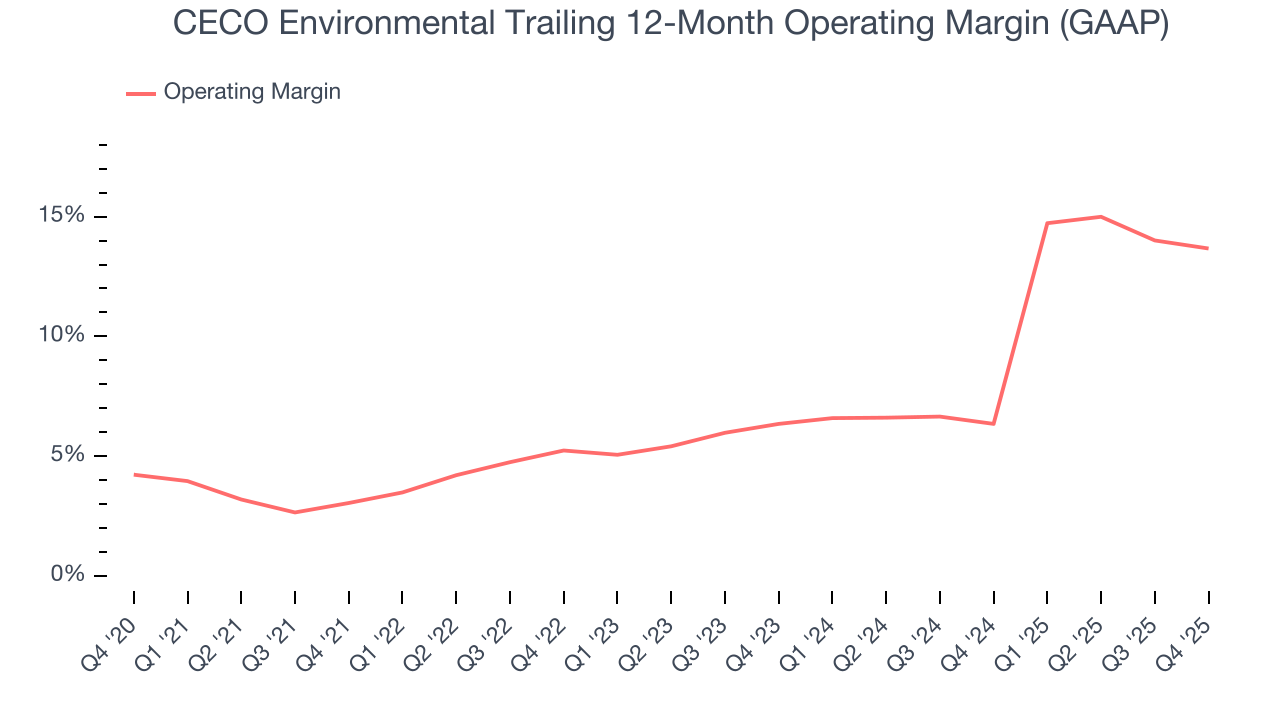

6. Operating Margin

CECO Environmental was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.9% was weak for a business services business.

On the plus side, CECO Environmental’s operating margin rose by 10.6 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, CECO Environmental generated an operating margin profit margin of 7.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

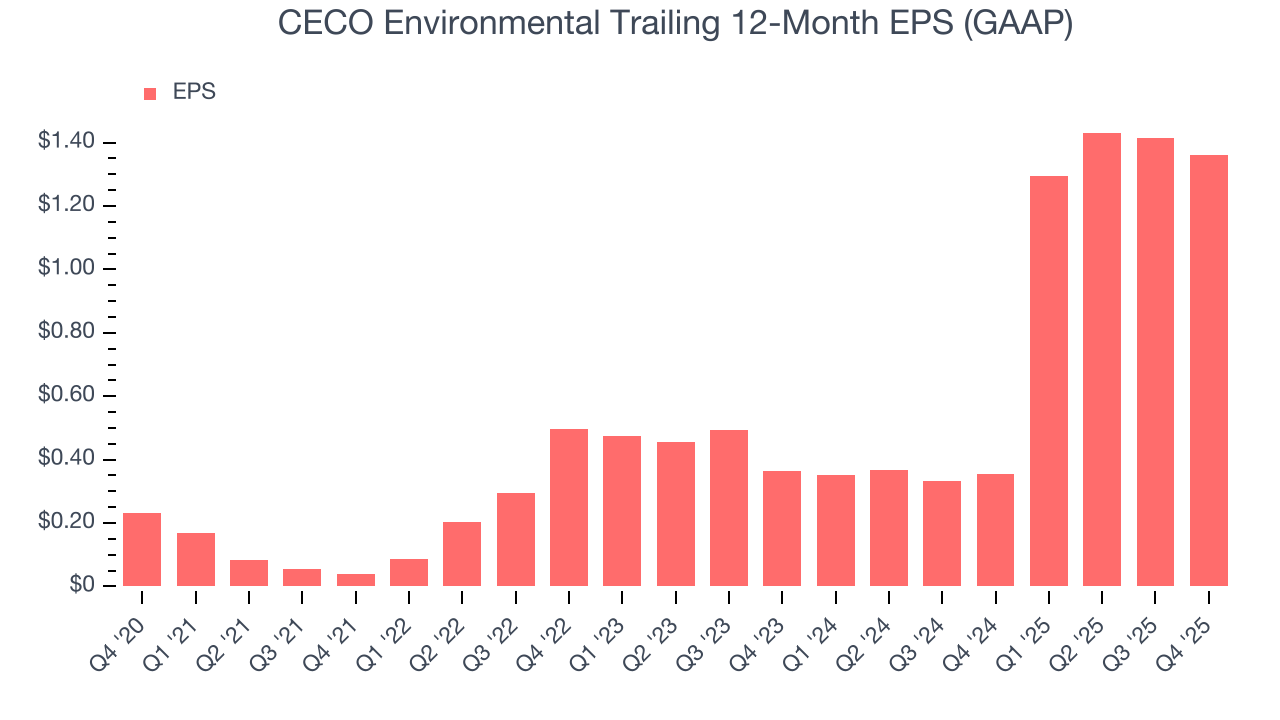

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

CECO Environmental’s EPS grew at an astounding 42.5% compounded annual growth rate over the last five years, higher than its 19.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into CECO Environmental’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, CECO Environmental’s operating margin was flat this quarter but expanded by 10.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For CECO Environmental, its two-year annual EPS growth of 93.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, CECO Environmental reported EPS of $0.08, down from $0.13 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects CECO Environmental’s full-year EPS of $1.36 to shrink by 19.5%.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

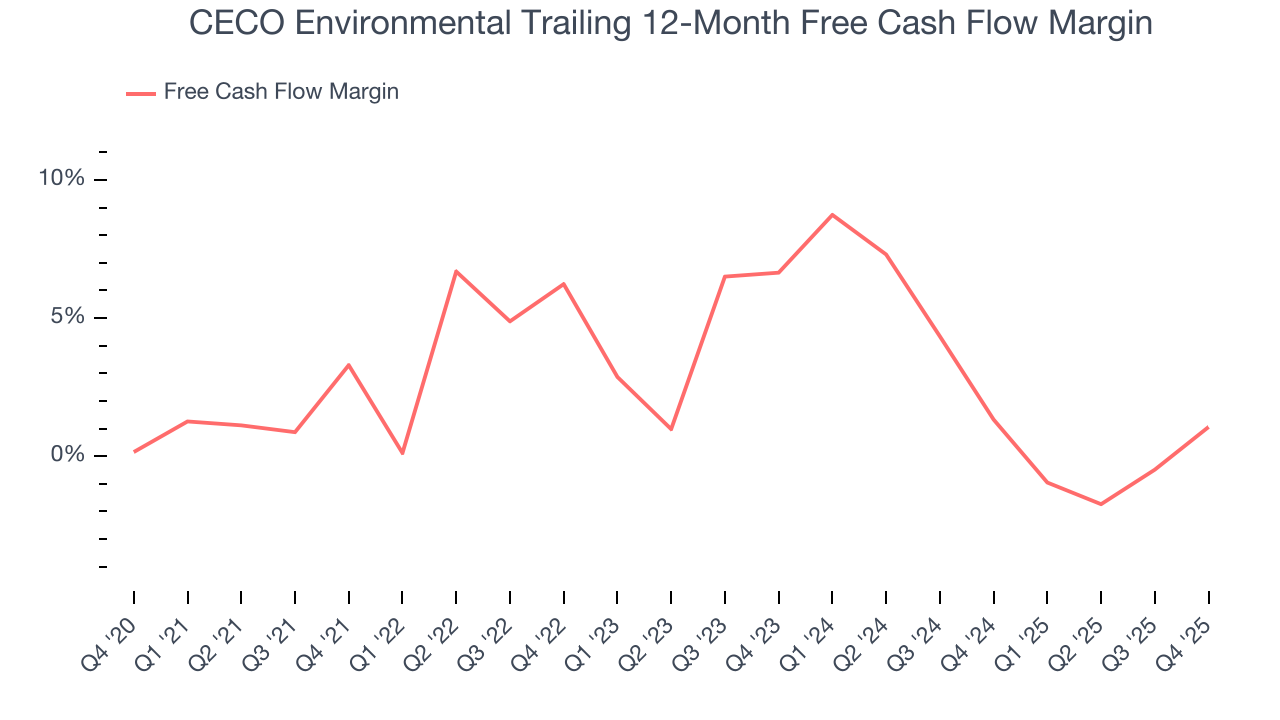

CECO Environmental has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.4%, subpar for a business services business.

Taking a step back, we can see that CECO Environmental’s margin dropped by 2.2 percentage points during that time. If the trend continues, it could signal it’s in the middle of an investment cycle.

CECO Environmental’s free cash flow clocked in at $7.29 million in Q4, equivalent to a 3.4% margin. Its cash flow turned positive after being negative in the same quarter last year. We hope the company can build on this trend.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

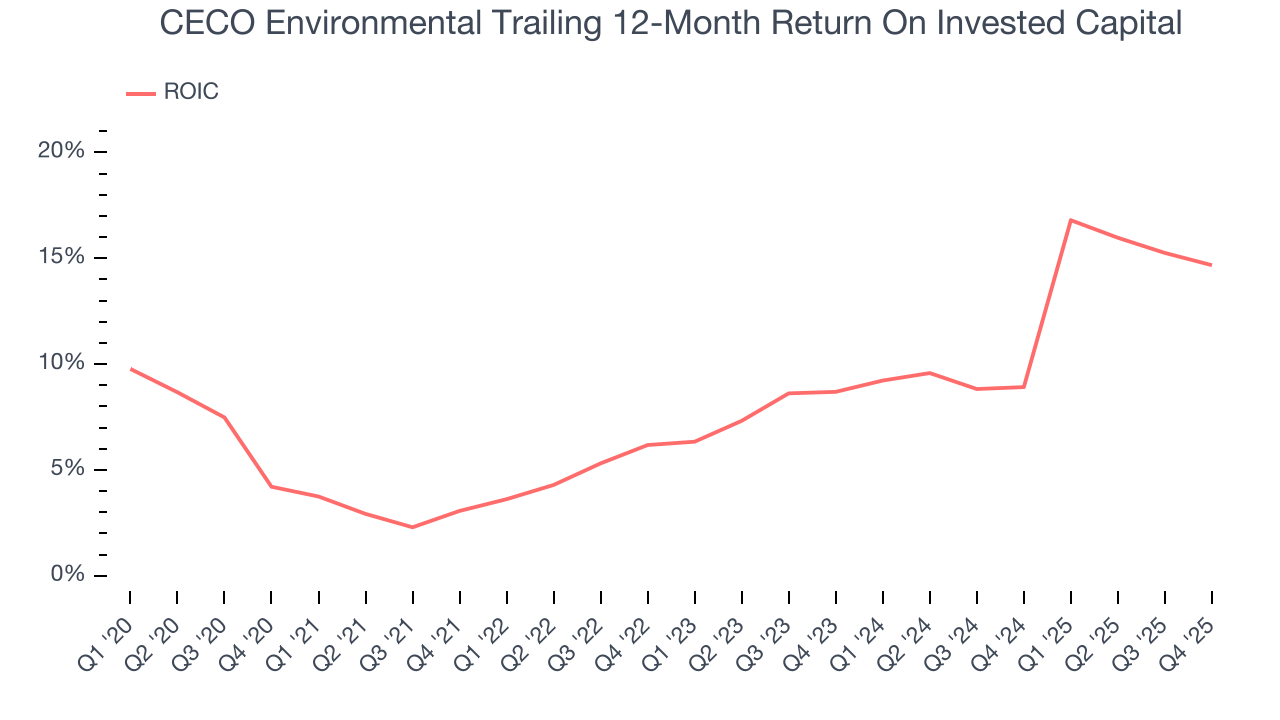

Although CECO Environmental has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.3%, somewhat low compared to the best business services companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, CECO Environmental’s has increased over the last few years. its rising ROIC is a good sign and could suggest its competitive advantage or profitable growth opportunities are expanding.

10. Balance Sheet Assessment

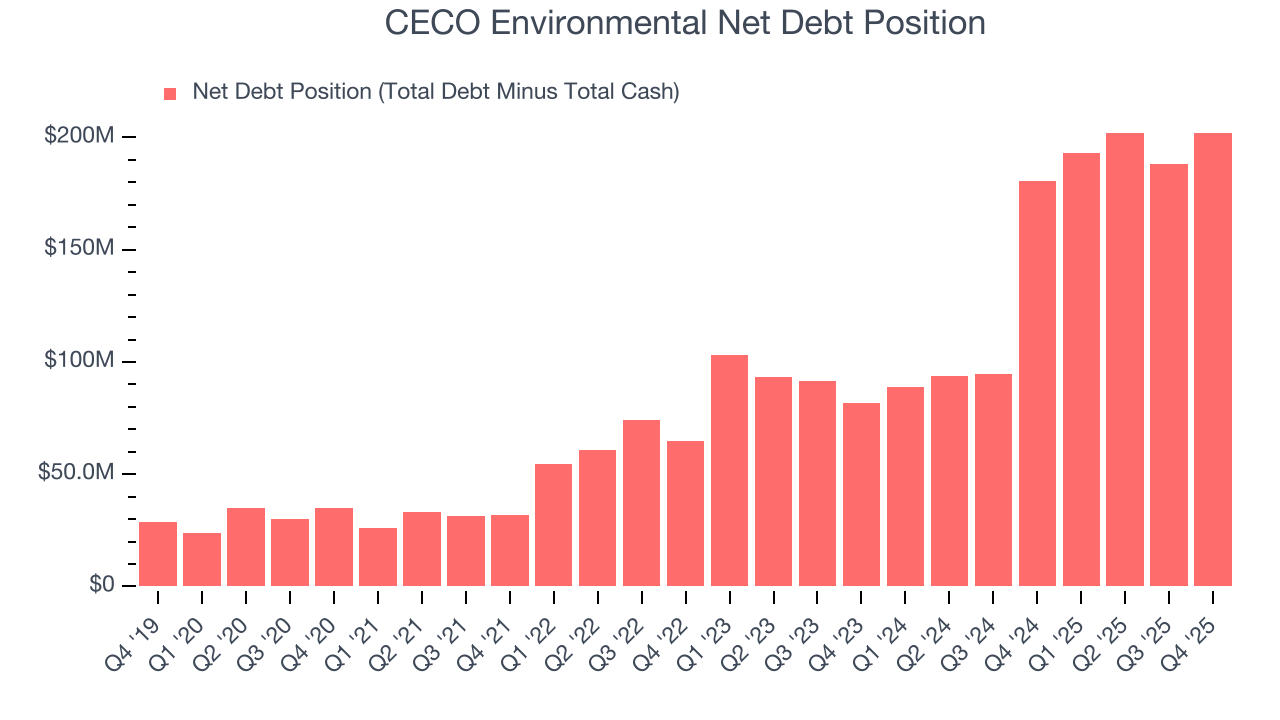

CECO Environmental reported $33.23 million of cash and $235.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $90.3 million of EBITDA over the last 12 months, we view CECO Environmental’s 2.2× net-debt-to-EBITDA ratio as safe. We also see its $11.43 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from CECO Environmental’s Q4 Results

We were impressed by CECO Environmental’s optimistic full-year revenue guidance, which blew past analysts’ expectations. EBITDA guidance also beat. We were also glad its revenue in the quarter outperformed Wall Street’s estimates. On the other hand, its EBITDA and EPS missed. Overall, this print was mixed. The stock remained flat at $77.17 immediately after reporting.

12. Is Now The Time To Buy CECO Environmental?

Updated: March 15, 2026 at 11:12 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in CECO Environmental.

There are several reasons why we think CECO Environmental is a great business. For starters, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. And while its subscale operations give it fewer distribution channels than its larger rivals, its expanding adjusted operating margin shows the business has become more efficient. On top of that, CECO Environmental’s projected EPS for the next year implies the company’s fundamentals will improve.

CECO Environmental’s P/E ratio based on the next 12 months is 35.4x. This multiple isn’t necessarily cheap, but we’ll happily own CECO Environmental as its fundamentals shine bright. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany relatively high valuations.

Wall Street analysts have a consensus one-year price target of $78.83 on the company (compared to the current share price of $53.54).