Tenable (TENB)

We’re skeptical of Tenable. Its decelerating growth and inability to generate meaningful profits make us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think Tenable Will Underperform

Starting with the widely-used Nessus vulnerability scanner first released in 1998, Tenable (NASDAQ:TENB) provides exposure management solutions that help organizations identify, assess, and prioritize cybersecurity vulnerabilities across their IT infrastructure and cloud environments.

- Operating margin failed to increase over the last year, indicating the company couldn’t optimize its expenses

- Estimated sales growth of 7.2% for the next 12 months implies demand will slow from its two-year trend

- On the bright side, its ARR trends over the last year show it’s maintaining a steady flow of long-term contracts that contribute positively to its revenue predictability

Tenable doesn’t satisfy our quality benchmarks. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than Tenable

At $20.87 per share, Tenable trades at 2.2x forward price-to-sales. Tenable’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Tenable (TENB) Research Report: Q4 CY2025 Update

Cybersecurity exposure management company Tenable (NASDAQ:TENB) announced better-than-expected revenue in Q4 CY2025, with sales up 10.5% year on year to $260.5 million. The company expects next quarter’s revenue to be around $258.5 million, coming in 0.8% above analysts’ estimates. Its non-GAAP profit of $0.48 per share was 15.9% above analysts’ consensus estimates.

Tenable (TENB) Q4 CY2025 Highlights:

- Revenue: $260.5 million vs analyst estimates of $251.8 million (10.5% year-on-year growth, 3.5% beat)

- Adjusted EPS: $0.48 vs analyst estimates of $0.41 (15.9% beat)

- Adjusted Operating Income: $57.31 million vs analyst estimates of $58.25 million (22% margin, 1.6% miss)

- Revenue Guidance for Q1 CY2026 is $258.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.86 at the midpoint, beating analyst estimates by 5.2%

- Operating Margin: 3.4%, down from 5.5% in the same quarter last year

- Free Cash Flow Margin: 31.1%, up from 20.5% in the previous quarter

- Billings: $327,800 at quarter end, down 99.9% year on year

- Market Capitalization: $2.39 billion

Company Overview

Starting with the widely-used Nessus vulnerability scanner first released in 1998, Tenable (NASDAQ:TENB) provides exposure management solutions that help organizations identify, assess, and prioritize cybersecurity vulnerabilities across their IT infrastructure and cloud environments.

Tenable's platform gives security teams visibility into vulnerabilities, misconfigurations, and compliance issues across their entire technology landscape. The company's flagship product, Tenable One, combines various security solutions to provide a comprehensive view of an organization's attack surface. This includes traditional IT assets, cloud resources, web applications, Active Directory environments, and operational technology systems used in industrial settings.

Behind Tenable's solutions is its research team of cybersecurity experts who continuously identify new vulnerabilities and security issues. The company employs artificial intelligence and machine learning to analyze vast amounts of security data, prioritize risks, and provide actionable remediation guidance. This helps security teams focus their efforts on the most critical issues first.

A typical customer might use Tenable to scan their network and discover that several cloud servers are running outdated software with known security flaws, while also identifying excessive user permissions that could be exploited by attackers. Tenable then helps prioritize which issues to fix first based on their potential impact.

Tenable generates revenue through subscription licenses to its software platforms. The company sells through a two-tiered channel model, working with distributors who sell to resellers, who then sell to end customers spanning industries from manufacturing and healthcare to government and finance.

4. Vulnerability Management

The demand for cybersecurity is growing as more and more businesses are moving their data and processes into the cloud, which along with a major increase in employees working remotely, has increased their exposure to attacks and malware. Additionally, the growing array of corporate IT systems, applications and internet connected devices has increased the complexity of network security, all of which has substantially increased the demand for software meant to protect data breaches.

Tenable competes with vulnerability management vendors like Qualys (NASDAQ:QLYS) and Rapid7 (NASDAQ:RPD), cloud security specialists including Wiz (private) and Palo Alto Networks (NASDAQ:PANW), and endpoint security providers with vulnerability assessment capabilities such as CrowdStrike (NASDAQ:CRWD).

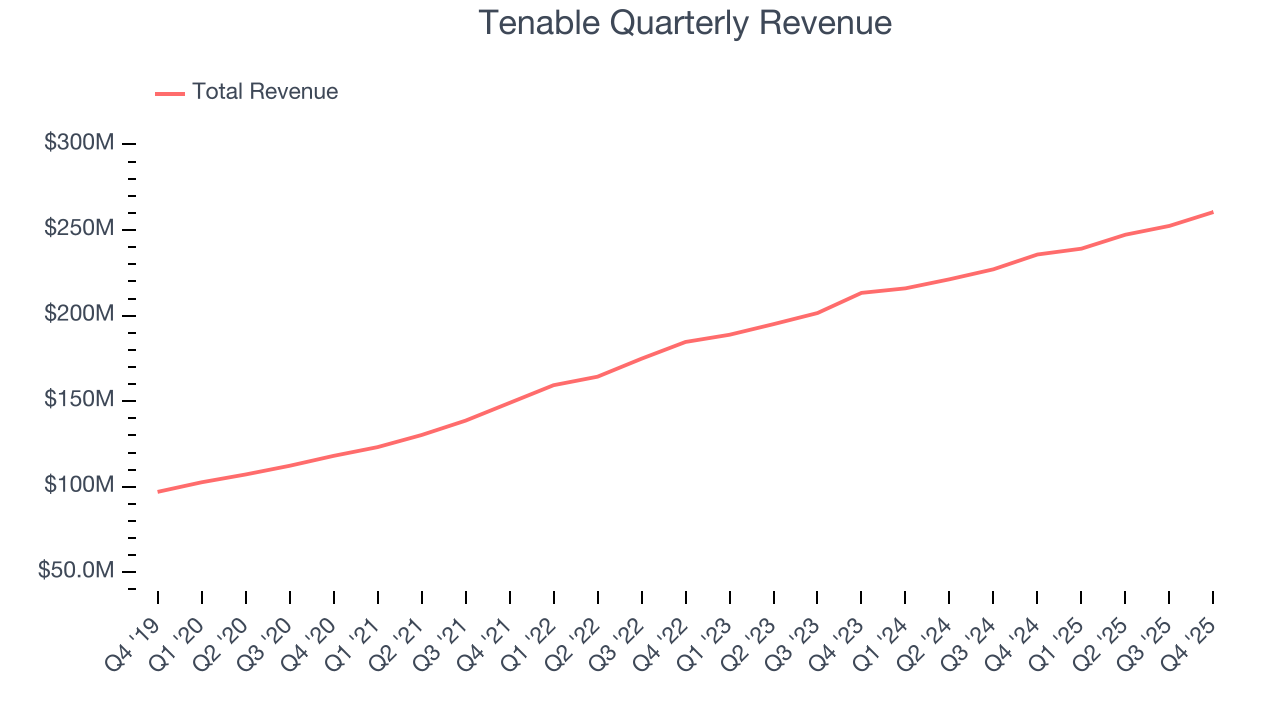

5. Revenue Growth

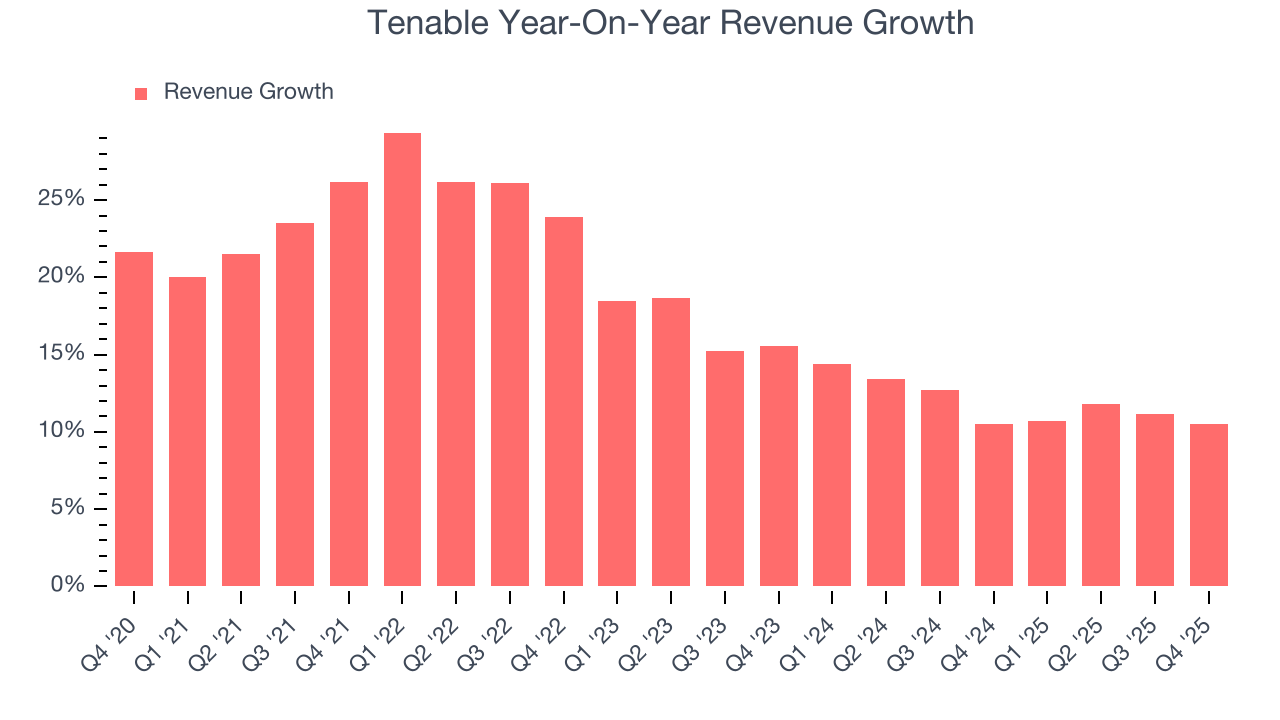

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Tenable’s 17.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Tenable’s recent performance shows its demand has slowed as its annualized revenue growth of 11.9% over the last two years was below its five-year trend.

This quarter, Tenable reported year-on-year revenue growth of 10.5%, and its $260.5 million of revenue exceeded Wall Street’s estimates by 3.5%. Company management is currently guiding for a 8.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

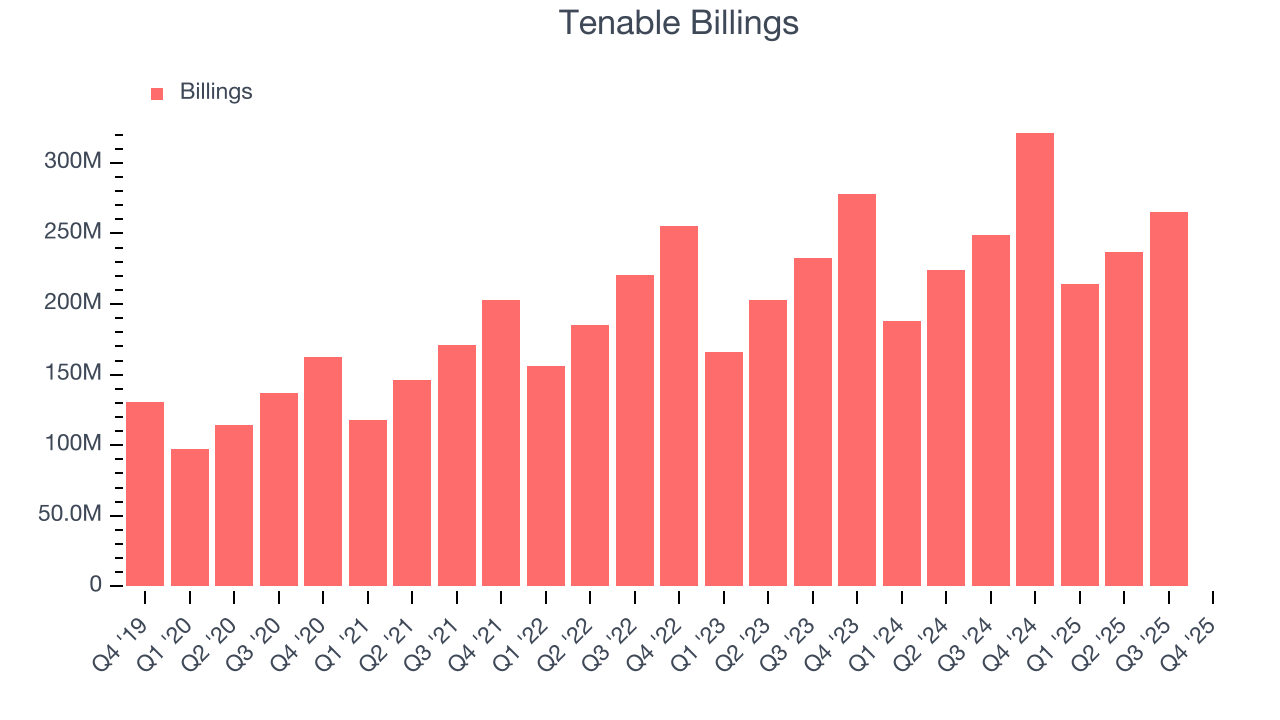

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Tenable’s billings came in at $327,800 in Q4, and it averaged 18.5% year-on-year declines over the last four quarters. This alternate topline metric underperformed its total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

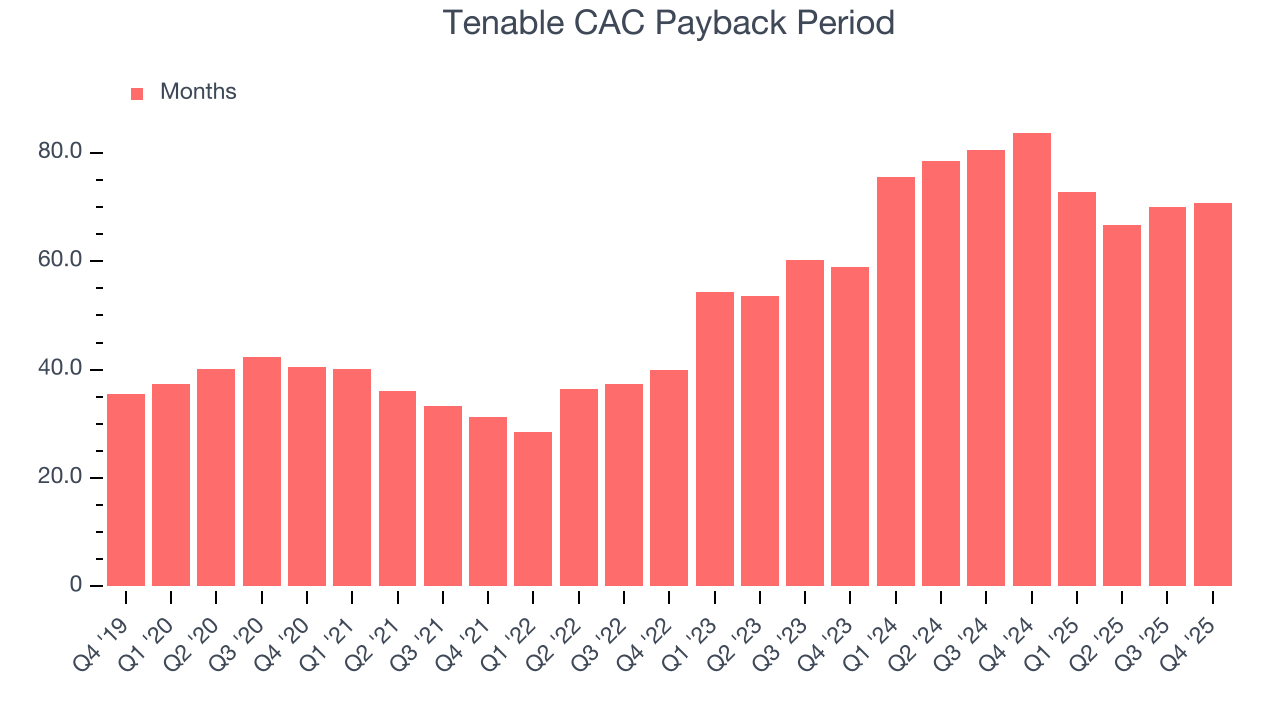

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s relatively expensive for Tenable to acquire new customers as its CAC payback period checked in at 70.8 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

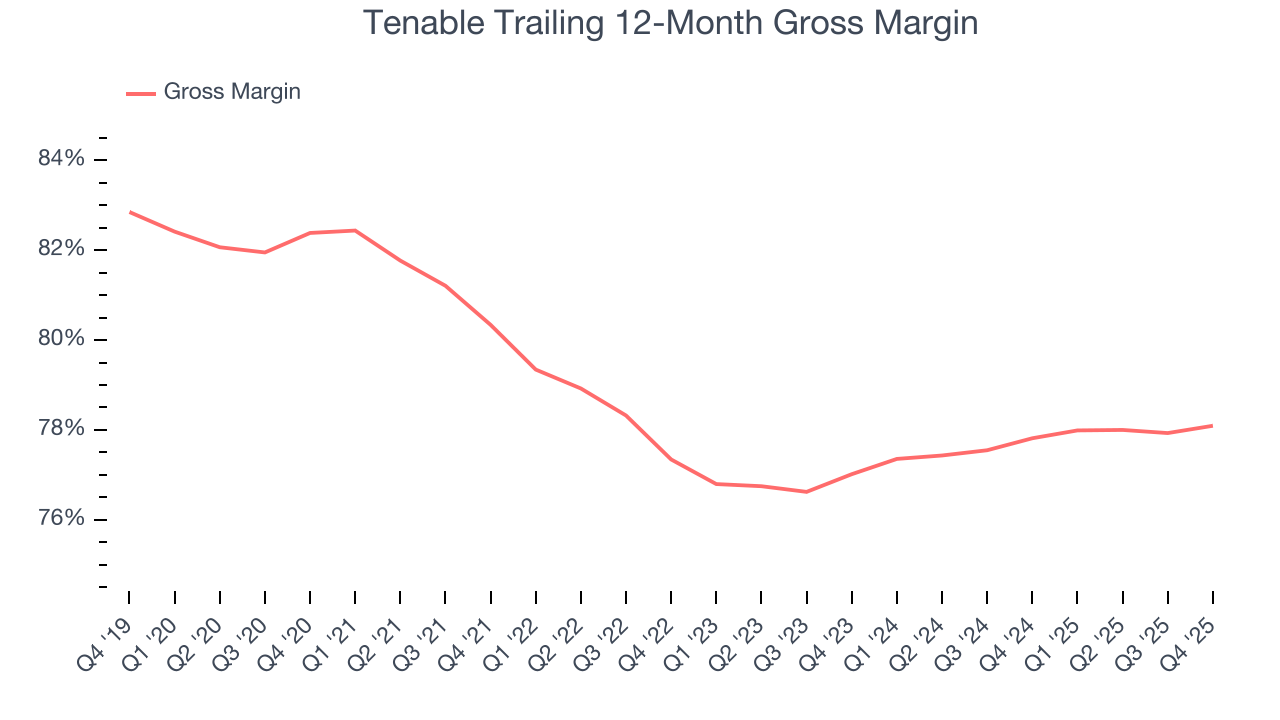

8. Gross Margin & Pricing Power

For software companies like Tenable, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Tenable’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an excellent 78.1% gross margin over the last year. That means Tenable only paid its providers $21.91 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Tenable has seen gross margins improve by 1.1 percentage points over the last 2 year, which is slightly better than average for software.

Tenable produced a 78.8% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

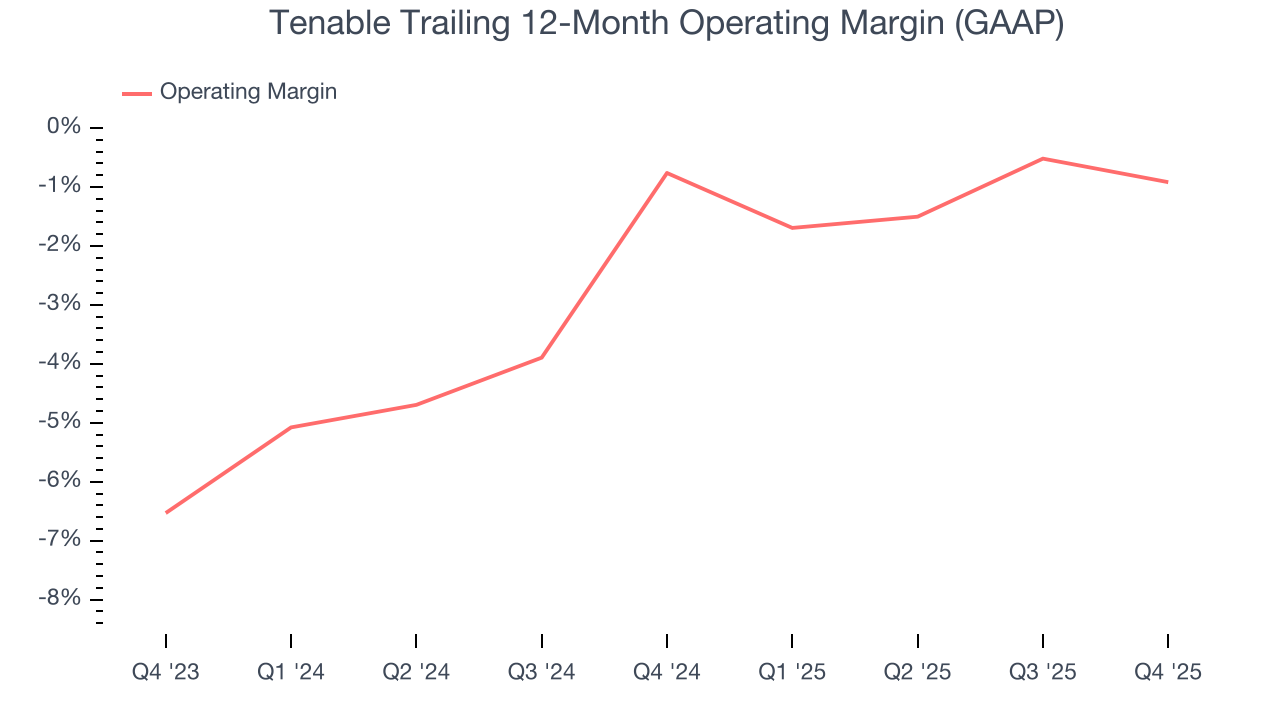

9. Operating Margin

Tenable was roughly breakeven when averaging the last year of quarterly operating profits, mediocre for a software business. This result is surprising given its high gross margin as a starting point.

Analyzing the trend in its profitability, Tenable’s operating margin might fluctuated slightly but has generally stayed the same over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Tenable generated an operating margin profit margin of 3.4%, down 2.1 percentage points year on year. Since Tenable’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

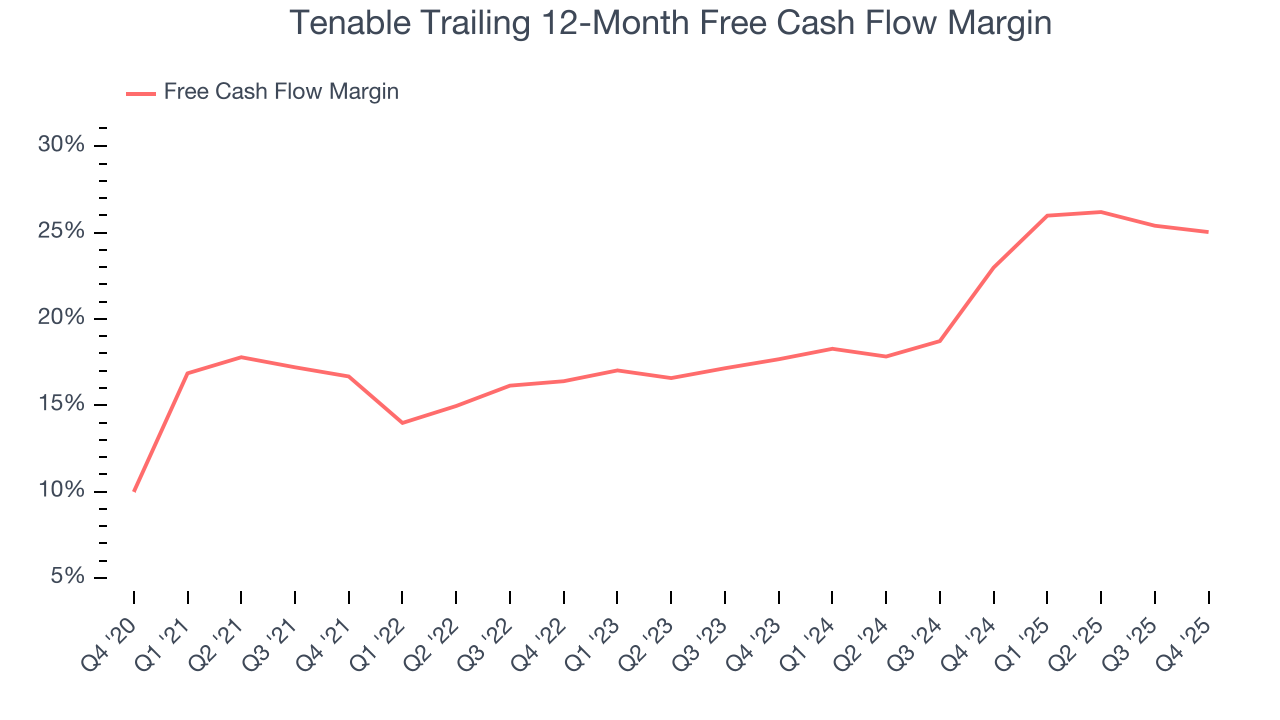

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Tenable has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors while maintaining a cash cushion. The company’s free cash flow margin averaged 25% over the last year, quite impressive for a software business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Tenable’s free cash flow clocked in at $80.9 million in Q4, equivalent to a 31.1% margin. The company’s cash profitability regressed as it was 2.2 percentage points lower than in the same quarter last year, but it’s still above its one-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

Over the next year, analysts predict Tenable’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 25% for the last 12 months will decrease to 23.5%.

11. Key Takeaways from Tenable’s Q4 Results

We were impressed by Tenable’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its full-year revenue guidance fell short of Wall Street’s estimates. Overall, we think this quarter was still solid. The stock traded up 5.8% to $20.87 immediately after reporting.

12. Is Now The Time To Buy Tenable?

Updated: February 4, 2026 at 9:19 PM EST

When considering an investment in Tenable, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Tenable isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its operating margin hasn't moved over the last year.

Tenable’s price-to-sales ratio based on the next 12 months is 2.2x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $34.37 on the company (compared to the current share price of $20.87).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.