The Pennant Group (PNTG)

We’re not sold on The Pennant Group. Its weak returns on capital indicate management was inefficient with its resources and missed opportunities.― StockStory Analyst Team

1. News

2. Summary

Why The Pennant Group Is Not Exciting

Spun off from The Ensign Group in 2019 to focus on non-skilled nursing healthcare services, Pennant Group (NASDAQ:PNTG) operates home health, hospice, and senior living facilities across 13 western and midwestern states, serving patients of all ages including seniors.

- Modest revenue base of $941.5 million gives it less fixed cost leverage and fewer distribution channels than larger companies

- Poor expense management has led to an adjusted operating margin that is below the industry average

- 6× net-debt-to-EBITDA ratio shows it’s overleveraged and increases the probability of shareholder dilution if things turn unexpectedly

The Pennant Group is in the doghouse. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than The Pennant Group

The Pennant Group’s stock price of $33.04 implies a valuation ratio of 25.1x forward P/E. This multiple is higher than most healthcare companies, and we think it’s quite expensive for the quality you get.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. The Pennant Group (PNTG) Research Report: Q4 CY2025 Update

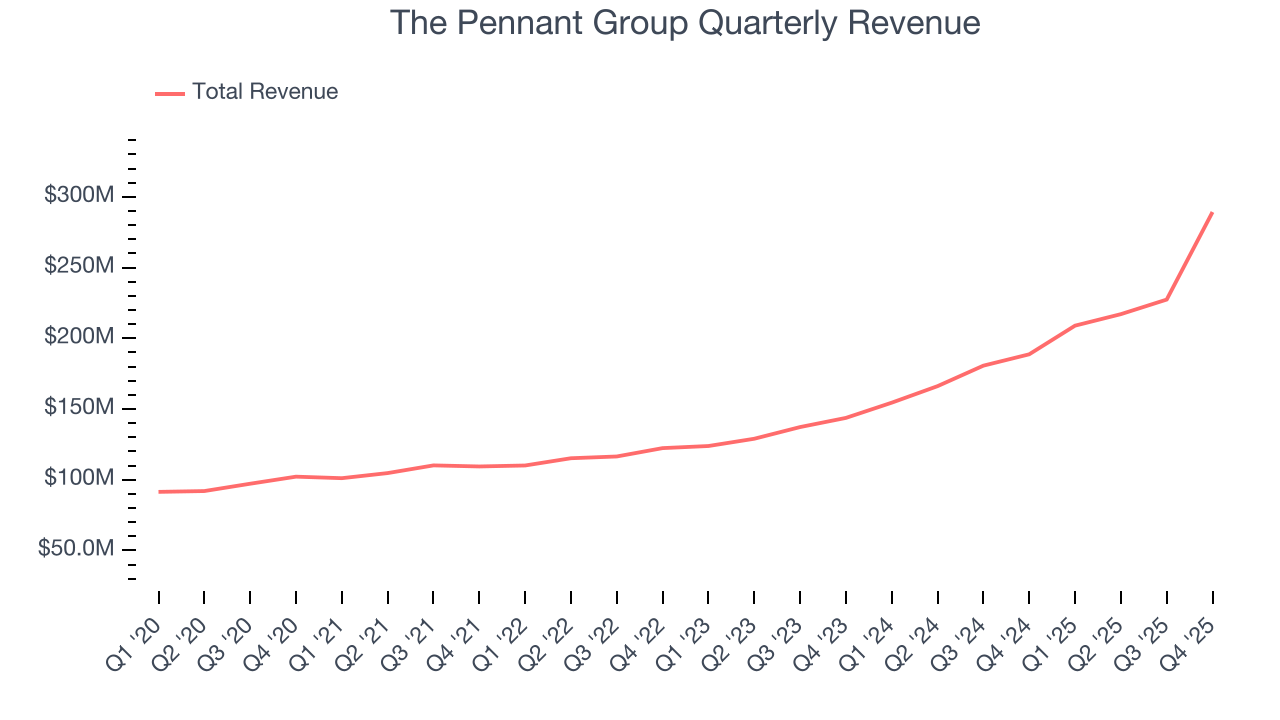

Senior living provider The Pennant Group (NASDAQ:PNTG) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 53.3% year on year to $289.3 million. The company expects the full year’s revenue to be around $1.15 billion, close to analysts’ estimates. Its non-GAAP profit of $0.34 per share was 7.7% above analysts’ consensus estimates.

The Pennant Group (PNTG) Q4 CY2025 Highlights:

- Revenue: $289.3 million vs analyst estimates of $275.2 million (53.3% year-on-year growth, 5.1% beat)

- Adjusted EPS: $0.34 vs analyst estimates of $0.32 (7.7% beat)

- Adjusted EBITDA: $22.37 million vs analyst estimates of $22.07 million (7.7% margin, 1.4% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.31 at the midpoint

- EBITDA guidance for the upcoming financial year 2026 is $91.3 million at the midpoint, below analyst estimates of $93.76 million

- Operating Margin: 6%, up from 4.9% in the same quarter last year

- Sales Volumes rose 81.3% year on year (-63.3% in the same quarter last year)

- Market Capitalization: $1.11 billion

Company Overview

Spun off from The Ensign Group in 2019 to focus on non-skilled nursing healthcare services, Pennant Group (NASDAQ:PNTG) operates home health, hospice, and senior living facilities across 13 western and midwestern states, serving patients of all ages including seniors.

Pennant Group's business is divided into two main segments: Home Health and Hospice Services, and Senior Living Services. The Home Health and Hospice segment provides clinical services like nursing, physical therapy, and medical social work in patients' homes, allowing them to receive care in comfortable, familiar settings. For example, a stroke recovery patient might receive regular visits from Pennant's physical therapists and nurses to regain mobility without needing to stay in a hospital. The hospice division focuses on end-of-life care, providing pain management and emotional support for terminally ill patients and their families.

The Senior Living segment operates assisted living, independent living, and memory care communities where residents receive varying levels of support based on their needs. These communities offer accommodations, meals, activities, and assistance with daily tasks. A typical resident might be an elderly person who needs help with medication management but doesn't require the intensive medical care of a nursing home.

Pennant generates revenue through a diverse mix of payment sources. Medicare and Medicaid programs fund a significant portion of home health and hospice services, while senior living facilities derive revenue primarily from private pay sources, with some government program support. The company uses a local leadership model, giving individual facility administrators significant autonomy to respond to local market needs and build relationships with referral sources like hospitals and physicians.

Pennant's operating structure is organized into portfolio companies with specialized leadership teams for each service line, allowing for targeted expertise in areas like home health operations or memory care. This structure supports both organic growth and strategic acquisitions, as the company continues to expand its footprint across the western and midwestern United States.

4. Senior Health, Home Health & Hospice

The senior health, home care, and hospice care industries provide essential services to aging populations and patients with chronic or terminal conditions. These companies benefit from stable, recurring revenue driven by relationships with patients and families that can extend many months or even years. However, the labor-intensive nature of the business makes it vulnerable to rising labor costs and staffing shortages, while profitability is constrained by reimbursement rates from Medicare, Medicaid, and private insurers. Looking ahead, the industry is positioned for tailwinds from an aging population, increasing chronic disease prevalence, and a growing preference for personalized in-home care. Advancements in remote monitoring and telehealth are expected to enhance efficiency and care delivery. However, headwinds such as labor shortages, wage inflation, and regulatory uncertainty around reimbursement could pose challenges. Investments in digitization and technology-driven care will be critical for long-term success.

Pennant Group competes with other home health and senior living providers including Amedisys (NASDAQ:AMED), LHC Group (owned by UnitedHealth Group, NYSE:UNH), Brookdale Senior Living (NYSE:BKD), and Encompass Health (NYSE:EHC).

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $942.8 million in revenue over the past 12 months, The Pennant Group is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

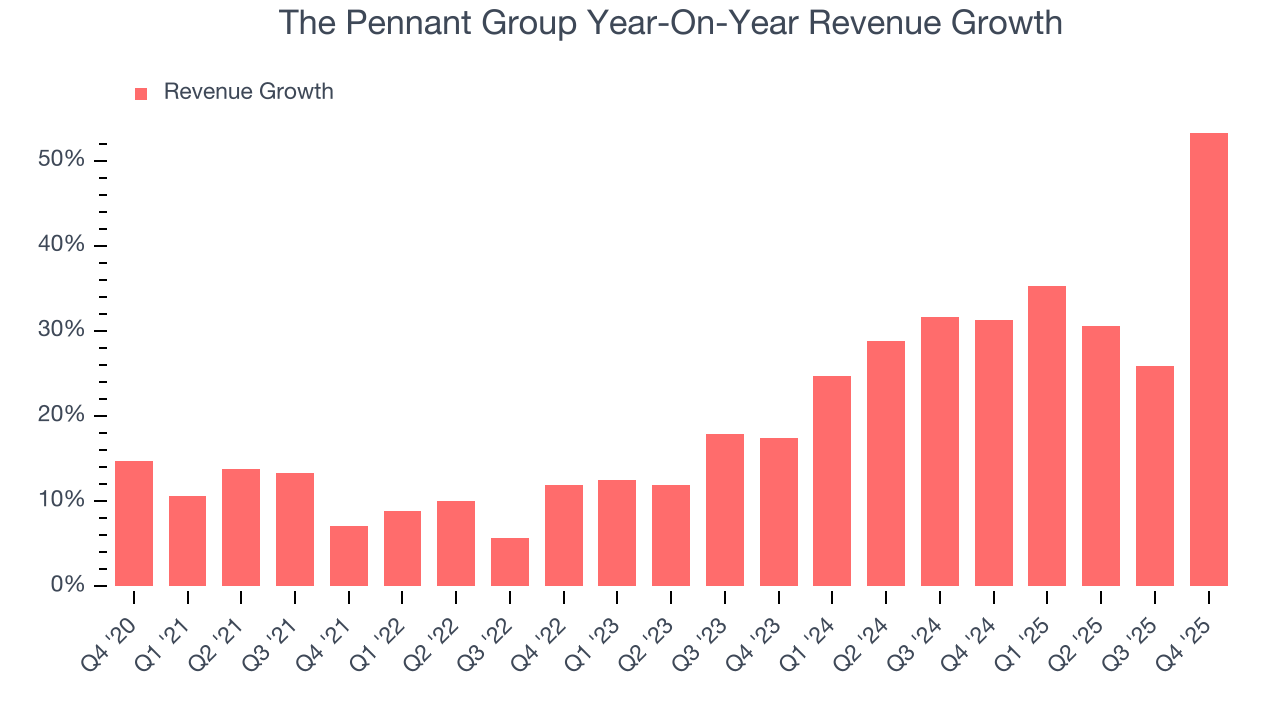

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, The Pennant Group grew its sales at an impressive 19.8% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. The Pennant Group’s annualized revenue growth of 32.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

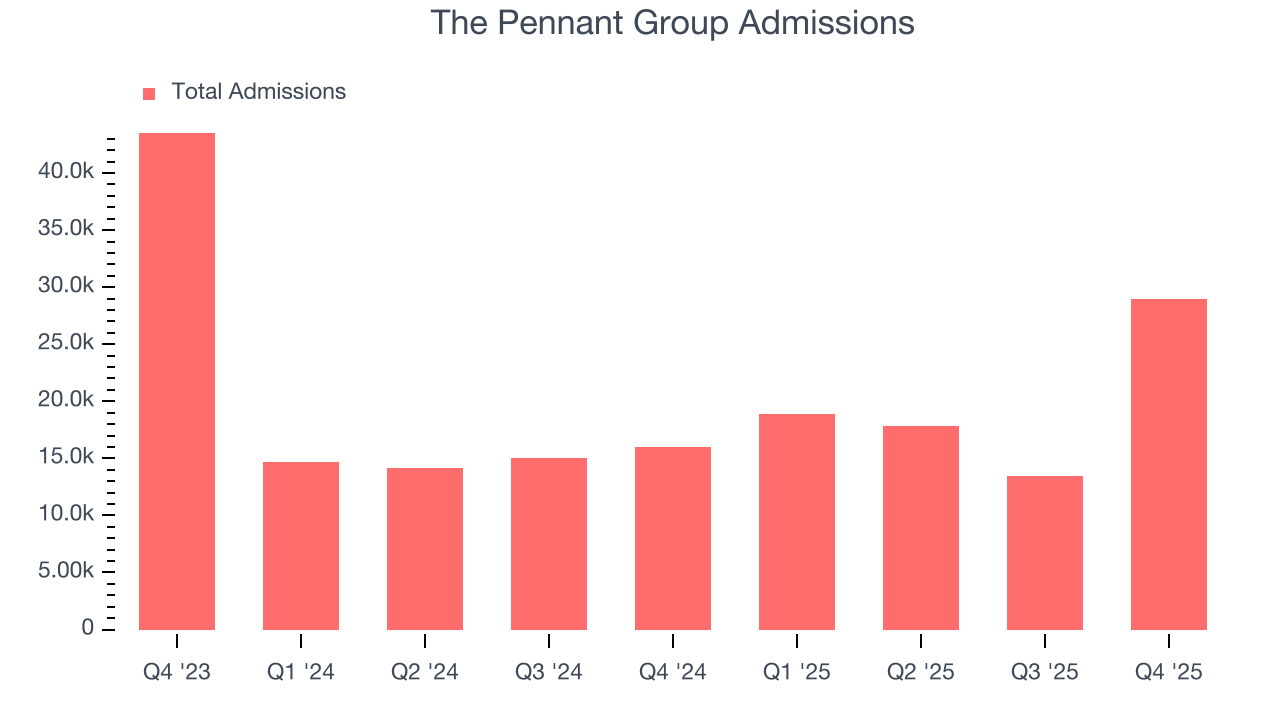

The Pennant Group also reports its number of admissions, which reached 28,941 in the latest quarter. Over the last two years, The Pennant Group’s admissions averaged 12.5% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, The Pennant Group reported magnificent year-on-year revenue growth of 53.3%, and its $289.3 million of revenue beat Wall Street’s estimates by 5.1%.

Looking ahead, sell-side analysts expect revenue to grow 22.4% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and indicates the market sees success for its products and services.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

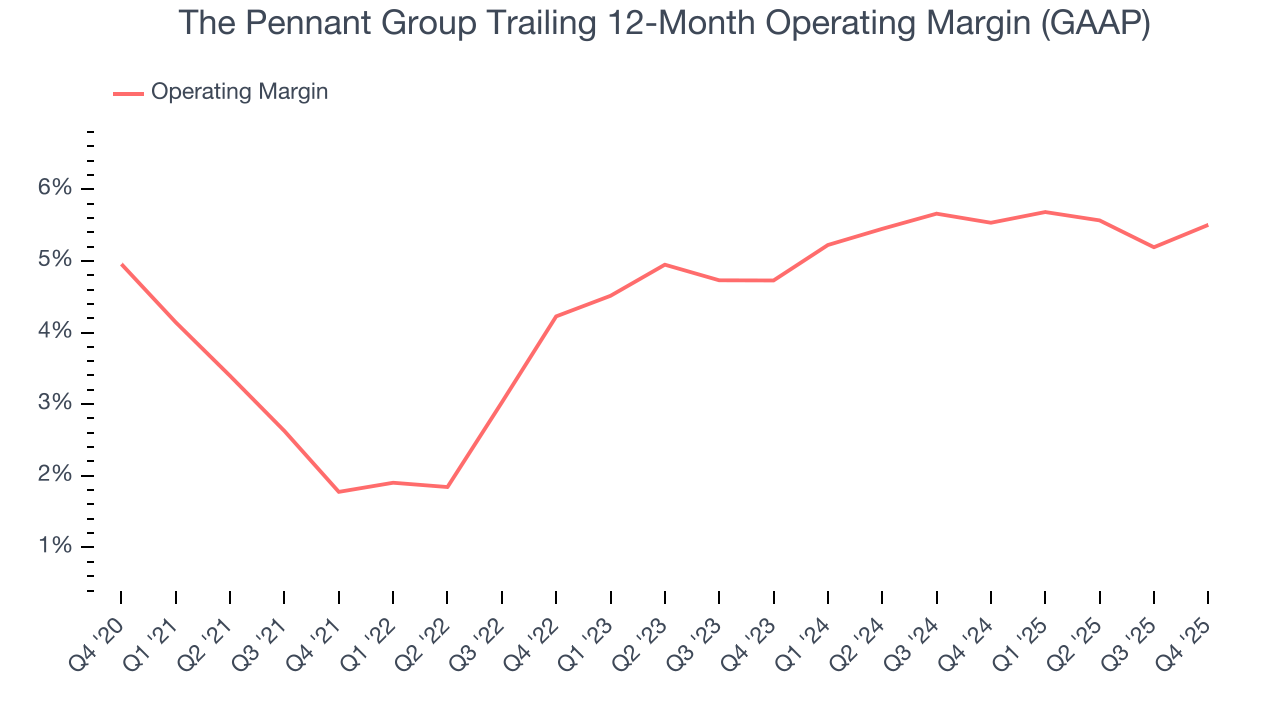

The Pennant Group was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.7% was weak for a healthcare business.

On the plus side, The Pennant Group’s operating margin rose by 3.7 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, The Pennant Group generated an operating margin profit margin of 6%, up 1.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

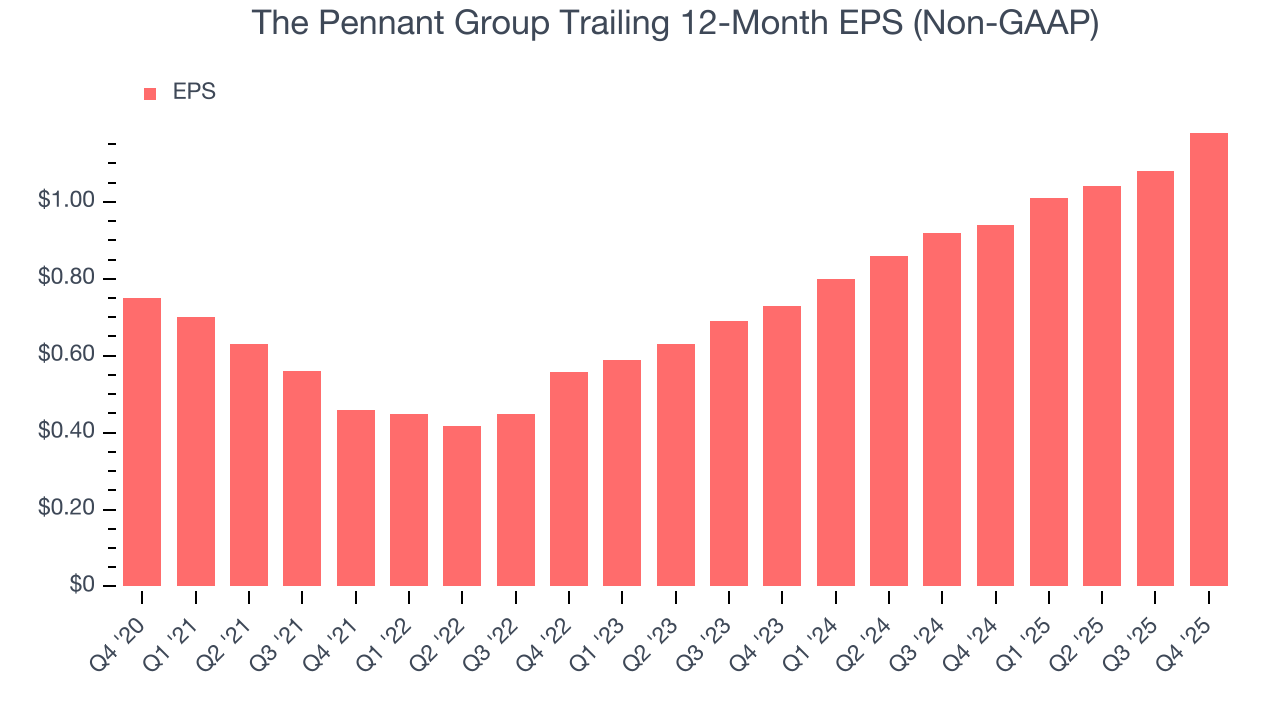

The Pennant Group’s EPS grew at a remarkable 9.5% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 19.8% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

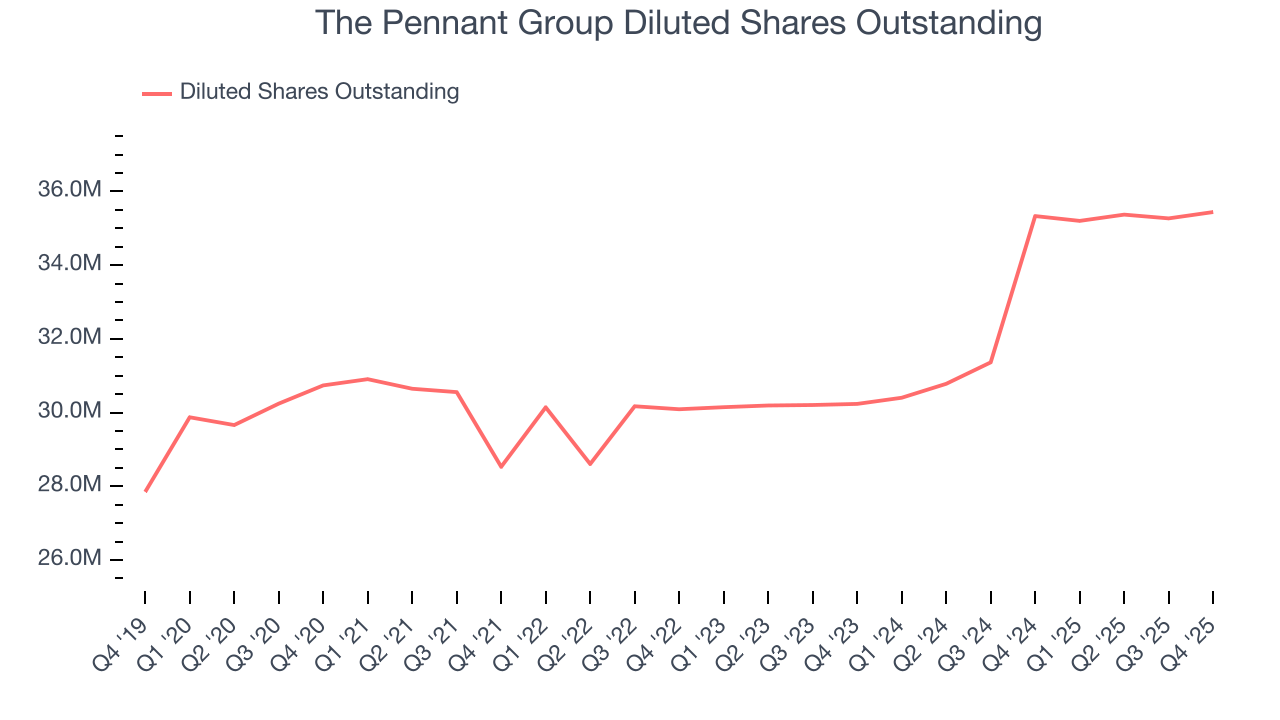

Diving into the nuances of The Pennant Group’s earnings can give us a better understanding of its performance. A five-year view shows The Pennant Group has diluted its shareholders, growing its share count by 15.3%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, The Pennant Group reported adjusted EPS of $0.34, up from $0.24 in the same quarter last year. This print beat analysts’ estimates by 7.7%. Over the next 12 months, Wall Street expects The Pennant Group’s full-year EPS of $1.18 to grow 10%.

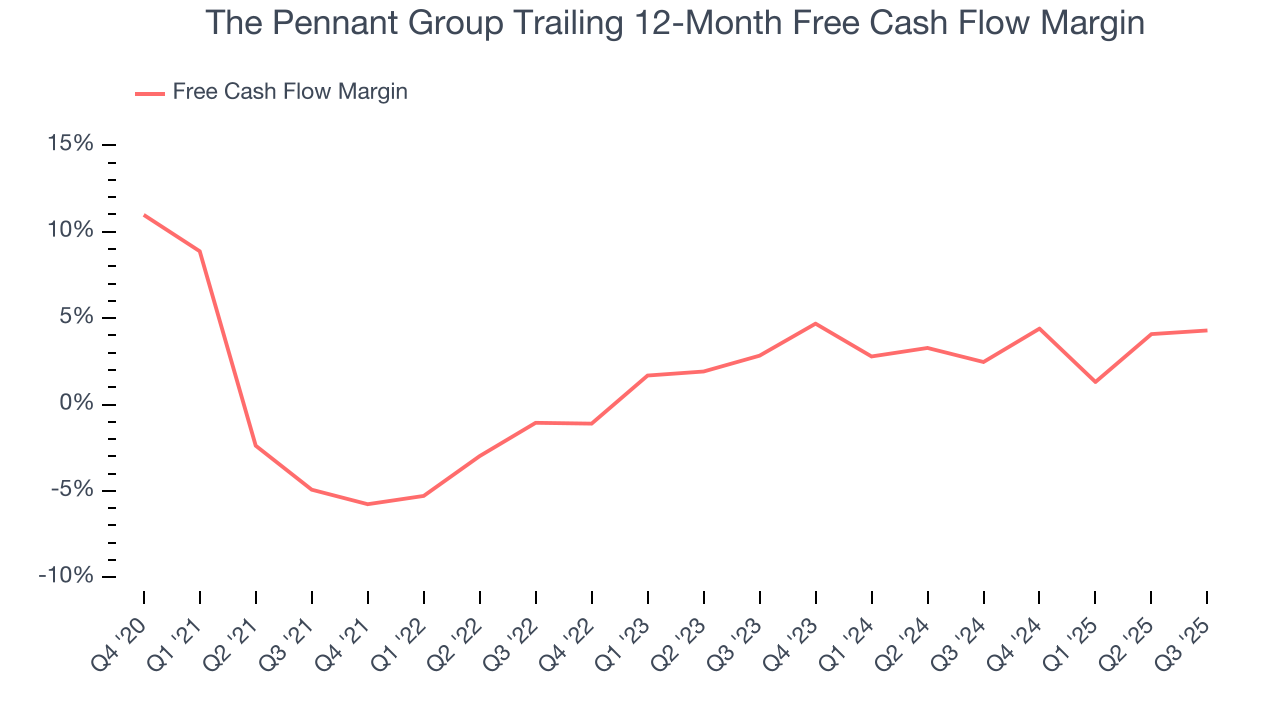

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

The Pennant Group has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.6%, subpar for a healthcare business.

Taking a step back, an encouraging sign is that The Pennant Group’s margin expanded by 8.3 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

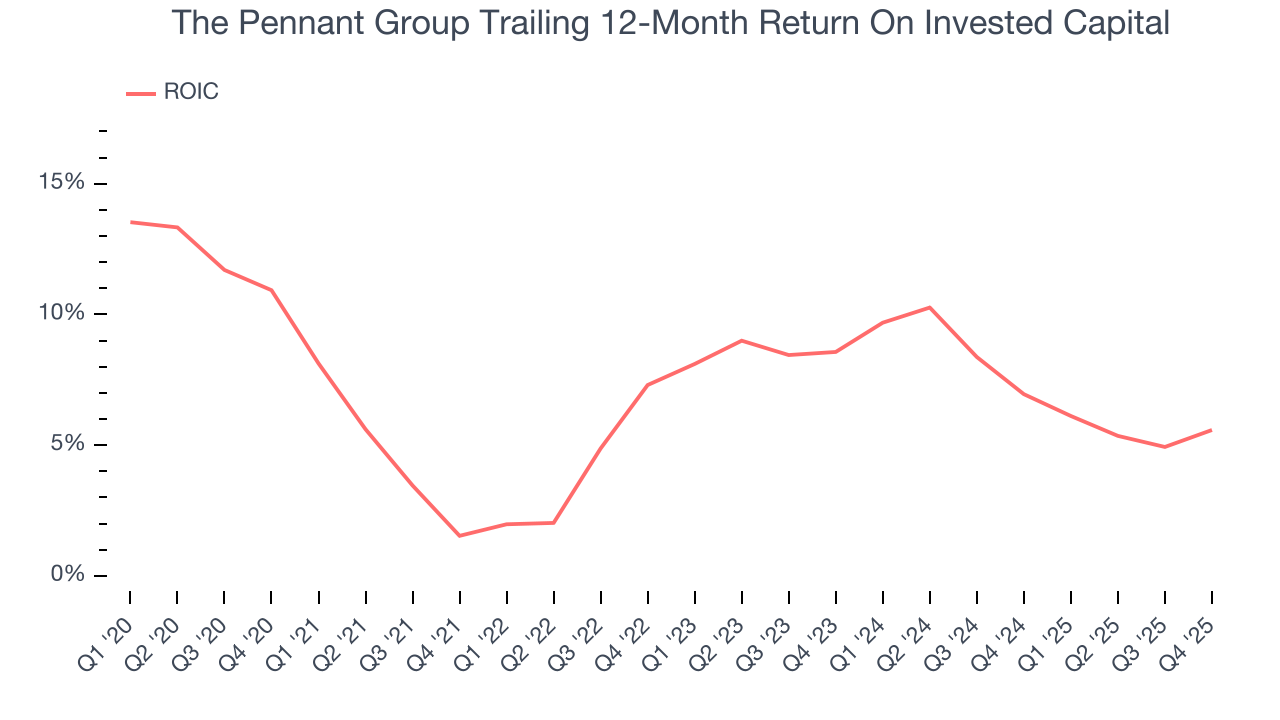

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

The Pennant Group historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, The Pennant Group’s ROIC averaged 1.8 percentage point increases each year over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

11. Balance Sheet Risk

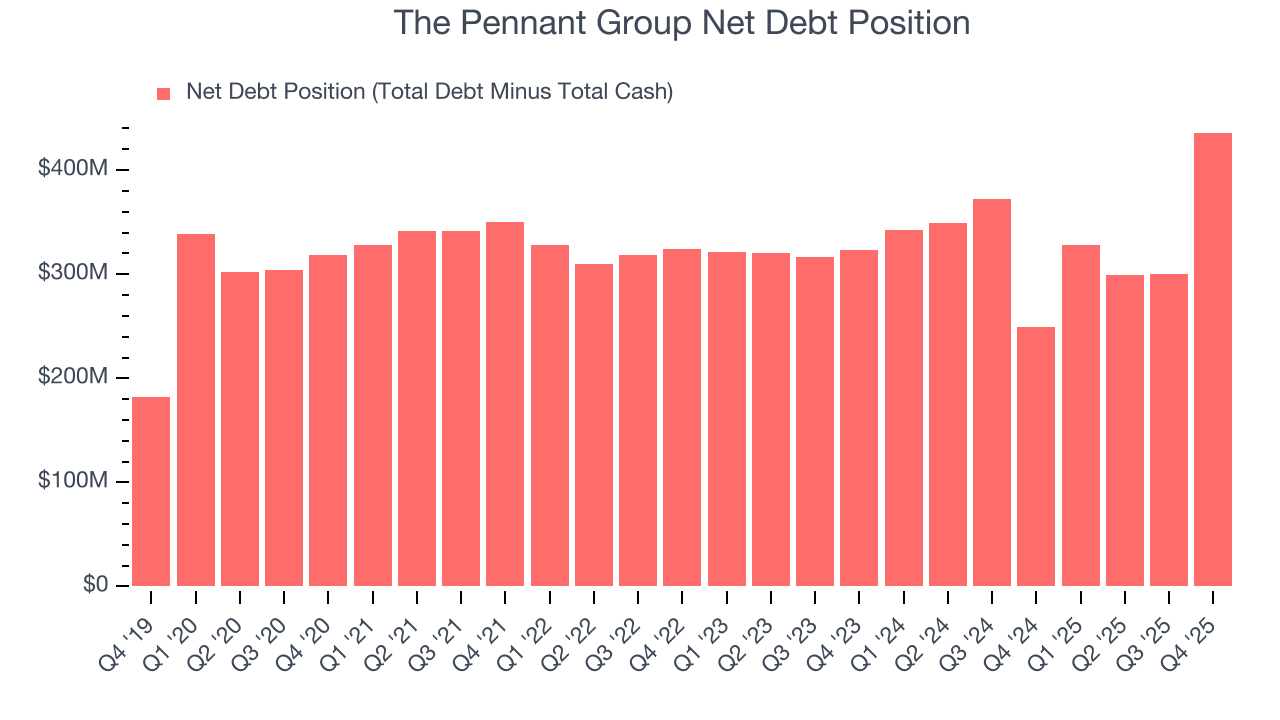

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

The Pennant Group’s $453.2 million of debt exceeds the $17.02 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $72.47 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. The Pennant Group could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope The Pennant Group can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from The Pennant Group’s Q4 Results

We were impressed by how significantly The Pennant Group blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 3.2% to $32.03 immediately after reporting.

13. Is Now The Time To Buy The Pennant Group?

Updated: March 18, 2026 at 12:34 AM EDT

Are you wondering whether to buy The Pennant Group or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

The Pennant Group is a pretty decent company if you ignore its balance sheet. First off, its revenue growth was impressive over the last five years and is expected to accelerate over the next 12 months. And while The Pennant Group’s subscale operations give it fewer distribution channels than its larger rivals, its rising cash profitability gives it more optionality.

The Pennant Group’s P/E ratio based on the next 12 months is 25.1x. All that said, we aren’t investing at the moment because its balance sheet makes us balk. We think a potential buyer of the stock should wait until the company generates sufficient cash flows or raises money.

Wall Street analysts have a consensus one-year price target of $37.83 on the company (compared to the current share price of $33.04).