Five9 (FIVN)

Five9 faces an uphill battle. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think Five9 Will Underperform

Taking its name from the "five nines" (99.999%) standard for optimal service reliability in telecommunications, Five9 (NASDAQ:FIVN) provides cloud-based software that enables businesses to run their contact centers with tools for customer service, sales, and marketing across multiple communication channels.

- Sky-high servicing costs result in an inferior gross margin of 55.2% that must be offset through increased usage

- Offerings struggled to generate meaningful interest as its average billings growth of 9.1% over the last year did not impress

- Estimated sales growth of 9.3% for the next 12 months implies demand will slow from its two-year trend

Five9’s quality is insufficient. There are better opportunities in the market.

Why There Are Better Opportunities Than Five9

Five9’s stock price of $15.70 implies a valuation ratio of 1.1x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Five9 (FIVN) Research Report: Q4 CY2025 Update

Cloud contact center software provider Five9 (NASDAQ:FIVN) announced better-than-expected revenue in Q4 CY2025, with sales up 7.8% year on year to $300.3 million. The company expects next quarter’s revenue to be around $299.5 million, close to analysts’ estimates. Its non-GAAP profit of $0.80 per share was 1.9% above analysts’ consensus estimates.

Five9 (FIVN) Q4 CY2025 Highlights:

- Revenue: $300.3 million vs analyst estimates of $298.2 million (7.8% year-on-year growth, 0.7% beat)

- Adjusted EPS: $0.80 vs analyst estimates of $0.78 (1.9% beat)

- Adjusted Operating Income: $61.62 million vs analyst estimates of $58.44 million (20.5% margin, 5.4% beat)

- Revenue Guidance for Q1 CY2026 is $299.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.18 at the midpoint, in line with analyst estimates

- Operating Margin: 6.6%, up from 1.5% in the same quarter last year

- Free Cash Flow Margin: 22.4%, up from 13.4% in the previous quarter

- Market Capitalization: $1.31 billion

Company Overview

Taking its name from the "five nines" (99.999%) standard for optimal service reliability in telecommunications, Five9 (NASDAQ:FIVN) provides cloud-based software that enables businesses to run their contact centers with tools for customer service, sales, and marketing across multiple communication channels.

Five9's Virtual Contact Center (VCC) platform allows organizations to manage customer interactions across voice, chat, email, web, social media, and mobile channels from a single unified system in the cloud. Unlike traditional on-premise contact center systems that require significant hardware investments and lengthy implementations, Five9's solution can be deployed rapidly with minimal upfront costs, allowing companies to quickly scale agent seats up or down based on business needs.

The company's platform incorporates artificial intelligence capabilities including Interactive Virtual Agents (IVAs) that can handle routine customer inquiries, Agent Assist technology that provides real-time guidance to human agents, and AI-powered analytics that deliver insights into customer interactions. Five9 also offers Workforce Engagement Management tools to optimize agent scheduling and performance.

A healthcare provider might use Five9 to route patient calls to the appropriate department, offer appointment scheduling through automated systems, and provide agents with instant access to patient records through CRM integrations. For retail clients, the platform can enable seamless customer support across phone, email, and social media while tracking purchase history.

Five9 generates recurring revenue through a subscription model based primarily on the number of agent seats and usage minutes, plus additional fees for specific functionalities like virtual agents or advanced analytics.

4. Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

Five9 competes with legacy on-premise contact center system providers like Avaya and Cisco Systems, cloud contact center software providers such as Genesys and NICE, smaller specialists like Content Guru and Talkdesk, and technology giants including Amazon, Twilio, and Microsoft that offer contact center development tools.

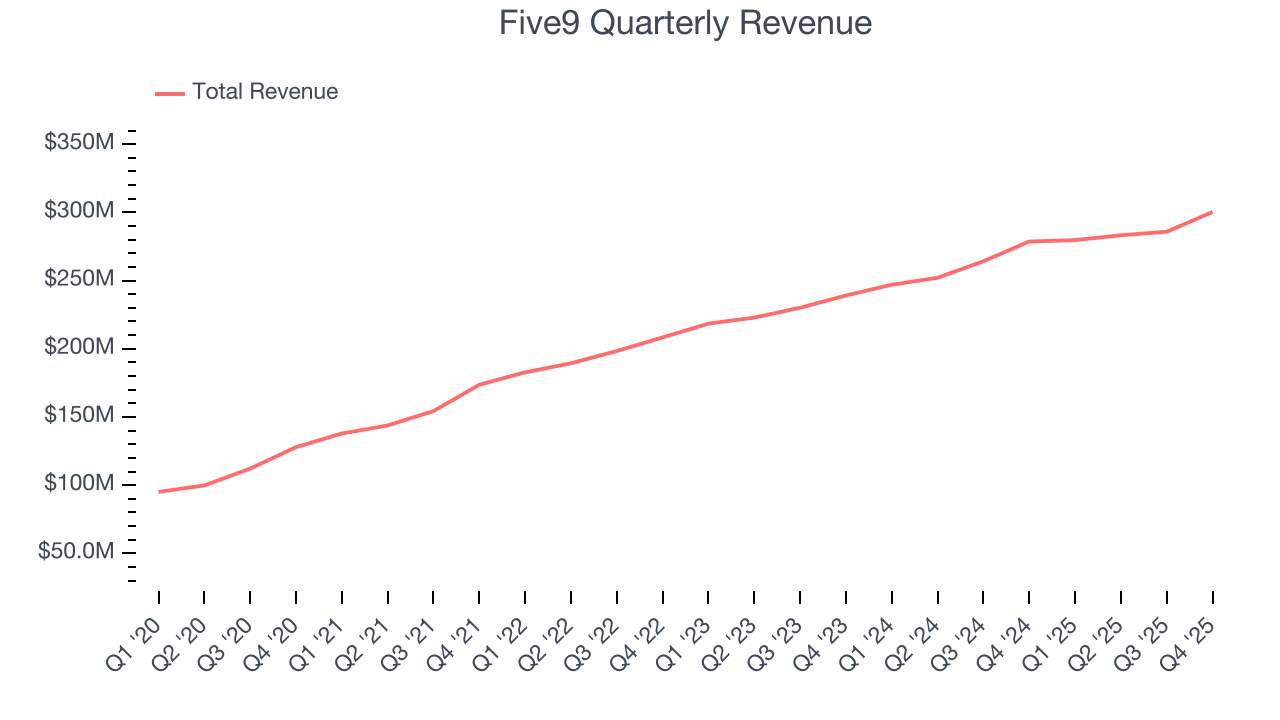

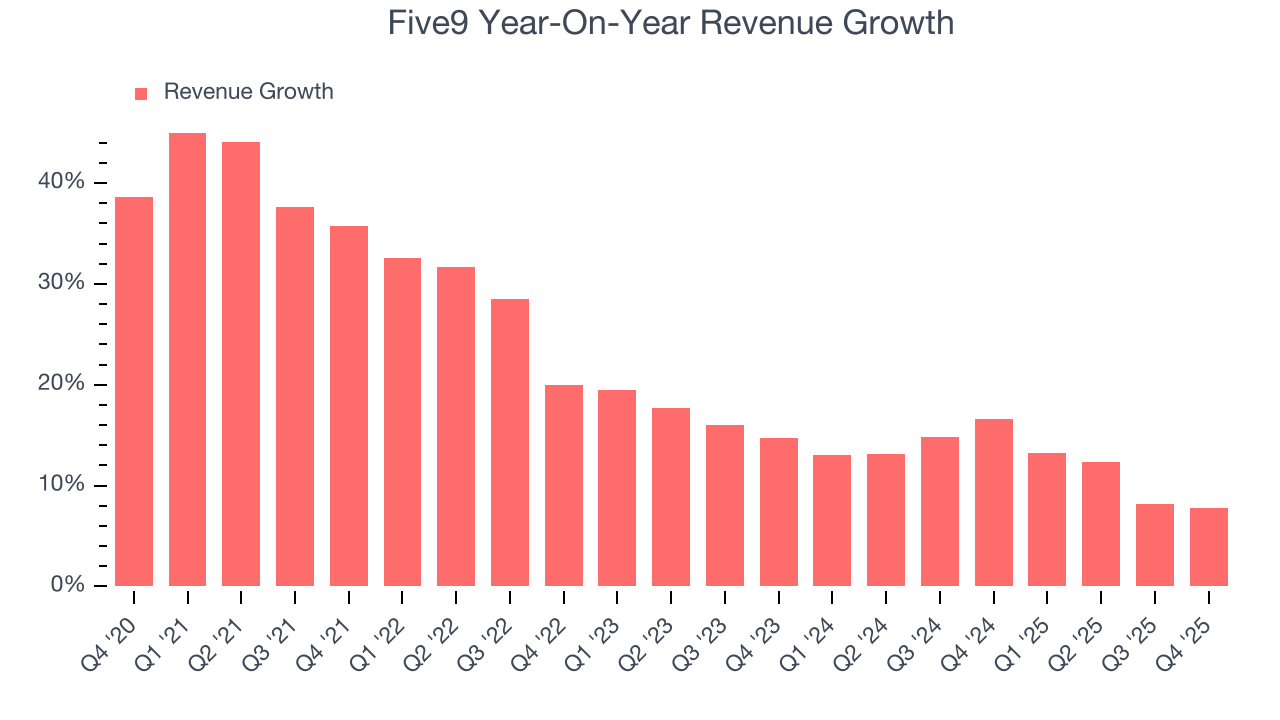

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Five9 grew its sales at a decent 21.4% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Five9’s recent performance shows its demand has slowed as its annualized revenue growth of 12.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Five9 reported year-on-year revenue growth of 7.8%, and its $300.3 million of revenue exceeded Wall Street’s estimates by 0.7%. Company management is currently guiding for a 7.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.2% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

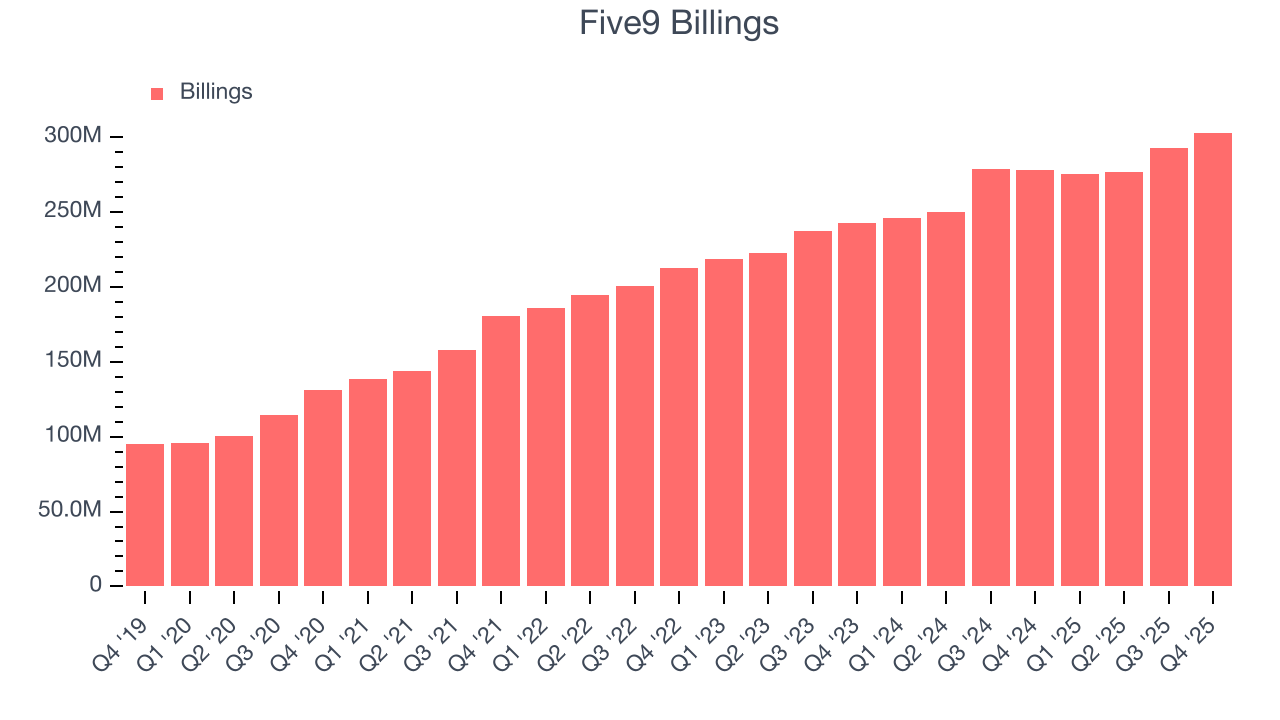

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Five9’s billings came in at $303.1 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 9.1% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Five9 to acquire new customers as its CAC payback period checked in at 175.2 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

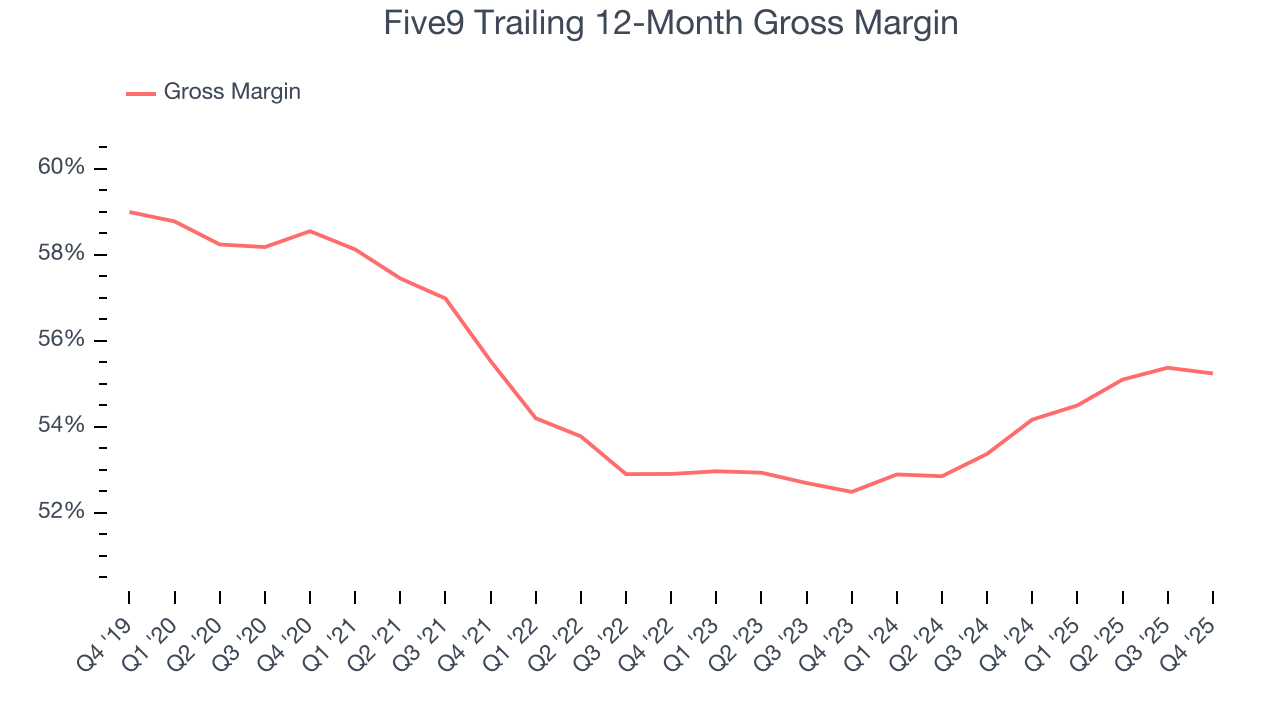

8. Gross Margin & Pricing Power

For software companies like Five9, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Five9’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 55.2% gross margin over the last year. That means Five9 paid its providers a lot of money ($44.76 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Five9 has seen gross margins improve by 2.8 percentage points over the last 2 year, which is very good in the software space.

Five9 produced a 55.4% gross profit margin in Q4, in line with the same quarter last year. Zooming out, Five9’s full-year margin has been trending up over the past 12 months, increasing by 1.1 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

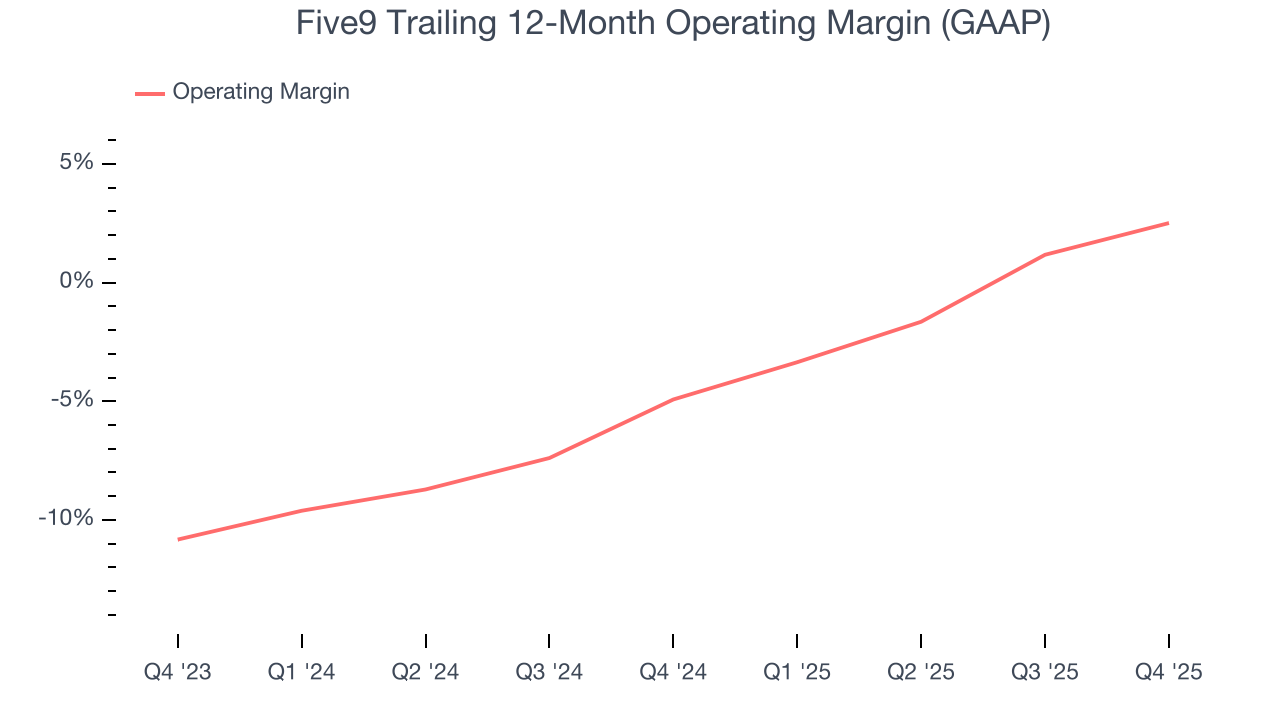

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Five9 has done a decent job managing its cost base over the last year. The company has produced an average operating margin of 2.5%, higher than the broader software sector.

Analyzing the trend in its profitability, Five9’s operating margin rose by 7.4 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Five9 generated an operating margin profit margin of 6.6%, up 5.1 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

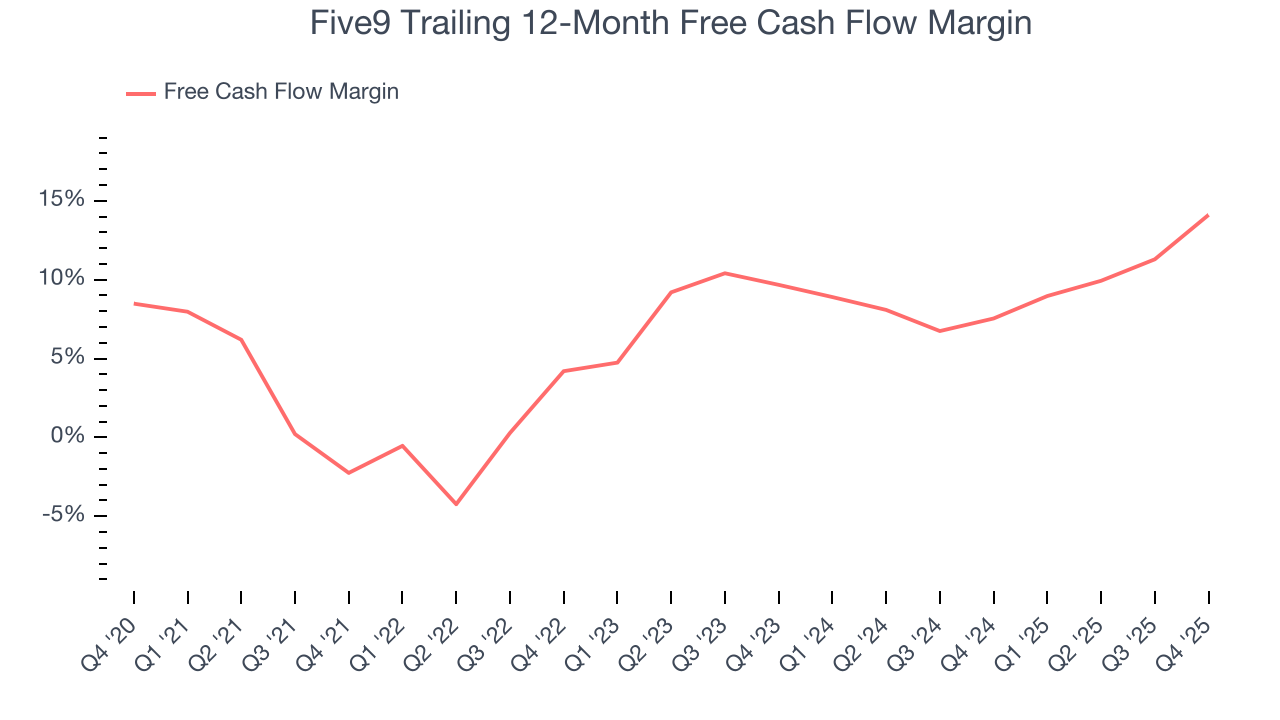

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Five9 has shown mediocre cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 14.1%, subpar for a software business.

Five9’s free cash flow clocked in at $67.31 million in Q4, equivalent to a 22.4% margin. This result was good as its margin was 10.7 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts’ consensus estimates show they’re expecting Five9’s free cash flow margin of 14.1% for the last 12 months to remain the same.

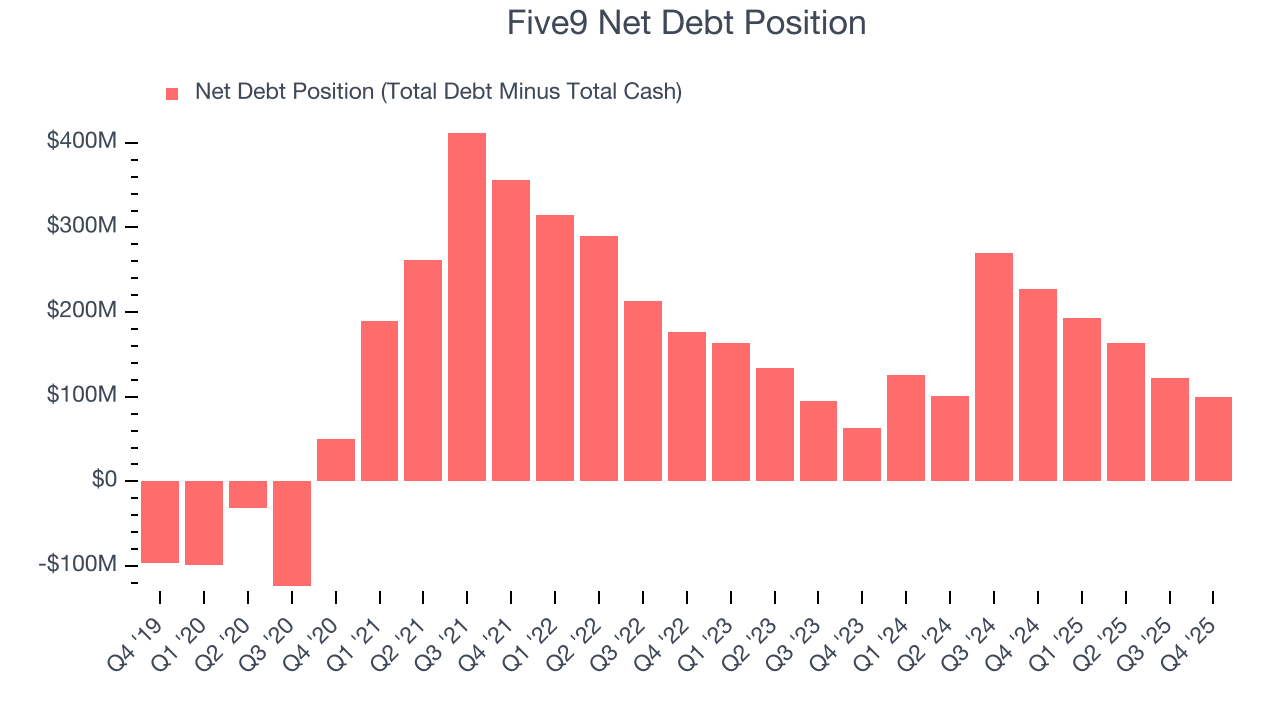

11. Balance Sheet Assessment

Five9 reported $696.9 million of cash and $796.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $269.7 million of EBITDA over the last 12 months, we view Five9’s 0.4× net-debt-to-EBITDA ratio as safe. We also see its $9.80 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Five9’s Q4 Results

We were impressed by how significantly Five9 blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 2.7% to $17.63 immediately following the results.

13. Is Now The Time To Buy Five9?

Updated: March 22, 2026 at 10:15 PM EDT

Are you wondering whether to buy Five9 or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

We cheer for all companies solving complex business issues, but in the case of Five9, we’ll be cheering from the sidelines. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its gross margins show its business model is much less lucrative than other companies. And while the company’s operating margins are in line with the overall software sector, the downside is its ARR has disappointed and shows the company is having difficulty retaining customers and their spending.

Five9’s price-to-sales ratio based on the next 12 months is 1.1x. This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $27.24 on the company (compared to the current share price of $15.70).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.