Xerox (XRX)

Xerox is up against the odds. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Xerox Will Underperform

Pioneering the modern office copier and inventing technologies like Ethernet and the laser printer, Xerox (NASDAQ:XRX) provides document management systems, printing technology, and workplace solutions to businesses of all sizes across the globe.

- Sales were flat over the last five years, indicating it’s failed to expand this cycle

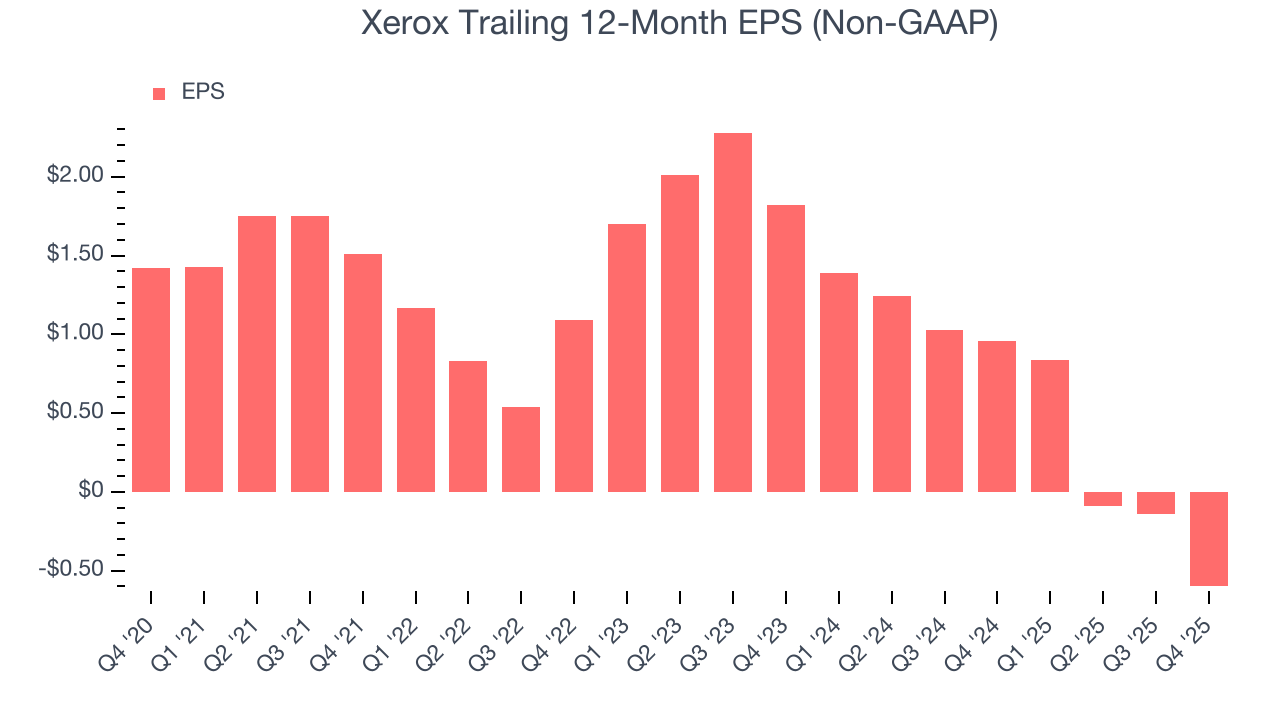

- Performance over the past five years shows each sale was less profitable, as its earnings per share fell by 19.4% annually

- High net-debt-to-EBITDA ratio of 8× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Xerox’s quality is insufficient. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Xerox

Xerox’s stock price of $1.40 implies a valuation ratio of 3.1x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Xerox (XRX) Research Report: Q4 CY2025 Update

Document technology company Xerox (NASDAQ:XRX) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 25.7% year on year to $2.03 billion. The company’s full-year revenue guidance of $7.5 billion at the midpoint came in 5.1% below analysts’ estimates. Its non-GAAP loss of $0.10 per share was significantly below analysts’ consensus estimates.

Xerox (XRX) Q4 CY2025 Highlights:

- Revenue: $2.03 billion vs analyst estimates of $2.05 billion (25.7% year-on-year growth, 0.9% miss)

- Adjusted EPS: -$0.10 vs analyst estimates of $0.10 (significant miss)

- Adjusted EBITDA: $58 million vs analyst estimates of $179.8 million (2.9% margin, 67.7% miss)

- Operating Margin: -3%, down from 2.1% in the same quarter last year

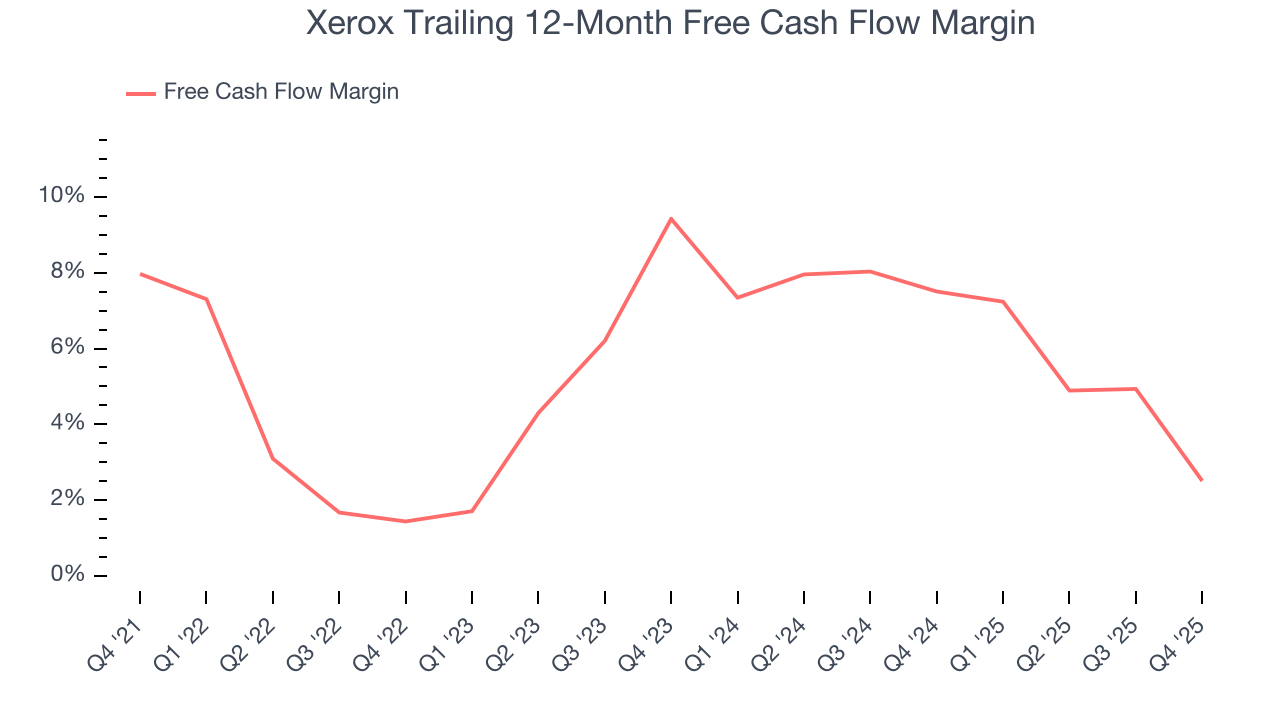

- Free Cash Flow Margin: 9.1%, down from 20.7% in the same quarter last year

- Market Capitalization: $298.3 million

Company Overview

Pioneering the modern office copier and inventing technologies like Ethernet and the laser printer, Xerox (NASDAQ:XRX) provides document management systems, printing technology, and workplace solutions to businesses of all sizes across the globe.

Xerox operates through two main segments: Print and Other, which encompasses document systems and IT services, and FITTLE, which provides financing solutions. The company's product portfolio is organized into several categories, including Workplace Solutions (desktop printers and multifunction devices), Production Solutions (high-volume printing equipment for commercial environments), and Xerox Services.

In the Workplace Solutions category, Xerox offers everything from small desktop printers to sophisticated multifunction devices with its ConnectKey software platform that enables digital workflow applications. The Production Solutions line targets graphic communications and in-plant printing operations with high-speed presses capable of handling variable data for personalized content.

Xerox Services represents the company's shift toward becoming a comprehensive technology provider rather than just a hardware manufacturer. Its Managed Print Services help organizations optimize their print infrastructure and secure their document environments. The company also offers Capture & Content Services for digitizing documents and automating workflows, Customer Engagement Services for personalized communications, and IT Services for small and mid-sized businesses.

A typical customer might be a large insurance company using Xerox's production printers to generate personalized policy documents, while also relying on Xerox's managed services to optimize their office printing fleet and digitize incoming mail. Xerox generates revenue through equipment sales, service contracts, supplies, and financing arrangements.

The company maintains manufacturing facilities in several locations, including its largest site in Webster, New York, where it produces high-end production printing equipment and consumables like toner.

4. Hardware & Infrastructure

The Hardware & Infrastructure sector will be buoyed by demand related to AI adoption, cloud computing expansion, and the need for more efficient data storage and processing solutions. Companies with tech offerings such as servers, switches, and storage solutions are well-positioned in our new hybrid working and IT world. On the other hand, headwinds include ongoing supply chain disruptions, rising component costs, and intensifying competition from cloud-native and hyperscale providers reducing reliance on traditional hardware. Additionally, regulatory scrutiny over data sovereignty, cybersecurity standards, and environmental sustainability in hardware manufacturing could increase compliance costs.

Xerox competes with several major players in the document technology and office equipment space, including Canon, HP Inc., Ricoh, Konica Minolta, and FUJIFILM Business Innovation Corp. (formerly Fuji Xerox).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

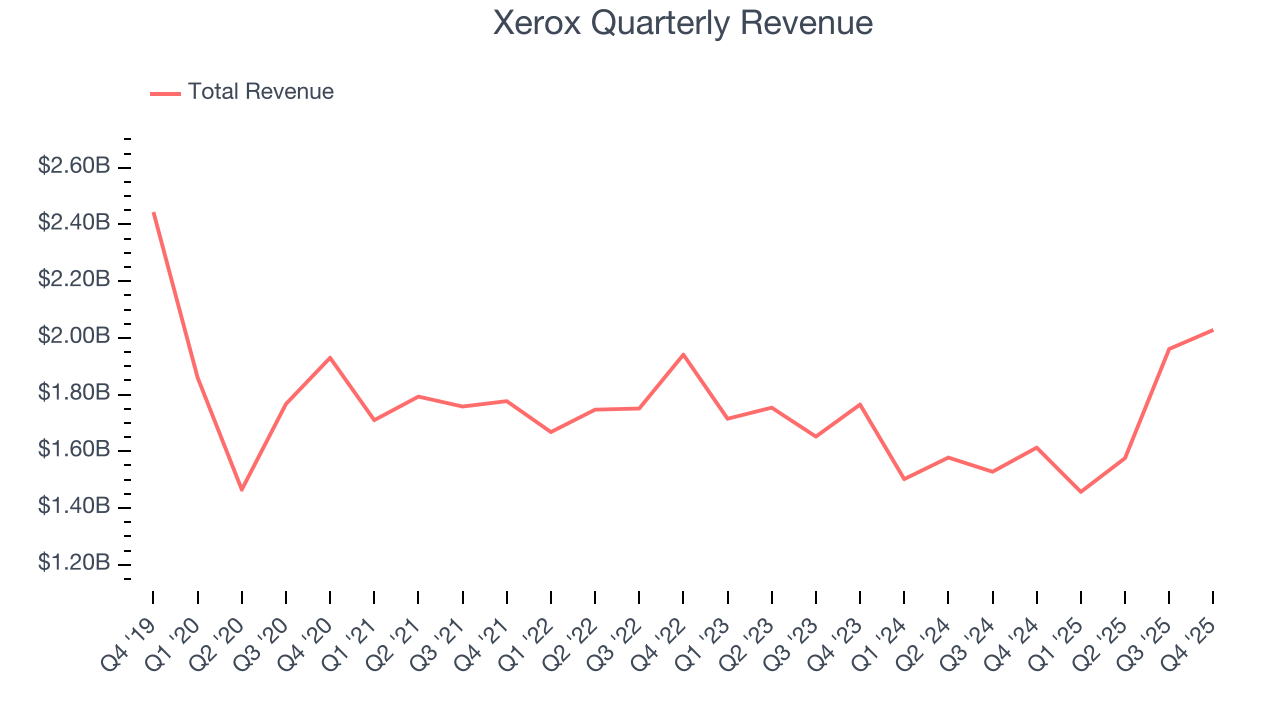

With $7.02 billion in revenue over the past 12 months, Xerox is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To accelerate sales, Xerox likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, Xerox struggled to increase demand as its $7.02 billion of sales for the trailing 12 months was close to its revenue five years ago. This shows demand was soft, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Just like its five-year trend, Xerox’s revenue over the last two years was flat, suggesting it is in a slump.

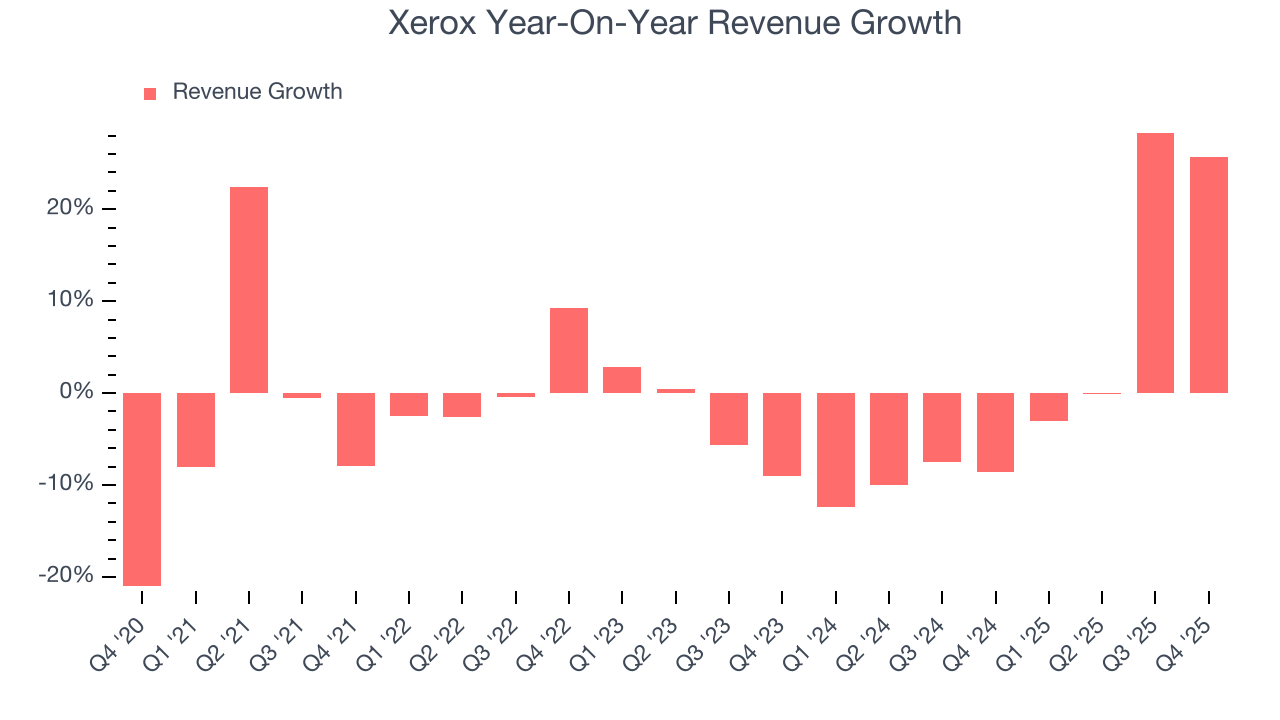

This quarter, Xerox generated an excellent 25.7% year-on-year revenue growth rate, but its $2.03 billion of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 12.1% over the next 12 months, an improvement versus the last two years. This projection is healthy and suggests its newer products and services will spur better top-line performance.

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

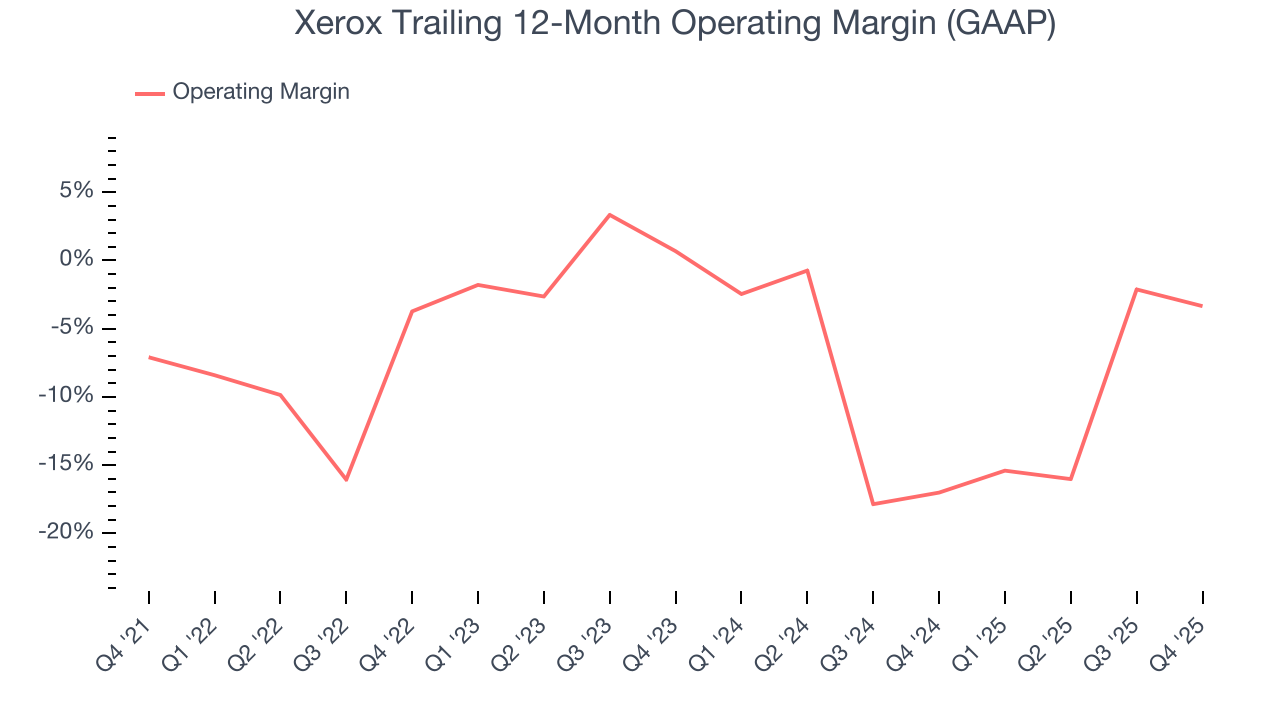

Xerox’s high expenses have contributed to an average operating margin of negative 5.9% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Xerox’s operating margin rose by 3.7 percentage points over the last five years. Still, it will take much more for the company to reach long-term profitability.

Xerox’s operating margin was negative 3% this quarter. The company's consistent lack of profits raise a flag.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Xerox, its EPS declined by 19.4% annually over the last five years while its revenue was flat. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Xerox, its two-year annual EPS declines of 52.6% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Xerox reported adjusted EPS of negative $0.10, down from $0.36 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Xerox’s full-year EPS of negative $0.60 will flip to positive $0.96.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Xerox has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.7% over the last five years, slightly better than the broader business services sector.

Taking a step back, we can see that Xerox’s margin dropped by 5.5 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Xerox’s free cash flow clocked in at $184 million in Q4, equivalent to a 9.1% margin. The company’s cash profitability regressed as it was 11.6 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

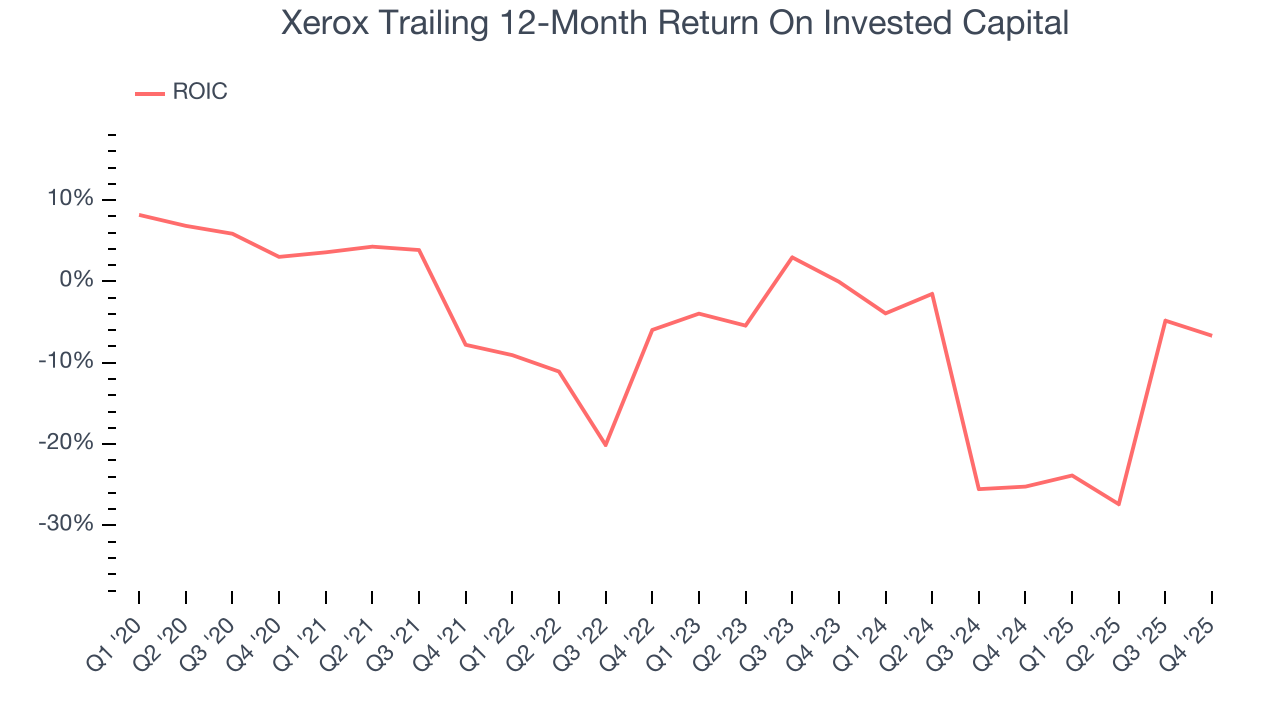

Xerox’s five-year average ROIC was negative 9.1%, meaning management lost money while trying to expand the business. Its returns were among the worst in the business services sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Xerox’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

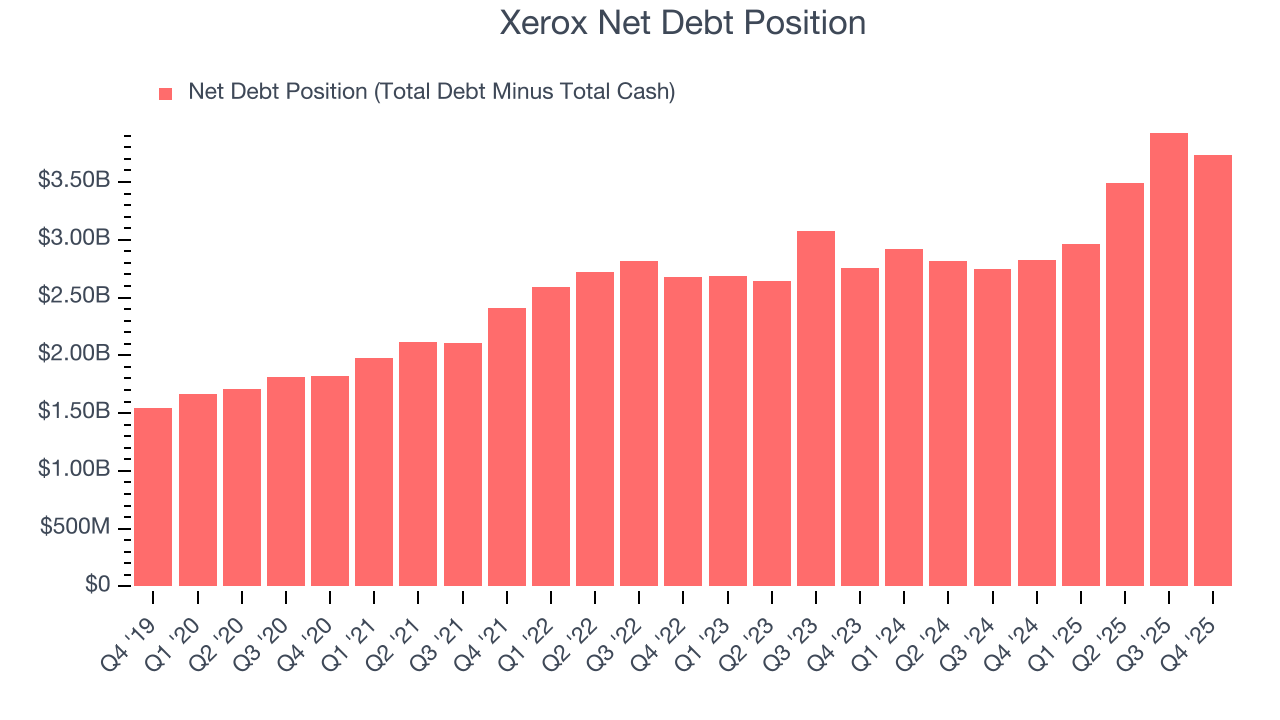

Xerox’s $4.25 billion of debt exceeds the $512 million of cash on its balance sheet. Furthermore, its 10× net-debt-to-EBITDA ratio (based on its EBITDA of $378 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Xerox could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Xerox can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Xerox’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.5% to $2.29 immediately following the results.

12. Is Now The Time To Buy Xerox?

Updated: March 29, 2026 at 12:39 AM EDT

Before making an investment decision, investors should account for Xerox’s business fundamentals and valuation in addition to what happened in the latest quarter.

Xerox falls short of our quality standards. To kick things off, its revenue growth was weak over the last five years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Xerox’s P/E ratio based on the next 12 months is 3.1x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $2.25 on the company (compared to the current share price of $1.40).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.