Borr Drilling (BORR)

We’re wary of Borr Drilling. Its weak returns on capital suggest it doesn’t generate sufficient profits, a sign of value destruction.― StockStory Analyst Team

1. News

2. Summary

Why Borr Drilling Is Not Exciting

Operating one of the world's youngest jack-up fleets with an average age under eight years, Borr Drilling (NYSE:BORR) operates jack-up rigs that drill oil and gas wells in shallow waters up to 400 feet deep for exploration and production companies.

- Cash-burning history makes us doubt the long-term viability of its business model

- Low returns on capital reflect management’s struggle to allocate funds effectively

- A positive is that its impressive 34.2% annual revenue growth over the last seven years indicates it’s winning market share this cycle

Borr Drilling is in the penalty box. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Borr Drilling

Borr Drilling is trading at $5.04 per share, or 7.5x forward EV-to-EBITDA. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Borr Drilling (BORR) Research Report: Q4 CY2025 Update

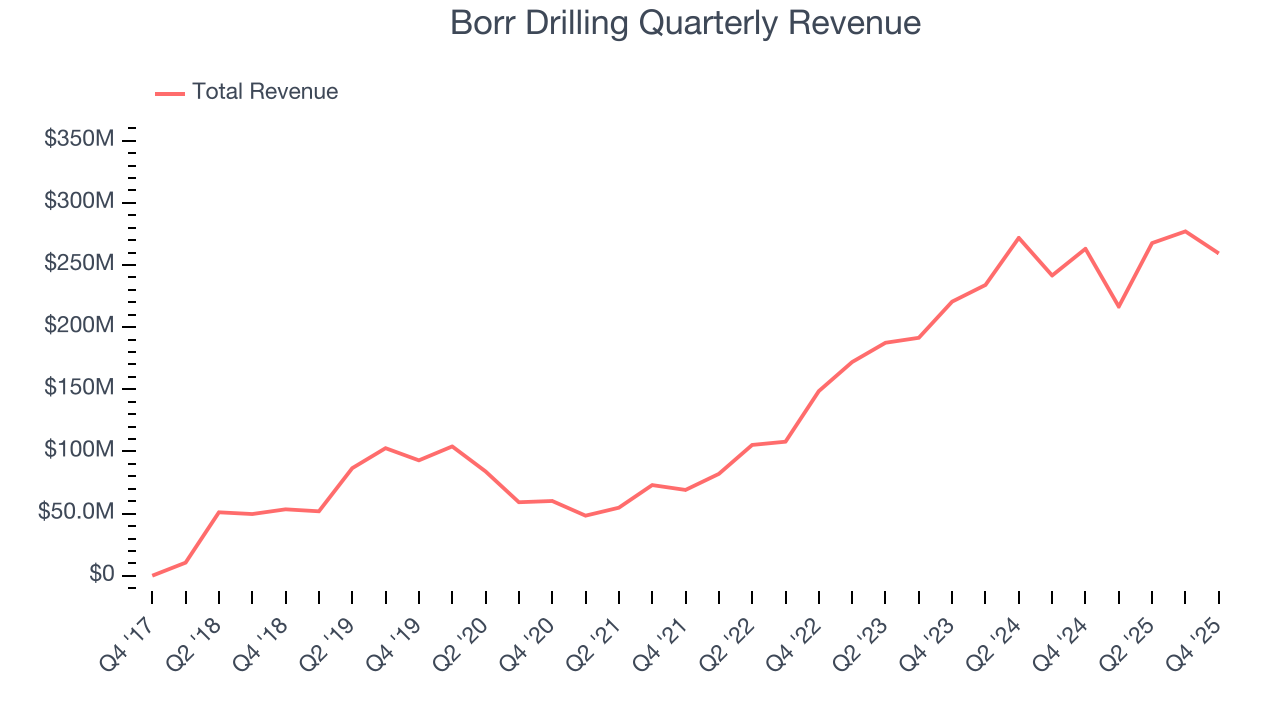

Offshore drilling contractor Borr Drilling (NYSE:BORR) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 1.4% year on year to $259.4 million. Its non-GAAP loss of $0 per share was $0.02 above analysts’ consensus estimates.

Borr Drilling (BORR) Q4 CY2025 Highlights:

- Revenue: $259.4 million vs analyst estimates of $240.1 million (1.4% year-on-year decline, 8.1% beat)

- Adjusted EPS: $0 vs analyst estimates of -$0.03 ($0.02 beat)

- Adjusted EBITDA: $107.9 million vs analyst estimates of $99.15 million (41.6% margin, 8.8% beat)

- Operating Margin: 25.9%, down from 38.5% in the same quarter last year

- Free Cash Flow was -$17.3 million compared to -$194 million in the same quarter last year

- Market Capitalization: $1.68 billion

Company Overview

Operating one of the world's youngest jack-up fleets with an average age under eight years, Borr Drilling (NYSE:BORR) operates jack-up rigs that drill oil and gas wells in shallow waters up to 400 feet deep for exploration and production companies.

The company specializes in jack-up rigs, which are mobile offshore platforms with legs that can be lowered to the seabed to elevate the drilling platform above the water surface. These rigs feature independent leg cantilever designs, allowing the drilling equipment to extend over the wellhead location. Jack-up rigs are particularly suited for shallow-water operations in continental shelf areas where water depths don't exceed approximately 400 feet.

Borr Drilling's fleet consists of 24 premium jack-up rigs, with nearly all built after 2013. The company defines premium rigs as those constructed in 2000 or later with modern capabilities. When an oil company like Saudi Aramco or ENI discovers oil reserves in shallow waters or needs to develop existing fields, they contract Borr Drilling's rigs on a dayrate basis—essentially paying a daily fee for the rig, equipment, and crew. These contracts typically cover either drilling a single well, multiple wells, or a specified time period ranging from a few months to several years.

The company operates across major oil-producing regions, including the Middle East, South East Asia, West Africa, Latin America, and the North Sea. While jack-up rigs can drill exploratory wells searching for new oil and gas deposits, the majority of current activity involves development drilling—drilling additional production wells in areas where hydrocarbons have already been discovered. Borr Drilling's customers include integrated oil majors, state-owned national oil companies like Saudi Aramco and Pemex, and independent exploration and production companies. The company also participates in joint ventures, notably in Mexico, where it provides drilling services and rig management through partnership arrangements.

4. Oilfield Services

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

Borr Drilling's competitors in the jack-up drilling market include Valaris (NYSE:VAL), Shelf Drilling, Noble Corporation (NYSE:NE), and ADES, along with regional operators like Velesto Energy in Malaysia.

5. Revenue Scale

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program. Borr Drilling’s $1.02 billion of revenue in the last year is pretty small for the industry, suggesting the company is subscale business in an industry where scale matters.

6. Revenue Growth

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Thankfully, Borr Drilling’s 27.1% annualized revenue growth over the last five years was incredible. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Even a long stretch in Energy can be shaped by a single commodity cycle, so extending the view to ten years adds another perspective and reveals which companies are built to grow regardless of the pricing regime. Borr Drilling’s annualized revenue growth of 34.2% over the last seven years is above its five-year trend.

This quarter, Borr Drilling’s revenue fell by 1.4% year on year to $259.4 million but beat Wall Street’s estimates by 8.1%.

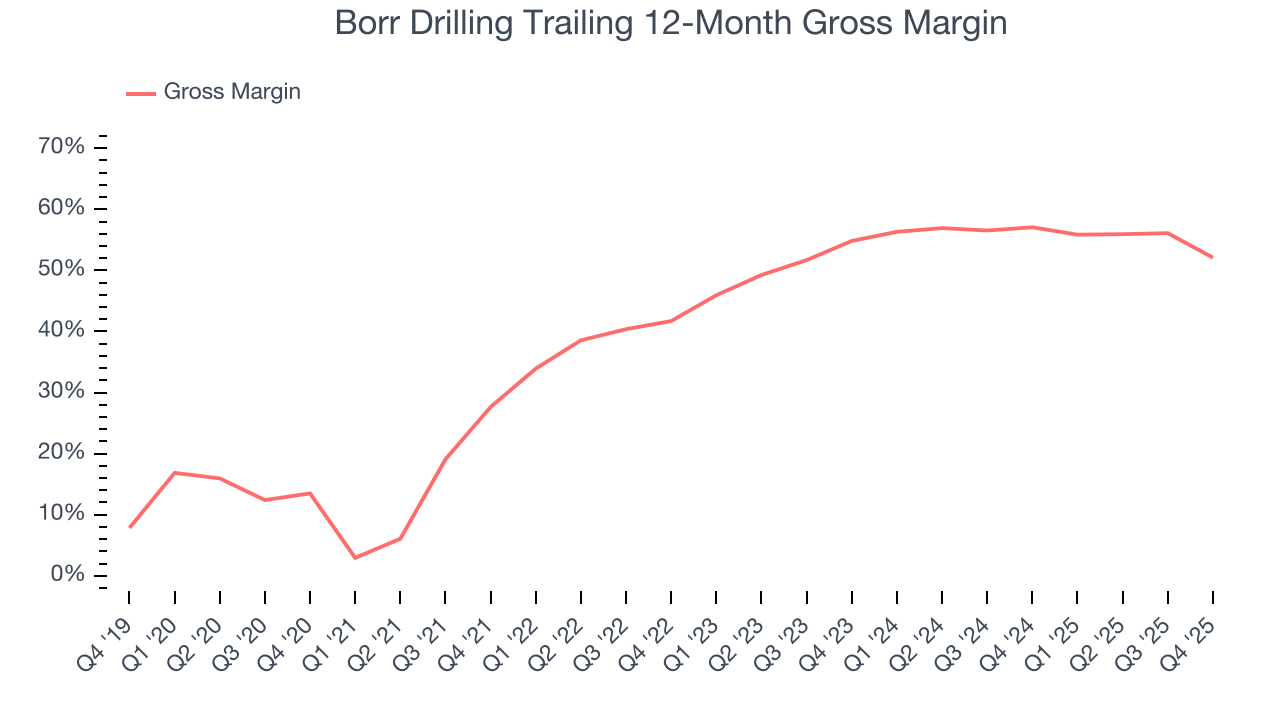

7. Gross Margin

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Borr Drilling, which averaged 51.1% gross margin over the last five years, exhibits decent unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an reasonable starting point for ultimate operating profits and free cash flow generation.

This quarter, Borr Drilling’s gross profit margin was 46% , marking a 15.7 percentage point decrease from 61.6% in the same quarter last year. Note that energy margins can be volatile due to commodity price changes.

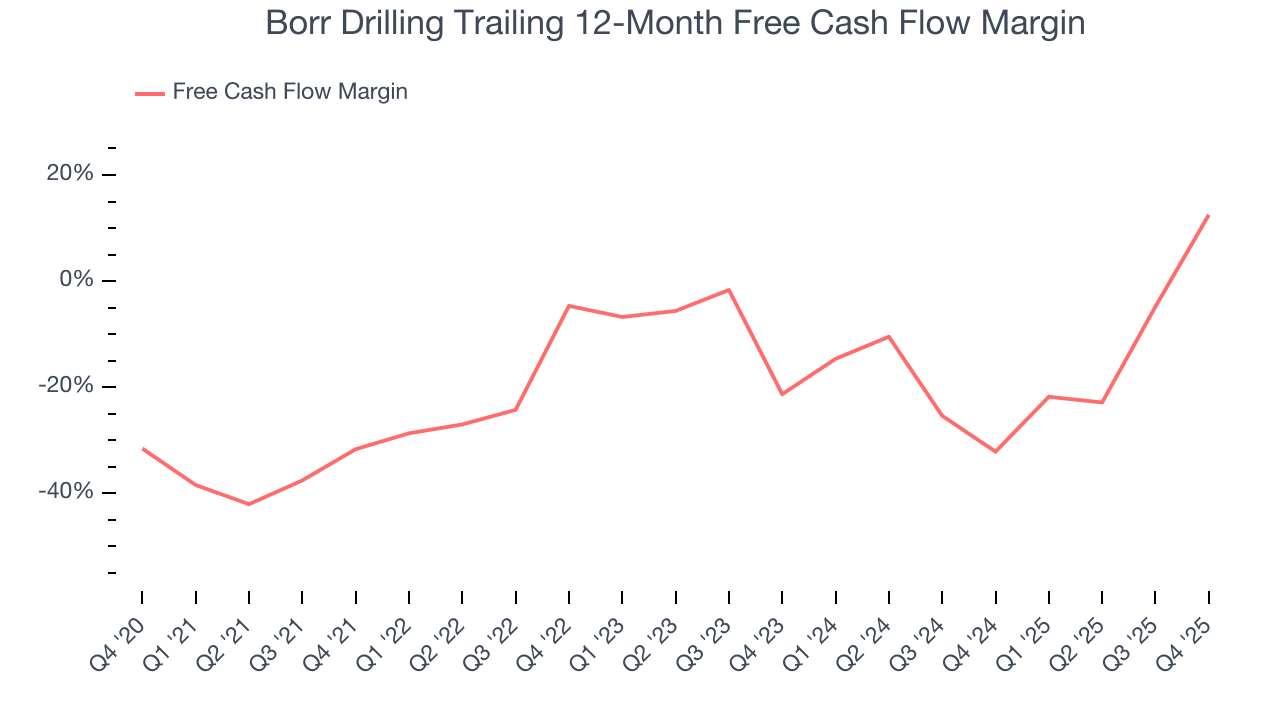

8. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

Borr Drilling’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 13.2%, meaning it lit $13.20 of cash on fire for every $100 in revenue.

Absolute FCF margin levels matter but so does stability of free cash flow. All else equal, we’d prefer a 25.0% average free cash flow margin that is quite steady no matter how commodity prices behave rather than extremely high margins when times are good and negative ones when they’re tough.

Borr Drilling’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 17.6 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Borr Drilling? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Borr Drilling burned through $17.3 million of cash in Q4, equivalent to a negative 6.7% margin. The company’s cash burn slowed from $194 million of lost cash in the same quarter last year.

9. Return on Invested Capital (ROIC)

Free cash flow tells investors how much money an Energy producer made, and ROIC takes this one step further by telling investors how well and effectively the business made it. ROIC illustrates how much operating profit a producer generated relative to the money it has raised (debt and equity).

We at StockStory like to look at ROIC over a ten-year period because energy investment cycles can involve up to five years of ramping production and another five years of harvesting. A decade view captures buying, extracting, and monetizing rather than just part of that picture. Borr Drilling historically did a mediocre job investing in profitable growth initiatives. Its seven-year average ROIC was 2.5%, lower than the typical cost of capital (how much it costs to raise money) for energy upstream and integrated energy companies.

10. Key Takeaways from Borr Drilling’s Q4 Results

It was good to see Borr Drilling beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock remained flat at $5.48 immediately following the results.

11. Is Now The Time To Buy Borr Drilling?

Updated: March 15, 2026 at 1:11 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Borr Drilling, you should also grasp the company’s longer-term business quality and valuation.

Borr Drilling isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth over the last five years was top-tier for the sector, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s revenue growth over the last seven years was top-tier for the sector, the downside is its cash burn raises the question of whether it can sustainably maintain growth.

Borr Drilling’s EV-to-EBITDA ratio based on the next 12 months is 7.5x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $5.84 on the company (compared to the current share price of $5.04).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.