Atlas Energy Solutions (AESI)

Atlas Energy Solutions is up against the odds. It not only burned cash historically but also has been less efficient lately. No need to stick around here.― StockStory Analyst Team

1. News

2. Summary

Why We Think Atlas Energy Solutions Will Underperform

Building the world's first long-haul proppant conveyor system to reduce truck traffic, Atlas Energy Solutions (NYSE:AESI) mines and processes sand used as proppant to prop open fractures in oil and gas wells during hydraulic fracturing.

- Efficiency has decreased over the last five years as its EBITDA margin fell by 20.8 percentage points

- poor earning stability in the sector may keep investors up at night

- Cash burn makes us question whether it can achieve sustainable long-term growth

Atlas Energy Solutions is in the penalty box. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Atlas Energy Solutions

Atlas Energy Solutions’s stock price of $13.22 implies a valuation ratio of 10.9x forward EV-to-EBITDA. This multiple is higher than that of energy upstream and integrated energy peers; it’s also rich for the business quality. Not a great combination.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Atlas Energy Solutions (AESI) Research Report: Q4 CY2025 Update

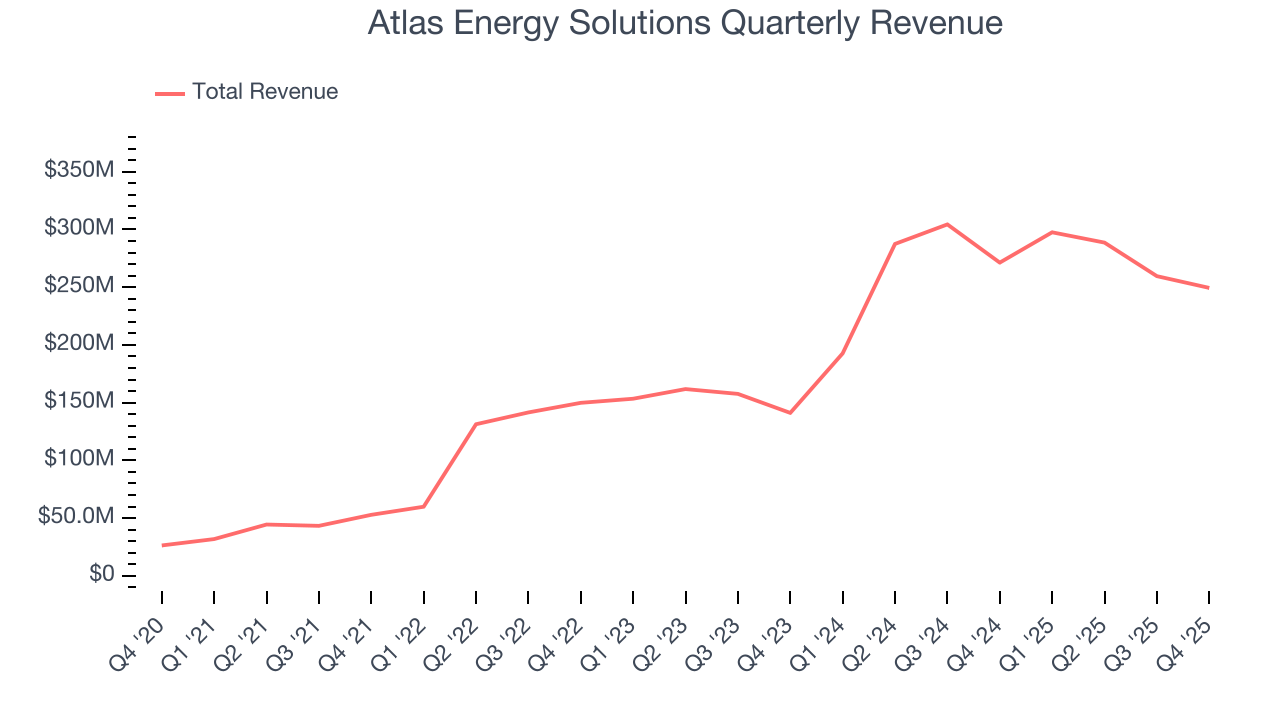

Proppant sand producer Atlas Energy Solutions (NYSE:AESI) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 8.1% year on year to $249.4 million. Its non-GAAP loss of $0.21 per share was 9.3% below analysts’ consensus estimates.

Atlas Energy Solutions (AESI) Q4 CY2025 Highlights:

- Revenue: $249.4 million vs analyst estimates of $240.1 million (8.1% year-on-year decline, 3.9% beat)

- Adjusted EPS: -$0.21 vs analyst expectations of -$0.19 (9.3% miss)

- Adjusted EBITDA: $36.74 million vs analyst estimates of $28.36 million (14.7% margin, 29.6% beat)

- Operating Margin: -6%, down from 11.3% in the same quarter last year

- Free Cash Flow was -$18.1 million compared to -$5.58 million in the same quarter last year

- Market Capitalization: $1.48 billion

Company Overview

Building the world's first long-haul proppant conveyor system to reduce truck traffic, Atlas Energy Solutions (NYSE:AESI) mines and processes sand used as proppant to prop open fractures in oil and gas wells during hydraulic fracturing.

The company operates three processing facilities on approximately 38,000 acres of land it owns or leases in Winkler and Ward counties in West Texas, placing it directly within the Permian Basin—one of the most prolific oil and gas producing regions in the United States. This location provides a competitive advantage by eliminating the need to transport sand from distant locations like Wisconsin or Illinois, reducing transportation costs and delivery times for oil and gas operators. The company controls more than 70% of the large open-dune acreage available for mining in the region, with sand deposits that produce the finer mesh sizes (40/70 and 100 mesh) currently preferred by the industry for well completion operations.

When an oil and gas company drills a well, it pumps a mixture of water, chemicals, and proppant sand into the rock formation at high pressure to create fractures. The sand grains hold these fractures open after the pressure is released, allowing oil and gas to flow from the rock into the well. For example, a drilling operator completing a horizontal well in the Delaware Basin might order several thousand tons of 40/70 mesh sand from Atlas Energy Solutions, which would be delivered directly from the nearby processing facility to the wellsite.

The company generates revenue through two channels: selling proppant at the mine gate to customers who arrange their own transportation, or providing an integrated mine-to-wellhead solution that includes transportation services using its own fleet of specialized trucks and trailers. The company also operates logistics services including portable silos and storage solutions at wellsites. Its customer base consists primarily of oil and gas exploration and production companies operating in the Delaware and Midland Basins, which together comprise the Permian Basin.

The company is constructing the Dune Express, a 42-mile electric conveyor system originating at its Kermit facilities and extending into the Northern Delaware Basin. This infrastructure project is designed to transport proppant from the mine to permanent and mobile loadout facilities near drilling activity, offering an alternative to truck transportation.

4. Oilfield Services

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

Atlas Energy Solutions competes with other proppant producers including U.S. Silica (NYSE:SLCA), Hi-Crush (NYSE:HCR), and private companies like Covia, High Roller Sand, Black Mountain Sand, Freedom Proppants, Alpine Silica, Badger Mining, Vista Proppants, and Capital Sand.

5. Revenue Scale

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks. Atlas Energy Solutions’s $1.1 billion of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night. is a small company in an industry where scale matters.

6. Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Over the last four years, Atlas Energy Solutions grew its sales at an incredible 58.8% compounded annual growth rate. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

This quarter, Atlas Energy Solutions’s revenue fell by 8.1% year on year to $249.4 million but beat Wall Street’s estimates by 3.9%.

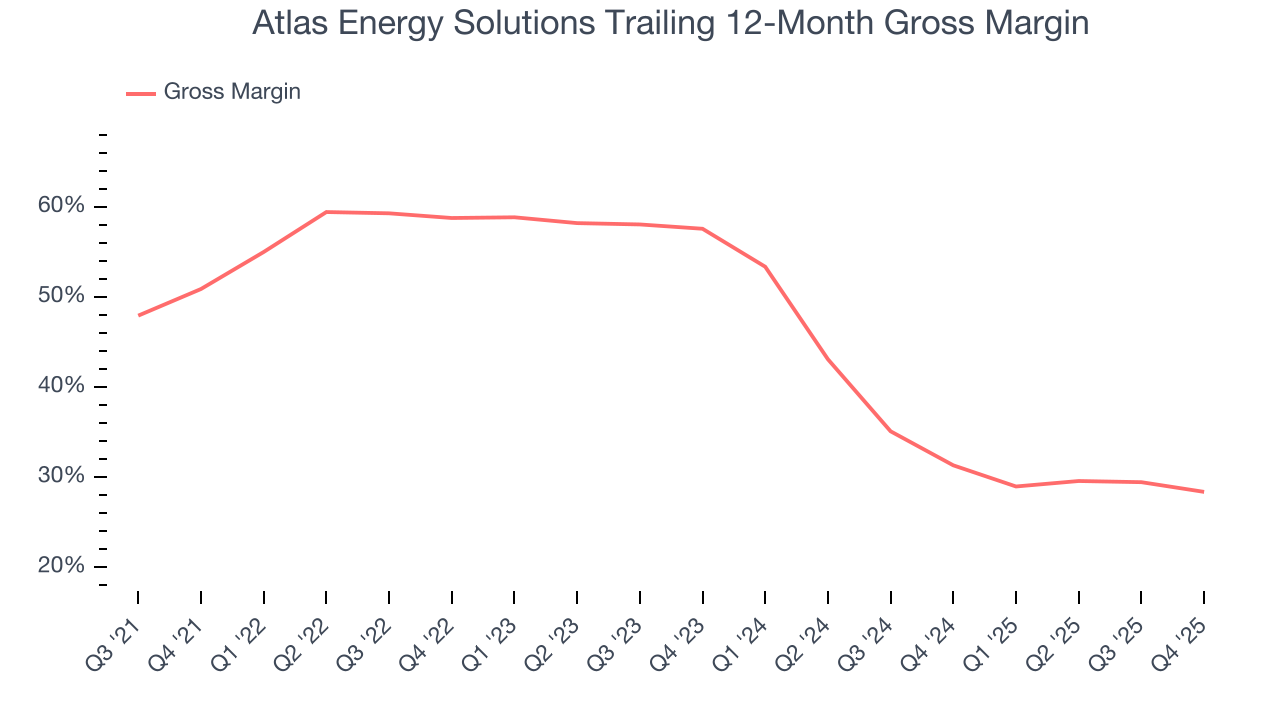

7. Gross Margin

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Atlas Energy Solutions, which averaged 40% gross margin over the last five years, exhibits poor unit economics in the sector. It means the company will struggle more at lower commodity prices than peers with better gross margins.

This quarter, Atlas Energy Solutions’s gross profit margin was 24.9% , marking a 4.7 percentage point decrease from 29.6% in the same quarter last year. Note that energy margins can be volatile due to commodity price changes.

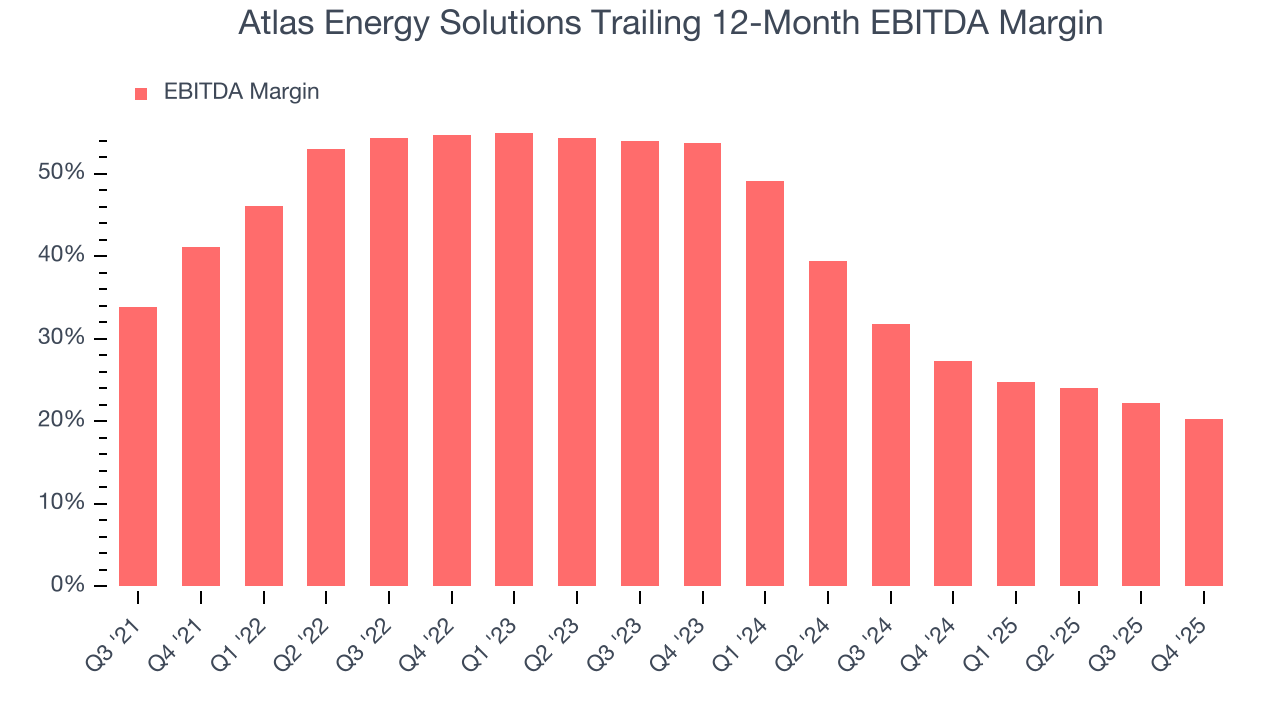

8. Adjusted EBITDA Margin

Atlas Energy Solutions has done a decent job managing its cost base over the last five years. The company has produced an average EBITDA margin of 34.3%, higher than the broader energy upstream and integrated energy sector.

Analyzing the trend in its profitability, Atlas Energy Solutions’s EBITDA margin decreased by 20.8 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Atlas Energy Solutions become more profitable in the future.

In Q4, Atlas Energy Solutions generated an EBITDA margin profit margin of 14.7%, down 8.6 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA beat Wall Street’s estimates by 29.6%.

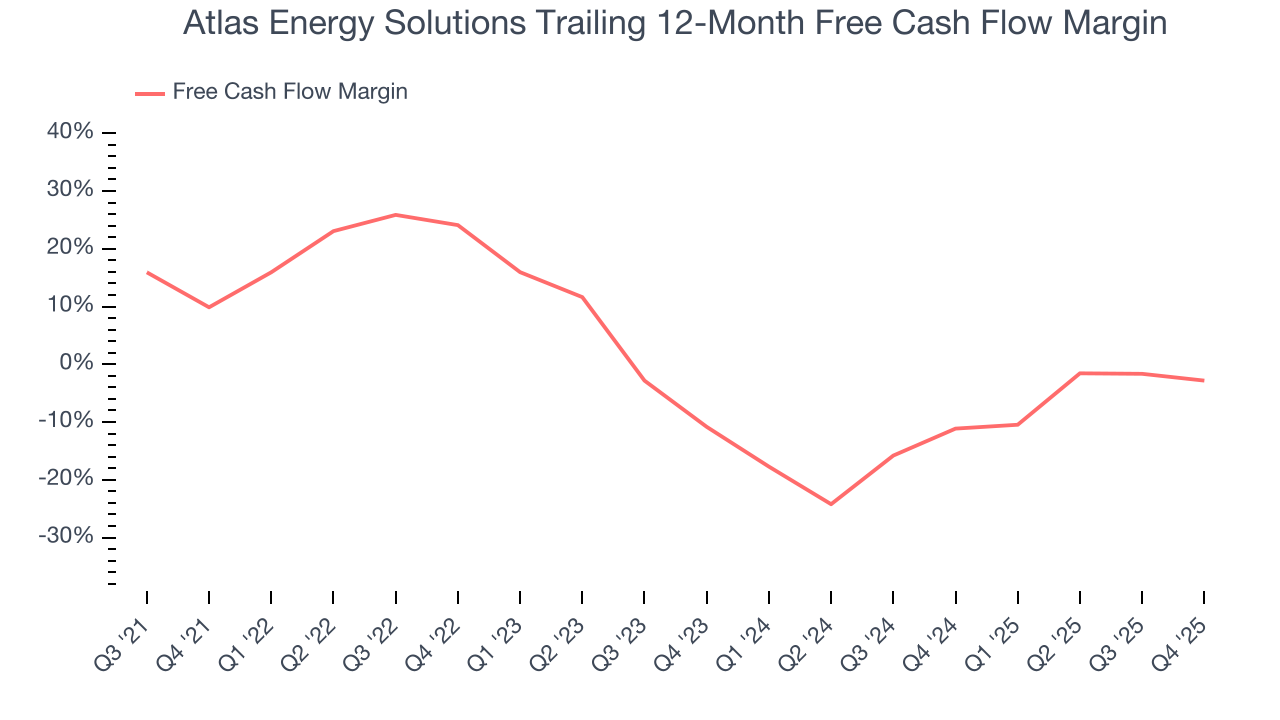

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Atlas Energy Solutions’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 2.4%. This means it lit $2.39 of cash on fire for every $100 in revenue.

While the level of free cash flow margins is important, their consistency matters just as much.

Atlas Energy Solutions’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 49.3 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Atlas Energy Solutions? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Atlas Energy Solutions burned through $18.1 million of cash in Q4, equivalent to a negative 7.3% margin. The company’s cash burn was similar to its $5.58 million of lost cash in the same quarter last year.

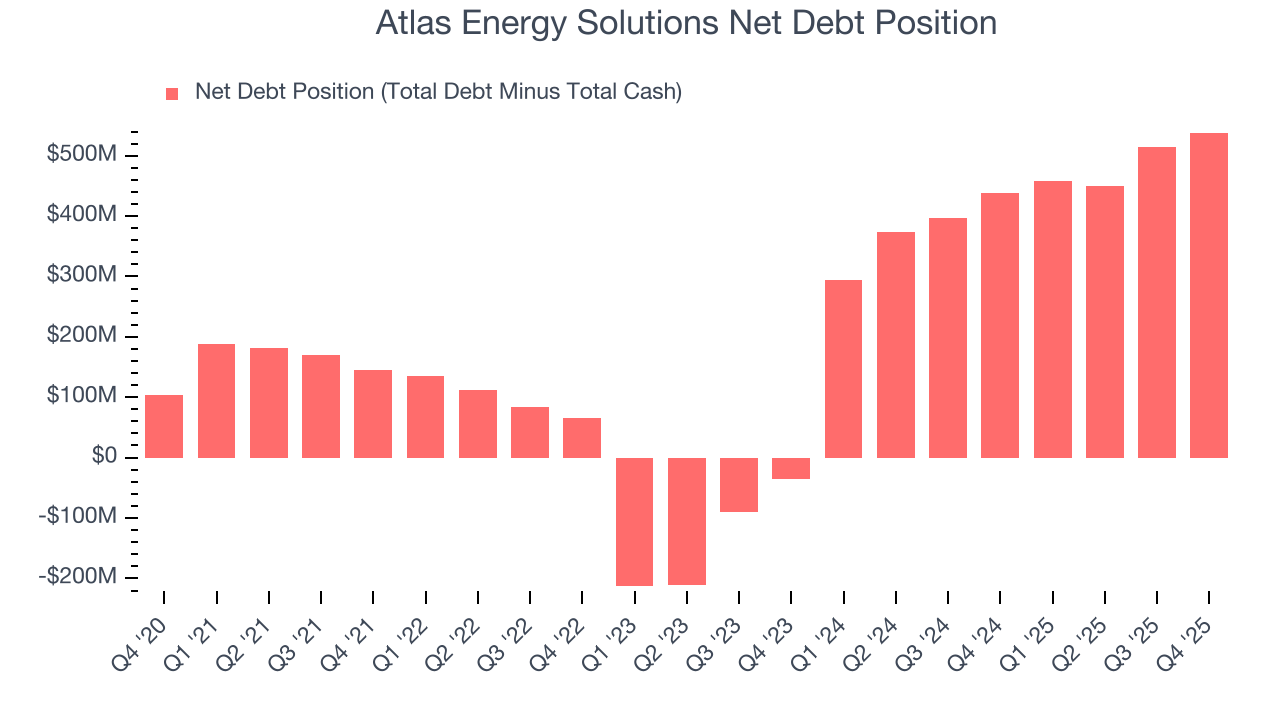

10. Balance Sheet Assessment

Atlas Energy Solutions reported $40.63 million of cash and $578.9 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $221.7 million of EBITDA over the last 12 months, we view Atlas Energy Solutions’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $58 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Atlas Energy Solutions’s Q4 Results

We were impressed by how significantly Atlas Energy Solutions blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this quarter featured some important positives. The stock traded up 1.1% to $12.03 immediately after reporting.

12. Is Now The Time To Buy Atlas Energy Solutions?

Updated: March 12, 2026 at 12:47 AM EDT

Before deciding whether to buy Atlas Energy Solutions or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Atlas Energy Solutions doesn’t pass our quality test. Although its revenue growth over the last four years was top-tier for the sector, it’s expected to deteriorate over the next 12 months and its volatility compared to commodity price volatility is bottom-tier in the sector, leading to highly volatile free cash flow. On top of that, the company’s declining EBITDA margin shows the business has become less efficient.

Atlas Energy Solutions’s EV-to-EBITDA ratio based on the next 12 months is 10.9x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $12.17 on the company (compared to the current share price of $13.22).