Lincoln Electric (LECO)

Lincoln Electric doesn’t excite us. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Lincoln Electric Is Not Exciting

Headquartered in Ohio, Lincoln Electric (NASDAQ:LECO) manufactures and sells welding equipment for various industries.

- Organic revenue growth fell short of our benchmarks over the past two years and implies it may need to improve its products, pricing, or go-to-market strategy

- Estimated sales growth of 6.4% for the next 12 months is soft and implies weaker demand

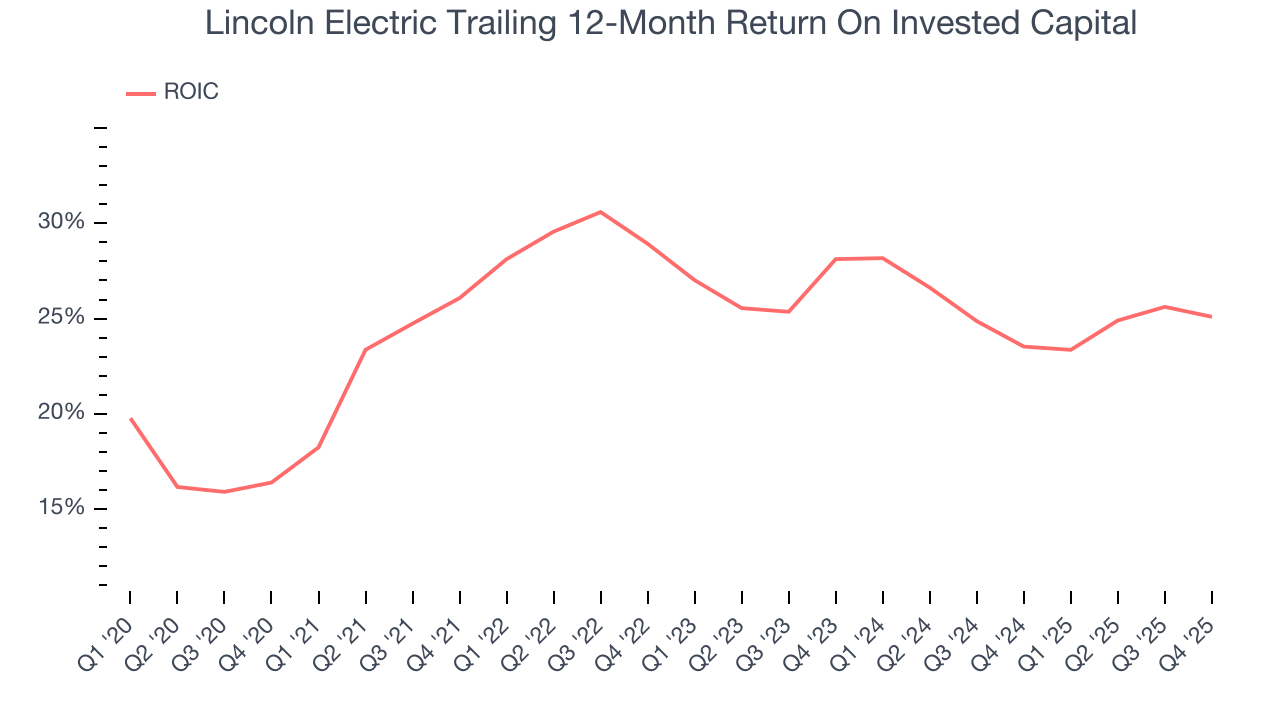

- A positive is that its industry-leading 26.3% return on capital demonstrates management’s skill in finding high-return investments

Lincoln Electric doesn’t fulfill our quality requirements. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Lincoln Electric

Lincoln Electric is trading at $267.30 per share, or 24.6x forward P/E. This multiple expensive for its subpar fundamentals.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Lincoln Electric (LECO) Research Report: Q4 CY2025 Update

Welding equipment manufacturer Lincoln Electric (NASDAQ:LECO) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 5.5% year on year to $1.08 billion. Its non-GAAP profit of $2.65 per share was 4.2% above analysts’ consensus estimates.

Lincoln Electric (LECO) Q4 CY2025 Highlights:

- Revenue: $1.08 billion vs analyst estimates of $1.09 billion (5.5% year-on-year growth, 1.5% miss)

- Adjusted EPS: $2.65 vs analyst estimates of $2.54 (4.2% beat)

- Adjusted EBITDA: $209.9 million vs analyst estimates of $217.3 million (19.5% margin, 3.4% miss)

- Operating Margin: 17.1%, in line with the same quarter last year

- Free Cash Flow Margin: 4.8%, down from 6.4% in the same quarter last year

- Organic Revenue rose 2.5% year on year (miss)

- Market Capitalization: $15.99 billion

Company Overview

Headquartered in Ohio, Lincoln Electric (NASDAQ:LECO) manufactures and sells welding equipment for various industries.

Lincoln Electric was established with an initial investment of $200, aimed at developing a unique electric motor for industrial uses. This small venture quickly evolved as the Lincoln brothers, John C. and James F., introduced their first variable voltage arc welder in 1911. This product marked the beginning of Lincoln Electric's journey into welding technology, where it has become a prominent player.

Lincoln Electric’s product line encompasses arc welding equipment, consumable welding products, and other cutting and joining solutions. The company's vast products include everything from basic arc welding power sources used in light manufacturing and maintenance to sophisticated robotic applications for high-volume production welding and fabrication. Lincoln Electric also produces a variety of consumables for arc welding, such as coated manual electrodes, solid wires for continuous feed in mechanized welding, and cored wires also used in mechanized settings. Additionally, under The Harris Products Group, Lincoln Electric offers solutions to the cutting, soldering, and brazing sectors, offering specialized gas equipment.

Lincoln Electric's products are predominantly sold through industrial distributors and retailers in the Americas, while outside this region, an international sales force and agents handle distribution. The company serves a wide array of end-user markets including general fabrication, energy, heavy industries, automotive and transportation, and construction and infrastructure.

Lincoln Electric's revenue streams primarily derive from the sale of its welding and cutting equipment, consumables, and associated accessories. Beyond initial equipment sales, Lincoln Electric benefits from recurring revenue sources including the sale of replacement parts and consumables, such as welding wires and electrodes. These consumables are essential to ongoing welding operations, ensuring a steady demand and continuous revenue flow. The revenue from Lincoln Electric's operations is closely tied to industrial production trends and steel consumption. These factors directly impact the demand for welding and cutting solutions, as they influence project volumes and the need for infrastructure development and maintenance.

Lincoln Electric uses a strategic acquisition strategy to enhance its market position, expand its product portfolio, and tap into new customer demographics. A prime example of this strategy is the acquisition of Air Liquide Welding in 2017, which significantly strengthened Lincoln Electric's presence in the European market and broadened its offerings in the global welding industry.

4. Professional Tools and Equipment

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Illinois Tool Works (NYSE:ITW), Colfax (NYSE:CFX), and Fronius (private).

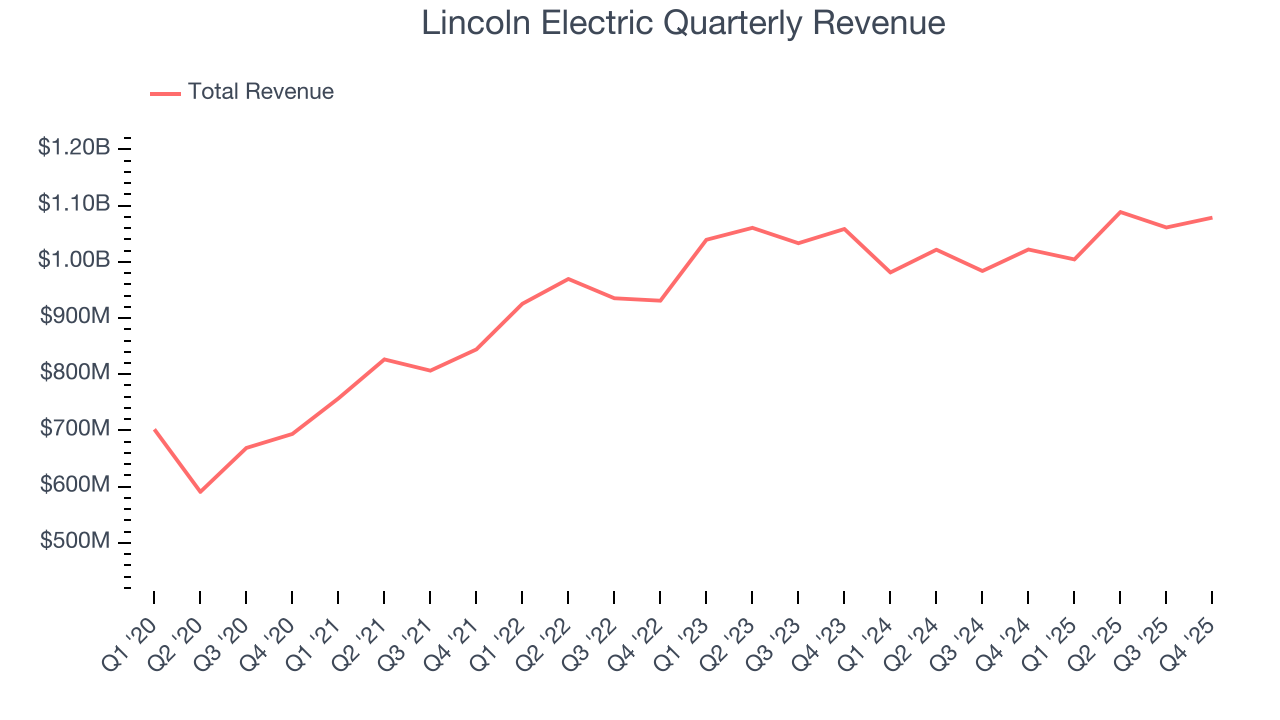

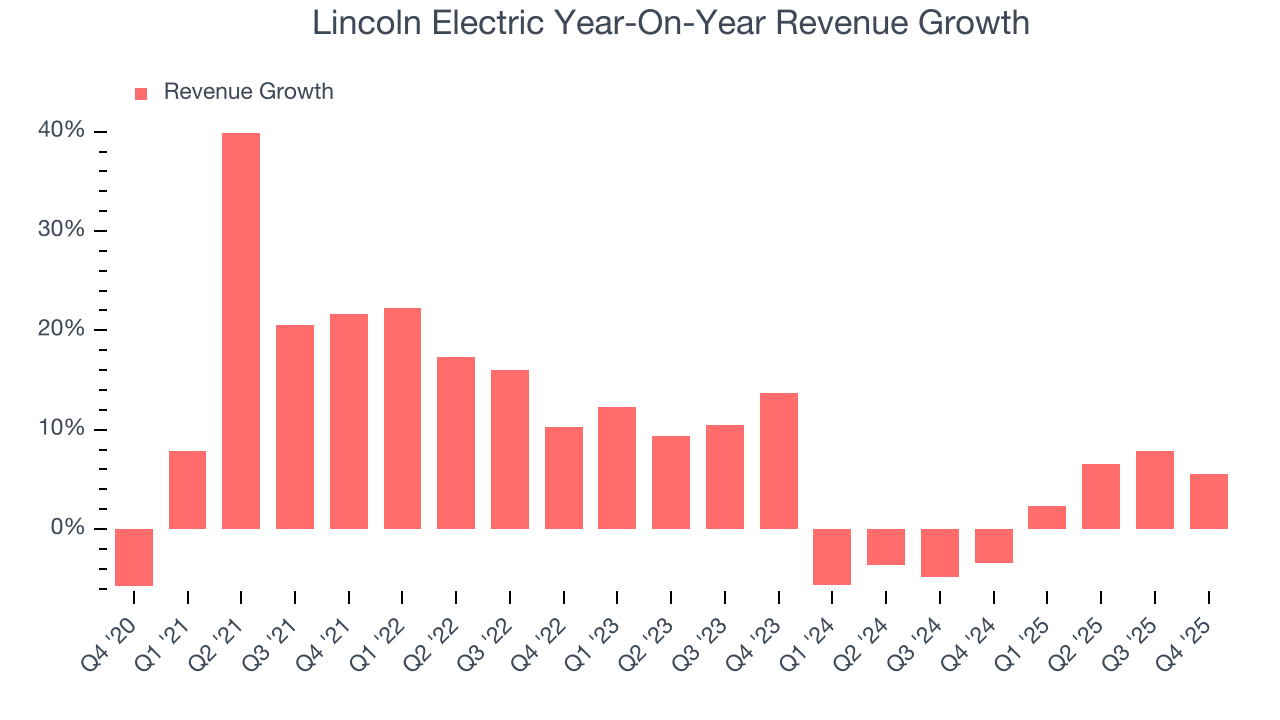

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Lincoln Electric grew its sales at a solid 9.8% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Lincoln Electric’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

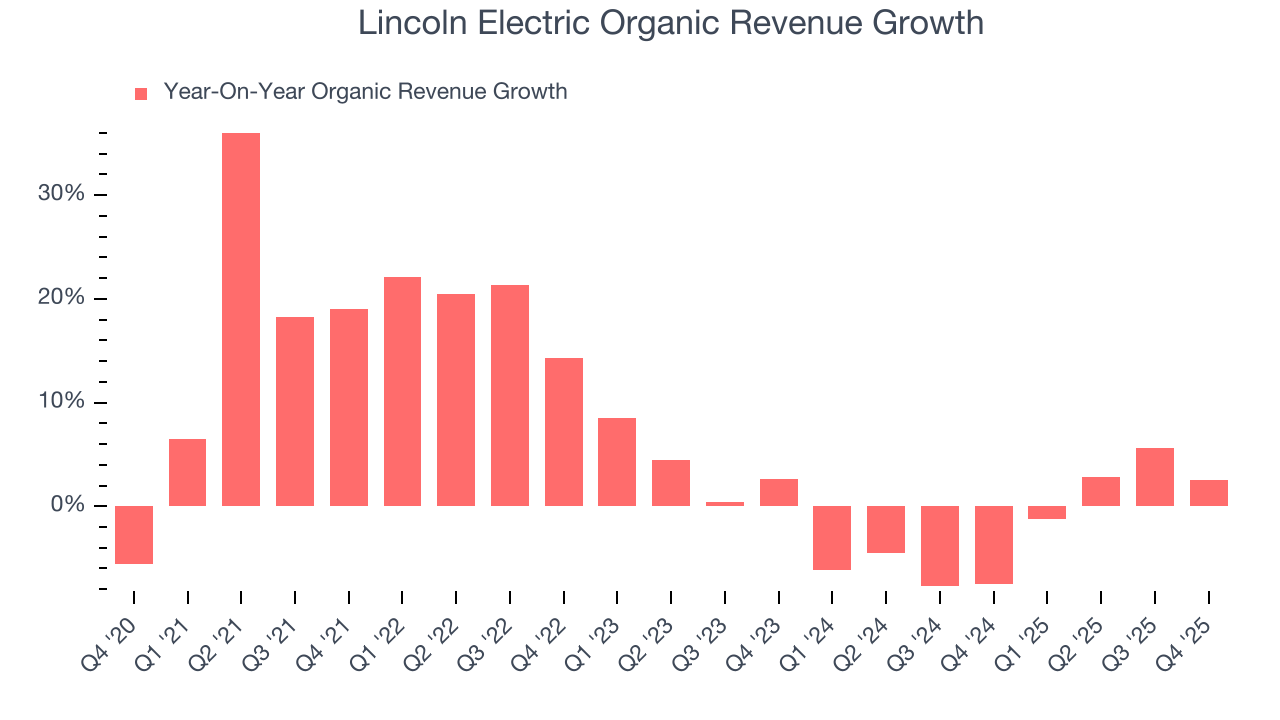

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Lincoln Electric’s organic revenue averaged 2% year-on-year declines. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Lincoln Electric’s revenue grew by 5.5% year on year to $1.08 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.1% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

6. Gross Margin & Pricing Power

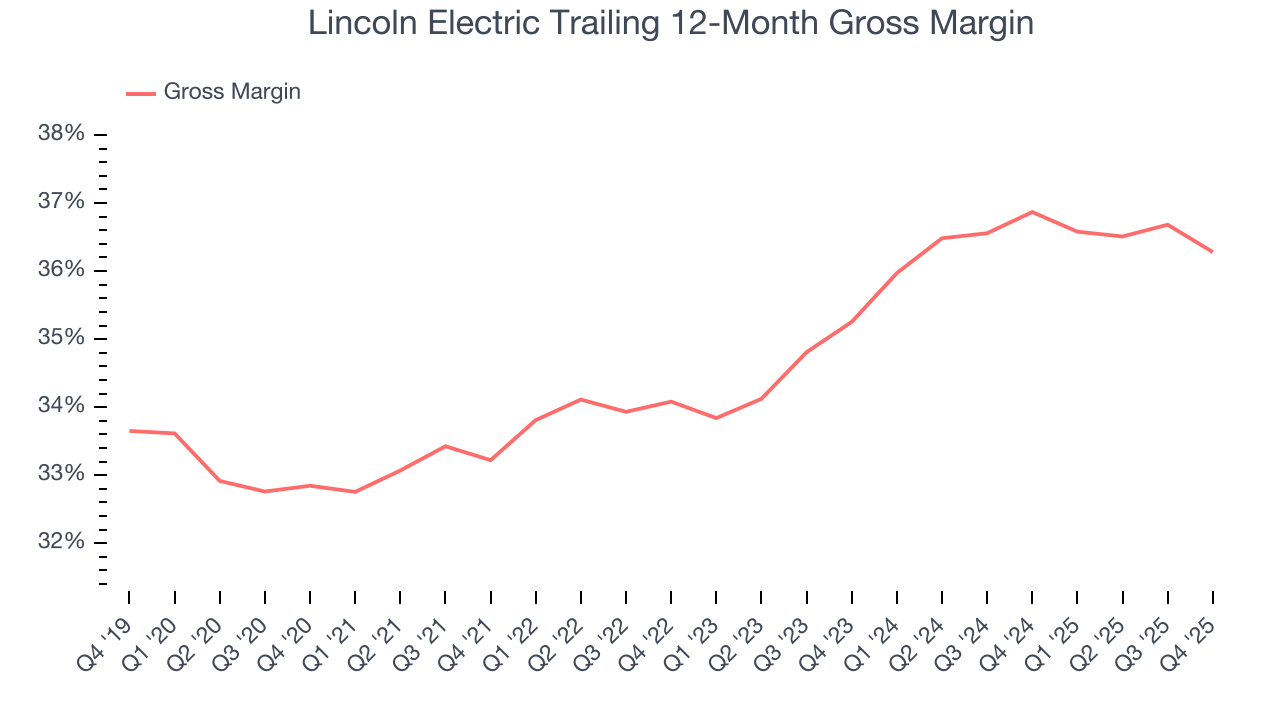

Lincoln Electric’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 35.2% gross margin over the last five years. Said differently, Lincoln Electric paid its suppliers $64.76 for every $100 in revenue.

In Q4, Lincoln Electric produced a 34.7% gross profit margin , marking a 1.6 percentage point decrease from 36.2% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

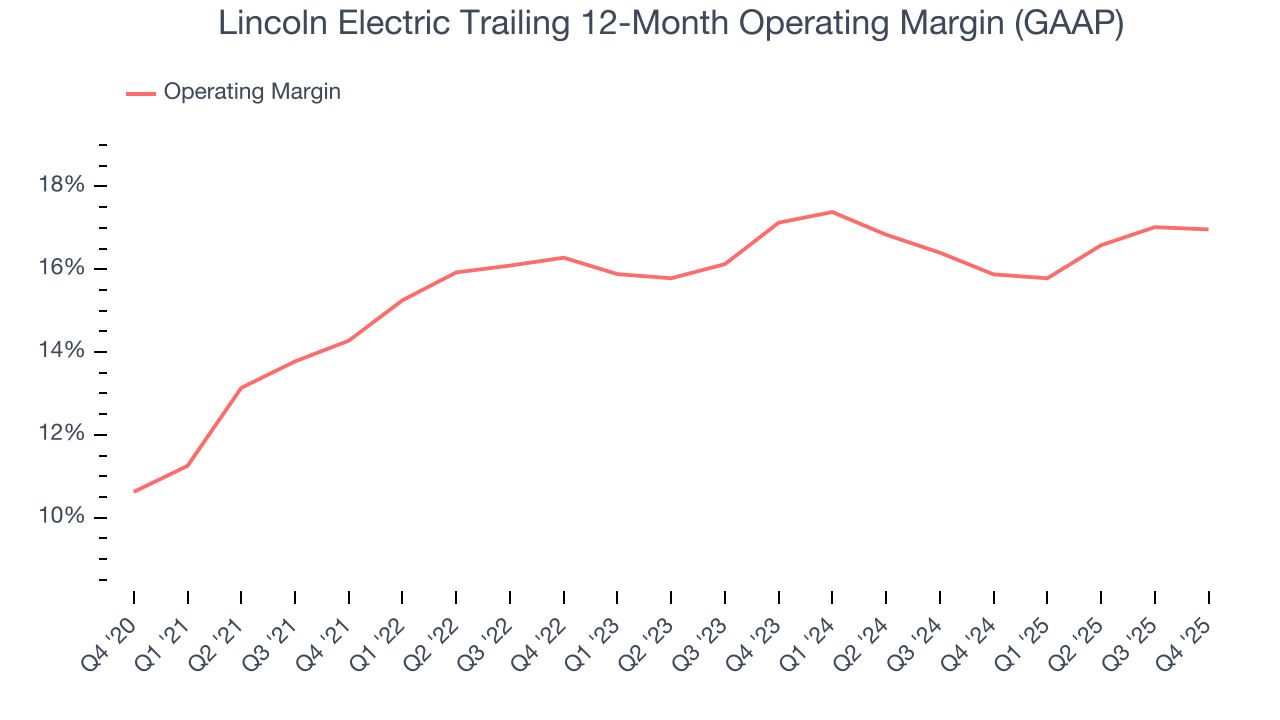

7. Operating Margin

Lincoln Electric has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.2%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Lincoln Electric’s operating margin rose by 2.7 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, Lincoln Electric generated an operating margin profit margin of 17.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

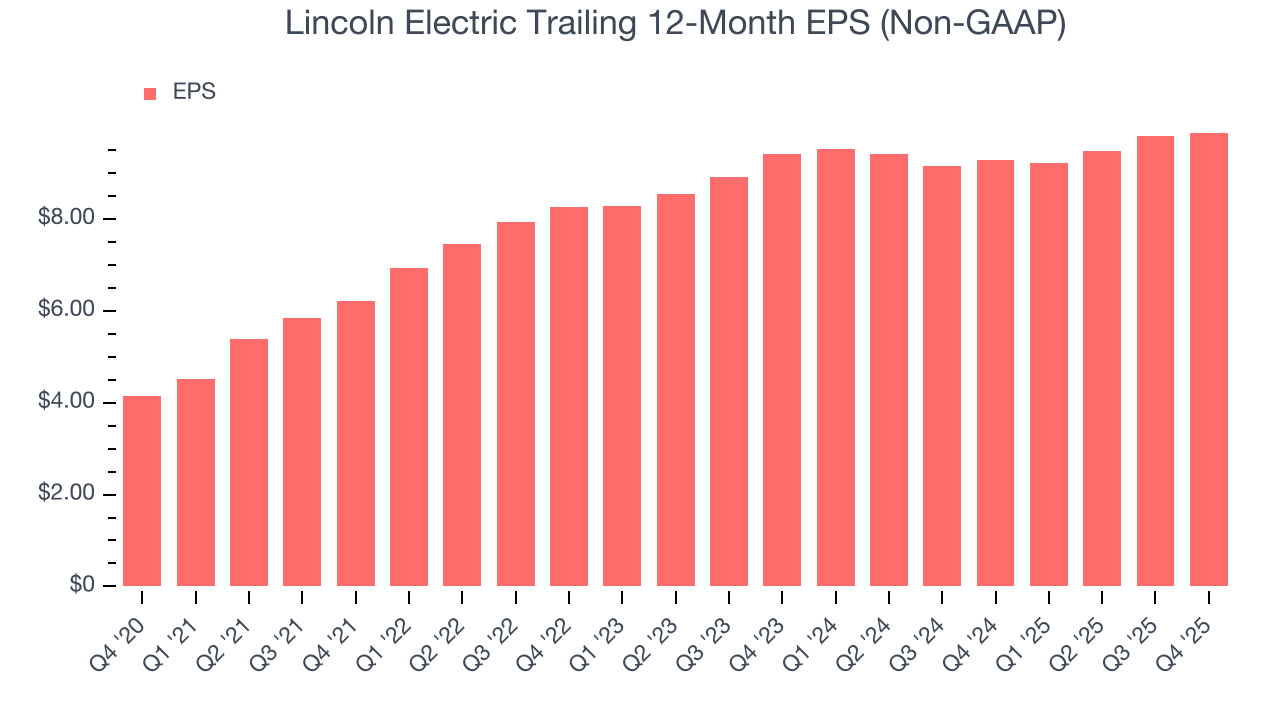

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Lincoln Electric’s EPS grew at an astounding 19% compounded annual growth rate over the last five years, higher than its 9.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

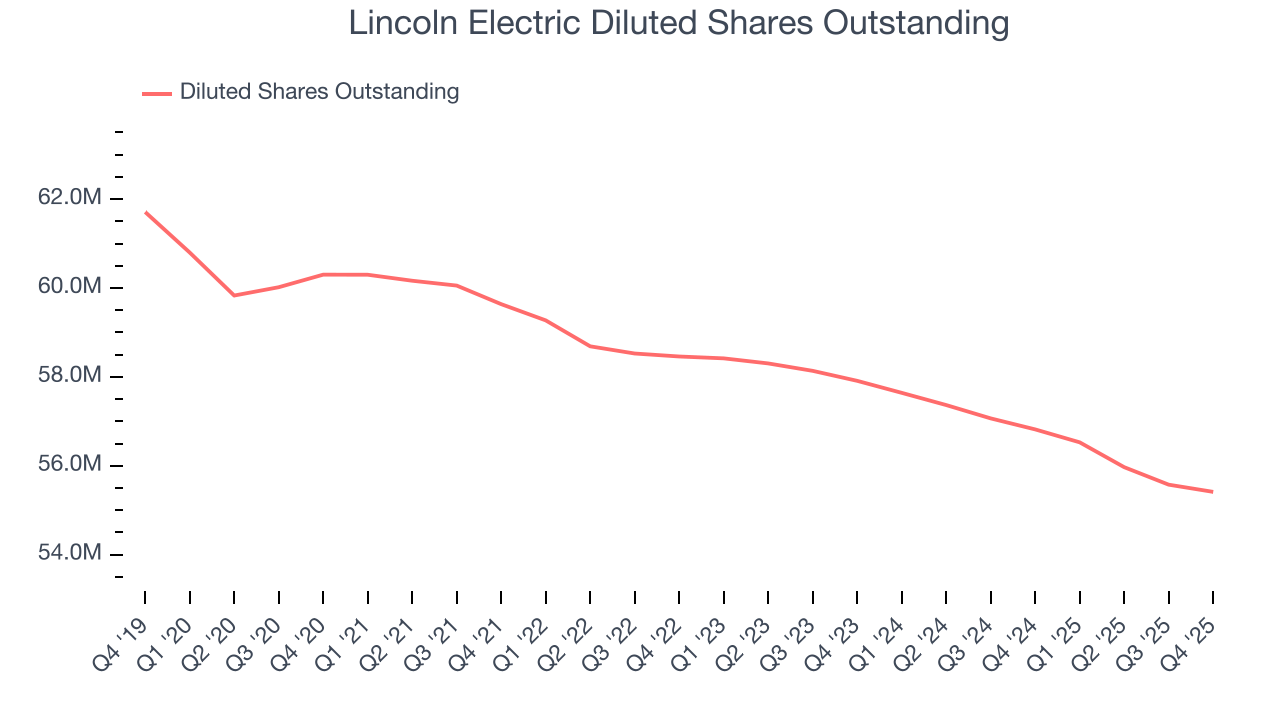

We can take a deeper look into Lincoln Electric’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Lincoln Electric’s operating margin was flat this quarter but expanded by 2.7 percentage points over the last five years. On top of that, its share count shrank by 8.1%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Lincoln Electric, its two-year annual EPS growth of 2.4% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Lincoln Electric reported adjusted EPS of $2.65, up from $2.57 in the same quarter last year. This print beat analysts’ estimates by 4.2%. Over the next 12 months, Wall Street expects Lincoln Electric’s full-year EPS of $9.88 to grow 9.8%.

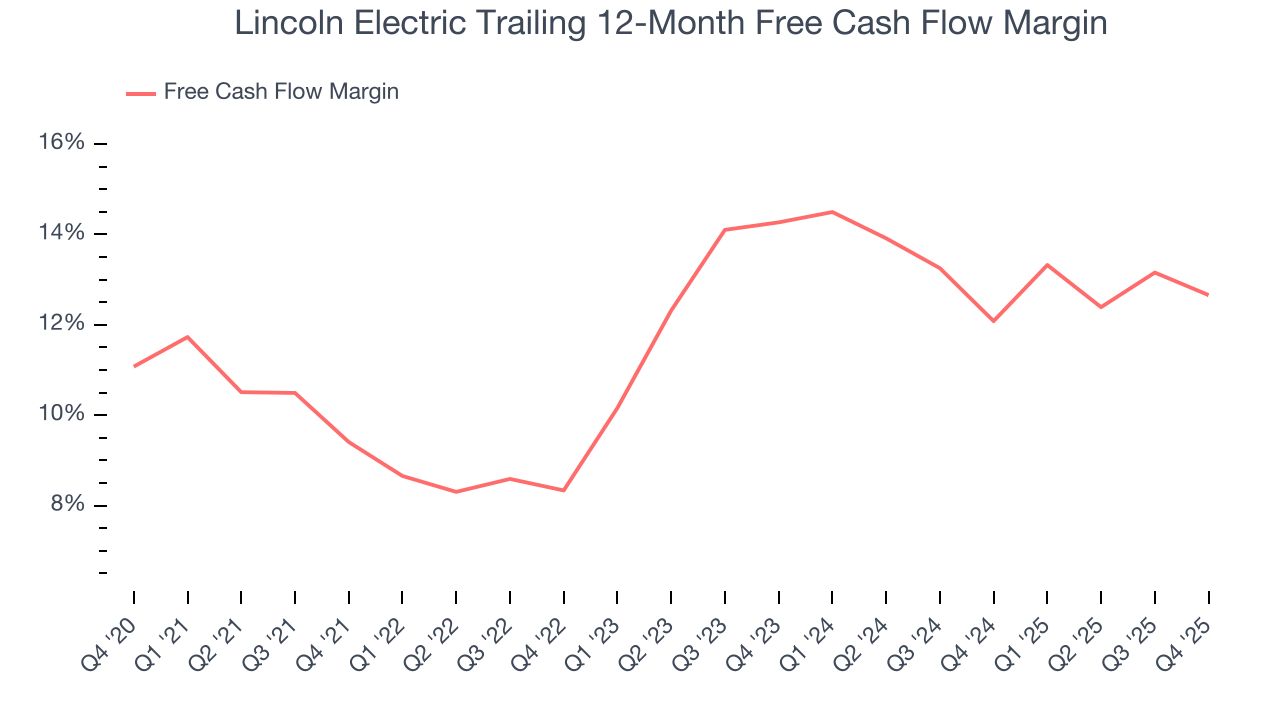

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Lincoln Electric has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 11.5% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Lincoln Electric’s margin expanded by 3.3 percentage points during that time. This is encouraging because it gives the company more optionality.

Lincoln Electric’s free cash flow clocked in at $52.02 million in Q4, equivalent to a 4.8% margin. The company’s cash profitability regressed as it was 1.6 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Lincoln Electric hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 26.3%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Lincoln Electric’s ROIC averaged 3.2 percentage point decreases each year. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

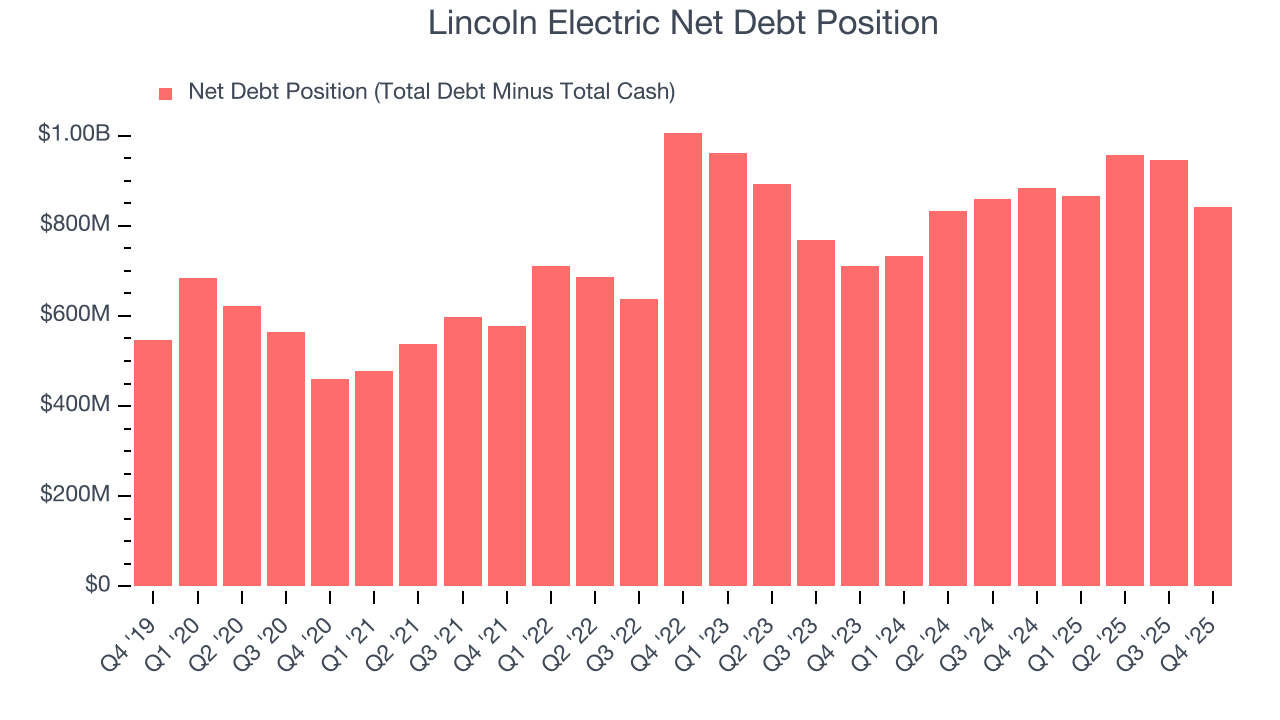

11. Balance Sheet Assessment

Lincoln Electric reported $308.8 million of cash and $1.15 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $832 million of EBITDA over the last 12 months, we view Lincoln Electric’s 1.0× net-debt-to-EBITDA ratio as safe. We also see its $25.23 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Lincoln Electric’s Q4 Results

It was good to see Lincoln Electric beat analysts’ EPS expectations this quarter. On the other hand, its organic revenue missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $290.27 immediately after reporting.

13. Is Now The Time To Buy Lincoln Electric?

Updated: March 11, 2026 at 10:57 PM EDT

Before investing in or passing on Lincoln Electric, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Lincoln Electric’s business quality ultimately falls short of our standards. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its organic revenue declined. And while the company’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its diminishing returns show management's prior bets haven't worked out.

Lincoln Electric’s P/E ratio based on the next 12 months is 24.6x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $308.30 on the company (compared to the current share price of $267.30).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.