Pitney Bowes (PBI)

Pitney Bowes doesn’t excite us. Its weak profitability and declining sales not only show demand is fading but also illustrate poor fundamentals.― StockStory Analyst Team

1. News

2. Summary

Why We Think Pitney Bowes Will Underperform

With a century-long history dating back to 1920 and processing over 15 billion pieces of mail annually, Pitney Bowes (NYSE:PBI) provides shipping, mailing technology, logistics, and financial services to businesses of all sizes.

- Annual sales declines of 11.8% for the past five years show its products and services struggled to connect with the market during this cycle

- Sales are expected to decline once again over the next 12 months as it continues working through a challenging demand environment

- A silver lining is that its earnings per share have outperformed its peers over the last five years, increasing by 35.3% annually

Pitney Bowes doesn’t live up to our standards. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Pitney Bowes

Pitney Bowes’s stock price of $10.35 implies a valuation ratio of 6.9x forward P/E. This sure is a cheap multiple, but you get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Pitney Bowes (PBI) Research Report: Q4 CY2025 Update

Shipping and mailing solutions provider Pitney Bowes (NYSE:PBI) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 7.5% year on year to $477.6 million. The company’s full-year revenue guidance of $1.81 billion at the midpoint came in 2.2% below analysts’ estimates. Its non-GAAP profit of $0.45 per share was 17.6% above analysts’ consensus estimates.

Pitney Bowes (PBI) Q4 CY2025 Highlights:

- Revenue: $477.6 million vs analyst estimates of $482.5 million (7.5% year-on-year decline, 1% miss)

- Adjusted EPS: $0.45 vs analyst estimates of $0.38 (17.6% beat)

- Adjusted EBITDA: $159 million vs analyst estimates of $150.6 million (33.3% margin, 5.6% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.50 at the midpoint, beating analyst estimates by 3.8%

- Operating Margin: 8%, up from 5.6% in the same quarter last year

- Free Cash Flow Margin: 44.4%, up from 21.8% in the same quarter last year

- Market Capitalization: $1.65 billion

Company Overview

With a century-long history dating back to 1920 and processing over 15 billion pieces of mail annually, Pitney Bowes (NYSE:PBI) provides shipping, mailing technology, logistics, and financial services to businesses of all sizes.

Pitney Bowes operates through three main business segments that work together to serve its diverse client base. The Global Ecommerce segment offers retailers a complete suite of shipping solutions, including domestic parcel delivery services through a network of sortation centers and transportation systems. This segment also provides cross-border services that help retailers manage international shipping by calculating duties and taxes at checkout, handling currency conversions, and managing customs documentation. Additionally, its digital delivery services enable clients to compare carrier options and track packages in real-time.

The Presort Services segment positions Pitney Bowes as the largest workshare partner of the United States Postal Service (USPS). Through this business, the company sorts and processes high volumes of mail at its nationwide operating centers, helping clients qualify for postal workshare discounts while expediting delivery times.

The Sending Technology Solutions (SendTech) segment provides physical and digital mailing and shipping technologies. These range from traditional postage meters to cloud-based software-as-a-service solutions that can be accessed via connected devices. For example, a small business might use Pitney Bowes' technology to print shipping labels, track packages, and manage postage expenses all from one platform.

Through its subsidiary, The Pitney Bowes Bank, the company offers financing options for equipment purchases and revolving credit solutions for postage and supplies. This banking arm also provides interest-bearing deposit accounts for clients who prepay postage, creating a financial ecosystem around its core shipping and mailing services.

The company experiences seasonal fluctuations in its business, with the fourth quarter typically generating higher revenue due to increased shipping volumes during the holiday season. Pitney Bowes markets its offerings through direct sales, partner channels, and digital platforms, providing ongoing support through call centers and on-site services.

4. Industrial & Environmental Services

Growing regulatory pressure on environmental compliance and increasing corporate ESG commitments should buoy the sector for years to come. On the other hand, environmental regulations continue to evolve, and this may require costly upgrades, volatility in commodity waste and recycling markets, and labor shortages in industrial services. As for digitization, a theme that is impacting nearly every industry, the increasing use of data, analytics, and automation will give rise to improved efficiency of operations. Conversely, though, the benefits of digitization also come with challenges of integrating new technologies into legacy systems.

Pitney Bowes competes with shipping and logistics giants like FedEx (NYSE:FDX), UPS (NYSE:UPS), and Stamps.com (now Auctane, private), as well as with ecommerce fulfillment providers such as Amazon Logistics (NASDAQ:AMZN) and ShipBob (private).

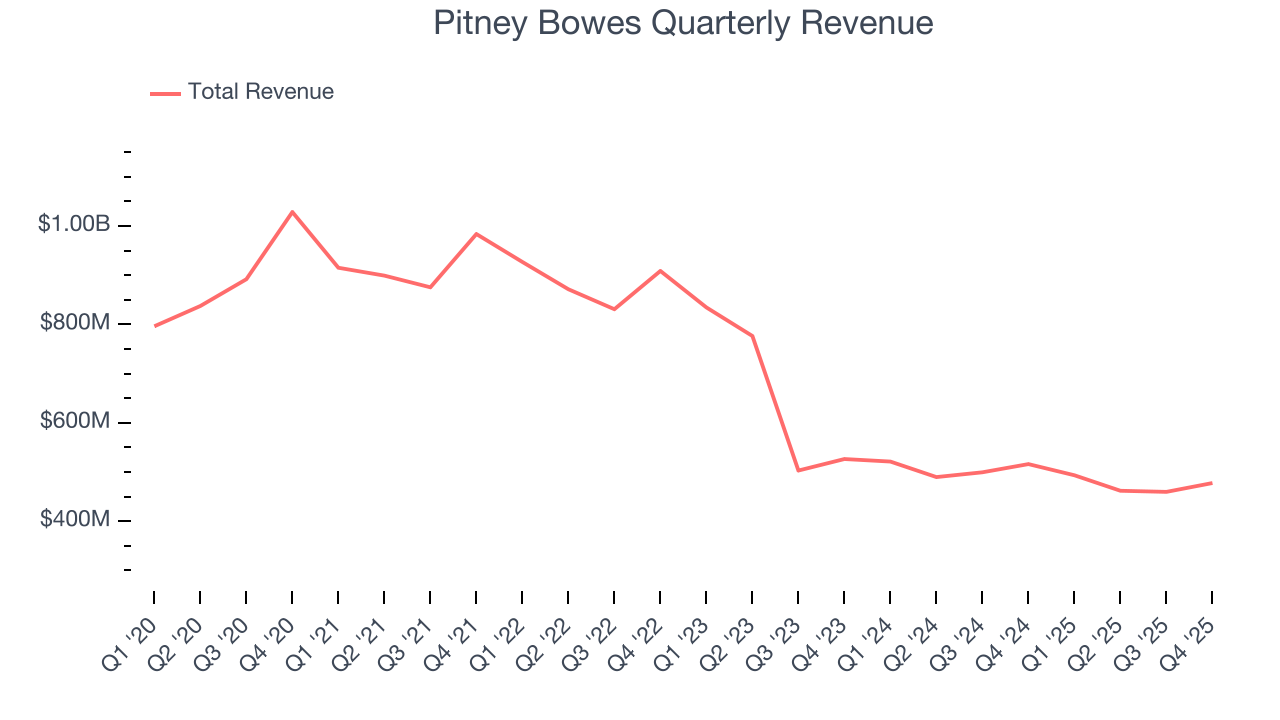

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.89 billion in revenue over the past 12 months, Pitney Bowes is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

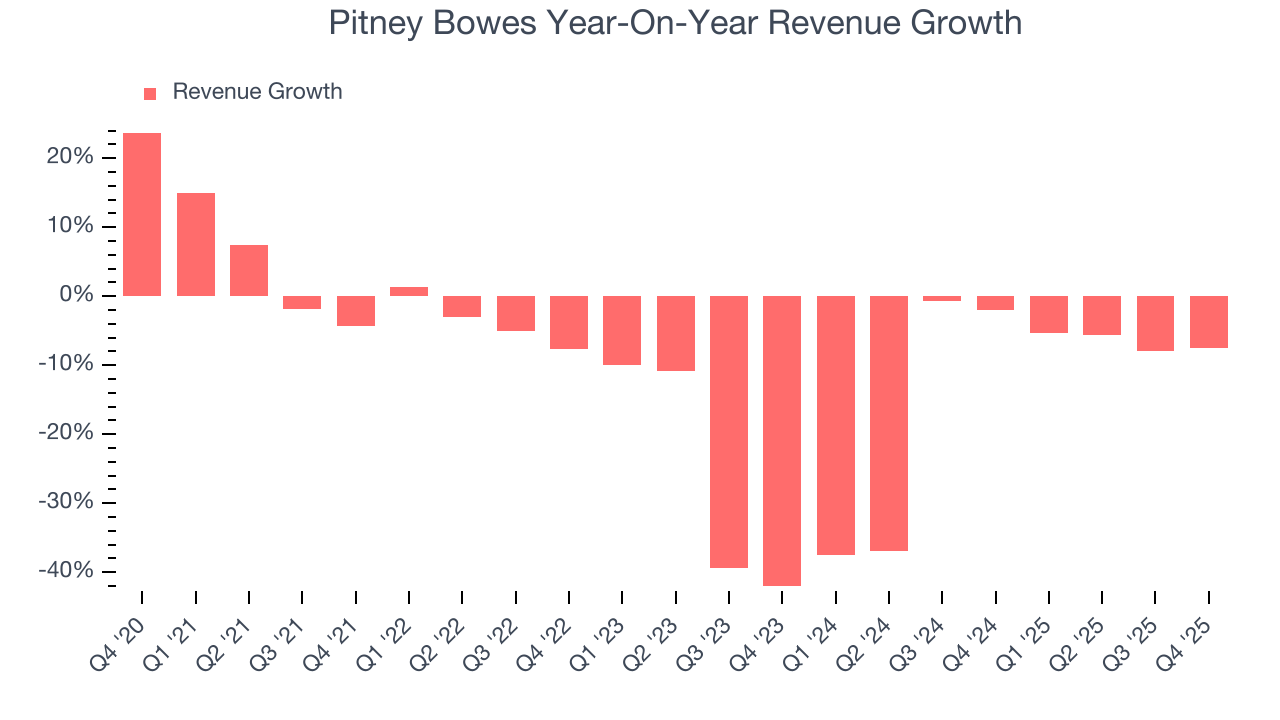

As you can see below, Pitney Bowes struggled to generate demand over the last five years. Its sales dropped by 11.8% annually, a poor baseline for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Pitney Bowes’s recent performance shows its demand remained suppressed as its revenue has declined by 15.3% annually over the last two years.

This quarter, Pitney Bowes missed Wall Street’s estimates and reported a rather uninspiring 7.5% year-on-year revenue decline, generating $477.6 million of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 2.2% over the next 12 months. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

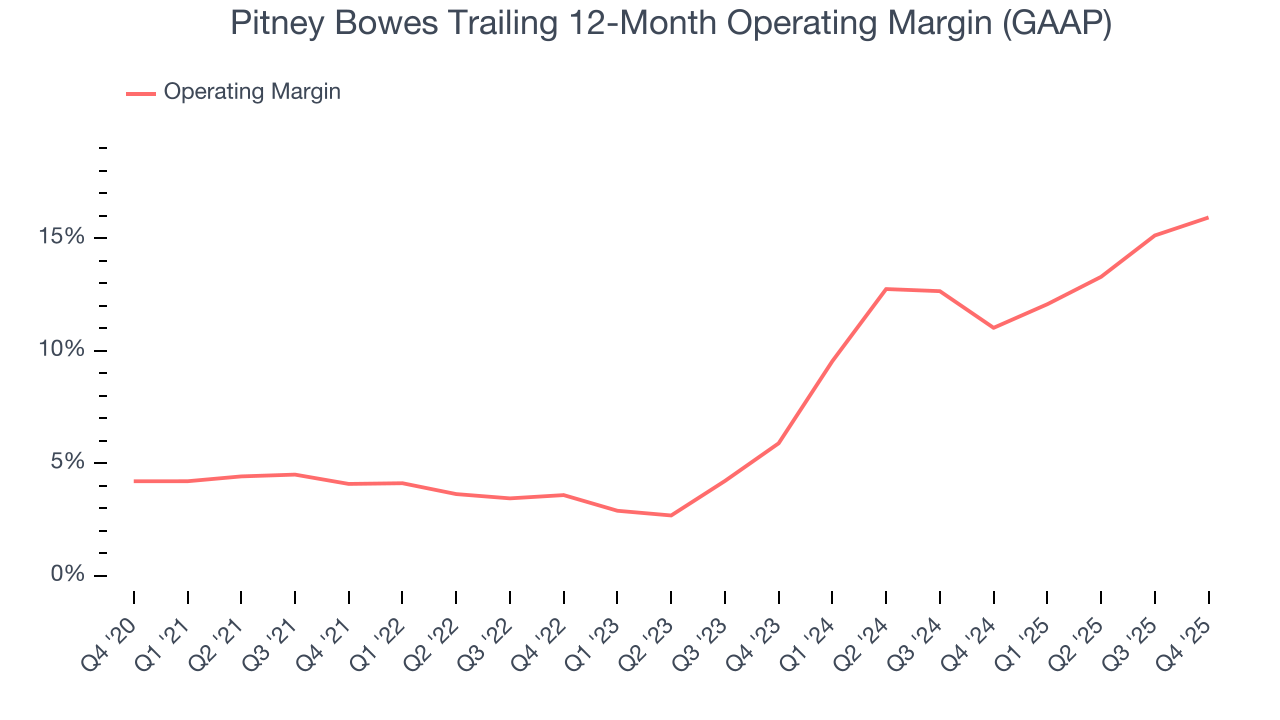

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Pitney Bowes was profitable over the last five years but held back by its large cost base. Its average operating margin of 7% was weak for a business services business.

On the plus side, Pitney Bowes’s operating margin rose by 11.8 percentage points over the last five years.

In Q4, Pitney Bowes generated an operating margin profit margin of 8%, up 2.4 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

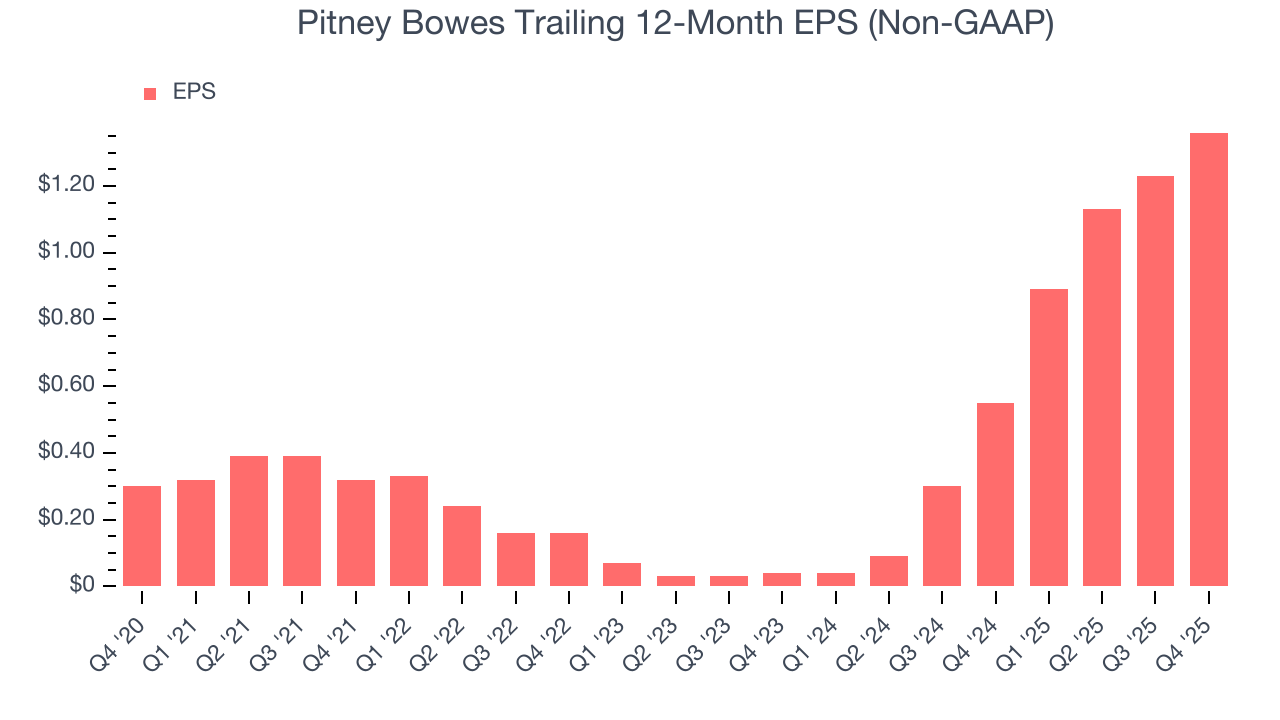

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Pitney Bowes’s EPS grew at an astounding 35.3% compounded annual growth rate over the last five years, higher than its 11.8% annualized revenue declines. This tells us management adapted its cost structure in response to a challenging demand environment.

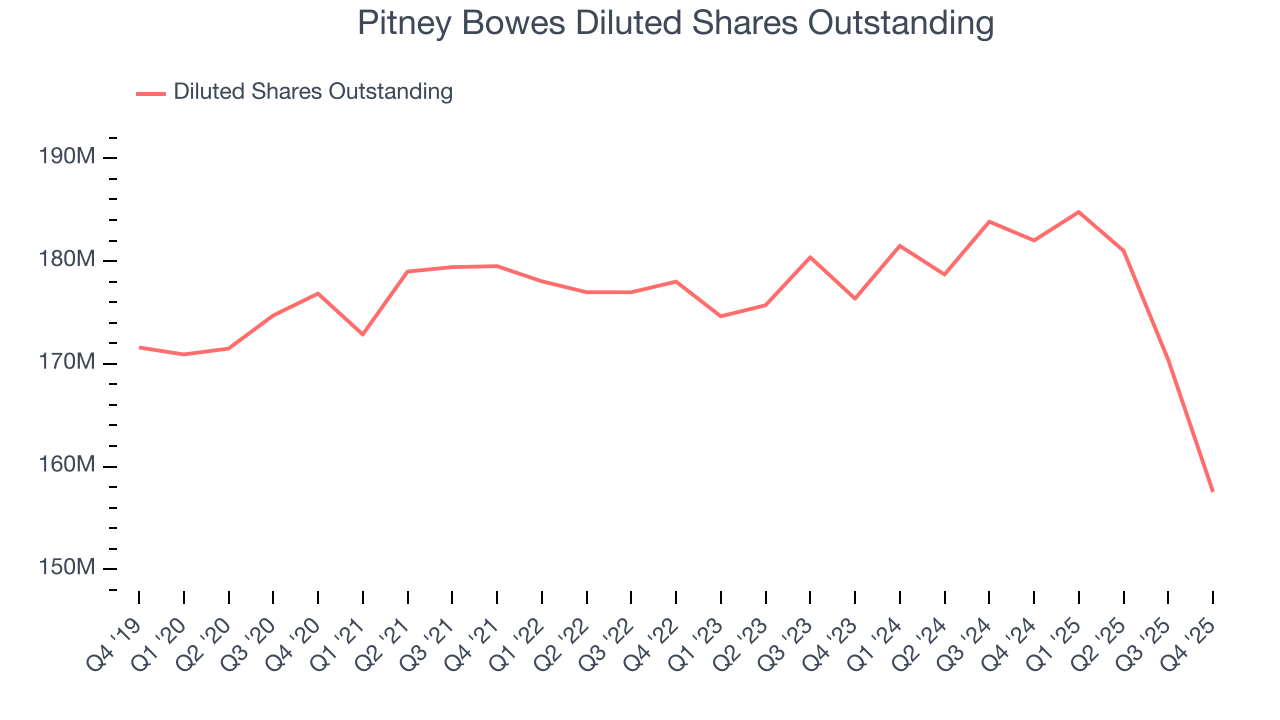

We can take a deeper look into Pitney Bowes’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Pitney Bowes’s operating margin expanded by 11.8 percentage points over the last five years. On top of that, its share count shrank by 10.9%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Pitney Bowes, its two-year annual EPS growth of 483% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Pitney Bowes reported adjusted EPS of $0.45, up from $0.32 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Pitney Bowes’s full-year EPS of $1.36 to grow 5.7%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

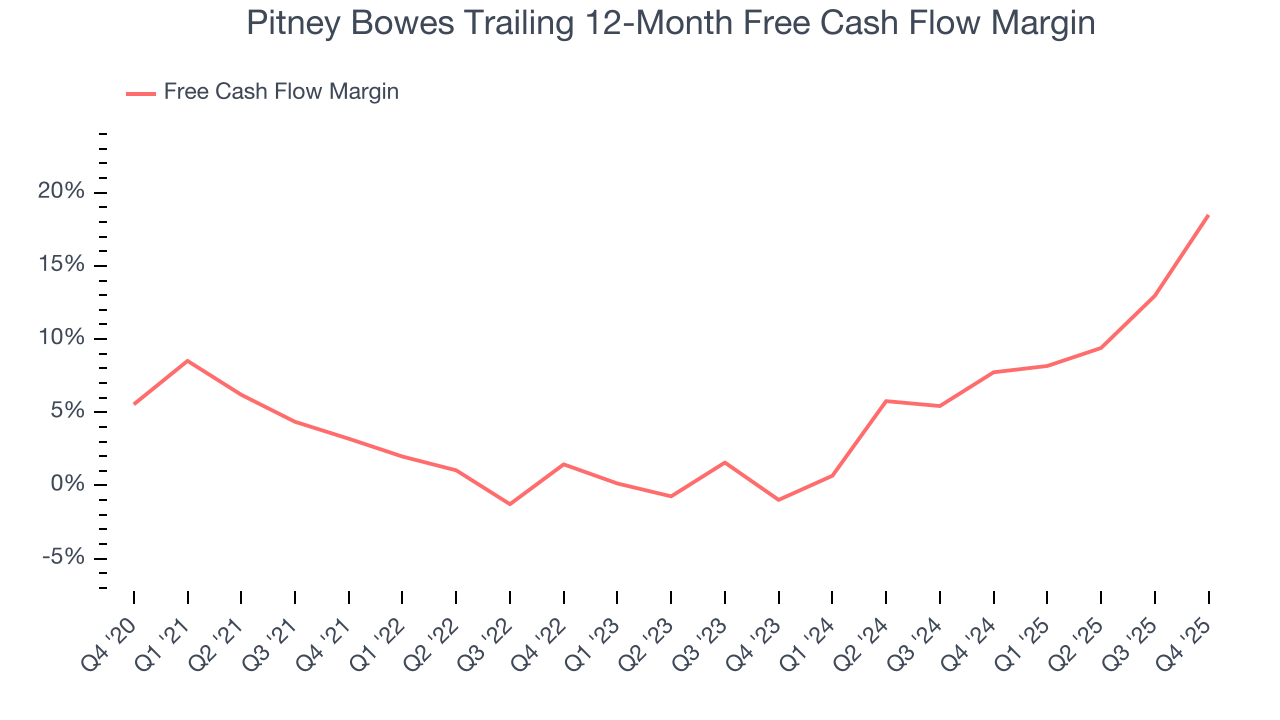

Pitney Bowes has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.7%, subpar for a business services business.

Taking a step back, an encouraging sign is that Pitney Bowes’s margin expanded by 15.3 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Pitney Bowes’s free cash flow clocked in at $211.9 million in Q4, equivalent to a 44.4% margin. This result was good as its margin was 22.6 percentage points higher than in the same quarter last year, building on its favorable historical trend.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

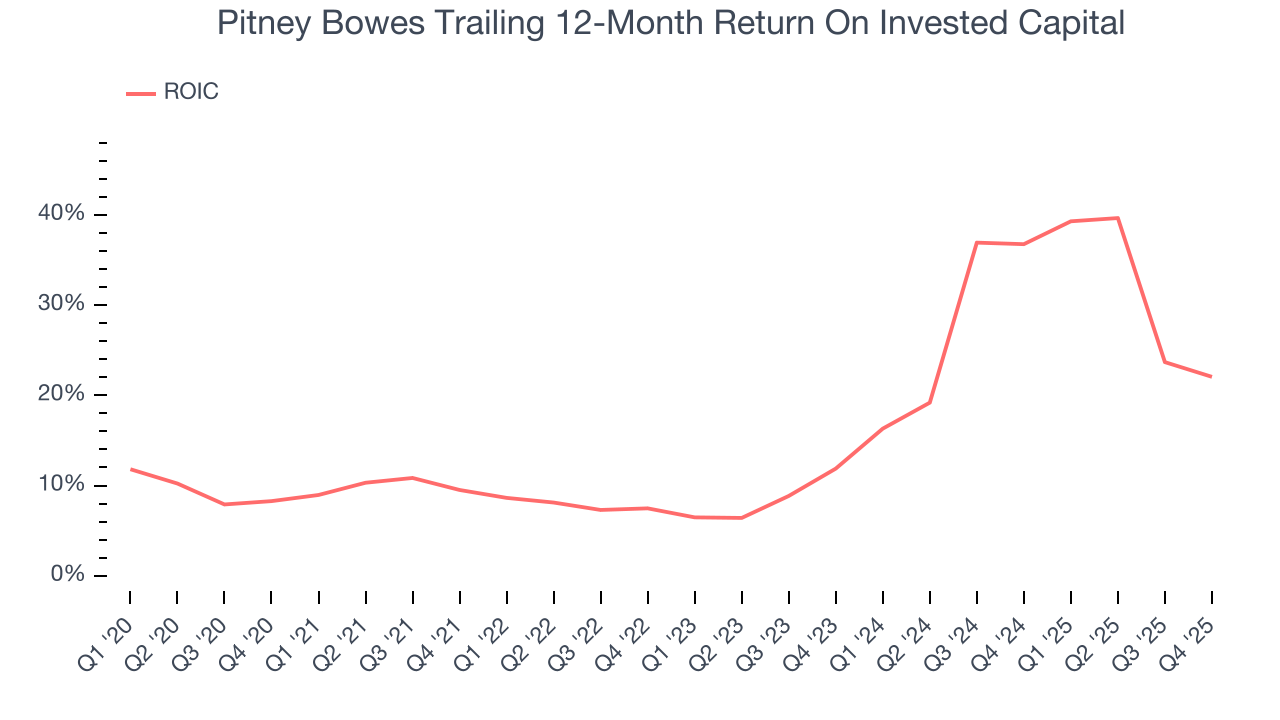

Although Pitney Bowes hasn’t been the highest-quality company lately because of its poor top-line performance, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 17.5%, impressive for a business services business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Pitney Bowes’s ROIC has increased significantly over the last few years. This is a good sign, and we hope the company can keep improving.

10. Balance Sheet Assessment

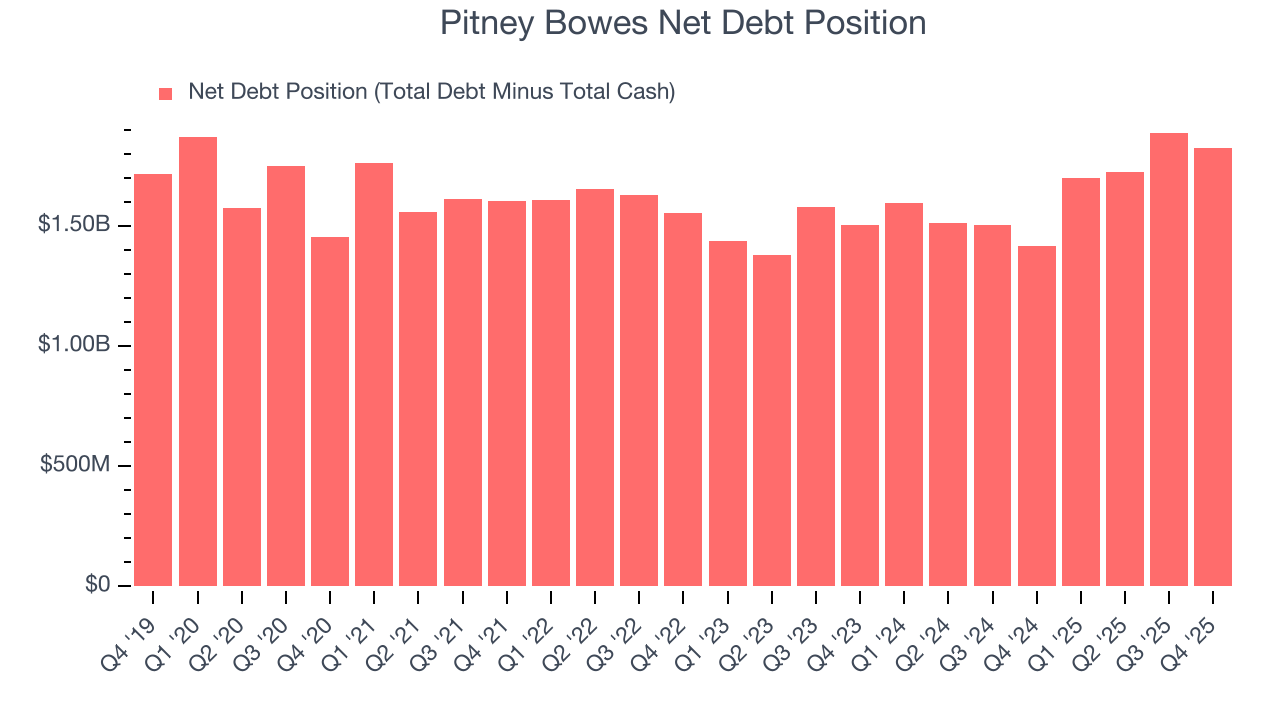

Pitney Bowes reported $297.1 million of cash and $2.12 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $599.9 million of EBITDA over the last 12 months, we view Pitney Bowes’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $49.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Pitney Bowes’s Q4 Results

It was good to see Pitney Bowes beat analysts’ EPS expectations this quarter. We were also glad its full-year EPS guidance outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 13.2% to $11.60 immediately following the results.

12. Is Now The Time To Buy Pitney Bowes?

Updated: March 15, 2026 at 11:31 PM EDT

Before making an investment decision, investors should account for Pitney Bowes’s business fundamentals and valuation in addition to what happened in the latest quarter.

Pitney Bowes isn’t a terrible business, but it doesn’t pass our quality test. First off, its revenue has declined over the last five years. And while Pitney Bowes’s rising cash profitability gives it more optionality, its operating margins are low compared to other business services companies.

Pitney Bowes’s P/E ratio based on the next 12 months is 6.9x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $12.50 on the company (compared to the current share price of $10.35).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.