Option Care Health (OPCH)

We’re not sold on Option Care Health. Its margins are so thin that any disruption could push it into the red, a scary situation.― StockStory Analyst Team

1. News

2. Summary

Why Option Care Health Is Not Exciting

With a nationwide network of 177 locations serving 43 states and a team of over 4,500 clinicians, Option Care Health (NASDAQ:OPCH) is the largest independent provider of home and alternate site infusion services, delivering medications and clinical support to patients across the United States.

- Responsiveness to unforeseen market trends is restricted due to its substandard adjusted operating margin profitability

- A silver lining is that its earnings per share have outperformed its peers over the last five years, increasing by 125% annually

Option Care Health’s quality isn’t great. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Option Care Health

Option Care Health is trading at $34.98 per share, or 19.6x forward P/E. While valuation is appropriate for the quality you get, we’re still not buyers.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Option Care Health (OPCH) Research Report: Q4 CY2025 Update

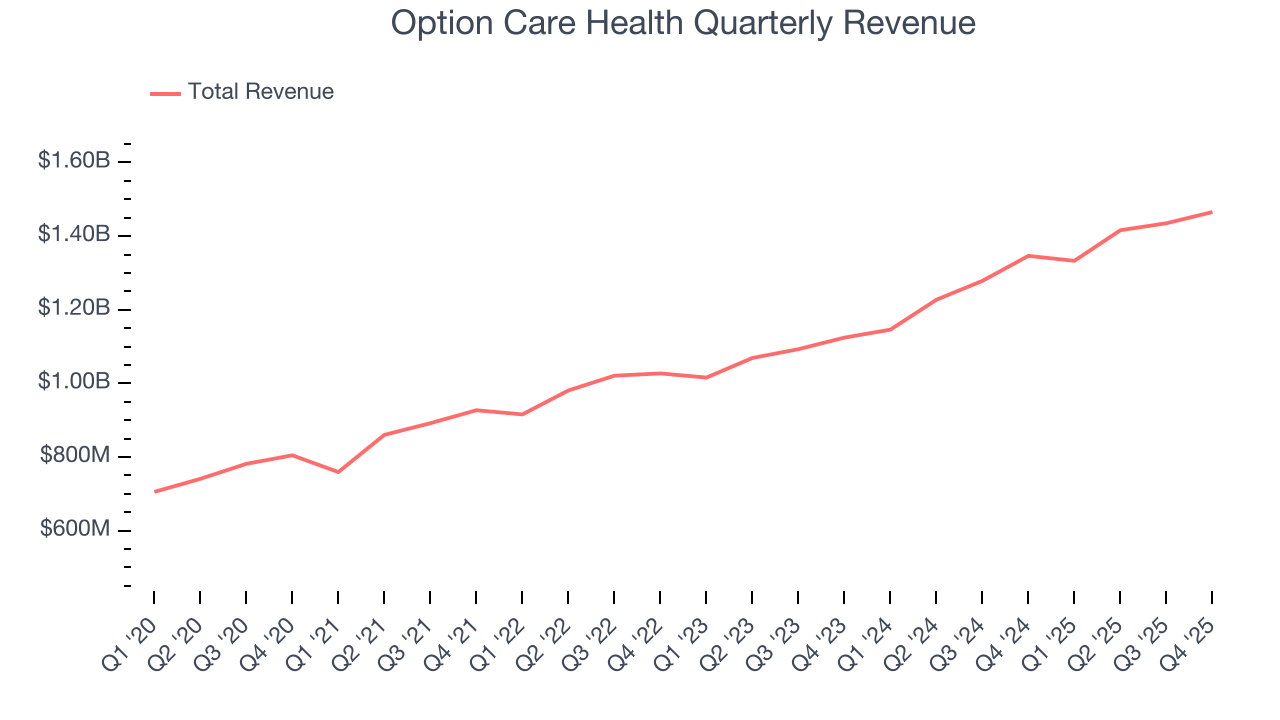

Alternate site health provider Option Care Health (NASDAQ:OPCH) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 8.8% year on year to $1.47 billion. On the other hand, the company’s full-year revenue guidance of $5.9 billion at the midpoint came in 1.4% below analysts’ estimates. Its non-GAAP profit of $0.46 per share was in line with analysts’ consensus estimates.

Option Care Health (OPCH) Q4 CY2025 Highlights:

- Revenue: $1.47 billion vs analyst estimates of $1.46 billion (8.8% year-on-year growth, in line)

- Adjusted EPS: $0.46 vs analyst estimates of $0.47 (in line)

- Adjusted EBITDA: $126 million vs analyst estimates of $125.5 million (8.6% margin, in line)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.87 at the midpoint, in line with analyst estimates

- EBITDA guidance for the upcoming financial year 2026 is $492.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 6.2%, in line with the same quarter last year

- Free Cash Flow Margin: 1.5%, similar to the same quarter last year

- Market Capitalization: $5.73 billion

Company Overview

With a nationwide network of 177 locations serving 43 states and a team of over 4,500 clinicians, Option Care Health (NASDAQ:OPCH) is the largest independent provider of home and alternate site infusion services, delivering medications and clinical support to patients across the United States.

Option Care Health specializes in administering complex medications through intravenous delivery in patients' homes or ambulatory infusion suites rather than hospitals. This approach offers patients greater comfort and convenience while typically reducing healthcare costs compared to inpatient treatment.

The company provides a comprehensive range of infusion therapies for chronic and acute conditions. These include anti-infective treatments for serious infections, nutrition support for patients unable to eat normally, immunoglobulin therapy for immune deficiencies, and specialized treatments for chronic inflammatory disorders, neurological conditions, bleeding disorders, heart failure, and high-risk pregnancies.

For example, a patient with a severe infection might be discharged from the hospital but still require six weeks of intravenous antibiotics. Option Care Health would deliver the medication, provide the necessary equipment, and send nurses to the patient's home to administer treatment and monitor their condition, all while coordinating with their physician.

Option Care Health generates revenue primarily through contracts with third-party payers, including private insurance companies, managed care organizations, Medicare, and Medicaid. The company is typically reimbursed for both the pharmaceuticals provided and the clinical services delivered. Its business model creates a four-way value proposition: patients receive care in comfortable settings, healthcare payers benefit from lower costs compared to hospital care, physicians gain support in managing complex cases, and pharmaceutical manufacturers secure a distribution channel for specialized medications.

The company maintains a nationwide infrastructure of pharmacies and ambulatory infusion suites, staffed by pharmacists, nurses, dietitians, and other healthcare professionals who work together to provide comprehensive patient care.

4. Senior Health, Home Health & Hospice

The senior health, home care, and hospice care industries provide essential services to aging populations and patients with chronic or terminal conditions. These companies benefit from stable, recurring revenue driven by relationships with patients and families that can extend many months or even years. However, the labor-intensive nature of the business makes it vulnerable to rising labor costs and staffing shortages, while profitability is constrained by reimbursement rates from Medicare, Medicaid, and private insurers. Looking ahead, the industry is positioned for tailwinds from an aging population, increasing chronic disease prevalence, and a growing preference for personalized in-home care. Advancements in remote monitoring and telehealth are expected to enhance efficiency and care delivery. However, headwinds such as labor shortages, wage inflation, and regulatory uncertainty around reimbursement could pose challenges. Investments in digitization and technology-driven care will be critical for long-term success.

Option Care Health competes with other home infusion providers including Optum Infusion Pharmacy (part of UnitedHealthcare), Coram CVS/specialty infusion services (a division of CVS Health), Amerita Specialty Pharmacy (a division of BrightSpring Health), KabaFusion, and Soleo Health, as well as numerous regional providers.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $5.65 billion in revenue over the past 12 months, Option Care Health has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

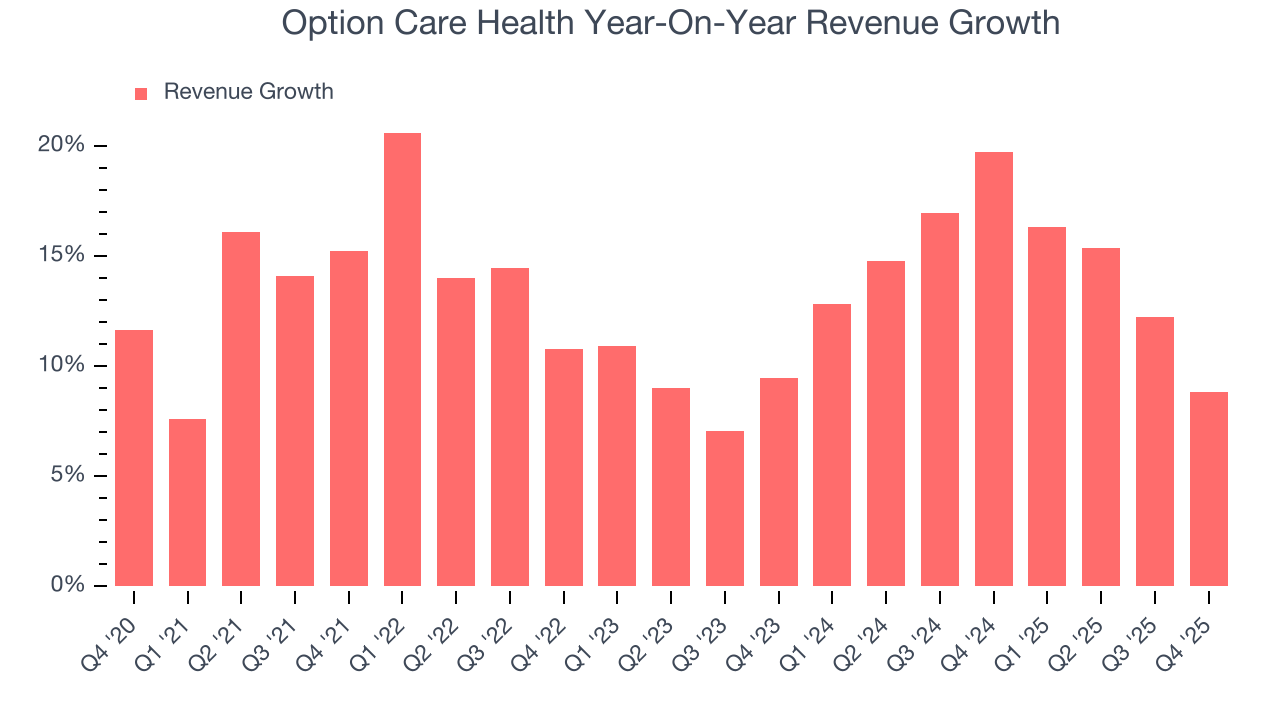

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Option Care Health grew its sales at a solid 13.3% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Option Care Health’s annualized revenue growth of 14.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Option Care Health grew its revenue by 8.8% year on year, and its $1.47 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last two years. Still, this projection is above the sector average and implies the market is baking in some success for its newer products and services.

7. Operating Margin

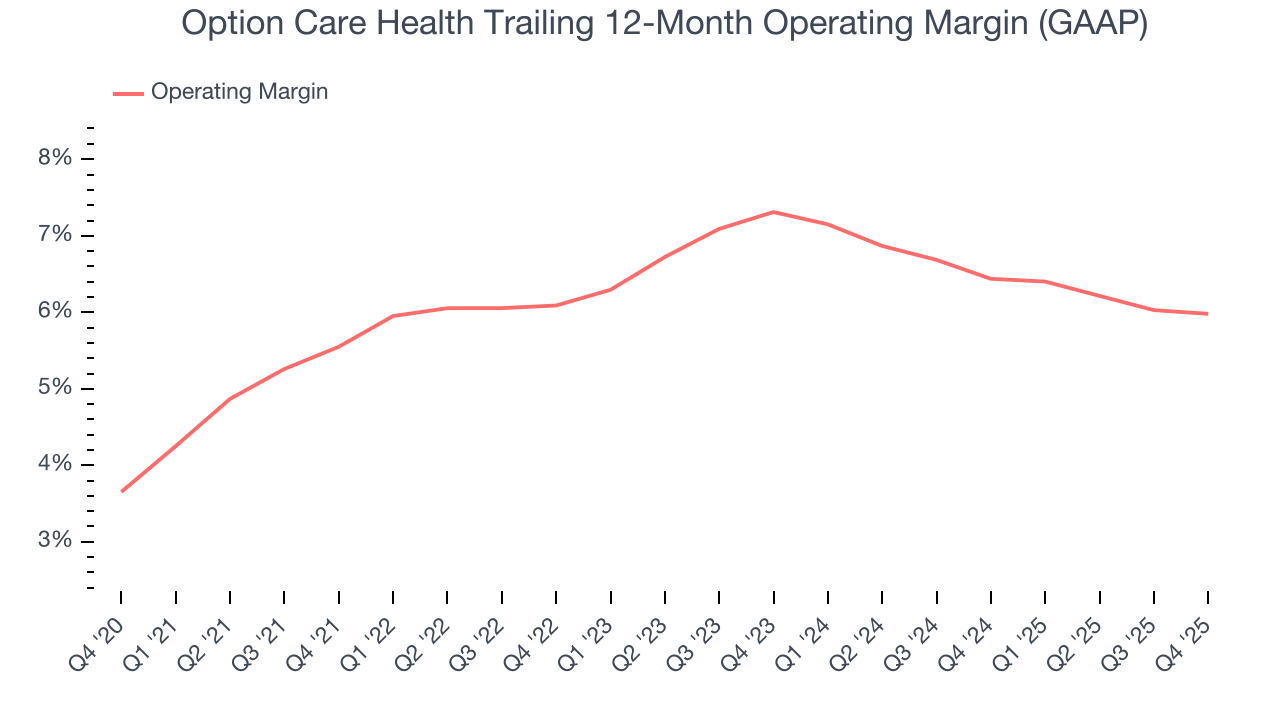

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Option Care Health’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 6.3% over the last five years. This profitability was mediocre for a healthcare business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, Option Care Health’s operating margin of 6% for the trailing 12 months may be around the same as five years ago, but it has decreased by 1.3 percentage points over the last two years.

In Q4, Option Care Health generated an operating margin profit margin of 6.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

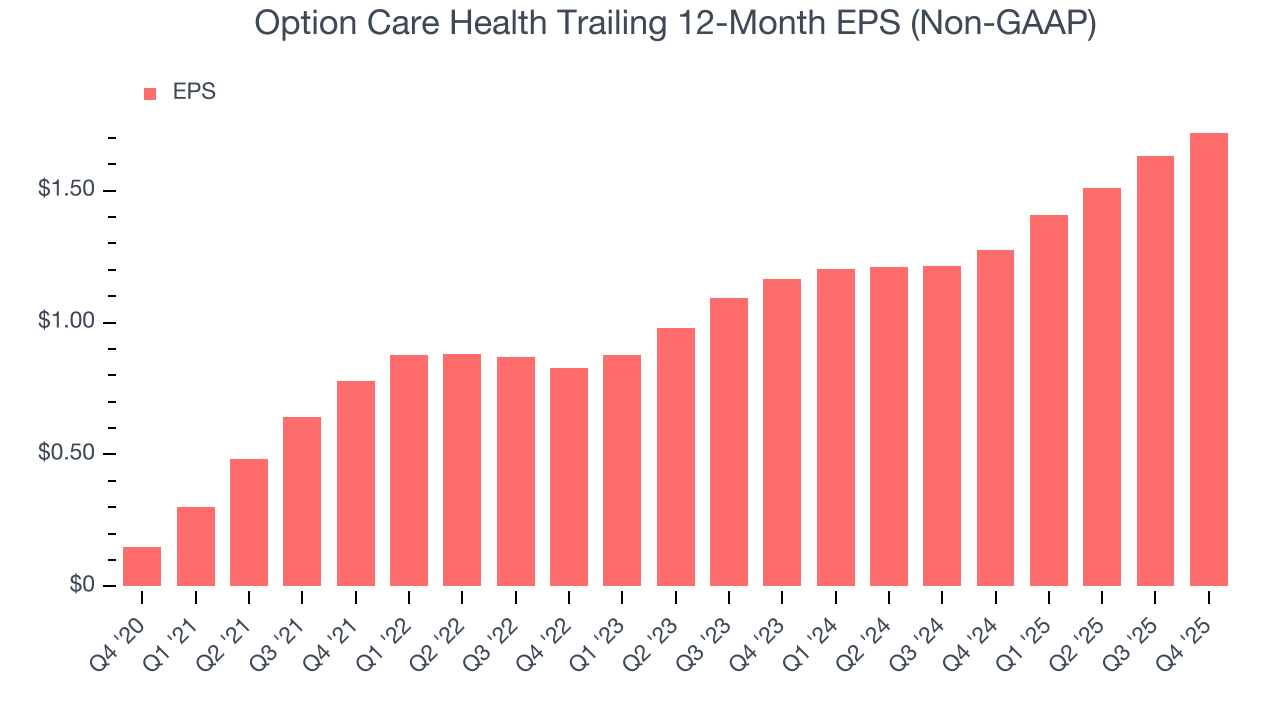

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Option Care Health’s EPS grew at an astounding 62.9% compounded annual growth rate over the last five years, higher than its 13.3% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

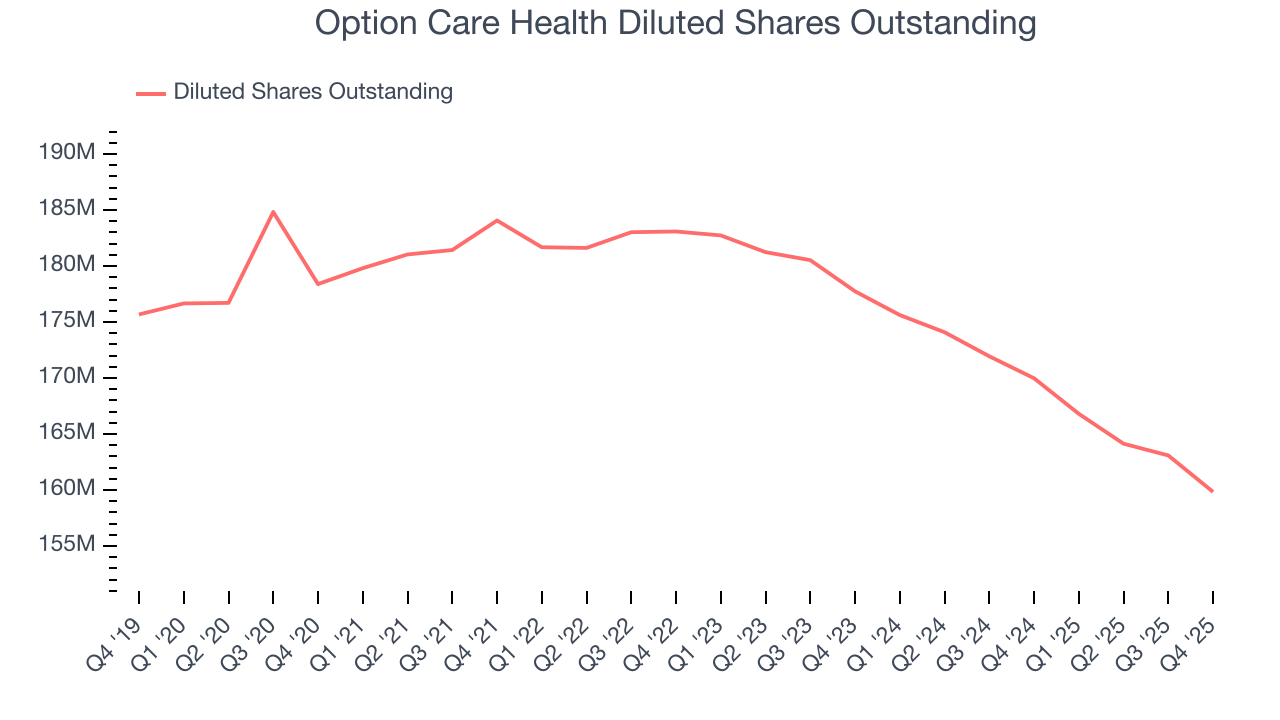

Diving into the nuances of Option Care Health’s earnings can give us a better understanding of its performance. A five-year view shows that Option Care Health has repurchased its stock, shrinking its share count by 10.4%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Option Care Health reported adjusted EPS of $0.46, up from $0.37 in the same quarter last year. Despite growing year on year, this print slightly missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Option Care Health’s full-year EPS of $1.72 to grow 9%.

9. Cash Is King

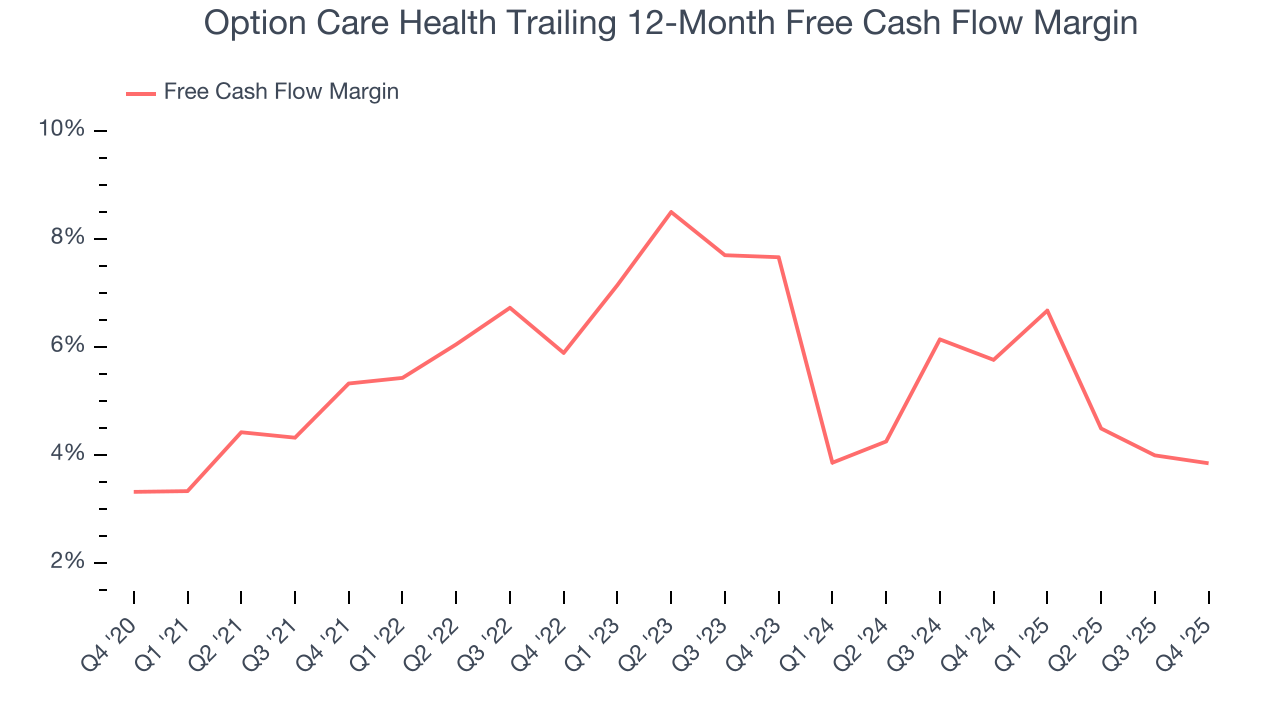

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Option Care Health has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.6% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that Option Care Health’s margin dropped by 1.5 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Option Care Health’s free cash flow clocked in at $22.25 million in Q4, equivalent to a 1.5% margin. This cash profitability was in line with the comparable period last year but below its five-year average. In a silo, this isn’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

10. Return on Invested Capital (ROIC)

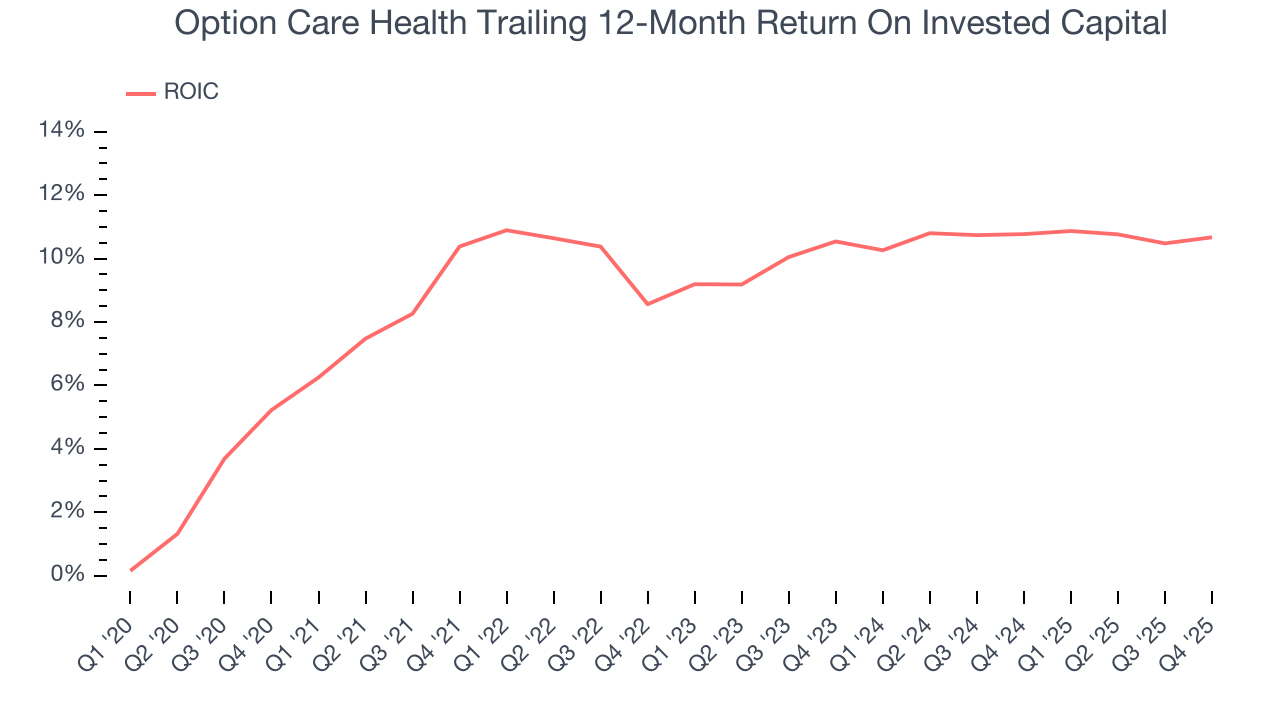

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Option Care Health’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 10.2%, slightly better than typical healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Option Care Health’s ROIC averaged 1.2 percentage point increases each year over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

11. Balance Sheet Assessment

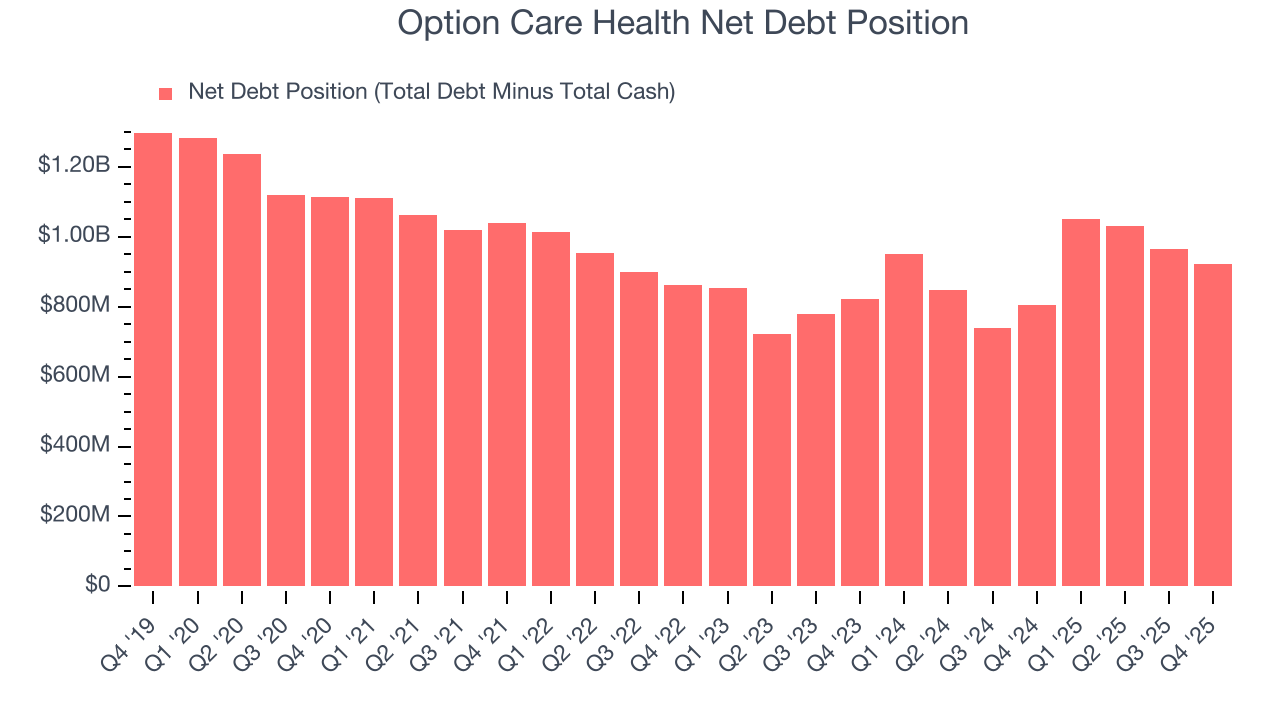

Option Care Health reported $232.6 million of cash and $1.15 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $471.3 million of EBITDA over the last 12 months, we view Option Care Health’s 2.0× net-debt-to-EBITDA ratio as safe. We also see its $56.78 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Option Care Health’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance slightly missed and its EPS was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.9% to $34.70 immediately following the results.

13. Is Now The Time To Buy Option Care Health?

Before investing in or passing on Option Care Health, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Option Care Health isn’t a bad business, but we have other favorites. First off, its revenue growth was solid over the last five years. And while Option Care Health’s operating margins are low compared to other healthcare companies, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Option Care Health’s P/E ratio based on the next 12 months is 19.3x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $39.82 on the company (compared to the current share price of $34.70).