Capital Southwest (CSWC)

We’re wary of Capital Southwest. Its decelerating revenue growth and even worse EPS performance give us little confidence it can beat the market.― StockStory Analyst Team

1. News

2. Summary

Why We Think Capital Southwest Will Underperform

Originally founded in 1961 as a venture capital investor that helped launch Texas Instruments, Capital Southwest (NASDAQ:CSWC) is a business development company that provides debt and equity financing to middle-market companies primarily in the United States.

- Incremental sales over the last five years were less profitable as its 7.2% annual earnings per share growth lagged its revenue gains

- A silver lining is that its impressive 28% annual revenue growth over the last five years indicates it’s winning market share this cycle

Capital Southwest falls short of our expectations. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Capital Southwest

At $21.91 per share, Capital Southwest trades at 9.7x forward P/E. This sure is a cheap multiple, but you get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Capital Southwest (CSWC) Research Report: Q4 CY2025 Update

Business development company Capital Southwest (NASDAQ:CSWC) announced better-than-expected revenue in Q4 CY2025, with sales up 18.2% year on year to $61.45 million. Its GAAP profit of $0.54 per share was 8.2% below analysts’ consensus estimates.

Capital Southwest (CSWC) Q4 CY2025 Highlights:

- Revenue: $61.45 million vs analyst estimates of $58.36 million (18.2% year-on-year growth, 5.3% beat)

- Pre-tax Profit: $34.63 million (56.4% margin)

- EPS (GAAP): $0.54 vs analyst expectations of $0.59 (8.2% miss)

- Market Capitalization: $1.35 billion

Company Overview

Originally founded in 1961 as a venture capital investor that helped launch Texas Instruments, Capital Southwest (NASDAQ:CSWC) is a business development company that provides debt and equity financing to middle-market companies primarily in the United States.

Capital Southwest operates as an internally managed BDC (Business Development Company), a specialized type of investment firm regulated under the Investment Company Act of 1940. The company focuses on providing customized financing solutions to businesses with annual earnings between $3 million and $25 million—the middle market segment that often falls between traditional bank lending and larger institutional investment.

The firm's investment strategy centers on first lien senior secured debt, though it also provides second lien loans, subordinated debt, and occasionally makes equity co-investments. Capital Southwest typically invests between $5 million and $25 million per transaction across diverse industries including healthcare, business services, consumer products, and industrial manufacturing. A typical client might be a family-owned business seeking growth capital for expansion or a company requiring financing for an acquisition.

For example, a regional healthcare services provider might partner with Capital Southwest to secure $15 million in debt financing to acquire a complementary business, allowing them to expand their service offerings and geographic reach without diluting family ownership.

Capital Southwest generates revenue primarily through interest income on its debt investments and potential capital appreciation on equity positions. The company operates under BDC regulations that require it to distribute at least 90% of taxable income to shareholders, resulting in relatively high dividend yields compared to other financial stocks. As a publicly traded BDC, Capital Southwest provides retail and institutional investors access to private credit investments that would otherwise be unavailable to them.

4. Specialty Finance

Specialty finance companies provide targeted lending or financial services for specific industries or needs. They benefit from expertise in particular sectors, often reduced competition in specialized niches, and tailored underwriting that can yield higher margins. Challenges include concentration risk in specific industries, difficulty achieving scale efficiencies, and potential vulnerability during sector-specific downturns affecting their specialized markets.

Capital Southwest competes with other publicly traded business development companies including Ares Capital (NASDAQ:ARCC), Main Street Capital (NYSE:MAIN), and Golub Capital (NASDAQ:GBDC), as well as private credit funds managed by large asset managers.

5. Revenue Growth

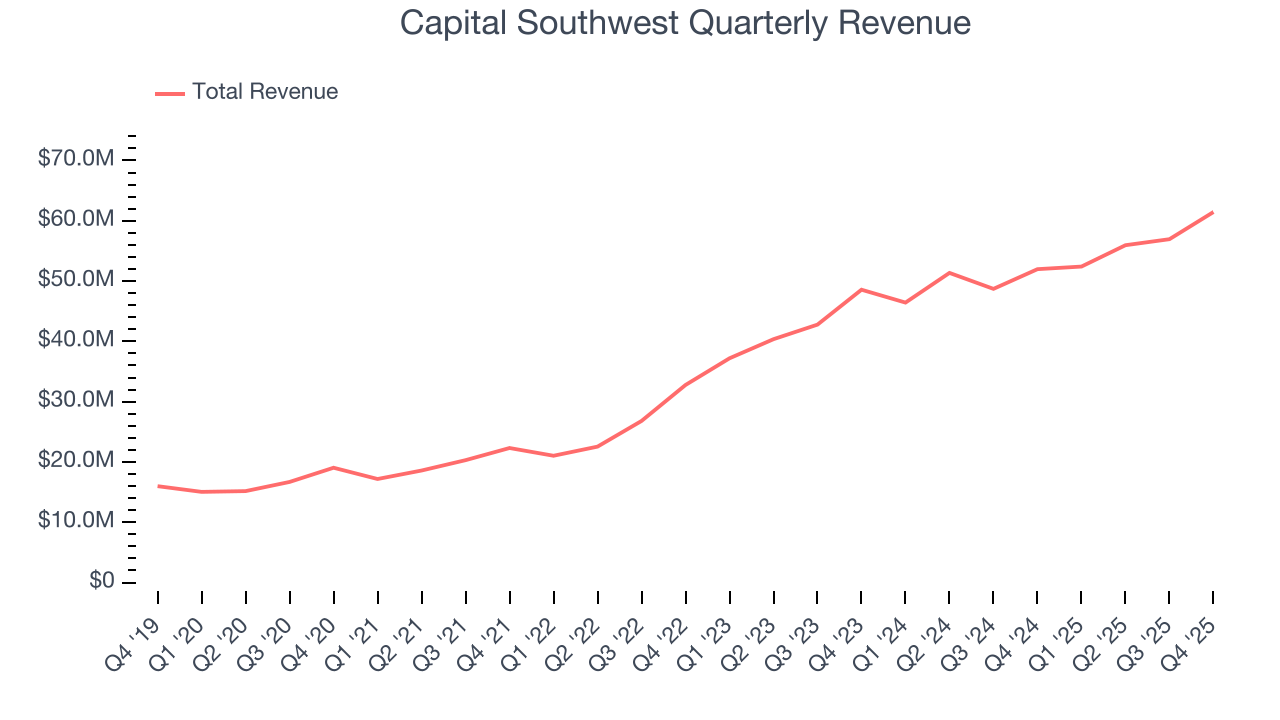

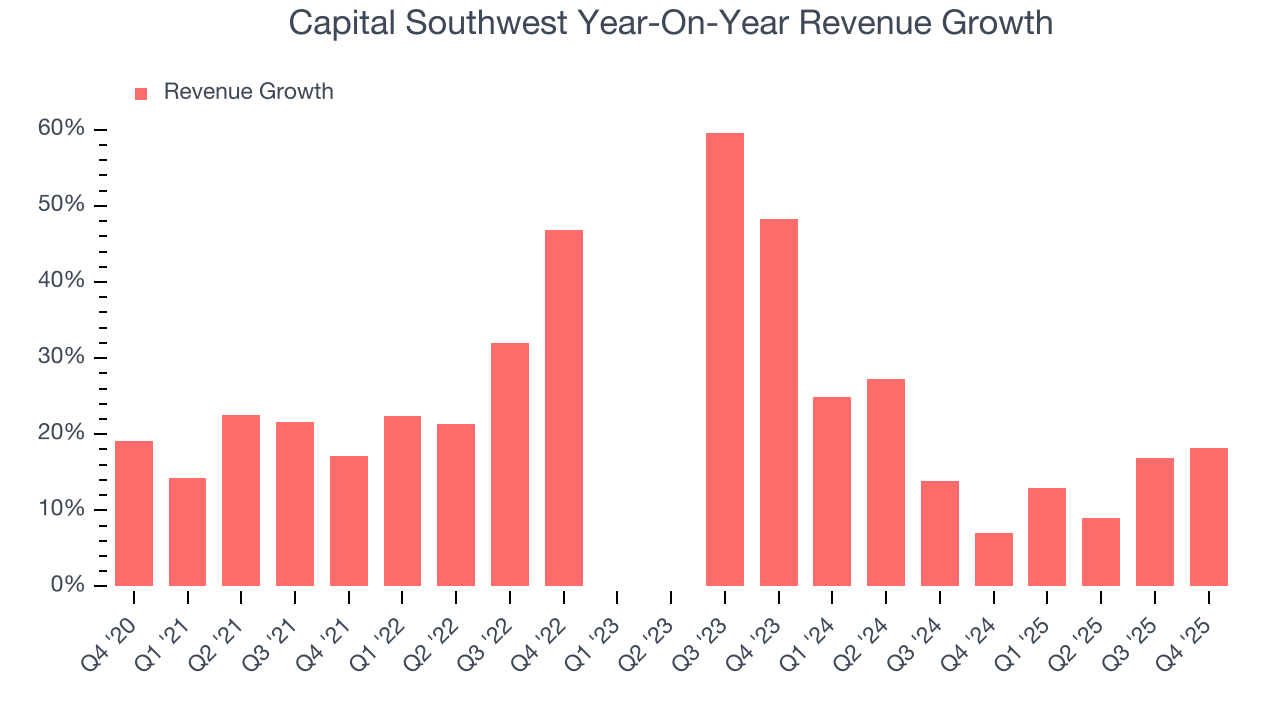

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Capital Southwest’s revenue grew at an incredible 28% compounded annual growth rate over the last five years. Its growth beat the average financials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Capital Southwest’s annualized revenue growth of 15.9% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Capital Southwest reported year-on-year revenue growth of 18.2%, and its $61.45 million of revenue exceeded Wall Street’s estimates by 5.3%.

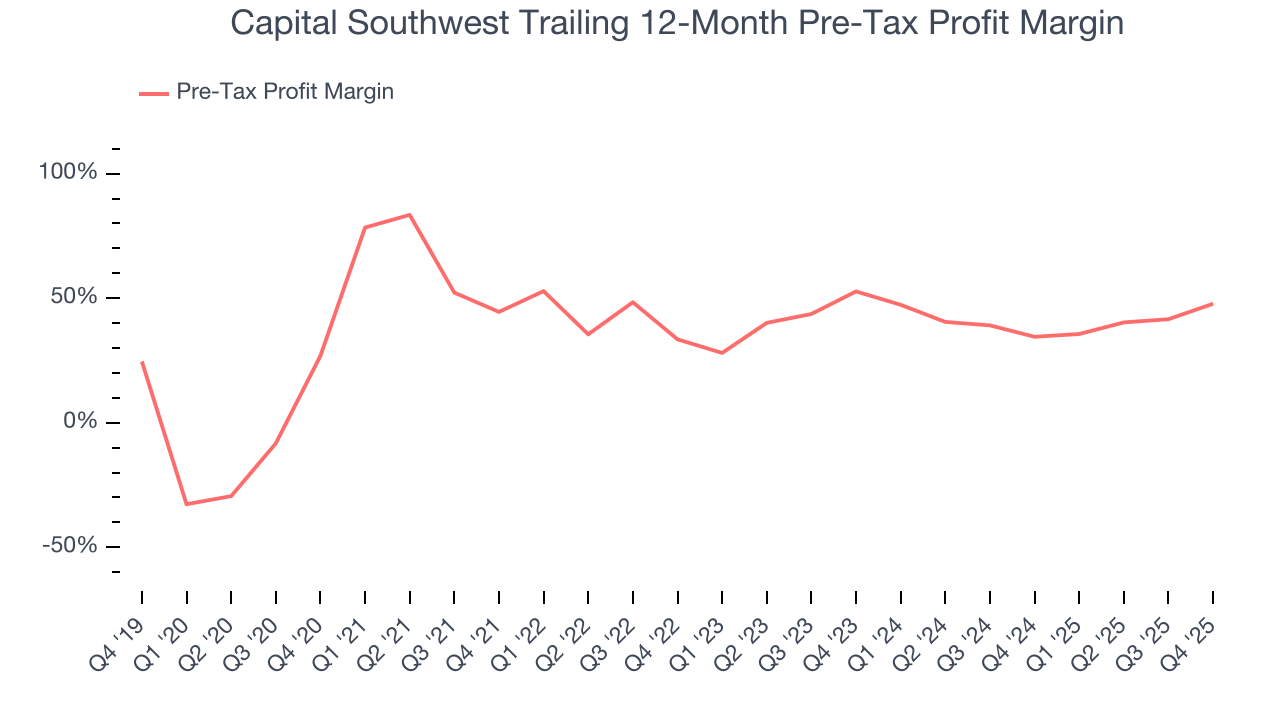

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Specialty Finance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last five years, Capital Southwest’s pre-tax profit margin has fallen by 20.9 percentage points, going from 44.5% to 47.8%. However, the company gave back some of its expense savings as its pre-tax profit margin declined by 4.9 percentage points on a two-year basis.

Capital Southwest’s pre-tax profit margin came in at 56.4% this quarter. This result was 24.4 percentage points better than the same quarter last year.

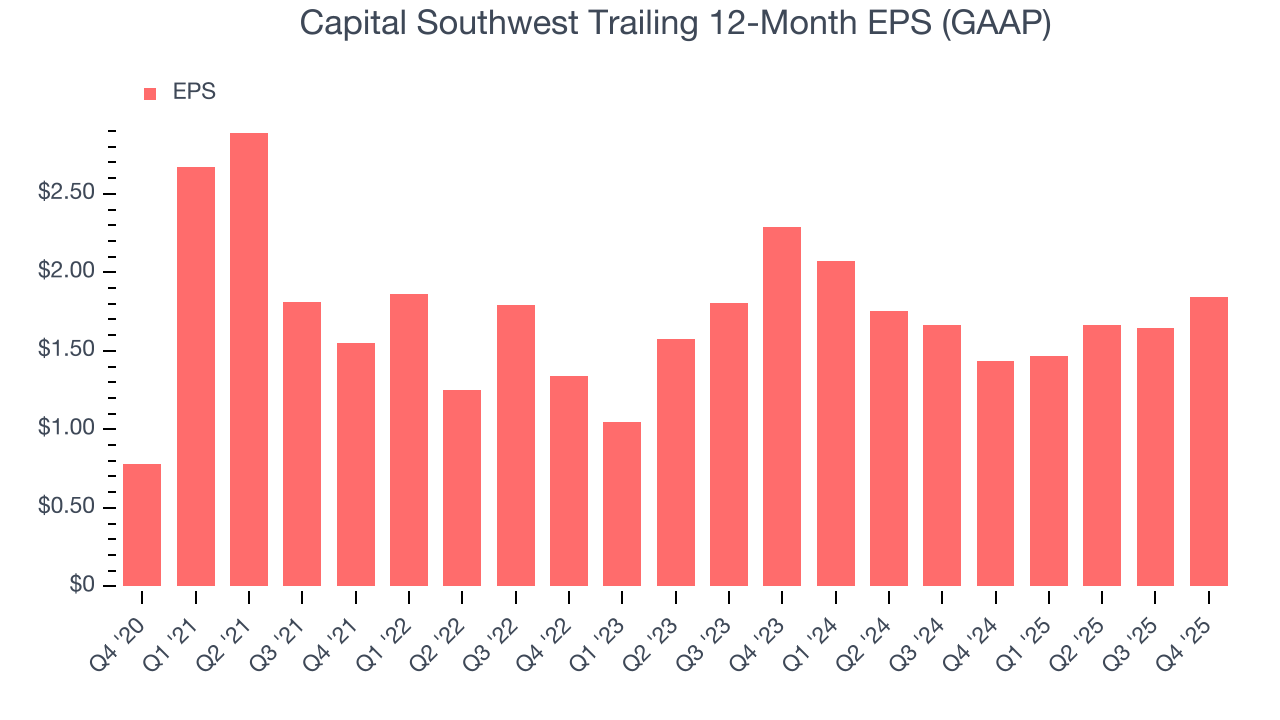

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Capital Southwest’s EPS grew at a remarkable 18.8% compounded annual growth rate over the last five years. Despite its pre-tax profit margin improvement during that time, this performance was lower than its 28% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Capital Southwest, its two-year annual EPS declines of 10.2% mark a reversal from its (seemingly) healthy five-year trend. We hope Capital Southwest can return to earnings growth in the future.

In Q4, Capital Southwest reported EPS of $0.54, up from $0.34 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Capital Southwest’s full-year EPS of $1.85 to grow 19.5%.

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Capital Southwest has averaged an ROE of 10.1%, respectable for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired.

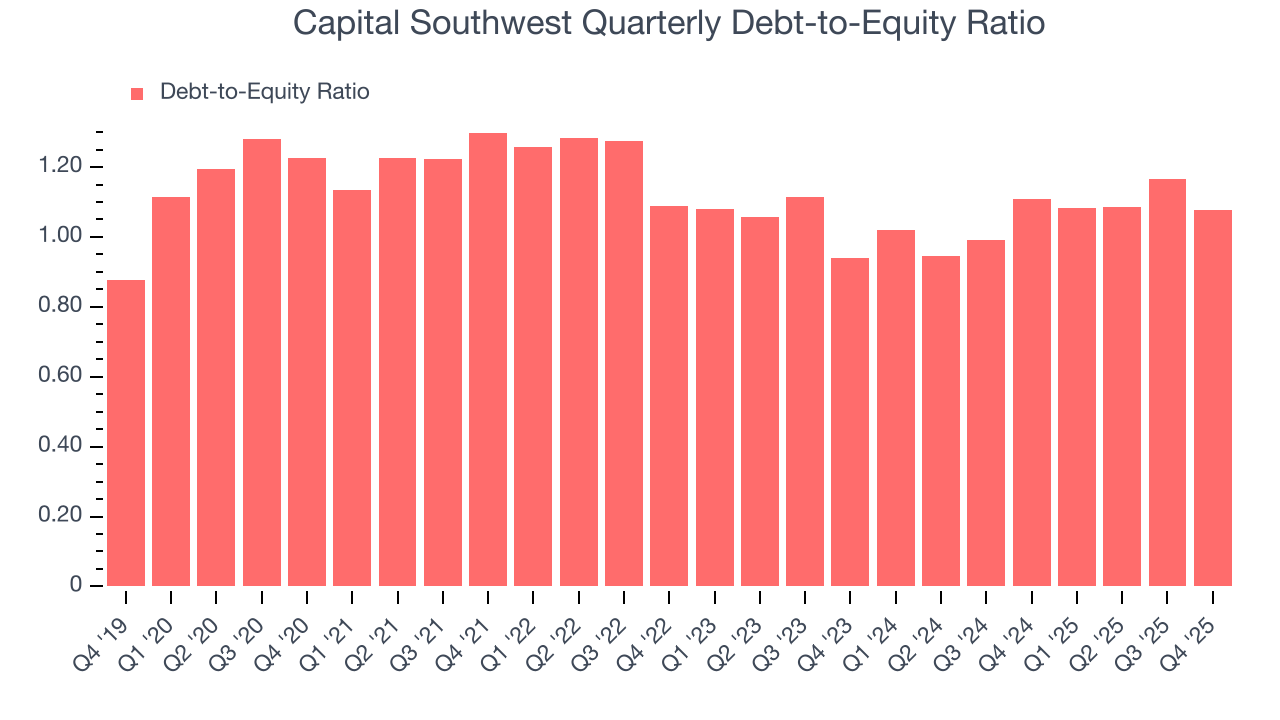

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Capital Southwest currently has $1.07 billion of debt and $995.6 million of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 1.1×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from Capital Southwest’s Q4 Results

We enjoyed seeing Capital Southwest beat analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The stock traded up 1.9% to $23.61 immediately after reporting.

11. Is Now The Time To Buy Capital Southwest?

Updated: March 27, 2026 at 12:42 AM EDT

When considering an investment in Capital Southwest, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Capital Southwest’s business quality ultimately falls short of our standards. Although its revenue growth was exceptional over the last five years, it’s expected to deteriorate over the next 12 months and its unimpressive EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders.

Capital Southwest’s P/E ratio based on the next 12 months is 9.7x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $24.40 on the company (compared to the current share price of $21.91).